- Aerospace & Defense

- Deep Space Exploration Market

Deep Space Exploration Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Deep Space Exploration Market by Application (Moon Exploration, Mars Exploration, Asteroid Missions, Transportation, Scientific Research, Others), Mission Type (Manned, Unmanned, Human Spaceflight, Robotic), Technology, End-User, and Regional Analysis for 2025 - 2032

Deep Space Exploration Market Share and Trends Analysis

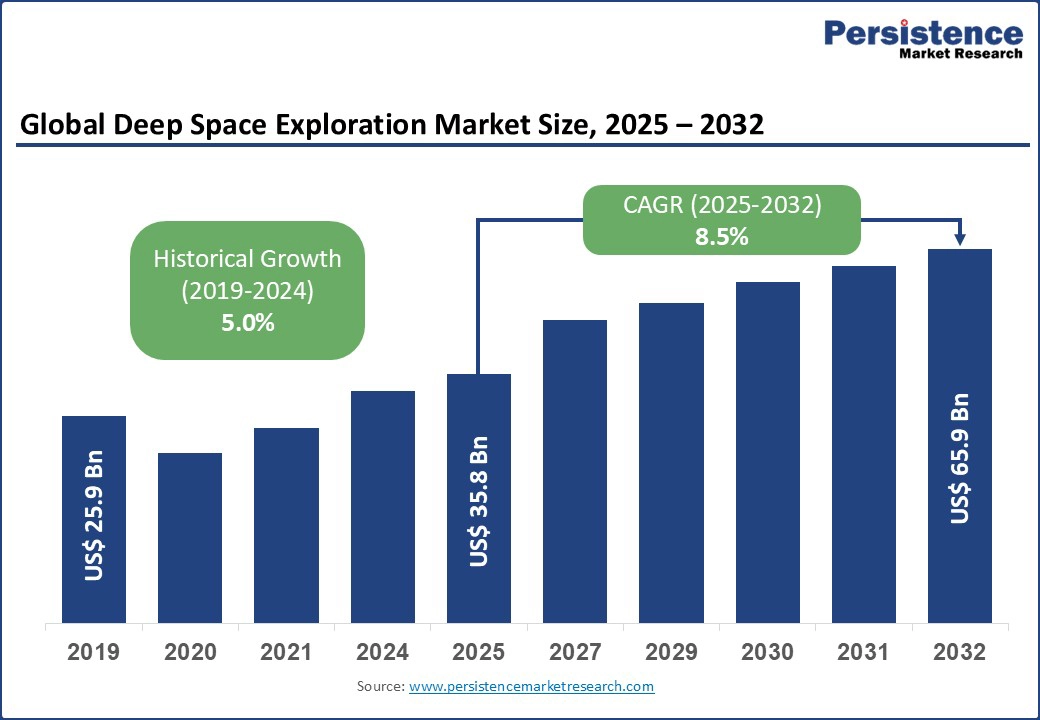

The global deep space exploration market size is likely to be valued at US$ 35.8 Bn in 2025, and is expected to reach US$ 65.9 Bn by 2032, growing at a CAGR of 8.5% during the forecast period 2025 - 2032.

| Global Market Attributes | Key Insights |

|---|---|

| Deep Space Exploration Market Size (2025E) | US$ 35.8 Bn |

| Market Value Forecast (2032F) | US$ 65.9 Bn |

| Projected Growth (CAGR 2025 to 2032) | 8.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.0% |

The commercialization of space infrastructure, advancements in propulsion and energy systems, and an increasing number of international collaborations for space missions are paving the way for a new era of exponential market growth.

Market Factors: Growth, Barriers, and Opportunity Analysis

Democratization of Technologies and Rising Private Sector Investment to Broaden Market Scope

The unprecedented democratization of space technology, combined with substantial private sector investment, enabling mission capabilities, is among the major factors fueling the deep space exploration market expansion. This trend, accentuated by breakthroughs in reusable rocket technology pioneered by SpaceX, and recent commercial contracts awarded for lunar payload delivery, is lowering launch costs and enabling innovation velocity.

