- Beverages

- Bottled Deep Ocean Water Market

Bottled Deep Ocean Water Market Size, Share, and Growth Forecast 2026 - 2033

Bottled Deep Ocean Water Market by Packaging (200–500 Ml, 500–1000 Ml, 1000–2000 Ml, Above 2000 Ml), End-user (Business to Business, Business to Consumer (Hypermarkets/Supermarkets, Specialty Stores, Online Retail, Others)), and Regional Analysis, 2026–2033

Bottled Deep Ocean Water Market Size and Trend Analysis

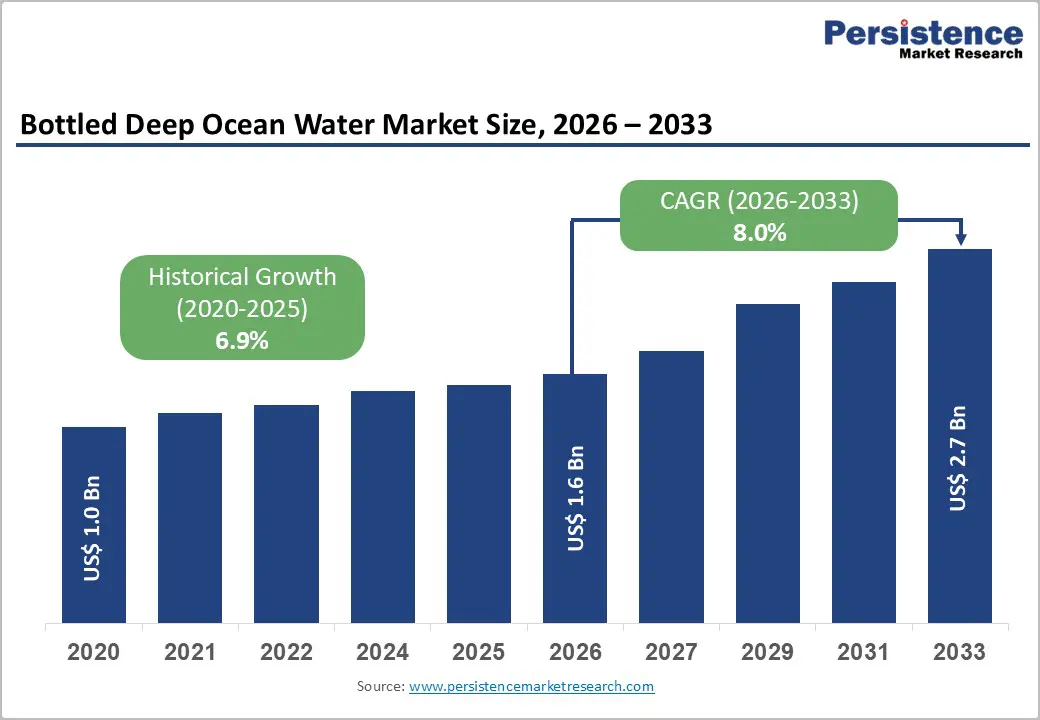

The global bottled deep ocean water market size is expected to be valued at US$ 1.6 billion in 2026 and projected to reach US$ 2.7 billion by 2033, growing at a CAGR of 8.0% between 2026 and 2033. The market is on a strong growth trajectory, driven by rising global consumer demand for premium functional beverages, expanding scientific recognition of deep ocean water's unique mineral and nutritional properties, and the premiumization of hydration products across health-conscious markets in the Asia Pacific, North America, and Europe.

Deep ocean water extracted from depths exceeding 200 meters is recognized for its high mineral density, low contamination profile, and stable low-temperature composition, with applications spanning direct consumption, cosmetics, food processing, and nutraceutical sectors. Growing wellness tourism, rising disposable incomes among urban middle-class demographics, and expanding online specialty retail channels are reinforcing consistent double-digit demand growth globally.

