- Medical Devices

- Urinary Drainage Bags Market

Urinary Drainage Bags Market Size, Trends Share, Growth, and Regional Forecast, 2026 to 2033

Urinary Drainage Bags Market by Product (Large Bags and Leg Bags), by Usage (Reusable and Disposable), by Capacity (0-500 ml, 500-1000 ml, and 1000-2000 ml) by End-user (Hospital, Specialty Clinics, Ambulatory Surgery Centers, and Others), and Regional Analysis from 2026 to 2033

Urinary Drainage Bags Market Share and Trends Analysis

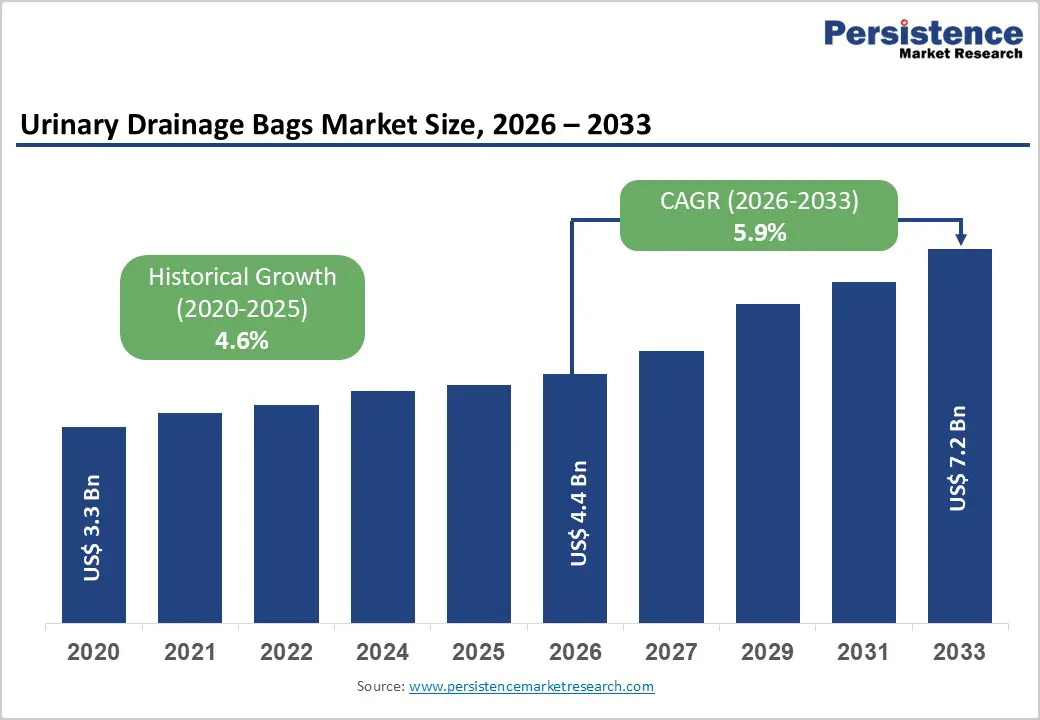

The global urinary drainage bags market size is estimated to grow from US$ 4.4 billion in 2026 to US$7.2 billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033.

Global demand for urinary drainage bags is rising steadily, driven by the increasing prevalence of urological disorders, urinary incontinence, benign prostatic hyperplasia, post-surgical urinary retention, and chronic conditions requiring long-term catheterization. Rising volumes of surgical procedures, trauma admissions, and intensive care cases are expanding the patient pool requiring continuous urine output management across hospitals and long-term care facilities.

