- Medical Devices

- Dermatology Diagnostic Device Market

Dermatology Diagnostic Device Market Size, Share, and Growth Forecast, 2025 - 2032

Dermatology Diagnostic Device Market by Product Type (Imaging Devices, Dermatoscopes, Microscopes), Application (Skin Cancer Diagnosis, Vascular Lesions Removal, Hair and Wrinkle Removal, Body Contouring and Fat Removal, and Others), and Regional Analysis for 2025 - 2032

Dermatology Diagnostic Device Market Size and Trends Analysis

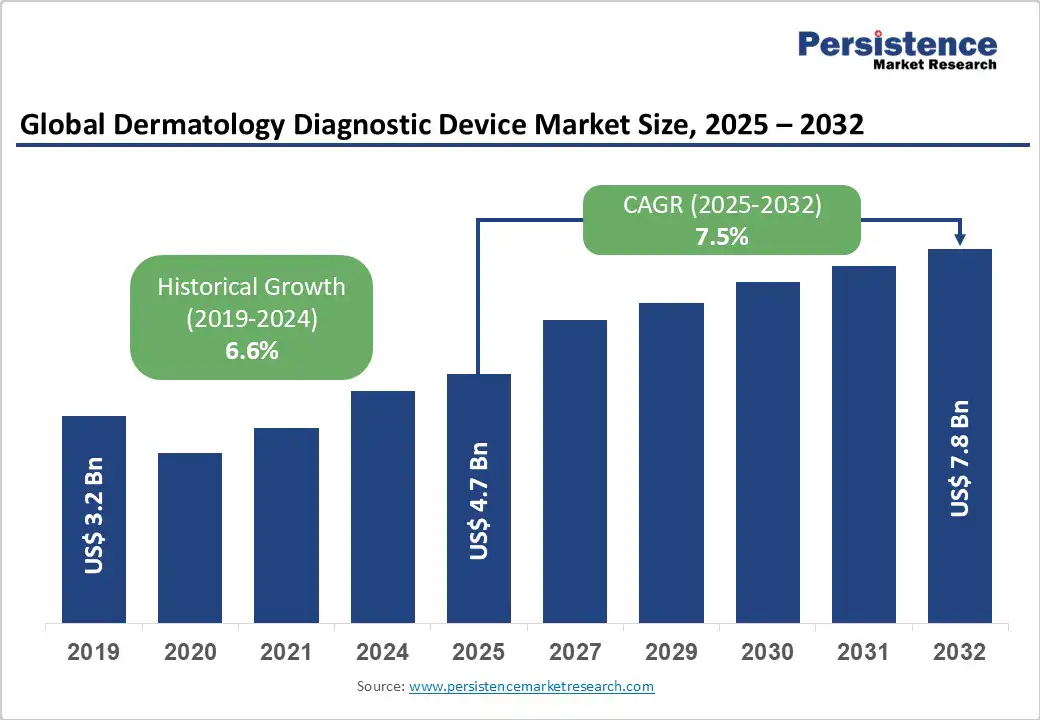

The global dermatology diagnostic device market size is likely to be valued at US$4.7 Bn in 2025 and expected to reach US$7.8 Bn by 2032, registering a robust CAGR of 7.5% during the forecast period from 2025 to 2032, fueled by the increasing demand for non-invasive skin assessment tools, advancements in imaging technologies, and a global push toward early detection of dermatological conditions.

The industry’s expansion is further supported by efforts to enhance diagnostic accuracy, foster AI integration in dermatology, and improve patient outcomes through precise lesion analysis, particularly in North America.