Key Industry Highlights:

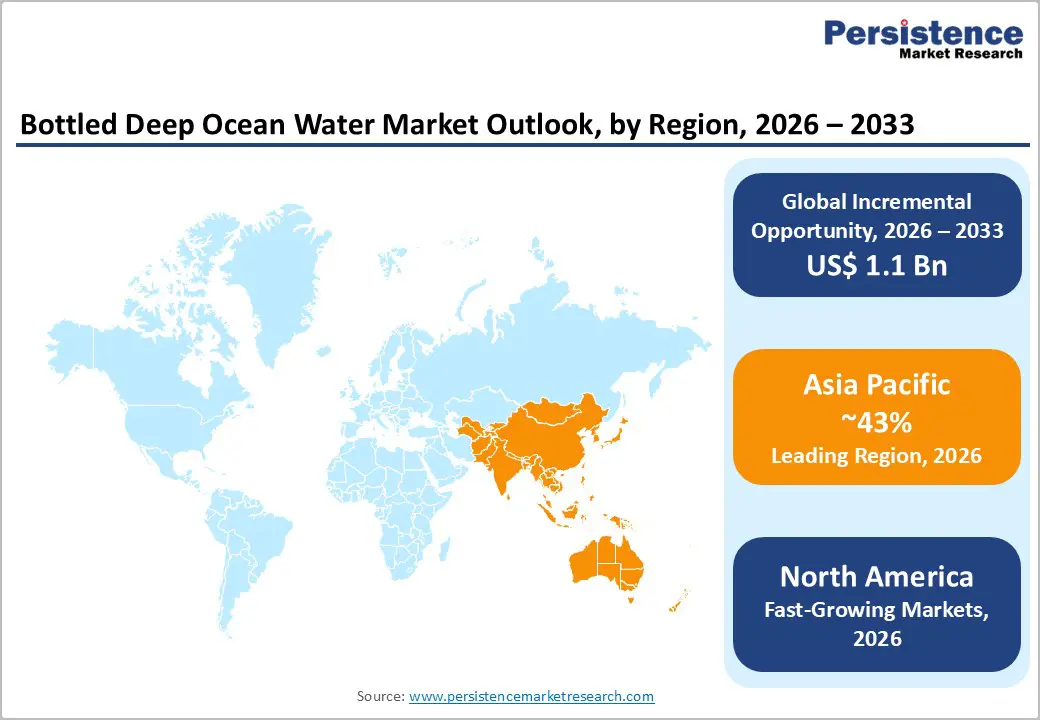

- Leading Region – Asia-Pacific leads the global bottled deep ocean water market with ~43% revenue share in 2025, supported by Japan’s established deep sea extraction industry, Taiwan’s Pacific seawater production capacity, and rising premium mineral water demand across China through cross-border e-commerce platforms.

- Fast-Growing Market – North America is the fast-growing regional market, driven by expanding distribution from wellness beverage brands, increasing consumer preference for mineral-rich functional hydration, and rising adoption of premium bottled wellness drinks through specialty retail and direct-to-consumer channels.