Key Industry Highlights

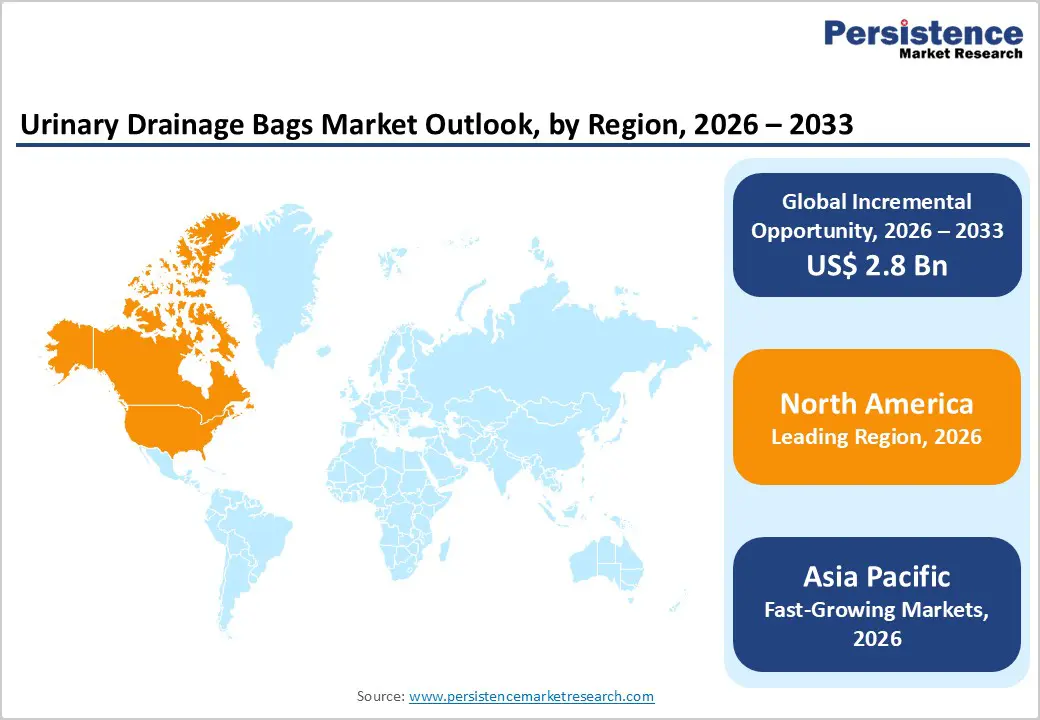

- Leading Region: North America holds the largest market share at 48.5%, supported by advanced healthcare infrastructure, high diagnosis rates of urological conditions, strong reimbursement frameworks, and widespread adoption of infection-control urinary drainage systems.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace due to a large patient pool, rising surgical volumes, rapid expansion of hospital and long-term care facilities, and increasing government investment in healthcare infrastructure.

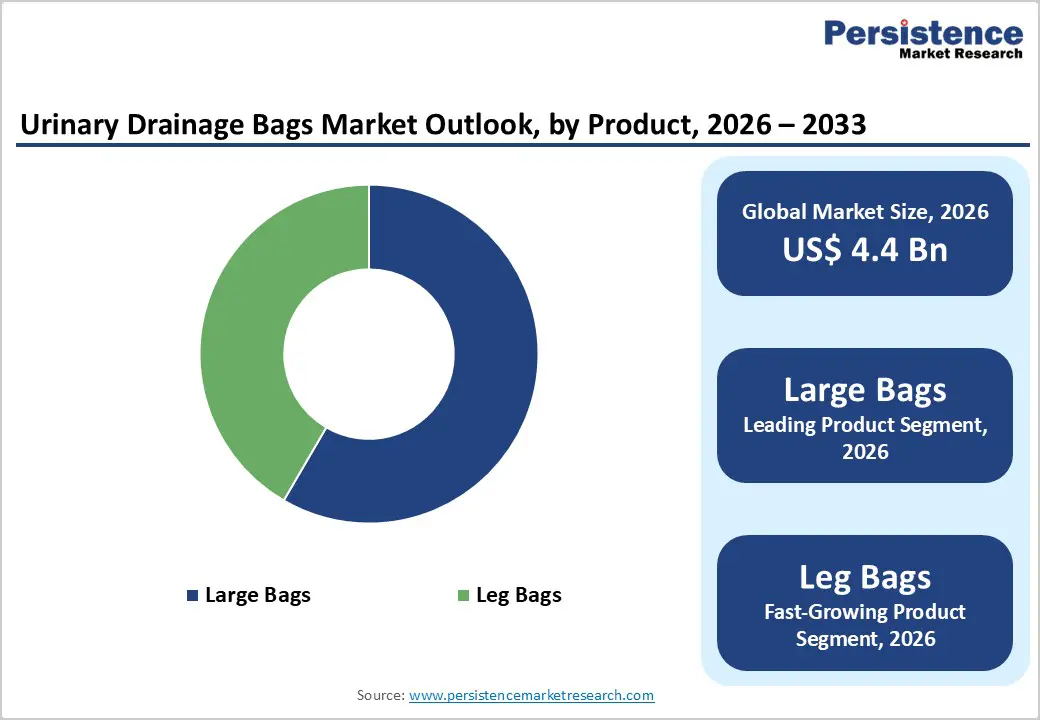

- Leading Product Segment: Large bags dominate the market due to their high capacity, suitability for continuous urine output monitoring, and widespread use across hospitals, intensive care units, and post-operative care settings.

