- Advanced Materials

- Cross Laminated Timber Market

Cross Laminated Timber Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Cross Laminated Timber Market by Bonding Technology (Mechanically Fastened, Adhesive-bonded), Application (Walls, Ceilings, Roof Structures, Beam, Other), End-user (Residential, Commercial, Industrial, Other), and Regional Analysis for 2025 - 2032

Cross Laminated Timber Market Size and Trend Analysis

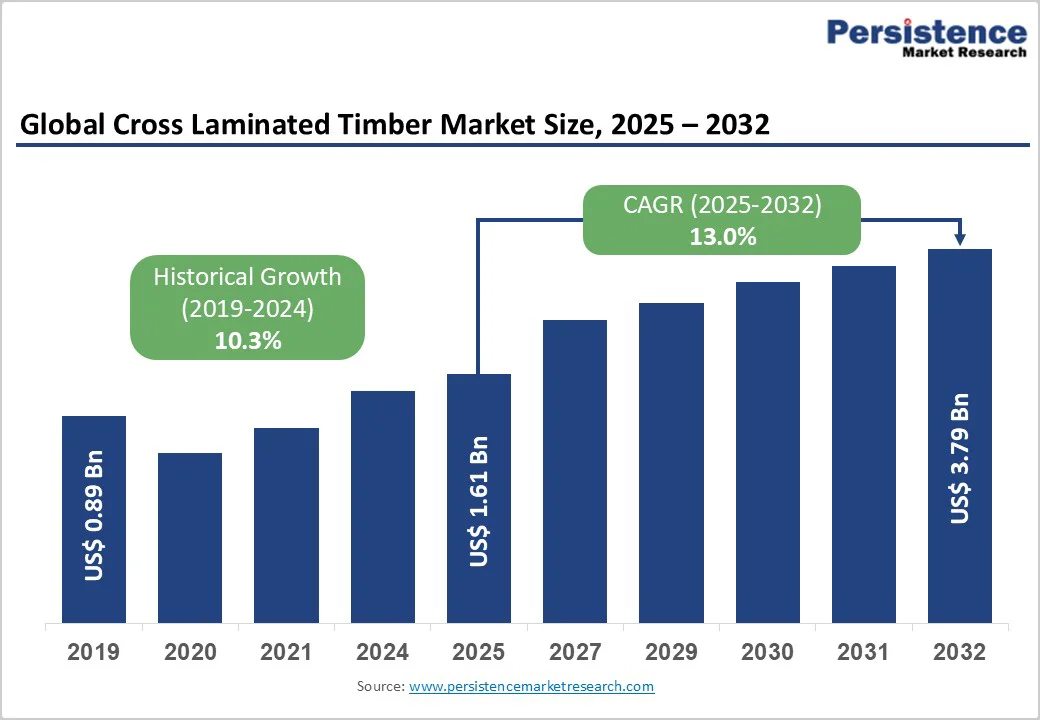

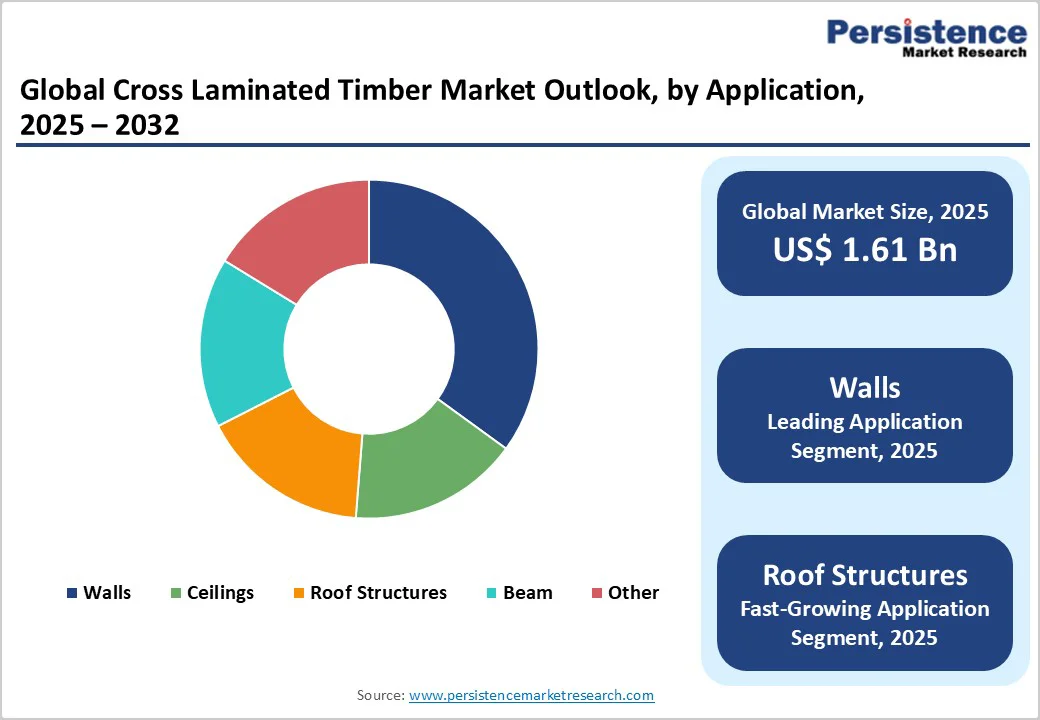

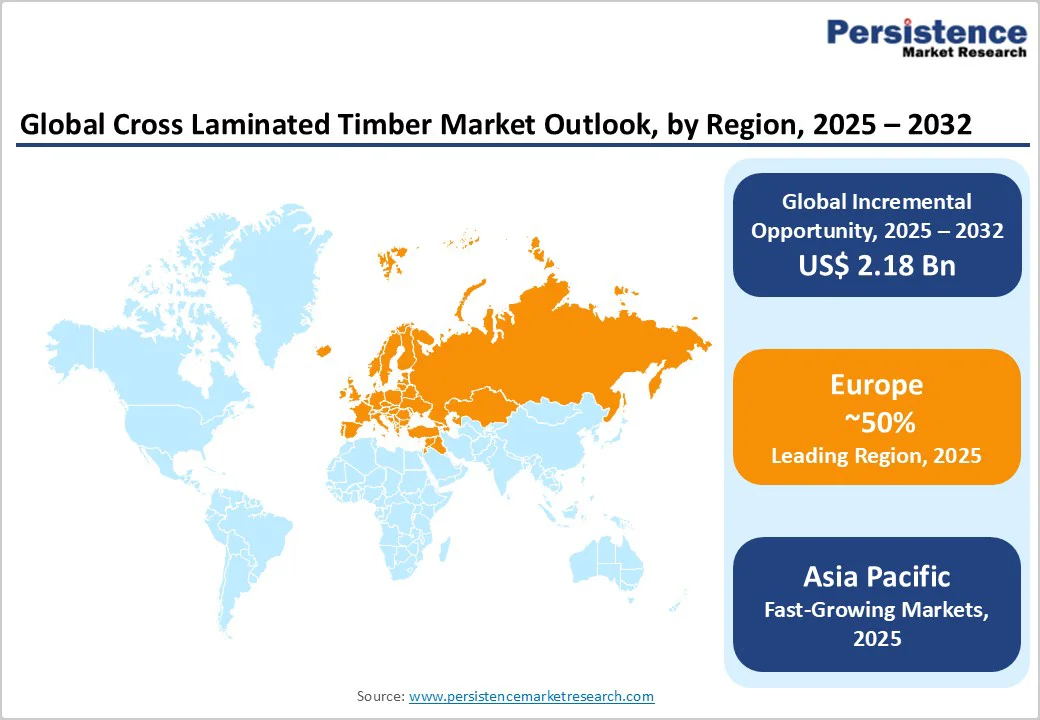

The global cross-laminated timber market size is valued at US$1.6 billion in 2025 and projected to reach US$3.8 billion by 2032, growing at a CAGR of 13.0% between 2025 and 2032.

Cross-laminated timber is emerging as a superior alternative to conventional steel and concrete, offering carbon sequestration of approximately 1.1 tonnes of CO2 per cubic meter and enabling construction time reductions of up to 30% through prefabrication.

The integration of CLT into building codes, particularly the 2021 International Building Code (IBC) revisions, which allow mass timber structures up to 18 stories and 270 feet tall, has unlocked unprecedented opportunities in mid-rise and high-rise construction.

Key Industry Highlights:

- Regional Leader: Europe leads as the dominant region, driven by stringent EU regulations and mature manufacturing, capturing over 50% global share through sustainable policy enforcement.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, propelled by urbanization in China and Japan.

- Leading Segment: Adhesive-bonded dominates bonding technology, holding 88% share for its strength and cost benefits in structural applications.

- Fastest Growing Segment: Residential end-user grows fastest, fueled by eco-housing demands and quick prefab builds.

