- Communication Infrastructure & Services

- Critical Communication Market

Critical Communication Market Size, Share, and Growth Forecast, 2026 – 2033

Critical Communication Market by Solution Type (Hardware, Services, Software), Technology (Land Mobile Radio (LMR), Long-Term Evolution (LTE)), End-User (Public Safety & Government Agencies, Transportation & Logistics, Utilities, Mining & Industrial, Oil & Gas, Others), and Regional Analysis for 2026-2033

Critical Communication Market Share and Trends Analysis

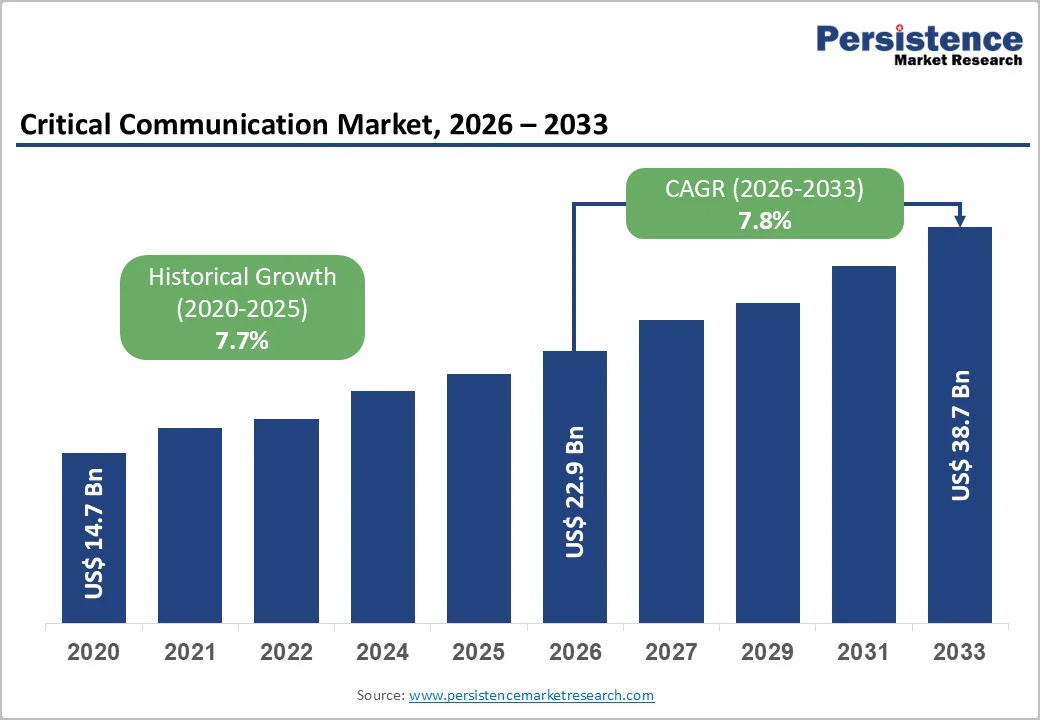

The global critical communication market size is likely to be valued at US$ 22.9 billion in 2026, and is projected to reach US$ 38.7 billion by 2033, growing at a CAGR of 7.8% during the forecast period 2026−2033. Mission-critical requirement for secure, resilient, and real-time communication systems across public safety, government, transportation, utilities, and industrial operations is the foremost factor favoring market expansion. The increasing frequency of natural disasters, cybersecurity threats, and infrastructure emergencies has elevated the strategic importance of interoperable communication platforms. Governments worldwide continue to modernize legacy networks, transitioning from land mobile radio (LMR) systems to long-term evolution (LTE) and broadband-enabled mission-critical services. Regulatory mandates emphasizing network reliability, redundancy, and spectrum efficiency further accelerate adoption. Technological convergence between hardware, software, and managed services enables scalable deployments and ensures operational continuity across diverse mission-critical environments.

