- Industrial Goods & Service

- Cross Roller Bearings Market

Cross Roller Bearings Market Size, Share, and Growth Forecast 2026 - 2033

Cross Roller Bearings Market by Product Type (Single Inner and Split Outer Ring, Split Inner and Single Outer Ring, Others), Dimension (18 to 50 mm, 50 to 150 mm, 150 to 250 mm, 250 to 400 mm, 400 to 630 mm, 630 to 800 mm, >800 mm), End-user (Manufacturing & Machinery, Automotive, Healthcare & Medical, Electronics & Semiconductors, Aerospace & Defense), and Regional Analysis for 2026 - 2033

Cross Roller Bearings Market Size and Trend Analysis

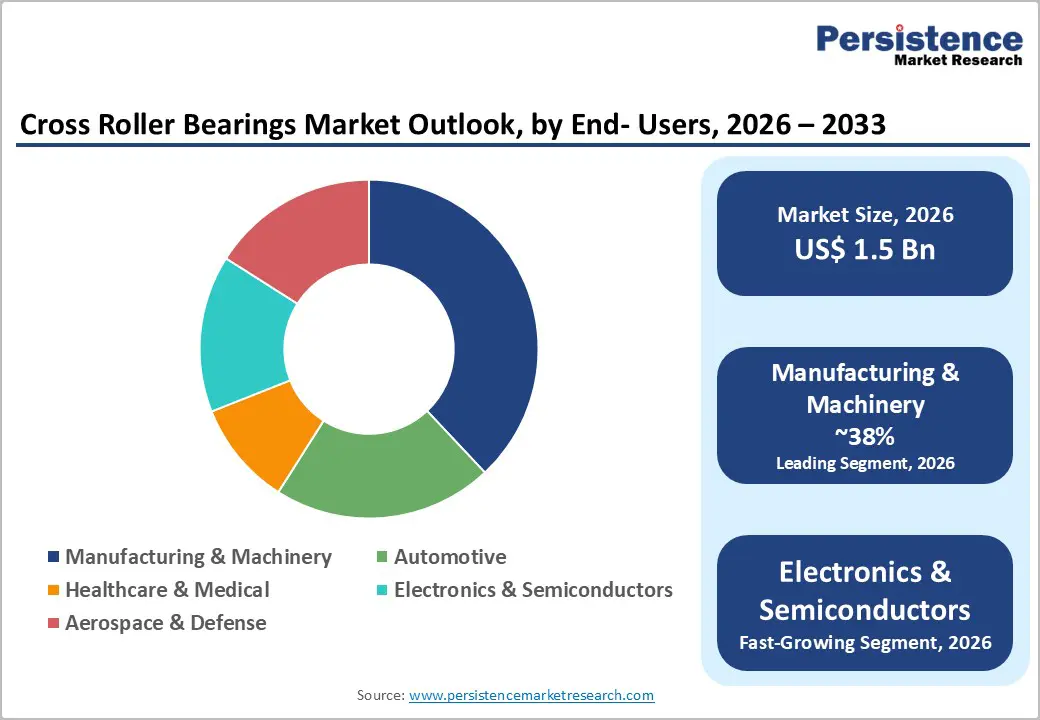

The global Cross Roller Bearings market size is valued at US$ 1.5 billion in 2026 and is projected to reach US$ 1.9 billion by 2033, growing at a CAGR of 3.5% between 2026 and 2033.

The cross-roller bearings market is experiencing sustained growth, driven primarily by rising demand from precision-critical industries such as robotics, semiconductor manufacturing, and medical devices. These bearings, capable of simultaneously handling radial, axial, and moment loads within a compact structure, are increasingly preferred in high-accuracy applications where conventional bearing arrangements fall short.