- Growth Opportunities: Urban high-rise opportunities via tech advancements offer key potential, enabling taller sustainable structures with 20% emission reductions.

| Key Insights | Details |

|---|---|

| Cross Laminated Timber Size (2025E) | US$1.6 Bn |

| Market Value Forecast (2032F) | US$3.8 Bn |

| Projected Growth CAGR (2025 - 2032) | 13.0% |

| Historical Market Growth (2019 - 2024) | 10.3% |

Market Dynamics

Drivers - Rising Demand for Sustainable Building Materials

The adoption of cross-laminated timber is propelled by global emphasis on sustainability in construction, as it sequesters carbon and reduces environmental impact compared to traditional materials. The European Union's Energy Performance of Buildings Directive, launched in January 2024, requires life cycle assessments for all new buildings, starting with large structures in 2028, and sets mandatory emission limits from 2030.

The U.S. Army Corps of Engineers now mandates the evaluation of mass timber options during design phases for all vertical construction projects. These initiatives align with LEED and BREEAM certifications, which increasingly reward carbon sequestration strategies.

CLT's renewable sourcing from FSC and PEFC-certified forests, combined with significantly lower energy consumption during manufacturing compared to concrete and steel, positions it as the material of choice for achieving net-zero construction targets across commercial, institutional, and residential sectors.

Supportive Government Policies and Building Codes

Favorable regulations worldwide are accelerating the integration of cross-laminated timber into mainstream construction by recognizing its structural viability. In North America, updated codes from the International Code Council permit taller timber buildings, spurring innovation in seismic-resistant designs. European directives, such as those under the EU Green Deal, mandate low-carbon materials, with cross-laminated timber qualifying for subsidies in renewable projects.

Timber harvesting equipment market advancements further optimize the supply chain from forest to fabrication. Projects utilizing CLT demonstrate overall cost savings of approximately 15% compared to traditional materials when accounting for reduced construction duration, simplified site management, fewer trade coordination requirements, and accelerated return to occupancy.

By harmonizing standards, governments are mitigating adoption barriers and fostering a conducive environment for growth. This regulatory backing convincingly positions cross-laminated timber as a cornerstone of future resilient infrastructure.

Restraints - Higher Initial Material Costs and Limited Manufacturing Capacity

The Cross Laminated Timber market faces constraints from elevated upfront material costs relative to conventional concrete and steel, particularly in regions with limited local production infrastructure. Despite long-term savings through reduced construction time and labor efficiency, initial CLT panel pricing remains 10-20% higher than traditional alternatives, creating procurement hesitation among cost-sensitive developers.

Manufacturing capacity constraints compound this challenge, with major European producers such as Binderholz (220,000 m³), Stora Enso (410,000 m³ across four facilities), and KLH Massivholz (125,000 m³) struggling to meet surging global demand.

The capital-intensive nature of CLT production facilities requires substantial investment in specialized pressing equipment, quality control systems, and kiln drying infrastructure. Transportation logistics for large-format panels further increase project costs in markets distant from manufacturing hubs, limiting penetration in emerging construction regions.

Moisture Sensitivity and Technical Specification Complexity

Cross-laminated timber applications face technical challenges related to moisture management and design specification complexity that can deter adoption among traditionally trained architects and engineers.

CLT panels require maintaining moisture content at 12% ± 3% during manufacturing and providing ongoing protection from water exposure during construction and operation to prevent dimensional variations, surface cracking, and potential delamination. This necessitates careful detailing of building envelopes, proper site storage protocols, and weather protection during installation, requirements that add complexity and possible delays to construction schedules.

Although cross-laminated timber manufactured to EN 16351 standards achieves fire class B-s1, d0 ratings and CLT can withstand fire exposure for 90 minutes, outperforming or matching conventional steel and concrete structures, architectural and building officials in North America express residual skepticism.

Insurance and liability concerns regarding long-term performance in humid climates further constrain market expansion in tropical and sub-tropical regions, where moisture-related degradation risks require additional protective treatments and monitoring systems.

Opportunity - Expansion in Urban Infrastructure and High-Rise Developments

Rapid urbanization presents significant potential for cross-laminated timber in mid- and high-rise buildings, particularly in densely populated cities seeking efficient construction. With global urban populations projected to rise by 68% by 2050, according to United Nations estimates, demand for quick-assembly materials will surge.

Innovations like hybrid systems combining cross-laminated timber with steel enable taller structures, as seen in recent Japanese projects exceeding 10 stories.

Government initiatives in India and ASEAN countries promote sustainable urban planning, offering subsidies for green materials. This opportunity is amplified by the growth of the Europe Room Cell Module Market, where prefabricated timber modules streamline modular construction. Companies can capitalize by investing in localized production and tapping into a market segment expected to grow at double-digit rates amid policy-driven infrastructure booms.