Key Industry Highlights

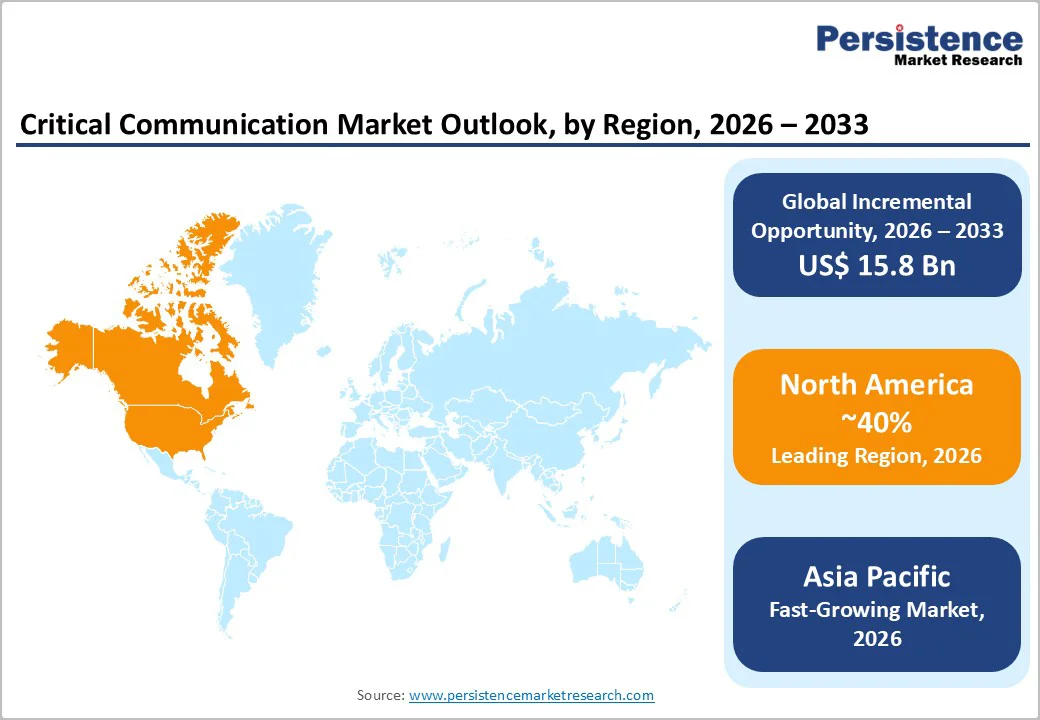

- Dominant Region: North America is predicted to hold a dominant 40% market share in 2026, driven by strong public safety investments and advanced mission-critical communication infrastructure.

- Fastest-growing Market: Asia Pacific is forecasted to be the fastest-growing market from 2026 to 2033, supported by expanding transportation and industrial infrastructure and increasing government initiatives for network modernization.

- Leading End-User: Public safety and government agencies are likely to lead with around 50% market share in 2026, powered by emergency network modernization, regulatory mandates, and sustained mission-critical infrastructure investments.

- Fastest-growing End-User: Transportation and logistics are slated to grow the fastest through 2033, owing to increasing investments in rail, airport, and port infrastructure.

- Key Drivers: Rising demand for secure and reliable real-time communication, increasing public safety and government investments, modernization of legacy networks, and adoption of broadband and 5G-based mission-critical technologies are primarily taking the market forward.

- December 2025: Google and RapidSOS enabled live video streaming from Android devices during 911 emergency calls, allowing dispatchers to receive real-time visual context for faster, more informed responses.

| Key Insights | Details |

|---|---|

| Critical Communication Market Size (2026E) | US$ 22.9 Bn |

| Market Value Forecast (2033F) | US$ 38.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Public Safety and Homeland Security Expenditure

Rising public safety and homeland security expenditure acts as a primary growth catalyst as governments prioritize uninterrupted command, control, and response capabilities across emergency services. Large-scale investments target communication reliability under extreme conditions, secure data exchange, and real-time coordination among police, fire, medical, and disaster response agencies. These spending patterns reflect a shift from basic voice systems toward integrated platforms that support situational awareness, encrypted broadband, and inter-agency interoperability aligned with national security objectives.