Key Market Highlights

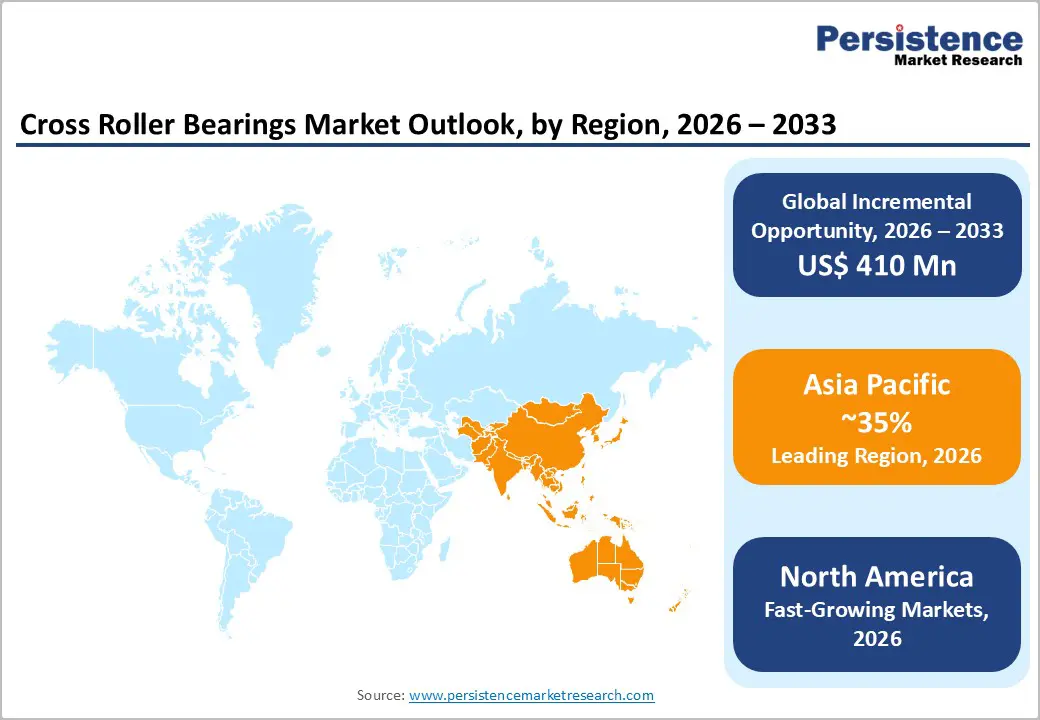

- Leading Region – Asia Pacific dominates the Cross Roller Bearings Market, driven by China's robotics density surpassing 392 units per 10,000 workers, Japan's precision bearing manufacturing leadership, and rapidly growing semiconductor investments across the region.

- Fastest Growing Region – North America represents a significant market for cross roller bearings, led predominantly by the United States, which accounts for the bulk of regional demand. The region's growth is underpinned by substantial investments in semiconductor fabrication.

- Dominant end-user Segment – The Manufacturing & Machinery segment leads with approximately 38% share, driven by CNC machine tool adoption, Industry 4.0 investments, and extensive use of precision bearings in industrial automation globally.

- Fastest Growing end-user Segment –The Healthcare & Medical segment is the fastest-growing end-user, fueled by rising surgical robot installations, expanding medical imaging equipment deployments, and FDA-accelerated robotic-assisted surgery approvals worldwide.

- Key Opportunity – Rising NATO defense budgets exceeding US$ 1.3 trillion and India's record INR 6.21 trillion defense allocation are creating durable demand for cross roller bearings in satellites, radar systems, and UAV platforms globally.

| Key Insights | Details |

|---|---|

|

Cross Roller Bearings Market Size (2026E) |

US$ 1.5 Bn |

|

Market Value Forecast (2033F) |

US$ 1.9 Bn |

|

Projected Growth CAGR (2026–2033) |

3.5% |

|

Historical Market Growth (2020–2025) |

2.5% CAGR |

Market Dynamics

Drivers - Surging Demand from Industrial Robotics and Automation

The rapid proliferation of industrial automation and robotics represents a dominant growth driver for the cross-roller bearings market. Cross roller bearings are integral to robotic joints, rotary axes, and articulated arms due to their ability to handle multi-directional loads with high rigidity in minimal space. The International Federation of Robotics (IFR) reported that global operational stock of industrial robots reached approximately 3.9 million units in 2023, up from 3.5 million in 2022, representing a growth of over 11%. Key markets such as China, Japan, South Korea, Germany, and the United States are significantly investing in factory automation. This sustained expansion of automated manufacturing infrastructure directly translates into elevated procurement volumes for precision cross roller bearings, sustaining a positive demand trajectory over the forecast period.