- Fastest-Growing Product Segment: Leg bags are experiencing rapid growth as demand for mobile, discreet urinary management solutions in homecare and ambulatory settings increases.

- Leading Usage Segment: Reusable remains the largest usage segment due to cost-effectiveness and extensive adoption in hospitals and long-term care facilities for prolonged catheterization.

- Fastest-Growing Usage Segment: Disposable products are expanding rapidly, driven by rising focus on infection prevention, improved hygiene standards, and increasing adoption in home healthcare

| Key Insights | Details |

|---|---|

| Urinary Drainage Bags Market Size (2026E) | US$ 4.4 Bn |

| Market Value Forecast (2033F) | US$ 7.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Dynamics

Driver - Rising Prevalence of Urological Disorders and Expanding Use of Catheterization Driving Market Growth

The growing global burden of urological disorders is a key driver supporting sustained growth of the urinary drainage bags market. Increasing incidence of urinary incontinence, benign prostatic hyperplasia (BPH), urinary retention, bladder dysfunction, chronic kidney disease, and post-surgical urinary complications is expanding the patient population requiring short-term and long-term catheterization. Aging demographics in developed and developing regions are particularly vulnerable to age-related bladder control issues, driving continuous demand for drainage bags across hospital, outpatient, and homecare settings.

Additionally, rising volumes of surgical procedures, trauma cases, and intensive care admissions are increasing the routine use of urinary catheters, directly supporting demand for compatible drainage bags. The growing shift toward home-based care and long-term care facilities is further accelerating the adoption of leg bags and disposable systems designed for mobility and infection control. Product innovations such as anti-reflux valves, improved tubing materials, odor-control mechanisms, and enhanced comfort features are improving patient compliance and safety. Together, increasing clinical need, expanding geriatric populations, and steady product improvements are driving consistent growth in the global urinary drainage bags market.

Restraints - Infection Risks, Cost Pressures, and Reimbursement Challenges Limiting Market Expansion

Despite strong demand fundamentals, the urinary drainage bags market faces several restraints that moderate its growth potential. Catheter-associated urinary tract infections (CAUTIs) remain a major clinical concern, often leading to stricter usage protocols, shorter catheterization durations, and preference for alternative management strategies where feasible. Hospitals and care facilities are under increasing regulatory pressure to reduce infection rates, which can limit prolonged or unnecessary use of drainage systems.

Cost sensitivity also acts as a barrier, particularly in low- and middle-income regions where reimbursement coverage for consumables such as drainage bags is limited or inconsistent. Disposable drainage bags, while preferred for infection control, increase recurring costs for healthcare providers and patients relying on out-of-pocket spending. In homecare settings, affordability often drives reuse beyond recommended durations, raising safety concerns. Additionally, limited patient education on proper handling and maintenance can lead to complications, reducing confidence in long-term use. Fragmented procurement systems, pricing pressure from bulk purchasing organizations, and competition from low-cost local manufacturers further constrain margins. These clinical, economic, and structural challenges continue to restrict faster market penetration despite rising demand.

Opportunity - Growth of Home Healthcare, Disposable Products, and Advanced Drainage Solutions, Creating New Growth Avenues

The expansion of preventive care and outpatient orthopedic services presents a significant growth opportunity for the global orthopedic braces and supports market. Healthcare systems worldwide are increasingly emphasizing early intervention, injury prevention, and non-surgical treatment pathways to reduce long-term costs and improve patient quality of life. This shift is driving increased prescription of braces for preventive use among aging populations, athletes, and individuals with early-stage The expanding home healthcare and long-term care segments present a significant opportunity for the urinary drainage bags market. Healthcare systems worldwide are shifting care delivery away from acute hospital settings toward home- and outpatient-based models to reduce costs and improve patient comfort. This trend is driving increased demand for leg bags, lightweight systems, and discreet drainage solutions that support mobility and independent living.