Budget expansion is driven by risk exposure linked to urbanization, critical infrastructure density, and asymmetric threats that demand faster decision cycles. According to the Stockholm International Peace Research Institute (SIPRI), global defense and security-related spending reached approximately US$ 2.4 trillion in 2023, reinforcing sustained funding momentum for advanced communication frameworks. Capital allocation focuses on network resilience, spectrum optimization, and lifecycle-managed systems that reduce operational failure during crises. This financial commitment strengthens procurement pipelines and accelerates technology upgrades across public safety ecosystems.

Spectrum Scarcity and Regulatory Hurdles

Spectrum scarcity and regulatory hurdles constrain deployment timelines and investment certainty across mission-critical communication ecosystems. Finite availability of dedicated frequency bands limits capacity for high-reliability, low-latency services required by emergency response and infrastructure operations. Allocation processes often prioritize commercial broadband use, leaving fragmented or congested spectrum for specialized applications. Licensing frameworks vary widely across regions, creating compliance complexity for multinational deployments. Long approval cycles, auction-driven pricing models, and inconsistent spectrum harmonization raise capital requirements and delay network rollouts, weakening operational readiness during high-risk scenarios.

Regulatory constraints further shape technology choices and network architecture decisions. Strict mandates on data sovereignty, encryption standards, and lawful interception increase system design costs and slow innovation cycles. Cross-border interoperability faces barriers where technical standards and spectrum policies lack alignment. Legacy regulatory structures struggle to keep pace with convergence of Land Mobile Radio and broadband technologies, reducing flexibility for hybrid deployments. These structural limitations restrict scalability, impede rapid modernization, and elevate total cost of ownership, placing pressure on public agencies and enterprises seeking resilient, future-ready communication capabilities.

Emergence of 5G MCX and AI Integration

The emergence of 5G mission-critical services (MCX) and artificial intelligence (AI) integration creates a strategic opportunity by redefining operational performance across high-risk environments. Ultra-low latency, network slicing, and enhanced uplink capabilities enable instant voice, video, and data exchange under extreme conditions. These capabilities support situational awareness through real-time video feeds, geolocation tracking, and data-rich command interfaces. AI-driven analytics enhance decision accuracy by processing vast data streams, identifying anomalies, and prioritizing alerts in time-sensitive scenarios. This convergence supports faster response coordination while maintaining service continuity during peak demand or network stress.

5G MCX combined with AI accelerates digital transformation by enabling automation, predictive intelligence, and scalable service models. For example, in October 2025, Tidal Wave and Consort Digital successfully piloted 5G-enabled mission-critical communications at Amlohri Coal Mine using Consort's MCX ONE platform on Tidal Wave's private 5G network, integrated with drones, cameras, and sensors. AI-powered network management optimizes spectrum use, predicts equipment failure, and strengthens cyber resilience. Intelligent edge computing reduces dependency on centralized infrastructure, ensuring uninterrupted performance in remote or disaster-affected areas. These advancements elevate operational efficiency, reduce human error, and support evolving regulatory expectations for reliability and resilience. The integration positions communication ecosystems as intelligent platforms rather than basic connectivity tools, driving long-term value creation for public and industrial stakeholders.

Category-wise Analysis

Solution Type Insights

Hardware is likely to be the leading segment with an estimated 45% of the critical communication market revenue share in 2026, supported by sustained investments in mission-critical radios, base stations, and core network infrastructure. Public safety and government entities require ruggedized, standards-compliant equipment designed for uninterrupted performance in harsh environments. Long replacement cycles, mandatory certifications, and nationwide network modernization programs reinforce consistent hardware procurement and revenue stability. Growing integration of advanced features such as broadband compatibility and IoT-ready modules further strengthens the demand for hardware.

Services are anticipated to be the fastest-growing segment from 2026 to 2033, driven by rising operational complexity and the shift toward outsourced expertise. Organizations increasingly rely on managed services, system integration, lifecycle support, and cybersecurity oversight to maintain resilient operations. As networks evolve toward broadband and software-centric architectures, demand for specialized service capabilities expands, strengthening recurring revenue models and long-term vendor engagement. Enhanced adoption of predictive maintenance and real-time monitoring solutions is expected to accelerate service segment expansion.