Expanding Semiconductor and Electronics Manufacturing Sector

The semiconductor industry's relentless pursuit of precision in wafer-handling equipment, lithography systems, and chip inspection platforms is a critical driver for cross roller bearings. These bearings support ultra-precise rotational and linear motion required in semiconductor fabrication, where positioning accuracy at the sub-micron level is non-negotiable. The Semiconductor Industry Association (SIA) reported global semiconductor sales surpassed US$ 526 billion in 2023, with significant investment commitments under policy frameworks such as the U.S. CHIPS and Science Act (US$ 52.7 billion) and the European Chips Act (over €43 billion). This capital inflow is expected to accelerate construction of new fabrication facilities, directly boosting demand for precision motion components, including cross roller bearings.

Restraints - High Manufacturing Costs and Complex Production Processes

Cross roller bearings require advanced manufacturing techniques including ultra-precision grinding, surface hardening, and meticulous assembly under controlled conditions which significantly elevate production costs compared to standard radial or thrust bearings. The specialized tooling and quality assurance processes necessary to meet tolerances within microns substantially limit margin flexibility for manufacturers. This cost burden is particularly prohibitive for small and mid-sized buyers in price-sensitive industrial segments. According to U.S. Bureau of Labor Statistics data, manufacturing input costs including skilled labor and precision tooling have risen by over 15% since 2020, compressing profitability and restraining broader market penetration, especially in emerging economies where budget-constrained end-users often opt for lower-cost conventional bearing alternatives.

Supply Chain Vulnerability for Specialty Steel and Raw Materials

Cross roller bearings rely heavily on high-grade bearing steel with exacting metallurgical properties primarily 52100 chromium steel and stainless-steel variants that are sourced from a limited number of qualified suppliers globally. Geopolitical disruptions, trade restrictions, and raw material price volatility have repeatedly impacted supply continuity. The World Steel Association noted that global crude steel production experienced significant disruptions between 2021 and 2023 due to energy cost spikes in Europe and trade restrictions in Asia. Such supply instability raises lead times and input costs, creating headwinds for manufacturers and limiting their ability to fulfil large-volume precision bearing orders within agreed delivery windows.

Opportunities - Growing Adoption in Medical Robotics and Surgical Systems

The medical robotics segment presents a compelling high-value growth opportunity for cross roller bearing manufacturers. Surgical robots, rehabilitation exoskeletons, and precision diagnostic imaging systems including CT scanners, MRI gantries, and C-arm imaging equipment demand bearings capable of delivering frictionless, repeatable motion in sterile or cleanroom environments. The International Federation of Medical and Biological Engineering (IFMBE) projects that global medical robotics installations will grow substantially through the late 2020s. The U.S. FDA has also accelerated clearance pathways for robotic-assisted surgical systems, enabling faster market entry for device manufacturers and correspondingly driving demand for high-precision cross roller bearings. This segment's premium pricing tolerance translates into favorable margins for specialized bearing suppliers.

Aerospace and Defense Modernization Programs Creating Sustained Demand

Governments globally are committing substantial resources to defense modernization and aerospace platform upgrades, creating a durable growth opportunity for the Cross Roller Bearings Market. Cross roller bearings are essential in satellite positioning mechanisms, radar antenna drives, missile guidance systems, and unmanned aerial vehicle (UAV) assemblies all of which require exceptional precision under extreme load and environmental conditions. NATO member states committed to increasing defense expenditure to 2% or above of GDP, with collective spending reaching approximately US$ 1.3 trillion in 2023. Similarly, India's Ministry of Defence announced a record INR 6.21 trillion defense budget for 2024–25, emphasizing indigenization. These programs are expected to sustain long-term procurement of precision components, including cross roller bearings, across aerospace and defense supply chains.