In December 2024, for example, Firefly Aerospace was awarded a contract worth US$ 179 million by NASA to deliver and operate six NASA instruments in the Gruithuisen Domes on the Moon’s near side in 2028, under NASA’s Commercial Lunar Payload (CLPS) initiative.

The sizeable reduction in aerospace manufacturing costs due to additive manufacturing and 3D printing techniques has empowered space startups and other emerging players to enter the market, creating a highly competitive ecosystem.

In 2024 alone, more than 250 space launches were conducted globally, highlighting the growing frequency with which space missions are being conducted. This surge will drive the demand for deep space communication systems, autonomous navigation, and AI-powered robotics, and, with the infusion of private capital, coupled with open-source initiatives for space software and hardware, expand market opportunities for satellite constellations, in-situ resource utilization (ISRU), and extraterrestrial habitat construction.

Restraint - Unpredictability of Deep Space to Erect Entry Barriers for Small Market Players

A prominent hindrance facing the market for deep space exploration is the harsh and unpredictable deep-space environment, which poses severe technological and operational challenges that can significantly escalate costs and risks. Unlike low Earth orbit, deep space subjects spacecraft and crew to prolonged exposure to cosmic radiation, microgravity-induced physiological effects, and extreme thermal fluctuations, all of which compromise mission reliability and human safety.

For example, NASA’s ongoing research on mitigating radiation impacts for Artemis and upcoming Mars missions highlights the complexity and expense of developing effective shielding technologies, life support systems, and autonomous emergency protocols.

The mysteries of deep space have thus necessitated continuous innovation in materials science, propulsion, and spacecraft design, which have driven up R&D expenditures and increased mission failure risk, acting as a formidable barrier to entry for smaller market players.

Opportunity - International Collaborations and AI-Driven Autonomous Missions to Create Profitable Avenues

The current dynamics of the deep space exploration market are being upturned by the rise of international collaborations coupled with advances in AI-driven autonomous missions, which is dramatically expanding mission scope while optimizing cost efficiencies. Geopolitical dynamics have moved nations to pool resources for ambitious projects, as shared infrastructure and interoperable technologies reduce duplication and accelerate timelines.

For example, NASA’s Artemis Accords, launched in October 2020, were initially signed by eight national space agencies from the United States, Australia, Canada, Italy, Japan, Luxembourg, the United Arab Emirates, and the United Kingdom. As of July 2025, the Accords have grown to include 56 signatory nations.

Furthermore, breakthroughs in onboard AI and robotics, such as AI-enabled rovers capable of complex terrain navigation on Mars without real-time human intervention, are unlocking innovation opportunities in autonomous systems for deep space’s communication-limited environments.

This technological leap enables sequential multi-target missions hitherto deemed impractical, multiplying scientific return and commercial potential alike. Investors and players focusing on these intersections in the form of deep space AI robotics, international space agency partnerships, and autonomous mission planning stand to gain from a rapidly maturing ecosystem.