Technology Insights

LMR is poised to dominate with a forecasted market share of 60% in 2026, powered by proven reliability, extensive deployment across public safety agencies, and critical role in mission-critical voice communications. LMR networks provide uninterrupted connectivity in extreme conditions, supporting voice, group calling, and emergency alerts efficiently. Its interoperability with legacy systems ensures smooth operations during multi-agency coordination. Agencies continue to invest in ruggedized, certified devices and network infrastructure. Long replacement cycles and strong familiarity with LMR technology sustain consistent procurement and reinforce its dominance in mission-critical environments.

LTE is estimated to be the fastest-growing segment from 2026 to 2033, fueled by broadband capabilities, multimedia support, standardization, and increasing adoption for modernized critical communication networks. LTE enables high-speed data, real-time video streaming, geolocation, and sensor integration, enhancing situational awareness and operational efficiency. Organizations are upgrading legacy networks to LTE for scalable, interoperable, and future-ready systems. The technology’s adaptability, coupled with growing demand for network flexibility and advanced analytics, positions LTE as the backbone for evolving mission-critical communication infrastructures.

End-User Insights

Public safety and government agencies are anticipated to secure around 50% of the revenue share in 2026, supported by continuous modernization programs, regulatory mandates, and the need for reliable mission-critical communication systems. These agencies require resilient and interoperable networks to ensure effective emergency response, law enforcement coordination, and disaster management. Investment in advanced radios, network infrastructure, and software solutions ensures uninterrupted operations. Long-term procurement cycles and stringent compliance requirements reinforce their market dominance, while ongoing upgrades to legacy systems maintain operational efficiency and strengthen public safety capabilities across urban and remote regions.

Transportation and logistics are expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by expanding rail networks, airports, and port infrastructure. Organizations increasingly adopt real-time communication systems to improve fleet coordination, enhance passenger safety, and optimize operational workflows. The huge demand for integrated voice, data, and tracking solutions supports efficiency across complex transport networks. Investments in broadband-enabled and AI-assisted communication technologies further accelerate growth. As logistics operations become more automated and safety-critical, this segment is poised for significant expansion across developed and emerging markets.

Regional Insights

North America Critical Communication Market Trends

North America is projected to lead with roughly 40% of the critical communication market share in 2026, supported by robust public safety investments and consistent government funding for next-generation networks. This dominance stems from mature infrastructure that seamlessly integrates LMR systems with LTE broadband, ensuring high reliability and interoperability among diverse agencies. Furthermore, the region is rapidly adopting advanced technologies such as Artificial Intelligence (AI)-assisted analytics and real-time data sharing, which enhance situational awareness and operational responsiveness during emergencies. For stakeholders, this environment encourages the modernization of legacy systems, creating a stable foundation for deploying resilient, scalable platforms that meet stringent regulatory mandates.

Beyond public safety, North America strengthens its leadership further through deep, long-term collaborations between technology providers and emergency response organizations, accelerating the rollout of mission-critical solutions. Integration with broader initiatives such as industrial automation, smart transportation, and smart city projects further boosts network redundancy and operational efficiency across sectors. These convergent trends not only drive sustained growth but also foster a climate of continuous technological advancement. Companies operating in this space should focus on delivering interoperable, data-driven tools that align with these modernization efforts to capture emerging opportunities in this highly developed market.

Europe Critical Communication Market Trends

Europe is expected to maintain a strong position in the critical communication market through extensive government initiatives and regulatory frameworks that prioritize network reliability, redundancy, and cross-agency interoperability. Public safety agencies, transportation authorities, and utility operators are replacing outdated systems with LTE and broadband-enabled solutions to improve operational efficiency and ensure uninterrupted communication during crises. Investments flow into advanced radios, software platforms, and managed services that deliver robust mission-critical connectivity across both densely populated urban centers and challenging remote locations. For vendors and system integrators, this modernization wave presents opportunities to provide compliant, future-ready infrastructure that aligns with stringent European standards and enhances emergency coordination capabilities.