Advancements in Technology and Sustainability Certifications

Technological progress in adhesives and digital modeling tools opens avenues for enhanced performance of cross-laminated timber, attracting eco-focused end-users. Integration with BIM software improves design precision, reducing waste by 15% according to engineering journals. Emerging certifications from FSC and PEFC validate sustainable sourcing, appealing to residential developers prioritizing certifications.

China's investments in automated factories are boosting exports. This ties into the Agroforestry Market, where sustainable timber harvesting supports supply chains. Future potential lies in seismic enhancements for the Asia-Pacific region, with developments promising 20% cost savings in retrofitting. Market participants can leverage these innovations to capture shares in the burgeoning green retrofit sector.

Category-wise Analyis

Bonding Technology Insights

The adhesive-bonded segment dominates the bonding technology category, holding approximately 88% market share due to its superior structural integrity and cost-efficiency in production. Adhesive-bonded CLT uses structural adhesives to bond lumber layers in alternating perpendicular orientations, creating composite panels with enhanced strength exceeding the capabilities of individual components.

This methodology enables larger panel sizes up to 16 meters in length and 3.45 meters in width, as produced by Stora Enso, facilitating diverse architectural designs without visible fasteners.

Adhesive bonding ensures airtight and watertight panel performance, critical for energy-efficient building envelopes that meet stringent thermal performance standards. Manufacturing processes maintain lumber moisture content at 12% ± 3% with assembly times of 15-60 minutes, depending on adhesive type and equipment.

Mechanically fastened CLT, though representing a smaller market share, serves specialized applications requiring reduced chemical usage, ease of disassembly, and enhanced recyclability.

Application Insights

The walls segment leads in applications, capturing around 35% of the market, driven by its versatility in load-bearing and non-structural uses in modern architecture. Wall systems benefit from CLT's exceptional structural performance in load-bearing applications, its capacity for tall structures, and its design flexibility, which permits custom openings for windows, doors, and mechanical penetrations.

European projects, including the HoHo Wien in Vienna and the H7 Office Building in Germany, showcase the performance of CLT walls. In residential and commercial settings, walls enable open-plan designs with minimal supports, aligning with aesthetic trends. This dominance stems from regulatory approvals for taller timber facades, particularly in Europe. As demand for lightweight enclosures grows, walls remain pivotal, supported by proven durability in diverse climates.

End-user Insights

The residential segment commands about 40% of the end-user market, fueled by homeowner preferences for eco-friendly, customizable homes that emphasize natural aesthetics. Cross-laminated timber's energy efficiency lowers heating needs, with studies showing 15-20% savings in operational costs. Rising single-family and multi-unit construction, backed by government housing incentives, is amplifying this trend.

Japan's residential timber construction boom, supported by the Fumio Kishida-led Liberal Democratic Party government, demonstrates government-backed initiatives that link sustainable building materials to carbon-emission targets and public health outcomes.

The segment achieves enhanced growth through industrial mass timber structures, such as the Windsor, Connecticut facility, demonstrating CLT's structural capabilities for large-span industrial requirements while meeting corporate sustainability commitments increasingly mandated by stakeholders and environmental, social, and governance frameworks.

Regional Insights

North America Cross-Laminated Timber Trends

North America's cross-laminated timber market thrives on the U.S. leadership in innovation, with the International Building Code updates in 2021 allowing buildings up to 18 stories, spurring projects like the T3 Minneapolis tower.

The U.S. Department of Agriculture Forest Service's Wood Innovations Grant program, which provides US$5 million annually, supports CLT testing and validation. The landmark Ascent project in Milwaukee, the world's tallest mass timber hybrid structure at 25 stories, received USDA grants enabling rigorous testing demonstrating CLT's compliance with structural and fire safety performance.

Canada complements this with federal incentives under the green construction through the Wood program, investing CAD 40 million in mass timber demos. Such trends show a 30% rise in residential applications since 2023, driven by urbanization in cities like Vancouver. Overall, the region's dynamics emphasize policy-driven sustainability and tech integration.

Europe Cross-Laminated Timber Trends

Europe dominates the global cross-laminated timber market, with 50% of the market share, due to harmonized ETAG 15 regulations, which enable seamless cross-border use. Germany advances market development through the Model Timber Construction Directive, streamlining approval processes, with North Rhine-Westphalia implementing progressive provisions.

The U.K.'s post-Brexit green pledges, including the Timber in Construction Roadmap, target 20% market penetration by 2030, as evidenced by London's hybrid towers. France's RE2020 code mandates low-carbon designs, increasing cross-laminated timber in public buildings by 25%.

