- Pharmaceuticals

- Dermatology Biologics Market

Dermatology Biologics Market Size, Share, and Growth Forecast 2026 - 2033

Dermatology Biologics Market by Product Type (Interleukin Inhibitors, Tumor Necrosis Factor Inhibitors), by End User (Hospital Pharmacies, Retail Pharmacies, e-Commerce), by Regional Analysis, 2026-2033

Dermatology Biologics Market Size and Trend Analysis

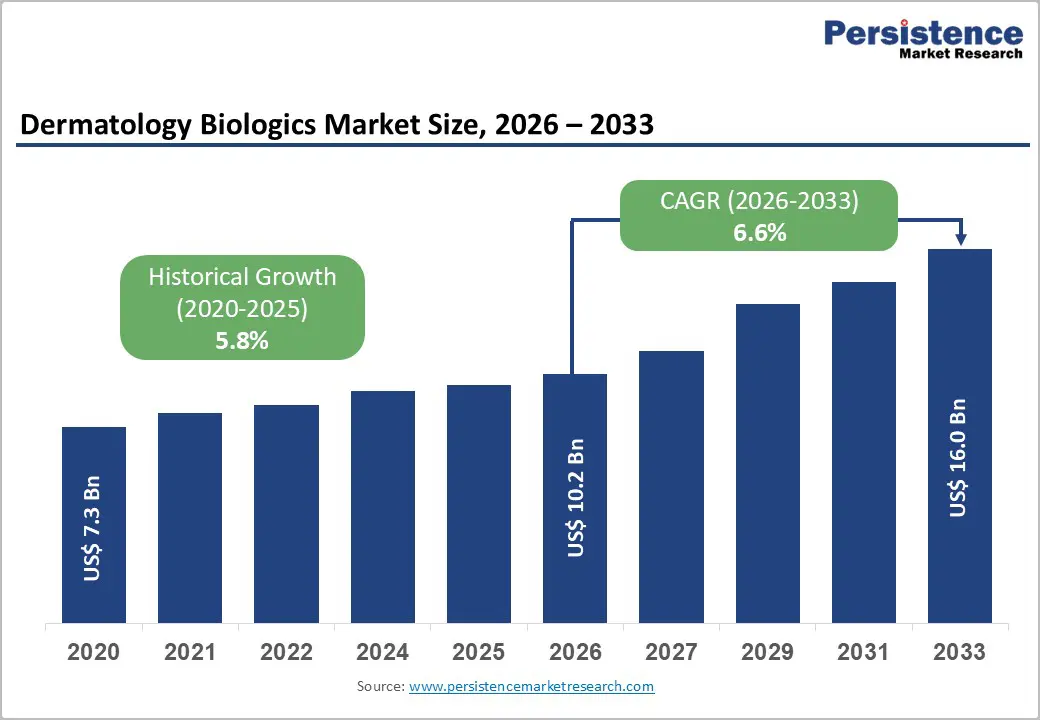

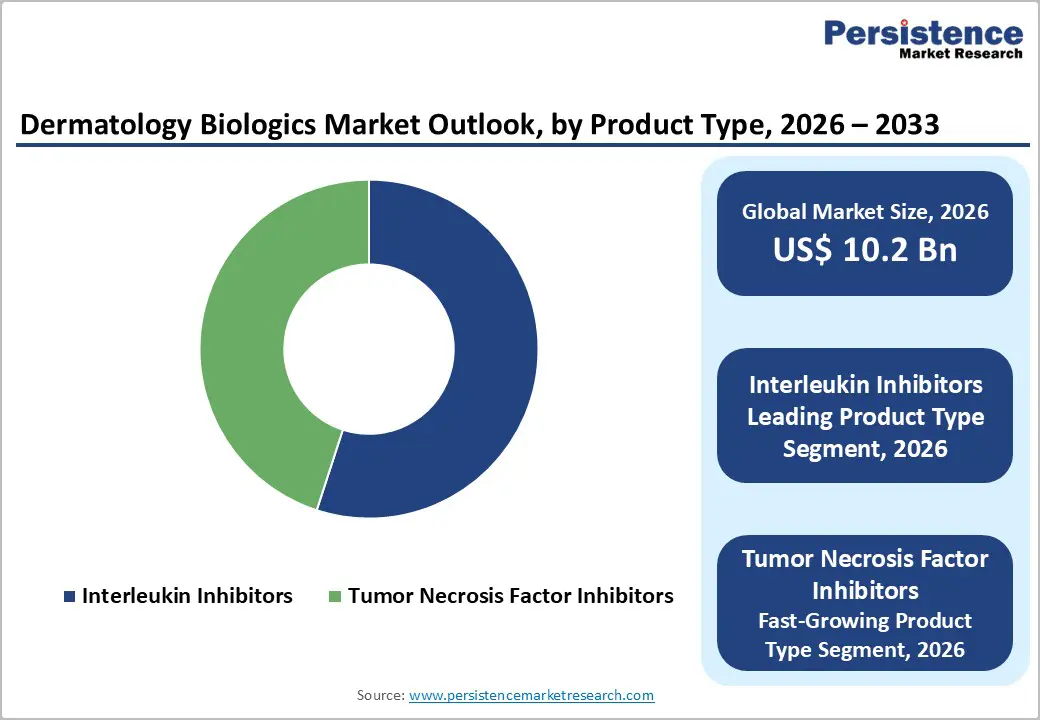

The global dermatology biologics market size is expected to be valued at US$ 10.2 billion in 2026 and projected to reach US$ 16.0 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033.

The dermatology biologics market has emerged as a critical segment within the broader dermatology therapeutics landscape, driven by the rising prevalence of chronic inflammatory skin disorders such as psoriasis, atopic dermatitis, and psoriatic arthritis. Biologics offer targeted immune modulation by inhibiting specific cytokines and pathways involved in disease progression, resulting in improved efficacy and safety compared to conventional systemic treatments. Their ability to deliver long-term disease control has transformed treatment standards, particularly for moderate to severe cases.