Category-wise Analysis

Technology Insights

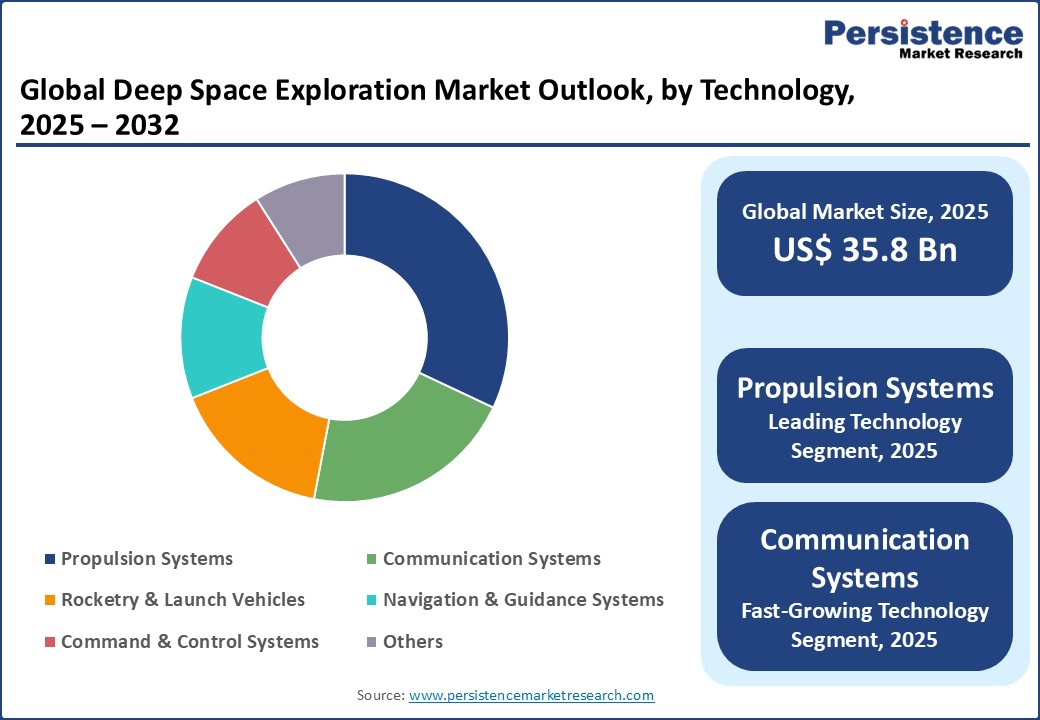

Propulsion systems are expected to hold the leading share of about 32.0% in the technology category in 2025, accounting for the largest portion of investments and technological focus. Encompassing both chemical and non-chemical propulsion technologies essential for mission viability beyond Earth's orbit, the urgency to reduce travel time and improve fuel efficiency for deep space missions is the main factor fueling innovations in these systems. Recent industry advancements, such as nuclear thermal propulsion (NTP) promise to drastically shorten Mars travel duration, as evidenced by NASA’s ongoing research investments and test programs in this endeavor.

The communication systems segment is poised to display the highest CAGR of approximately 14.3% through 2032. The reason for the prolific growth of this segment is that enhanced deep space communication networks are pivotal for maintaining real-time connectivity across vast distances, addressing data latency challenges and facilitating autonomous mission control. The growing complexity of interplanetary missions and the rise of satellite mega-constellations have fueled the demand for robust, secure, and high-throughput communication infrastructures.

The segment also benefits from the exponential rise in data-intensive deep space missions and the introduction of AI-enabled autonomous spacecraft requiring uninterrupted, low-latency communication channels. Emerging laser communication technologies, such as NASA’s Laser Communications Relay Demonstration (LCRD), offer superior bandwidth and energy efficiency over traditional radio frequency (RF) systems, making this technology as a prime market catalyst.

Application Insights

Moon exploration is anticipated to be the dominant application segment in 2025, commanding an estimated market revenue share of 34.0%. The announcement of numerous lunar missions by different space agencies, increasing public-private partnerships for deep space exploration, and renewed interest in establishing a sustainable human presence on the Moon are the factors aiding the dominance of this segment.

Programs such as NASA’s Artemis, China’s Chang’e lunar missions, ISRO’s Chandrayaan, and commercial initiatives targeting lunar payload delivery and resource extraction bolster this segment’s outlook. Recent successful Artemis missions have reiterated the possibility of deploying reusable lunar landers, ISRU technology for water ice extraction, and lunar gateway infrastructure. Public engagement in lunar science augmented by the spectacular imagery fed by rovers and educational outreach enhances public-private investment in these missions.

Asteroid missions are likely to stand out as the fastest-growing application segment, projected to register a CAGR of nearly 14.0% through 2032. These missions, initially confined to scientific curiosity, have escalated into commercially attractive ventures due to advancements in asteroid mining technologies and metal extraction potential.

Early projects by private players such as Planetary Resources and breakthroughs in autonomous prospecting robots are already widening the growth outlook of this segment. The insatiable appetite for rare earth elements and platinum-group metals accessible on asteroids compounds is stimulating investor interest and spurring technological innovation.