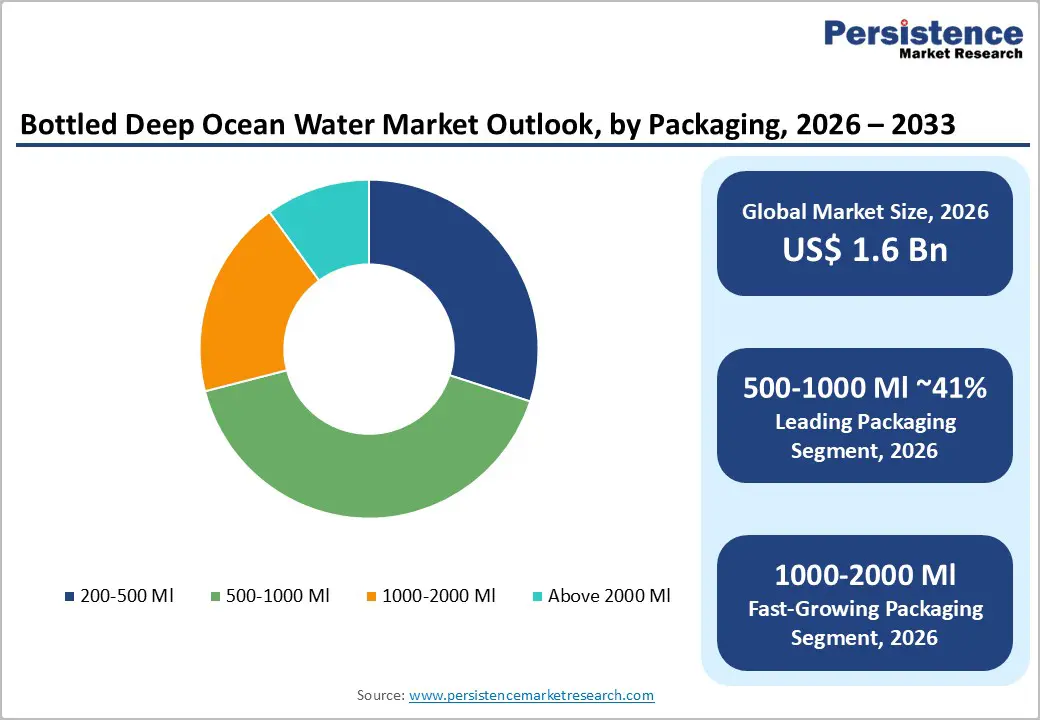

- Dominant Segment – The 500–1000 ml packaging segment dominates with ~41% market share in 2025, supported by strong demand for single-serve daily hydration, fitness recovery applications, and convenience-focused purchasing behavior among health-conscious consumers.

- Fast-Growing Packaging Segment – The 1000–2000 ml packaging segment is the fastest growing, driven by increasing household consumption, growing foodservice procurement, and higher value-per-unit preference among repeat consumers seeking economical larger pack formats.

- Key Opportunity – Major opportunities exist in B2B channel expansion through cosmetic ingredient supply, luxury hospitality water services, and food processing applications, enabling producers to diversify revenue streams beyond direct consumer beverage sales.

Market Dynamics

Drivers - Rising Consumer Demand for Premium Functional and Mineral-Rich Hydration Products

The global shift toward premium, health-functional beverages is a foundational demand driver for bottled deep ocean water. Deep seawater extracted from depths greater than 200 meters is naturally enriched with over 70 trace minerals, including magnesium, calcium, potassium, and vanadium nutrients documented in peer-reviewed studies in journals including the Journal of Nutritional Science and Vitaminology and Marine Drugs for supporting cardiovascular health, electrolyte balance, and metabolic function. The International Bottled Water Association (IBWA) reports consistent growth in the premium bottled water sub-category globally, with consumers increasingly willing to pay price premiums for clinically differentiated hydration options. Japan's long-established deep ocean water consumption culture, supported by Japan's Agency for Marine-Earth Science and Technology (JAMSTEC) research, has validated functional benefits that are now driving adoption across North American and European wellness markets.

Government-Supported Deep Ocean Water Infrastructure Development in Japan and Taiwan

Institutional support for deep ocean water extraction and commercialization infrastructure has been a critical market enabler, particularly in Japan and Taiwan, where national policy frameworks have facilitated industry development. In Japan, the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) and local prefectural governments in Kochi, Toyama, and Niigata have funded deep ocean water extraction facilities since the 1990s, enabling the establishment of commercial operators including Muroto Deep Sea Water Co., Ltd. and Niigata Sado Deepsea Water Co., Ltd. Taiwan's government-funded research on Pacific deep seawater off its eastern coastline has supported domestic brands including Taiwan Yes Deep Ocean Water Co., Ltd. The state-backed infrastructure reduces capital access barriers for commercial operators, enabling consistent product availability and quality standardization that supports market development.

Restraints - Limited Geographic Extraction Feasibility Constraining Global Supply Scale

Commercially viable deep ocean water extraction is geographically constrained to coastal locations with access to continental shelf depths of 200+ meters within economically feasible pipeline distances from shore. Currently, viable commercial extraction sites are concentrated primarily in Hawaii (U.S.), Japan (Kochi, Toyama, Niigata), Taiwan, Norway, and select Pacific Island locations. This geographic concentration limits the global scalability of production capacity and creates logistical challenges for international distribution, restricting the ability of market participants to fully address global demand without incurring prohibitive shipping costs for a water-heavy product category.

Opportunities - B2B Applications in Cosmetics, Food Processing, and Hospitality Sector Expansion

The Business-to-Business (B2B) application segment represents a high-growth diversification opportunity for bottled deep ocean water producers, enabling revenue generation beyond direct consumer sales. Deep ocean water's unique mineral composition and biological cleanliness have attracted interest from premium cosmetics formulators with brands incorporating deep seawater in skincare products marketed for hydration and mineral replenishment.