Current market trends highlight increasing regulatory approvals, expanding indications, and growing adoption across pediatric and adult populations. The emergence of biosimilars is improving affordability and access, while ongoing research in precision medicine is shaping next-generation biologic therapies. Together, these trends are supporting steady market expansion globally.

Key Market highlights

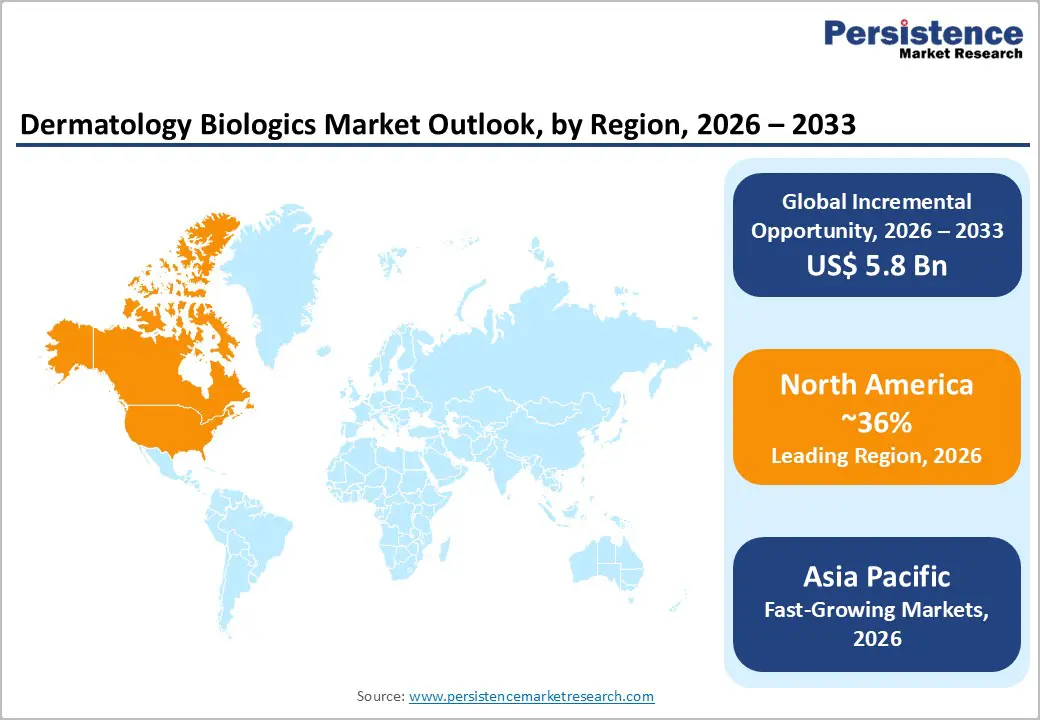

- Leading Region: North America dominates the dermatology biologics market, holding approximately 37–38% share in 2026, supported by high disease prevalence, strong reimbursement frameworks, advanced healthcare infrastructure, and a high number of FDA-approved biologic therapies.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by increasing awareness of biologic treatments, rising healthcare expenditure, expanding access to advanced dermatology care, and growing adoption in countries such as China and India.