For example, JAXA’s Hayabusa2 and NASA’s OSIRIS-Rex have sufficiently validated the commercial feasibility of asteroid material extraction. Rapid advancements in remote sensing technologies and autonomous prospecting robots are facilitating high-precision identification of volatile and metal-rich asteroids.

Regional Insights

North America Deep Space Exploration Market Trends

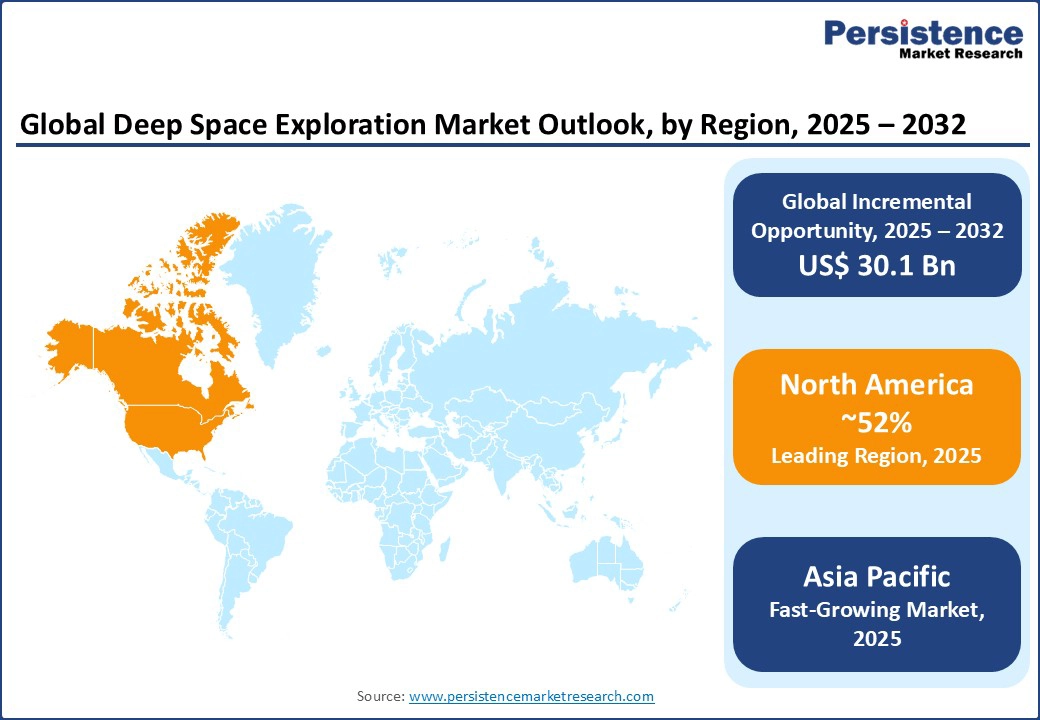

At 52.0%, North America will dominate the deep space exploration market share in 2025, mainly on account of the overwhelming presence of NASA and the U.S. Department of Defense, alongside a vibrant and well-capitalized private aerospace sector spearheaded by SpaceX and Blue Origin.

The region’s leadership is solidified by robust government budgets aimed at ambitious lunar and Martian missions, cutting-edge propulsion technology development, and pioneering reusable launch vehicles. The integration of AI-powered autonomous spacecraft systems and advanced space communication infrastructure has elevated mission efficacy and expanded commercial feasibility.

Geopolitical competition and strategic military interests have further fed funding and innovation intensity in deep space exploration ventures. Moreover, recent path-breaking developments such as SpaceX’s Starship program and DARPA’s deep space photon communication project have cemented the predominance of North America in technology leadership.

Asia Pacific Deep Space Exploration Market Trends

Asia Pacific is set to be the fastest-growing regional market, with a CAGR forecast of 8.1% from 2025 to 2032. The market here is supported by growing government investments in space technology by China, India, Japan, and South Korea. China's lunar exploration and Mars missions, India’s Chandrayaan and Mangalyaan successes, and Japan’s rover technologies have emboldened regional space ambitions.