Category-wise Analysis

Product Type Insights

The Single Inner and Split Outer Ring segment holds the leading share in the cross-roller bearings market, accounting for approximately 55% of the overall product type segment. This dominance is attributable to the configuration's superior ease of installation and its compatibility with compact housing designs key requirements in robotics, medical imaging, and semiconductor handling equipment. The single inner ring design offers enhanced rigidity and facilitates torque transmission without compromising radial load capacity. Major producers including THK Co., Ltd. and NSK Ltd. have developed extensive product catalogues around this configuration. Furthermore, standardized outer ring dimensions enable direct interchangeability across multiple OEM platforms, reducing engineering design lead times and supporting widespread adoption in high-volume industrial automation applications globally.

Dimension Analysis

The 50 to 150 mm dimension segment commands the largest revenue share among all dimension categories in the cross-roller bearings market, representing approximately 34% of the total. This range is most widely applied across industrial robotic joints, CNC machine tool rotary tables, and compact automation modules arguably the highest-volume end-use applications. Bearings in this dimensional band offer an optimal balance between load capacity and compactness, making them universally applicable across manufacturing, semiconductor, and medical sectors. Published product data from THK Co., Ltd. and NSK Ltd. confirms that their highest-volume cross roller ring and cross roller bearing product lines fall within this dimensional range, reflecting consistent demand from global OEM customers in precision machinery and equipment manufacturing.

End-user Insights

The manufacturing & machinery segment is the leading end-user category in the cross-roller bearings market, holding a dominant share of approximately 38%. This segment encompasses CNC machining centres, rotary tables, grinding machines, and industrial automation equipment all of which require the multi-directional load-handling capability intrinsic to cross roller bearings. According to United Nations Industrial Development Organization (UNIDO), global manufacturing value added reached approximately US$ 16.8 trillion in 2022, with significant capital expenditure directed toward precision machinery upgrades. The increasing deployment of smart factories and Industry 4.0 initiatives as observed across Germany, Japan, China, and the United States further reinforces sustained demand from the manufacturing and machinery sector, cementing its position as the dominant end-user segment in this market.

Regional Insights

North America Cross Roller Bearings Market Trends

North America represents a significant market for cross roller bearings, led predominantly by the United States, which accounts for the bulk of regional demand. The region's growth is underpinned by substantial investments in semiconductor fabrication, driven by the U.S. CHIPS and Science Act, which allocated over US$ 52.7 billion to domestic chip manufacturing. This policy-driven expansion of fabrication facilities is directly stimulating procurement of precision motion components, including cross roller bearings, across wafer-handling and photolithography systems.

Additionally, robust defense and aerospace spending by the U.S. Department of Defense which maintained a budget exceeding US$ 886 billion in FY2024continues to drive demand for high-precision bearings in satellite systems, radar platforms, and UAVs. The region also benefits from a well-established innovation ecosystem, with companies like RBC Bearings Incorporated and Timken Company investing in advanced materials research and digital manufacturing capabilities to strengthen their competitive positions.

Europe Cross Roller Bearings Market Trends

Europe's cross roller bearings market is driven by the region's concentration of precision engineering, automotive manufacturing, and industrial automation expertise. Germany remains the dominant contributor, home to global bearing leaders such as Schaeffler AG and FAG Bearings, as well as a dense base of machine tool and robotics manufacturers. The European Chips Act (over €43 billion) is additionally spurring semiconductor equipment investments across Germany, the Netherlands, and France, driving downstream bearing demand.

Regulatory harmonization through EU Machinery Regulation (EU) 2023/1230 is pushing manufacturers to ensure higher safety and reliability standards in industrial machinery, indirectly supporting premium bearing specifications. United Kingdom and France are investing in aerospace and medical device manufacturing, while Spain is witnessing growing automation adoption in automotive assembly. These multi-sector drivers collectively sustain Europe's position as a significant revenue-generating region in the global cross roller bearings landscape.