- Dominant Segment: Interleukin inhibitors lead the market with over 55% share in 2026, owing to superior clinical efficacy, favorable safety profiles, and broad use in moderate to severe psoriasis and atopic dermatitis.

| Report Attribute | Details |

|---|---|

|

Dermatology Biologics Market Size (2026E) |

US$ 10.2 billion |

|

Market Value Forecast (2033F) |

US$ 16.0 billion |

|

Projected Growth CAGR (2026-2033) |

6.6% |

|

Historical Market Growth (2020-2025) |

5.8% |

Market Dynamics

Driver- Target-specific Mechanism Driving Adoption of Dermatology Biologics

The adoption of dermatology biologics is strongly driven by their target-specific mechanism of action, which offers clear advantages over conventional systemic therapies. Unlike traditional treatments that broadly suppress the immune system, biologics are designed to selectively inhibit specific cytokines or immune pathways involved in disease pathogenesis, such as TNF-α, IL-17, and IL-23. This precision improves clinical outcomes by effectively controlling disease activity while reducing off-target effects and long-term toxicity. As a result, biologics have become a preferred option for chronic and immune-mediated dermatological conditions, particularly moderate to severe psoriasis, psoriatic arthritis, and related inflammatory disorders. Their ability to deliver sustained disease control has significantly transformed treatment standards in dermatology.

Another important growth driver is the expanding use of biologics in pediatric populations. Several biologic therapies have received regulatory approval for treating moderate to severe psoriasis in children, addressing an unmet need where conventional therapies are often limited by safety concerns. Early intervention with biologics can improve quality of life, prevent disease progression, and reduce psychosocial burden in younger patients. Growing clinical evidence supporting safety and efficacy across age groups, along with increasing physician confidence, continues to drive wider adoption of dermatology biologics globally.

Restraint- Pressure to Provide Cost-effective Products

The high and continually rising cost of dermatology biologics remains a significant restraint on market growth. Biologic therapies for conditions such as psoriasis require long-term or lifelong treatment, placing a substantial financial burden on patients, healthcare systems, and insurers. In the context of limited healthcare budgets and competing priorities, payers increasingly scrutinize the cost-effectiveness of biologic therapies, which can delay reimbursement decisions and restrict patient access. These cost pressures are expected to intensify, particularly in publicly funded healthcare systems, limiting broader adoption despite strong clinical benefits.

Additionally, limited awareness and inadequate education regarding skin diseases and biologic therapies in low- and middle-income countries further constrain market growth. Lack of trained specialists and insufficient patient knowledge can lead to underdiagnosis, delayed treatment, or improper use of biologics, increasing the risk of adverse reactions. Concerns over safety, combined with affordability challenges, reduce physician and patient acceptance in emerging markets. Together, high treatment costs and low awareness levels are expected to hinder the expansion of the dermatology biologics market during the 2026–2033 forecast period.

Opportunity- Growth in Biosimilars and Personalized Medicine

The increasing availability of biosimilars presents a major opportunity for the dermatology biologics market by significantly improving treatment affordability. Biosimilars typically offer 40–60% cost savings compared to originator biologics, making advanced therapies accessible to a larger patient population. As regulatory pathways for biosimilars become more streamlined, especially in the U.S. and Europe, approvals are accelerating and competition is intensifying. This pricing pressure is encouraging wider adoption among cost-sensitive healthcare systems and supporting earlier initiation of biologic therapy in clinical practice.

In parallel, the shift toward personalized medicine is creating new growth avenues. Advances in genomics and biomarker research enable better patient stratification, allowing clinicians to select biologics based on individual genetic and immunological profiles. This tailored approach improves treatment response rates and reduces trial-and-error prescribing. Asia Pacific is emerging as a key hub for biosimilar manufacturing and biologic innovation, supported by strong production capabilities and growing R&D investments. Companies focusing on customized biologics and precision-driven therapies are well positioned to capture high growth opportunities in the coming years.

Category-wise Insights

Product Type Analysis

Interleukin inhibitors represent the largest product category in the dermatology biologics market, accounting for approximately 55% of total market share in 2025. Their leadership is primarily attributed to strong clinical efficacy in managing chronic inflammatory skin conditions such as psoriasis and atopic dermatitis. By selectively targeting key cytokines involved in immune-mediated inflammation, including IL-4, IL-13, and IL-17, these therapies deliver faster symptom control and sustained disease remission compared to older biologic classes. Agents such as dupilumab and secukinumab have demonstrated consistent improvement in skin clearance, pruritus reduction, and patient-reported outcomes across multiple clinical trials.

Another factor supporting the dominance of interleukin inhibitors is their expanding range of approved indications and favorable safety profile. These therapies are increasingly prescribed for patients with moderate to severe disease who do not respond adequately to topical treatments or conventional systemic agents. Long-term safety data and convenient dosing schedules have further strengthened physician confidence, reinforcing the widespread adoption of interleukin inhibitors in routine dermatology practice.