Stora Enso's four European plants have a combined annual capacity of 410,000 m³, establishing market dominance. The EU Energy Performance of Buildings Directive mandates life cycle assessments from 2028 and emission limits from 2030, cementing CLT's regulatory advantage. Austria's CLT innovation leadership continues with KLH Massivholz's second production facility in Bad St. Leonhard, with a 125,000 m³ capacity.

Asia Pacific Cross Laminated Timber Trends

Asia Pacific is the fastest-growing Cross Laminated Timber region, driven by urbanization pressures, green building initiatives, and technological localization.

Japan leads regional adoption, with 36 planning applications for mid-rise and high-rise timber buildings in 2024, double the previous year's volume, supported by the Fumio Kishida-led government's timber-construction mandate to address carbon emissions and public health challenges. The Tokyo Olympics (2021) and Osaka World Expo showcase world-class mass timber architecture, including what is projected to become the world's largest timber structure.

Australia and New Zealand benefit from XLam's pioneering role as Australasia's first CLT manufacturer since 2010, utilizing locally grown plantation pine with sustainable harvest and replanting cycles. XLam's transition to 100% renewable energy at its Wodonga, Victoria, facility reduces the carbon footprint by 45% (from 447 kg CO2e to 248 kg CO2e per cubic meter), demonstrating regional sustainability leadership.

Competitive Landscape

The global cross laminated timber market remains fragmented, with over 50 players globally, though European firms hold 60% influence via established capacities. Companies pursue expansion through mergers, like Pfeifer Group's acquisitions, and R&D in bio-adhesives for enhanced durability.

Leaders differentiate via certifications like PEFC, ensuring traceability. Emerging models include modular prefabrication hubs, reducing logistics by 30%. This structure encourages innovation amid rising demand.

Key Market Developments

- April 2024: Stora Enso completed the Bourdonnières School in Nantes, France, the first project utilizing its automated coating line for cross-laminated timber, demonstrating advanced surface treatment capabilities for enhanced durability and aesthetic performance in institutional applications.

- January 2024: The European Union launched the Energy Performance of Buildings Directive, establishing mandatory life cycle assessments for large new buildings from 2028 and emission limits from 2030, fundamentally shifting the regulatory landscape in favor of low-carbon construction materials, including CLT.

- November 2024: Stora Enso announced a strategic review of its Central European operations covering seven sawmills in Austria and Czechia, signaling portfolio optimization in response to evolving market dynamics and capacity utilization challenges affecting the broader timber industry.

Top Companies in Cross Laminated Timber

- Stora Enso (Finland): A pioneer in mass timber, it leads with integrated forestry-to-product chains, supplying CLT for iconic projects like the Mjøstårnet. Revenue from wood products exceeds €9 billion, underscoring the importance of sustainability certifications.

- Binderholz GmbH (Austria): Known for vertically integrated operations, it produces 500,000 m³ annually, focusing on custom CLT solutions. Its influence stems from EU-compliant innovations that serve residential markets robustly.

- KLH Massivholz GmbH (Austria): Specializing in prefabricated CLT systems, it holds strong portfolio in commercial builds, with exports to Asia. Maturity in engineering drives its leadership in high-performance panels.

Companies Covered in Cross Laminated Timber Market

- Stora Enso

- Mayr Melnhof Holz Holding AG

- Binderholz GmbH

- Xlam Ltd.

- Pfeifer Holding GmbH

- Schilliger Holz AG

- KLH Massivholz GmbH

- Eugen Decker Holzindustrie KG

- Katerra

- Nordic Structures

- Mercer Mass Timber

- HASSLACHER Holding GmbH

- Structurlam Mass Timber Corporation

Frequently Asked Questions

The global Cross Laminated Timber market is valued at US$1.6 Bn in 2025 and expected to reach US$3.8 Bn by 2032, reflecting a 13.0% CAGR driven by sustainable construction trends.

Key drivers include government policies promoting green buildings and rising sustainability awareness, with EU Green Deal initiatives boosting adoption by reducing carbon footprints in construction.

Adhesive-bonded leads with 88% share, offering superior strength and efficiency for structural uses, as validated by industry standards.

Europe leads due to harmonized regulations like ETAG 15 and strong manufacturing in Germany and Austria, holding over 50% global influence.

Urban high-rise developments offer potential through tech like BIM integration, enabling 20% faster builds and aligning with Asia Pacific infrastructure growth.

Leading players include Stora Enso, Binderholz GmbH, and KLH Massivholz GmbH, dominating with innovative production and global supply chains.