Key Industry Highlights:

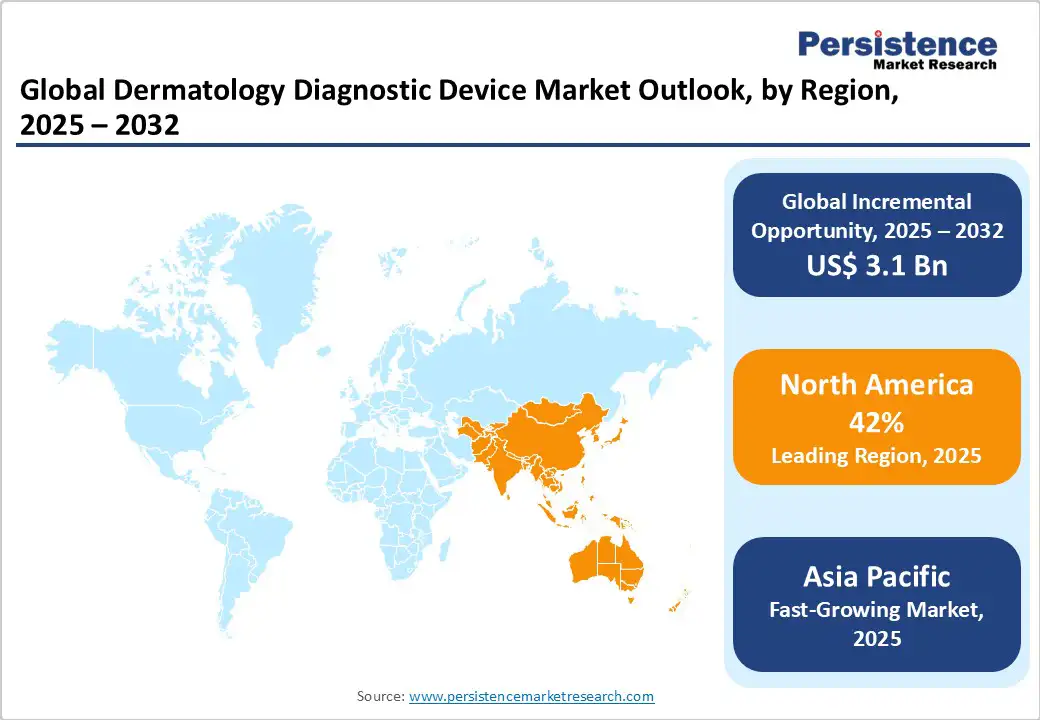

- Leading Region: North America is expected to hold a 42% market share in 2025, driven by advanced healthcare infrastructure, widespread adoption of innovative diagnostic devices, and significant investments in skin cancer research.

- Fastest-growing Region: Asia Pacific, propelled by increasing prevalence of skin disorders, rising healthcare spending, and expanding access to dermatology tools in countries such as China and India.

- Dominant Product Type: Imaging Devices account for approximately 40% of the global dermatology diagnostic device market share in 2025, owing to their critical role in high-resolution visualization and advancements in AI-enhanced analysis.