End Use Analysis

Hospital pharmacies hold a leading position in the dermatology biologics market, capturing nearly 45% of total end-use share in 2025. This dominance is driven by the high utilization of hospital-based facilities for initiating and administering biologic therapies, particularly infusion-based treatments such as tumor necrosis factor inhibitors. Severe and refractory dermatological cases often require close clinical supervision during initial dosing, making hospital settings the preferred point of care. The availability of trained healthcare professionals and advanced monitoring infrastructure further supports safe and effective biologic administration.

In addition, hospital pharmacies benefit from integrated inpatient and outpatient services, allowing seamless coordination between dermatologists, pharmacists, and nursing staff. Reimbursement structures in many healthcare systems favor hospital dispensing for high-cost biologics, improving access and compliance. Rising hospitalization rates for complex dermatological conditions and increased referrals to tertiary care centers continue to strengthen the role of hospital pharmacies within the overall dermatology biologics distribution landscape.

Regional Insights

North America Dermatology Biologics Market Trends and Insights

North America remains a key contributor to the global dermatology biologics market, with the U.S. accounting for nearly 73.9% of the regional share in 2025. Market growth is strongly supported by a steady increase in U.S. FDA approvals for biologic therapies targeting chronic dermatological conditions. The availability of approved biologics across pediatric and adult populations has expanded the eligible patient pool. For instance, etanercept is approved for patients aged four years and older, ustekinumab for those aged twelve and above, and secukinumab for children as young as six, strengthening adoption across age groups.

In addition, the high prevalence of psoriasis, eczema, acne, and other inflammatory skin disorders continues to drive demand for advanced therapies. Pharmaceutical companies are actively investing in marketing, physician education, and product innovation, further accelerating uptake. Strong reimbursement frameworks, advanced healthcare infrastructure, and high patient awareness collectively support sustained revenue growth for dermatology biologics in the U.S. market.

Asia Pacific Dermatology Biologics Market Trends and Insights

Asia Pacific is emerging as a high-growth region for dermatology biologics, led by China, which accounted for approximately 40.6% of the East Asia market share in 2025. Rising patient preference for biologic therapies is a key factor supporting market expansion in the country. Biologics are increasingly favored due to their targeted mechanism of action, improved clinical efficacy, and better safety profile compared to conventional systemic treatments. This shift reflects growing awareness among patients and clinicians regarding the long-term benefits of precision-based therapies.

Additionally, China’s expanding healthcare infrastructure and increasing access to advanced dermatological treatments are supporting wider adoption. Local manufacturing capabilities and government initiatives aimed at strengthening biologics production are further contributing to market growth. As dermatological disease burden continues to rise with urbanization and lifestyle changes, demand for effective and durable treatment options is expected to increase, positioning China as a major growth engine for the Asia Pacific dermatology biologics market.

Competitive Landscape

Market Structure Analysis

Leading manufacturers are actively securing FDA approvals for new biologic product portfolios to enhance their competitive positioning and expand global market access. These regulatory approvals support broader commercialization and reinforce companies’ long-term product strategies. In parallel, the dermatology biologics market is witnessing increased consolidation, with major players pursuing mergers and acquisitions to strengthen pipelines, expand geographic presence, and gain access to advanced technologies. Strategic collaborations and partnerships are also increasingly adopted to accelerate research, optimize manufacturing capabilities, and improve distribution networks. Together, these initiatives enable companies to reinforce their dermatology biologics offerings and sustain growth in an increasingly competitive landscape.?

Key Market Developments

- In June 2022, AbbVie announced the European Medicines Agency's approval for upadacitinib with the brand name RINVOQ®.

- In January 2022, Amgen and Generate Biomedicines announced a collaboration to develop protein therapeutics for around five clinical targets across various therapeutic areas and multiple modalities.

- In December 2021, Samsung Biologics and AstraZeneca expanded their manufacturing partnerships to improve COVID and cancer therapy facilities.

Companies Covered in Dermatology Biologics Market

- Merck and Co. Inc.

- Novartis AG

- Pfizer Inc.

- AbbVie Inc.

- Amgen Inc.

- AstraZeneca

- Celgene Corporation

- Eli Lilly and Company

- Johnson and Johnson (Janssen Biotech Inc.)

- Others

Frequently Asked Questions

The global dermatology biologics market is expected to reach US$ 10.2 billion in 2026.

Rising prevalence of psoriasis (125 million cases globally) and FDA/ EMA approvals for advanced inhibitors fuel demand.

North America leads with 36% share in 2025.

Biosimilars and label expansions like Dupixent for urticaria offer cost savings and new revenue streams.

Leaders include AbbVie, Novartis, Pfizer, and Janssen, focusing on R&D and partnerships.