Asia Pacific Cross Roller Bearings Market Trends

Asia Pacific is the leading regional market for cross roller bearings, fueled by the region's manufacturing scale, robotics adoption, and semiconductor expansion. China leads the region, with domestic robot density surpassing 392 units per 10,000 workers in manufacturing as of 2023 per IFR data, driving substantial cross roller bearing consumption. Japan contributes through its world-class precision machinery sector, home to market leaders THK Co., Ltd., NSK Ltd., NTN Corporation, and JTEKT Corporation.

India is emerging as a significant growth frontier, supported by the government's Production Linked Incentive (PLI) Scheme targeting electronics, semiconductors, and advanced manufacturing. The Cross Roller Bearings Market Size & Share Analysis projects robust regional growth, consistent with Asia Pacific's growing dominance as both a production hub and high-volume consumer of precision bearing components.

Competitive Landscape

The global cross roller bearings market exhibits a moderately consolidated structure, with the top five players collectively accounting for a substantial share of global revenues. Established multinationals such as NSK Ltd., THK Co., Ltd., Schaeffler AG, and SKF Group dominate through deep application expertise, extensive product portfolios, and global distribution networks. These leaders differentiate via continued R&D investment in advanced steel metallurgy, surface coating technologies, and digitally enabled predictive maintenance solutions. Emerging players from China, including C&U Group and Zhejiang Jinxin Technology Co., Ltd., are intensifying price-based competition, particularly in mid-range dimensional segments, while global leaders focus on value-added precision solutions for high-complexity applications in aerospace, medical, and semiconductor markets.

Key Developments:

- January 2025, Schaeffler AG announced the expansion of its Schweinfurt precision bearings production facility to increase manufacturing capacity for high-precision cross roller and slewing ring bearings serving robotics and semiconductor equipment customers.

- September 2023: NSK Ltd. unveiled a new generation of cross roller bearings featuring proprietary NN-series surface treatment technology to extend bearing service life by up to 30%, targeting medical equipment and semiconductor manufacturing customers.

Companies Covered in Cross Roller Bearings Market

- NSK Ltd.

- THK Co., Ltd.

- Schaeffler AG

- SKF Group

- JTEKT Corporation

- RBC Bearings Incorporated

- C&U Group

- NTN Corporation

- Koyo Bearings

- Timken Company

- FAG Bearings

- Zhejiang Jinxin Technology Co., Ltd.

Frequently Asked Questions

The global Cross Roller Bearings Market is valued at US$ 1.5 Bn in 2026 and is expected to reach US$ 1.9 Bn by 2033, advancing at a CAGR of 3.5% during the forecast period of 2026–2033, supported by increasing demand from robotics, semiconductor equipment, and medical device sectors.

The primary demand drivers include the rapid expansion of industrial robotics with global operational robot stock exceeding 3.9 million units per IFR 2023 data and the accelerated semiconductor fabrication investment triggered by the U.S. CHIPS and Science Act and the European Chips Act, both of which stimulate demand for ultra-precision cross roller bearings across wafer-handling and lithography systems.

The Single Inner and Split Outer Ring segment holds a leading share of approximately 55% in the Cross Roller Bearings Market. This configuration is preferred for its compact design, ease of integration, and versatility across robotic joints, semiconductor equipment, and medical imaging systems, with broad support across the product portfolios of THK Co., Ltd. and NSK Ltd.

Asia Pacific is the dominant region in the Cross Roller Bearings Market, accounting for the largest revenue share globally. China's robot density of 392 units per 10,000 manufacturing workers, Japan's role as home to world-leading bearing manufacturers including THK Co., Ltd. and NSK Ltd., and growing semiconductor investments across India and ASEAN collectively underpin regional market leadership.

The leading companies operating in the global Cross Roller Bearings Market include NSK Ltd., THK Co., Ltd., Schaeffler AG, SKF Group, JTEKT Corporation, RBC Bearings Incorporated, NTN Corporation, Timken Company, Koyo Bearings, FAG Bearings, C&U Group, and Zhejiang Jinxin Technology Co., Ltd.