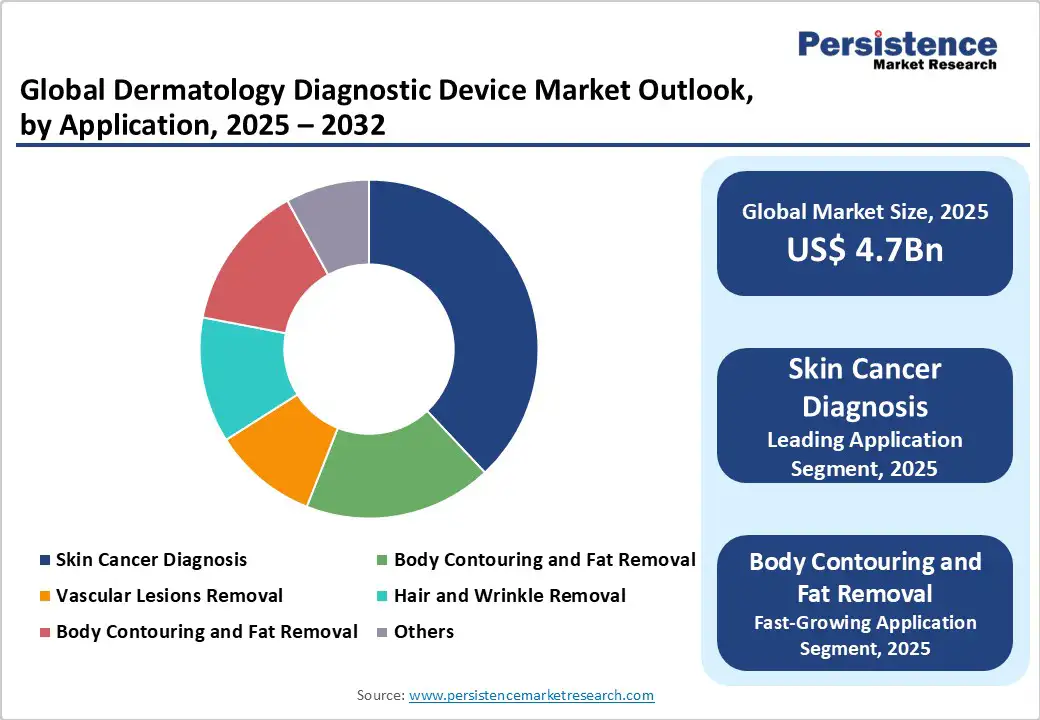

- Leading Application: Skin Cancer Diagnosis with a 38% share, reflecting its critical role in early melanoma detection and preventive screening procedures.

| Key Insights | Details |

|---|---|

|

Dermatology Diagnostic Device Market Size (2025E) |

US$4.7 Bn |

|

Market Value Forecast (2032F) |

US$7.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.2% |

Market Dynamics

Driver - Rising Demand for Early Detection Tools amid Increasing Skin Cancer Prevalence and Technological Advancements

The global surge in demand for early detection tools is a primary driver of the dermatology diagnostic device market. According to the World Health Organization (WHO) and recent estimates from the International Agency for Research on Cancer (IARC), skin cancers represent the most common group of cancers diagnosed worldwide, with more than 1.5 million new cases estimated in 2022, due to factors such as UV exposure and an aging population. This alarming prevalence is exacerbated by an increasing incidence of melanoma, with millions diagnosed globally and substantial mortality, as reported in recent studies, alongside a significant number of cases expected in the United States.

In response, governments and healthcare providers are investing heavily in diagnostic infrastructure, with the United States leading in the adoption of dermatoscopes and imaging devices through programs such as the National Cancer Institute's skin cancer screening initiatives, which aim to support preventive coverage gaps. In Europe, where skin cancer rates are steadily increasing, initiatives such as the EU's Beating Cancer Plan highlight the growing focus on non-invasive diagnostic technologies.

Restraint - High Costs of Production and Stringent Regulatory Compliance

The high costs associated with developing and manufacturing dermatology diagnostic devices represent a significant restraint on market growth. These devices rely on advanced components, including high-definition cameras, sophisticated optical sensors, and AI-powered processors, all of which demand extensive research and development to ensure precision, reliability, and user safety. As a result, production costs are substantially higher than those of basic diagnostic tools, creating affordability challenges for healthcare providers and clinics, particularly in resource-limited or price-sensitive regions.

Regulatory compliance further amplifies these financial pressures. Securing approvals from authorities such as the FDA and obtaining CE marking in Europe necessitates rigorous clinical validations, safety testing, and adherence to quality standards. These processes are time-intensive, which delays product launches and increases overall development costs. Additionally, variability in device calibration due to environmental and operational factors complicates standardization, reducing consistency across different clinical settings. Smaller manufacturers often struggle to absorb these expenses, which limits competition and hinders the scalability of innovative diagnostic solutions. Collectively, these financial, regulatory, and technical challenges pose a significant barrier to market expansion.

Opportunity - Innovation in Formulations and E-commerce Expansion

Advancements in AI-driven imaging and portable diagnostic technologies present significant opportunities for market growth in dermatology. Machine learning algorithms capable of accurately classifying skin lesions and detecting early signs of melanoma enhance diagnostic precision and speed, enabling healthcare providers to deliver more effective and timely interventions. These innovations pave the way for integrated, premium diagnostic platforms that combine high-resolution imaging with AI-assisted analysis, improving clinical outcomes and patient satisfaction.