The global cosmetic ingredient market's premium naturals segment, reported by Cosmetics Europe to be among the fastest-growing formulation categories, represents a high-value industrial demand channel. Luxury hotels and high-end restaurant groups in Japan, Taiwan, and Hawaii are additionally incorporating deep ocean water in culinary applications and premium beverage menus, creating consistent institutional procurement volumes. Expanding B2B channel partnerships by Ako Kasei Co., Ltd. and Panablu Co., Ltd. demonstrate the commercial viability of this multi-application expansion strategy.

Category-wise Insights

Packaging Analysis

The 500–1000 ml packaging segment leads the global bottled deep ocean water market, commanding ~41% of total packaging-based market share in 2025. This dominant position reflects the format's alignment with individual single-serve consumption occasions, including daily hydration, fitness recovery, and wellness routines that represent the core use case for deep ocean water among its primary health-conscious consumer base. The 500–1000 ml format offers an optimal balance between value-for-consumption and the premium price-per-unit economics that make deep ocean water commercially viable at retail. Japan's extensive deep ocean water retail distribution across convenience store chains, health food stores, and hypermarkets has been standardized around 500 ml and 710 ml bottle formats. Leading producers, including Kona Deep and Taiwan Yes Deep Ocean Water Co., Ltd., have built their core consumer product lines around this size range.

End-user Insights

The Business-to-Consumer (B2C) channel leads the bottled deep ocean water market end-use segment, accounting for ~58% of total end-use share in 2025. Within the B2C channel, specialty health stores and online retail are growing particularly rapidly, while hypermarkets and supermarkets provide the broadest geographic reach for premium bottled water products.

Japan's mature deep ocean water retail market demonstrates the B2C channel's potential depth, with products available across Seven-Eleven Japan and regional supermarket chains. The International Bottled Water Association (IBWA) confirms the expanding premium water category in retail globally. North American B2C channel growth through specialty wellness retailers including Whole Foods Market and direct-to-consumer e-commerce platforms is reinforcing B2C channel leadership as the primary revenue-generating sales pathway for bottled deep ocean water brands globally.

Regional Insights

North America Bottled Deep Ocean Water Market Trends and Insights

North America is the fastest-growing regional market for bottled deep ocean water, driven by the U.S.' expanding premium wellness beverage culture, rising consumer curiosity about mineral-rich functional water alternatives, and the commercial development activities of Hawaiian-origin brands. Growing e-commerce penetration and specialty health retail expansion are improving product accessibility beyond initial early-adopter demographics in coastal wellness markets.

U.S. Bottled Deep Ocean Water Market Size

The U.S. accounts for ~88% of the North American market in 2025, driven by Hawaii-based production from Kona Deep and Hawaii Deep Blue LLC. State-supported extraction infrastructure at Keahole Point, Hawaii, combined with growing national e-commerce distribution and premium retail partnerships, is underpinning above-average U.S. market growth.

Europe Bottled Deep Ocean Water Market Trends and Insights

Europe represents a nascent but growing market for bottled deep ocean water, characterized by strong consumer preference for premium mineral waters and a well-developed specialty health food retail ecosystem. Norwegian deep seawater extraction initiatives and growing import of Japanese and Hawaiian deep ocean water products through wellness e-commerce channels are gradually building European market awareness and demand.

Germany Bottled Deep Ocean Water Market Size

Germany holds ~22% of the European bottled deep ocean water market in 2025, underpinned by Germany's mature premium mineral water culture and well-developed health specialty retail network. Rising German consumer interest in functional and mineral-dense hydration products consistent with the country's broader natural health food market growth, is driving gradual deep ocean water adoption through import distribution channels.

UK Bottled Deep Ocean Water Market Size

The UK accounts for ~18% of the European market in 2025. The UK's thriving premium wellness retail sector, encompassing Holland & Barrett and independent health food stores alongside growing online premium water subscription services, is creating accessible import channels for Japanese and Hawaiian deep ocean water brands targeting British wellness consumers.

France Bottled Deep Ocean Water Market Size

France accounts for ~15% of the European bottled deep ocean water market in 2025. France's cultural appreciation for premium mineral waters and sophisticated culinary water selection in high-end dining where deep ocean water is gaining traction as a unique table water offering creates both B2C and B2B hospitality channel growth opportunities for market entrants.