Several key factors underpin the Europe critical communication market growth, including a strong emphasis on standardization and seamless cross-border interoperability that enables multinational response efforts. The integration of communication networks with smart city and industrial infrastructure creates synergies that boost overall system performance and situational intelligence. Widening adoption of AI-driven network management, predictive maintenance tools, and advanced cybersecurity measures strengthens service reliability and operational resilience against evolving threats. The deployment of private networks for utilities, transportation, and defense sectors enhances control and performance, ensuring that communication platforms meet rigorous regulatory and operational requirements while supporting efficient multi-sector coordination and safety.

Asia Pacific Critical Communication Market Trends

Asia Pacific is forecasted to be the fastest-growing regional market for critical communication between 2026 and 2033, stimulated by rapid urbanization, industrial expansion, and large-scale infrastructure development. Governments and enterprises are prioritizing modernization of legacy communication networks to support public safety, transportation, and industrial operations. Rising adoption of LTE and broadband-enabled mission-critical solutions, combined with investments in private 5G networks, accelerates deployment of advanced voice, data, and video communication systems. Integration of artificial intelligence and IoT-enabled monitoring enhances real-time operational efficiency and predictive maintenance, strengthening network performance and service reliability.

Key factors driving Asia Pacific growth include increasing government funding for emergency response modernization, strategic public-private partnerships, and rising focus on cybersecurity and network resilience in industrial and urban centers. Emerging economies are implementing standardized, interoperable communication protocols to support multi-agency coordination during disasters and high-demand events. Expansion of smart city projects, logistics networks, and connected industrial systems stimulates demand for robust, scalable communication solutions that enhance operational efficiency and safety.

Competitive Landscape

The global critical communication market structure is moderately consolidated, with the top five players controlling approximately 50% of revenue, reflecting a balance between established vendors and emerging competitors. Key players include Motorola Solutions, Inc., Nokia, Ericsson, Airbus, Harris Technologies, Inc., and Thales, who maintain competitive positioning through technology leadership, regulatory compliance, and service capabilities. Leading companies differentiate themselves through advanced technology offerings, including mission-critical radios, LTE and broadband solutions, and AI-enabled network management.

The critical communication market continues to grow as vendors expand their portfolios across hardware, software, and managed services to meet evolving demands. Their presence, extensive client networks, and research and development initiatives enable scalable, interoperable, and future-ready communication platforms. Adoption of AI-driven network analytics, predictive maintenance, and cybersecurity solutions further strengthens operational efficiency.

Key Industry Developments

- In November 2025, HMD Secure partnered with Dutch connectivity innovator Lyfo to provide mission-critical and business-critical users with seamless borderless communication. The collaboration integrates Lyfo's intelligent network-switching software into HMD's rugged, European-built hardware, ensuring devices automatically connect to the strongest available mobile network for uninterrupted connectivity.

- In November 2025, C-DOT teamed up with NAM InfoCom under its MCX Alliance to co-develop a 3GPP-compliant mission critical communication solution featuring Mission Critical Push-to-Talk (MCPTT), Mission Critical Data (MCData), and enhanced Mission Critical Video (MCVideo) for 4G/5G networks. NAM InfoCom will create the MCVideo module with multi-stream support, recording, group calling, and floor control to meet Public Protection and Disaster Relief (PPDR) needs.

- In September 2025, Nokia launched the Mission-Safe Phone, a rugged, military-grade smartphone designed for defense and public safety with MIL-STD-810H/IP68 certification, supporting encrypted 4G/5G broadband and high-bandwidth mission-critical push-to-talk (PTT). It integrates with Nokia's Banshee tactical radios to enable secure multimedia communications in extreme environments.

Frequently Asked Questions

The global critical communication market is projected to reach US$ 22.9 billion in 2026.

The growing demand for secure, reliable, and real-time communication systems across public safety, government, transportation, utilities, and industrial sectors is driving the market.

The market is poised to witness a CAGR of 7.8% from 2026 to 2033.

Increasing adoption of 5G mission-critical services, AI-enabled network intelligence, private broadband networks, and modernization of legacy communication infrastructure across public safety and industrial sectors.

Some of the key market players include Motorola Solutions, Inc., Nokia, Ericsson, Airbus, and Harris Technologies, Inc.