The growing adoption of e-commerce platforms for medical equipment further expands market potential by providing direct access to clinics and healthcare professionals, particularly in remote and underserved regions. Portable dermatoscopes and microscope-integrated systems can now reach areas with limited infrastructure, increasing affordability and accessibility. Strategic collaborations with telemedicine providers amplify these benefits, enabling remote consultations, virtual screenings, and continuous patient monitoring. Collectively, these technological innovations, combined with digital distribution channels and ecosystem partnerships, foster widespread adoption of advanced dermatology diagnostic devices and drive sustained growth across global markets.

Segmental Insights

Product Type Insights

The dermatology diagnostic device market is segmented into imaging devices, dermatoscopes, and microscopes. Imaging devices dominate, holding approximately 40% of market share in 2025, due to their proven efficacy in multi-spectral analysis, lesion mapping, and integration into digital workflows. Imaging devices are widely used in clinical settings for comprehensive skin assessments, offering automated reporting that reduces diagnostic time.

Dermatoscopes are the fastest-growing segment, driven by increasing demand for handheld, portable solutions in primary care. Dermatoscopes offer polarized light examination as a targeted option, with advancements in digital connectivity and LED illumination making them suitable for teledermatology in mobile populations.

Application Insights

The dermatology diagnostic device market is segmented into skin cancer diagnosis, vascular lesions removal, hair and wrinkle removal, body contouring and fat removal, and others. Skin Cancer Diagnosis dominates, holding approximately 38% of market share in 2025, due to its proven efficacy in melanoma screening, biopsy guidance, and integration into oncology protocols. Skin cancer applications are widely used in specialized clinics, offering early detection that improves survival rates.

Body Contouring and Fat Removal is the fastest-growing segment, driven by increasing demand for aesthetic procedures in cosmetic dermatology. These applications provide non-invasive sculpting as elective options, with advancements in ultrasound-guided devices making them suitable for long-term use in wellness-focused populations.

Regional Insights

North America Dermatology Diagnostic Device Market Trends

North America dominates the global dermatology diagnostic device market, expected to account for 42% share in 2025, driven by a robust healthcare ecosystem, high infrastructure investments, and a cultural emphasis on preventive dermatology and technological innovation. The U.S. market is a frontrunner in the global dermatology diagnostic devices sector, driven by rising melanoma incidence, increasing adoption of AI-integrated imaging solutions, and strong regulatory support. Growing awareness of skin cancer prevention and demand for non-invasive screening tools have accelerated the adoption of advanced diagnostic devices across clinics, hospitals, and telemedicine platforms.

Key drivers include regulatory facilitation from the FDA’s Center for Devices and Radiological Health, which has streamlined approvals for imaging and AI-assisted tools, enabling faster market entry for innovative devices. Teledermatology platforms, such as DermEngine by MetaOptima, and partnerships with insurance providers further expand access to advanced diagnostics, particularly for aging populations and patients in remote areas.

Additionally, research funding from institutions such as the NIH supports innovation in high-resolution imaging technologies, including confocal microscopy and integrated AI analysis, ensuring North America maintains leadership in clinical efficacy and adoption. Combined technological, regulatory, and infrastructure advantages position the U.S. as the primary growth hub for dermatology diagnostics in the region, with strong potential for continued expansion.

Europe Dermatology Diagnostic Device Market Trends

Europe holds a significant share of the global dermatology diagnostic devices market, supported by comprehensive public health systems and a strong focus on cancer prevention and early detection. Leading countries, including Germany and the United Kingdom, drive regional growth through strategic initiatives and policy frameworks that encourage innovation and accessibility. Programs such as Europe’s Beating Cancer Plan promote early detection and adoption of advanced diagnostic technologies, fueling demand for dermatoscopes, imaging systems, and microscope-integrated devices in oncology care.