Public-private partnerships are gaining pace, buttressed by national policies encouraging commercial space enterprises. Increasing infrastructure development in the form of regional spaceports and R&D hubs, combined with the adoption of robotics, AI-enabled mission automation, and satellite constellation deployment, are accelerating market expansion.

Europe Deep Space Exploration Market Trends

Europe holds a steady position with around 15.0% of the market share, primarily because of collaborative programs headed by the European Space Agency (ESA), focusing on scientific research, inter-agency partnerships, and development of components for international missions.

Deepening partnerships with NASA and China National Space Administration (CNSA), alongside investments in spacecraft payloads, navigation systems, and shared lunar gateway infrastructure, highlight the strategic stance of the European Union (EU). Government space agencies and private players in the region are leveraging strengths in precision engineering and robotics innovation, promoting sustainable space exploration and environmental monitoring from orbit.

Competitive Landscape

The global deep space exploration market landscape is increasingly influenced by cutthroat competition between established aerospace giants, novel startups, and state-backed space agencies, creating a fertile ground for technological innovation and strategic partnerships.

The surge in government funding for ambitious programs such as NASA's Artemis and ESA's Lunar Gateway projects, alongside escalating private-sector investments led by companies such as SpaceX, whose reusable launch technologies are revolutionizing cost structures, are the foremost drivers.

A distinctive trend is the rise of collaborative ecosystems where mergers, acquisitions, and joint ventures have accelerated the development of advanced propulsion systems, autonomous robotics, and deep-space communication networks, reducing time-to-market for next-generation solutions.

The democratization of space access has further intensified market competition, compelling firms to adopt agile innovation models and invest heavily in AI, additive manufacturing, and ISRU technologies.

Key Industry Developments:

- In September 2025, SpaceX conducted a static-fire test on the Super Heavy booster B15, igniting all 33 Raptor engines for approximately 10 seconds at its Starbase facility in Texas, as part of final preparations for Starship Flight Test 11. This rapid follow-up comes less than two weeks after the highly successful Flight Test 10 and signals that SpaceX may attempt Flight Test 11 as early as later this month, maintaining impressive development momentum.

- In August 2025, Agnikul Cosmos, a Chennai-based private space startup, produced the world’s largest single-piece 3D-printed rocket engine entirely from Inconel superalloy in one seamless build. Eliminating welds, joints, and fasteners from fuel inlet to plume outlet, the engine features enhanced structural integrity and slashes production time by over 60%. The company also secured a U.S. patent for this ground-breaking design and manufacturing process.

- In July 2025, facing soaring costs in the US$ 8-US$ 11 billion range and potential cancellation under the 2026 U.S. federal budget, NASA’s Mars Sample Return (MSR) mission might be salvageable thanks to a leaner, commercially minded proposal from aerospace giant Lockheed Martin. The company has offered to execute the mission under a firm-fixed-price contract for under US$ 3 billion, aiming to reduce complexity by scaling down the lander, ascent vehicle, and Earth re-entry system, while leveraging proven, heritage-based designs.

Companies Covered in Deep Space Exploration Market

- Space Exploration Technologies Corp. (SpaceX)

- The Boeing Company

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Blue Origin Enterprises, L.P.

- Airbus SE

- Thales Alenia Space

- Sierra Nevada Corporation

- Rocket Lab USA, Inc.

- Maxar Technologies Inc.

- Astrobotic Technology, Inc.

- NEC Space Technologies, Ltd.

- Indian Space Research Organisation (ISRO)

- China National Space Administration (CNSA)

- European Space Agency (ESA)

Frequently Asked Questions

The global deep space exploration market is projected to reach US$ 35.8 billion in 2025.

The unprecedented democratization of space technology and the explosive growth in private sector investments in space exploration ventures are driving the market.

The market is poised to witness a CAGR of 8.5% from 2025 to 2032.

The rising number of international space collaborations driven by geopolitical dynamics and advances in AI-driven autonomous missions are key market opportunities.

Space Exploration Technologies Corp. (SpaceX), The Boeing Company, and Lockheed Martin Corporation are some key players.