The rising preference for disposable urinary drainage bags, driven by improved infection control and ease of use, is opening new revenue streams, particularly in developed markets with strong regulatory standards. Technological advancements, including antimicrobial materials, closed drainage systems, improved valve designs, and enhanced ergonomics, are improving safety and patient outcomes. Customizable capacity options and gender-specific designs are further expanding adoption across diverse patient groups. E-commerce platforms and direct-to-consumer distribution channels are improving product accessibility and awareness, especially for patients with chronic conditions. In emerging economies, rising healthcare expenditure, an expanding elderly population, and increasing diagnosis rates of urological conditions are expected to support long-term demand. These trends collectively position homecare expansion and product innovation as key growth drivers for the market.

Category-wise Analysis

By Product, Large Capacity and Standard Urinary Drainage Bags Lead Due to High Clinical Utilization

The product segment is projected to dominate the global urinary drainage bags market in 2026, accounting for a revenue share of 58.4%. Segment leadership is primarily driven by the widespread use of standard and large-capacity urinary drainage bags across acute care hospitals, post-operative settings, and long-term care facilities. These products are essential for managing urinary retention, post-surgical recovery, and critically ill patients requiring continuous urine output monitoring. Urinary drainage bags offer reliable fluid collection, ease of monitoring, and compatibility with commonly used Foley and suprapubic catheters, making them indispensable in routine clinical workflows. High physician familiarity, standardized procurement protocols, and strong integration into hospital infection-control practices further support adoption. Continuous improvements in bag materials, anti-reflux valve systems, odor control mechanisms, and graduated volume markings are enhancing safety and usability. The availability of multiple capacity options and closed drainage systems also supports usage across diverse care settings, reinforcing the dominance of this product category within the overall market.

By Usage, Reusable Segment Leads Driven by Cost Efficiency and Long-Term Care

The reusable segment is projected to dominate the global urinary drainage bags market in 2026, accounting for a revenue share of 45.0%. This leadership is primarily driven by its cost-effectiveness and suitability for long-term and repeated use, particularly in hospitals, long-term care facilities, and homecare settings. Reusable urinary drainage bags are widely adopted for patients requiring extended catheterization, where durability and lower replacement frequency help reduce overall treatment costs. Growing geriatric populations and rising prevalence of chronic urological conditions are increasing the demand for long-term urinary management solutions, further supporting adoption of reusable products. In resource-constrained healthcare systems, reusable bags remain a preferred option due to budget limitations and inconsistent reimbursement for disposables. Improvements in material quality, cleaning protocols, and valve mechanisms have enhanced product safety and usability, improving clinician and patient confidence. Additionally, increased emphasis on sustainable healthcare practices is encouraging reuse where infection risks can be effectively managed. These factors collectively continue to support the dominance of the reusable segment within the urinary drainage bags market.

By End-user, Hospitals Dominate Driven by High Patient Volume and Critical Care Demand

The end-user segment is projected to dominate the global urinary drainage bags market in 2026, accounting for 44.6% of revenue. Hospitals represent the largest demand center due to high volumes of surgical procedures, trauma cases, intensive care admissions, and patients requiring prolonged catheterization. These settings rely heavily on urinary drainage bags for accurate fluid balance monitoring, infection control, and post-operative care. Hospitals benefit from centralized procurement, standardized usage protocols, and access to trained clinical staff, ensuring consistent utilization of drainage systems. The presence of intensive care units, emergency departments, and specialized surgical wards further strengthens demand. While specialty clinics and ambulatory surgery centers are increasing usage for short-term procedures, hospitals remain dominant due to their role in managing complex and high-acuity cases. Ongoing investments in infection prevention programs and patient safety initiatives continue to reinforce hospital leadership in the market.

Regional Insights

North America Urinary Drainage Bags Market Trends

The North America urinary drainage bags market is expected to dominate globally with a value share of 48.5% in 2026, led primarily by the United States. The region benefits from a highly developed healthcare infrastructure, advanced hospital systems, and strong adherence to infection-control protocols. High prevalence of chronic urological conditions, including urinary incontinence, prostate disorders, and post-surgical complications, continues to drive consistent demand for urinary drainage solutions. A rapidly aging population and high rates of hospital admissions further support sustained utilization across acute and long-term care settings.

North America also demonstrates strong adoption of disposable and closed drainage systems due to stringent regulatory standards aimed at reducing catheter-associated urinary tract infections. The presence of leading medical device manufacturers, robust clinical training programs, and widespread availability through hospitals, home care providers, and retail channels strengthens regional leadership. Additionally, growing emphasis on home healthcare and post-acute care management continues to expand demand beyond traditional hospital environments.