Germany, with its well-established medtech sector and strong reimbursement policies, invests heavily in research and development, supporting advanced dermatoscopes for evaluating vascular lesions and other skin conditions. The United Kingdom benefits from NHS digital transformation initiatives, enabling faster adoption of imaging devices and integration of high-resolution microscopy in dermatology practices.

Cross-border collaborations and coordinated supply chains for optical components further enhance efficiency and accessibility, reflecting Europe’s emphasis on equity and high-quality care. These factors collectively position Europe as a mature and steadily growing market for dermatology diagnostic devices, combining technological innovation with a strong healthcare infrastructure.

Asia Pacific Dermatology Diagnostic Device Market Trends

Asia Pacific is poised for rapid expansion in the global dermatology diagnostic devices market, driven by demographic shifts, urbanization, and ongoing healthcare modernization. Leading countries, such as China and India, are central to this growth, supported by government-backed programs that promote the adoption of advanced medical technology and strengthen diagnostic infrastructure. Rising prevalence of skin disorders, including melanoma and other dermatological conditions, further fuels demand for reliable diagnostic solutions.

In China, a focus on high-quality, export-ready medical devices accelerates innovation in imaging technologies, while extensive government initiatives support the deployment of dermatoscopes and microscope-integrated systems across hospitals and clinics. In India, national health programs aim to improve access to affordable dermatology diagnostic tools in rural and semi-urban regions, particularly for skin cancer screening and early detection efforts.

E-commerce platforms enhance distribution efficiency, enabling scalable delivery of advanced diagnostic devices to diverse populations. Combined with increasing technological literacy, investments in AI-assisted imaging, and government support, these factors position the Asia Pacific as the fastest-growing region with significant potential for widespread adoption of dermatology diagnostic technologies.

Competitive Landscape

The competitive landscape of the global dermatology diagnostic device market is moderately fragmented, comprising a mix of established global manufacturers and emerging regional players. Companies prioritize continuous innovation, including AI-assisted imaging, high-resolution dermatoscopes, and microscope-integrated systems, to differentiate their offerings. Strategic mergers, acquisitions, and geographic expansion allow firms to enter new markets, strengthen distribution networks, and capitalize on growing demand for advanced, non-invasive diagnostic solutions in both developed and emerging regions.

Key Developments

- January 2024: DermaSensor Inc. announced FDA clearance for its real-time, non-invasive skin cancer evaluation system, capable of detecting all three common skin cancers—melanoma, basal cell carcinoma, and squamous cell carcinoma with high accuracy.

- July 2025: GHO Capital announced the acquisition of FotoFinder Systems, a leading dermatology diagnostic device manufacturer. The move underscores GHO’s commitment to expanding its MedTech portfolio, targeting innovative solutions in skin imaging and cancer detection to enhance global healthcare outcomes and accessibility.

Companies Covered in Dermatology Diagnostic Device Market

- MetaOptima Technology Inc

- Illuco Co., Ltd.

- FotoFinder Systems GmbH

- Michelson Diagnostics Ltd. (MDL)

- HEINE Optotechnik GmbH & Co. KG

- F. Hoffmann-La Roche Ltd

- Rudolf Riester GmbH

- Warner and Webster Pty Ltd

- DermLite

- KIRCHNER & WILHELM GmbH & Co. KG

Frequently Asked Questions

The dermatology diagnostic device market is projected to reach US$4.7 Bn in 2025.

Rising skin cancer incidence, technological advancements in imaging, and preventive healthcare initiatives are key drivers.

The dermatology diagnostic device market is poised to witness a CAGR of 7.5% from 2025 to 2032.

Innovations in AI diagnostics and portable devices, such as teledermatology tools, present significant growth opportunities.

MetaOptima Technology Inc, Illuco Co., Ltd., FotoFinder Systems GmbH, Michelson Diagnostics Ltd. (MDL), DermLite, and KIRCHNER & WILHELM GmbH & Co. KG are among the leading players, known for their innovative diagnostic solutions.