Asia Pacific Bottled Deep Ocean Water Market Trends and Insights

Asia-Pacific leads the global bottled deep ocean water market with ~43% of total market share in 2025, anchored by Japan's decades-long deep ocean water commercialization heritage and Taiwan's significant Pacific deep seawater extraction industry. China's growing premium health beverage market is creating new import demand, with Chinese consumers increasingly seeking differentiated mineral water products from Japan and Taiwan through cross-border e-commerce platforms.

India Bottled Deep Ocean Water Market Size

India holds ~8% of Asia Pacific market share in 2025, representing an early-stage but rapidly developing market. Rising urban affluence, growing wellness awareness among India's expanding upper-middle class and increasing availability of imported premium water brands through Amazon India and specialty health stores in metro cities are driving initial deep ocean water market entry and awareness-building.

Japan Bottled Deep Ocean Water Market Size

Japan is the dominant country market in Asia-Pacific, accounting for ~38% of the regional share in 2025. Government-supported extraction facilities in Kochi, Toyama, and Niigata prefectures, established domestic brands, including Muroto Deep Sea Water Co., Ltd. and Niigata Sado Deepsea Water Co., Ltd., and deep ocean water's integration into mainstream convenience retail sustain Japan's market leadership.

Competitive Landscape

The global bottled deep ocean water market is highly fragmented, with a diverse mix of geographically specialized producers predominantly based in Japan, Taiwan, Hawaii, and Norway competing in regionally defined market ecosystems. Key players, including Kona Deep, Hawaii Deep Blue LLC., Taiwan Yes Deep Ocean Water Co., Ltd., Muroto Deep Sea Water Co., Ltd., and Panablu Co., Ltd. differentiate through extraction depth claims, mineral profile documentation, packaging premiumization, and B2B application development. Emerging business model trends include direct-to-consumer subscription models, luxury hospitality partnerships, and cosmetic ingredient supply channel development targeting premium skincare formulators globally.

Key Developments:

- In July 2024, the company signed a distribution agreement with Taiwan YES to supply premium deep ocean water products sourced from 662m depth in Hualien, Taiwan.

- In June 2024, Chlorophyll Water partnered with rePurpose Global to recover one ocean-bound plastic bottle for every bottle sold, strengthening sustainability efforts in the premium bottled water industry.

Global Bottled Deep Ocean Water Market - Key Insights & Details

|

Key Insights |

Details |

|

Historical Market Value (2020) |

US$ 1.0 Billion |

|

Current Market Value (2026) |

US$ 1.6 Billion |

|

Projected Market Value (2033) |

US$ 2.7 Billion |

|

CAGR (2026–2033) |

8.0% |

|

Leading Region |

Asia-Pacific, ~43% market share (2025) |

|

Dominant Packaging |

500–1000 Ml, ~41% market share (2025) |

|

Top-ranking End Use |

Business to Consumer (B2C), ~58% share (2025) |

|

Incremental (2026–2033) |

US$ 1.1 Billion |

Companies Covered in Bottled Deep Ocean Water Market

- Hawaii Deep Blue LLC.

- Kona Deep

- Taiwan Yes Deep Ocean Water Co., Ltd.

- Destiny Deep Sea Water

- Deep Ocean Water Company LLC.

- iROC Corporation

- Panablu Co., Ltd.

- Ako Kasei Co., Ltd.

- Muroto Deep Sea Water Co., Ltd.

- Niigata Sado Deepsea Water Co., Ltd.

- Tropical World Food

- Ôdeep

- Ocean’s Halo

- Seven-Eleven Hawai, Inc.

- Others

Frequently Asked Questions

The global bottled deep ocean water market is estimated to be valued at US$ 1.6 billion in 2026.

Growing blood transfusion demand, rising healthcare awareness, and improved safety standards are driving the disposable blood bags industry's expansion.

Asia-Pacific leads the global bottled deep ocean water market with ~43% of total market share in 2025.

Advancements in biodegradable materials, increasing healthcare investments, and expanding blood donation programs create significant growth opportunities in this market.

Poly Medicure Limited, Grifols, S.A., Macopharma Bharat Transfusion Solution, Fresenius Kabi India Pvt. Ltd., TERUMO PENPOL Pvt. Limited and Others.