Europe Urinary Drainage Bags Market Trends

The Europe urinary drainage bags market is expected to grow steadily, supported by an aging population and rising prevalence of chronic urological and post-surgical conditions. Countries such as Germany, the U.K., France, Italy, and the Nordic nations are key contributors due to well-established public healthcare systems and strong access to hospital and long-term care services. European healthcare systems place significant emphasis on patient safety, infection prevention, and cost-effective care delivery, supporting the adoption of standardized urinary drainage solutions.

Increasing use of disposable drainage bags and closed systems aligns with regional infection-control guidelines. Growth in outpatient procedures, rehabilitation centers, and elderly care facilities is further expanding demand. Additionally, strong regulatory oversight, focus on product quality, and preference for clinically validated devices are driving consistent procurement. Investments in homecare services and chronic disease management are expected to support stable, long-term market expansion across the region.

Asia Pacific Urinary Drainage Bags Market Trends

The Asia Pacific urinary drainage bags market is expected to register a relatively high CAGR of around 7.9% between 2026 and 2033, driven by rapid development of healthcare infrastructure and rising awareness of urological health. Countries including China, India, Japan, South Korea, and Southeast Asian nations are witnessing increasing diagnosis rates of urinary disorders, supported by improving access to hospitals and diagnostic services. Expanding geriatric populations, rising surgical volumes, and growing prevalence of chronic diseases are significantly increasing demand for urinary drainage solutions.

Government investments in healthcare modernization, hospital expansion, and infection prevention programs are accelerating adoption. The region is also seeing growth in private hospitals, medical tourism, and homecare services, improving product availability across urban and semi-urban areas. Increasing affordability of disposable drainage bags and rising patient awareness of hygiene and safety are expected to sustain strong long-term growth across the Asia Pacific.

Competitive Landscape

The global urinary drainage bags market is highly competitive, with strong participation from companies such as ConvaTec, Inc., Cardinal Health, Teleflex, Inc., Coloplast, and BD. These players benefit from broad urinary care portfolios encompassing leg bags, large-capacity drainage bags, closed drainage systems, and catheter-compatible accessories, along with long-standing relationships with hospitals, urologists, and long-term care providers. Their competitive positioning is further strengthened by advanced manufacturing capabilities, adherence to infection-control standards, and well-established global distribution networks spanning acute care, home care, and institutional settings.

Competitive strategies are primarily focused on expanding disposable and reusable drainage bag offerings, enhancing infection prevention through anti-reflux valves and closed systems, improving patient comfort and mobility, and supporting effective urine output monitoring in both acute and long-term care pathways. Companies are also investing in product line extensions, clinical validation, and education programs for healthcare professionals and caregivers to ensure proper usage and compliance. Geographic expansion across emerging markets, coupled with continuous innovation in materials, ergonomics, odor control, and sustainability-focused designs, is intensifying competition and supporting the ongoing evolution of the urinary drainage bags market.

Key Developments:

- In November 2025, BD (Becton, Dickinson and Company), a leading global medical technology company, introduced the PureWick™ Portable Collection System, a discreet, first-of-its-kind, battery-powered personal urine management device designed specifically for wheelchair users to enhance mobility and independence both within and outside the home.

- On 4 June 2025, King George’s Medical University (KGMU) was granted a design registration patent for a newly developed IFT uro bag connector, a device that enables standard adult urinary drainage bags to be connected to infant feeding tubes, facilitating safer and more sterile urine collection in infants, particularly in resource-constrained healthcare settings.

Companies Covered in Urinary Drainage Bags Market

- ConvaTec, Inc.

- Cardinal Health

- Teleflex, Inc.

- Coloplast

- BD

- McKesson Medical Surgical, Inc.

- Amsino International, Inc.

- Flexicare Medical Ltd.

- Medline Industries, Inc.

- Manfred Sauer GmbH

- Coloplast

- B. Braun SE

- Hollister

- Others

Frequently Asked Questions

The global urinary drainage bags market is projected to be valued at US$ 4.4 Bn in 2026.

Rising prevalence of urological disorders, aging populations, increasing surgical volumes, and growing demand for long-term catheterization across hospital and homecare settings are driving the global urinary drainage bags market.

The global urinary drainage bags market is poised to witness a CAGR of 5.9% between 2026 and 2033.

Expansion of home healthcare, rising adoption of disposable and infection-control drainage systems, and growing demand from emerging markets present key growth opportunities.

ConvaTec, Inc., Cardinal Health, Teleflex, Inc., Coloplast, and BD are some of the key players in the urinary drainage bags market.