- Pharmaceuticals

- Controlled Substance API Market

Controlled Substance API Market Size, Share, and Growth Forecast, 2026 – 2033

Controlled Substance API Market by Product Type (Opioids, Stimulants, Depressants, Cannabinoids, Others), Application (Pain Management, ADHD & Cognitive Disorders, Anxiety/Depression Treatment, Opioid Dependence Therapy, Other Medical Uses), End-User (Pharmaceutical Manufacturers, Research Laboratories, CMOs, Hospitals & Clinics), and Regional Analysis for 2026-2033

Controlled Substance API Market Share and Trends Analysis

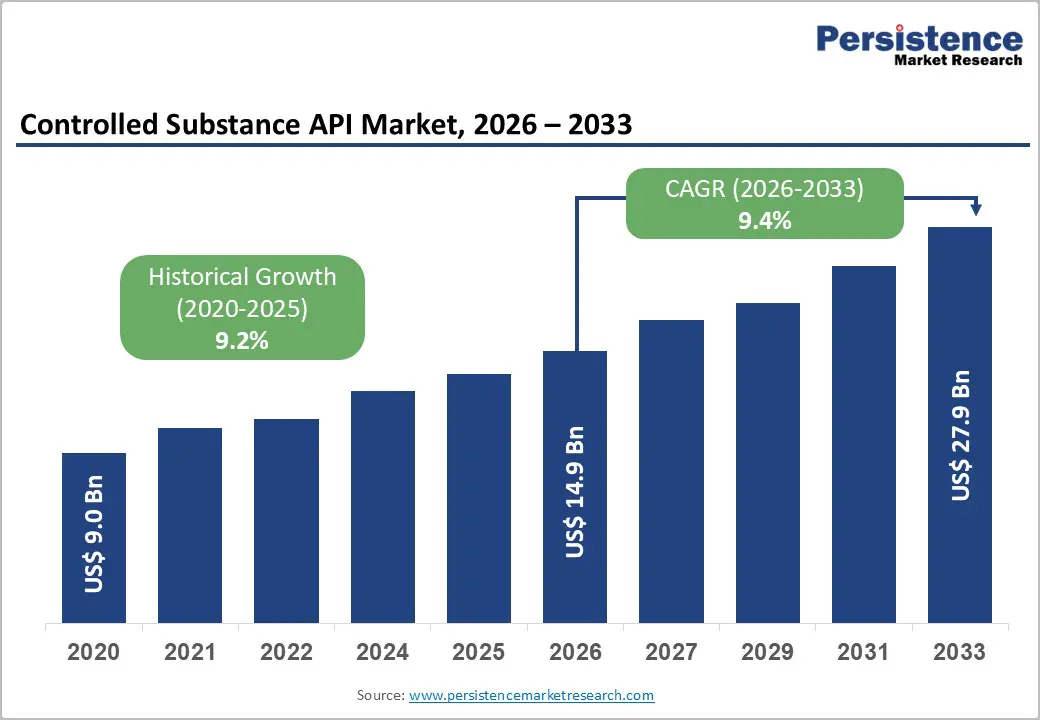

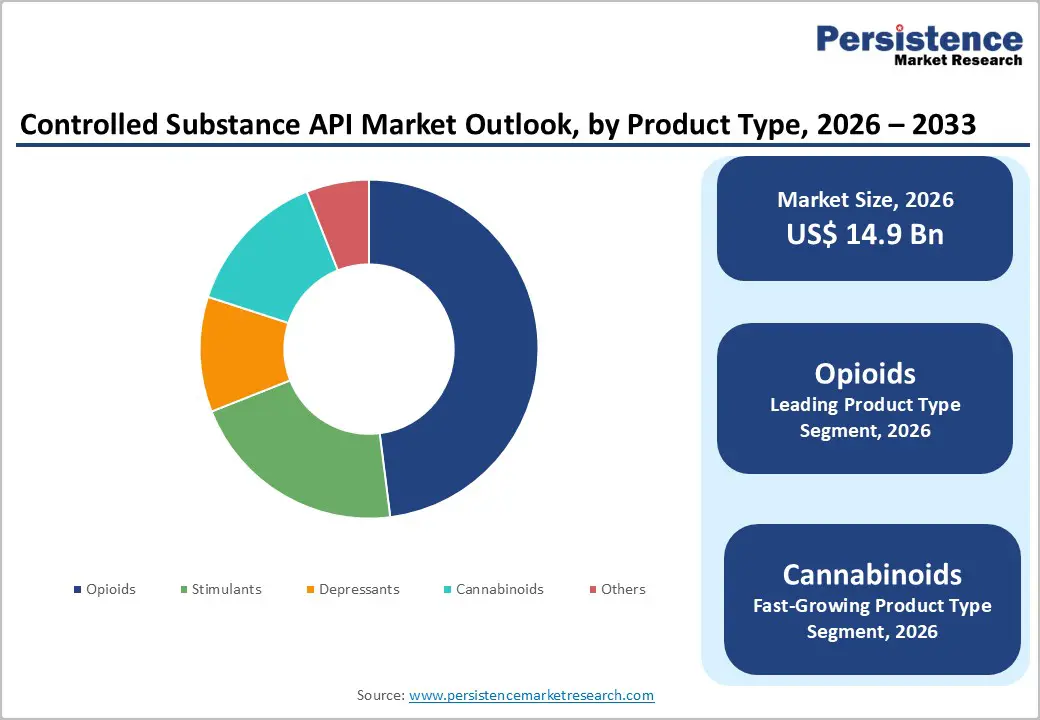

The global controlled substance API market size is likely to be valued at US$ 14.9 billion in 2026, and is projected to reach US$ 27.9 billion by 2033, growing at a CAGR of 9.4% during the forecast period 2026−2033.

The market demonstrates structurally resilient growth as controlled-substance active pharmaceutical ingredients (APIs) remain integral to the treatment of pain, neurological disorders, mental health conditions, and substance dependence. Expansion reflects sustained demographic aging, rising chronic disease prevalence, and continued clinical reliance on regulated pharmacological interventions. Increasing clinical awareness around evidence-based pain management and neuropsychiatric treatment reinforces long-term demand stability across inpatient and outpatient care settings. Treatment adoption remains supported by formal clinical guidelines issued by regulatory and public health authorities, which preserve the role of controlled substances within clearly defined therapeutic pathways.

Key Industry Highlights

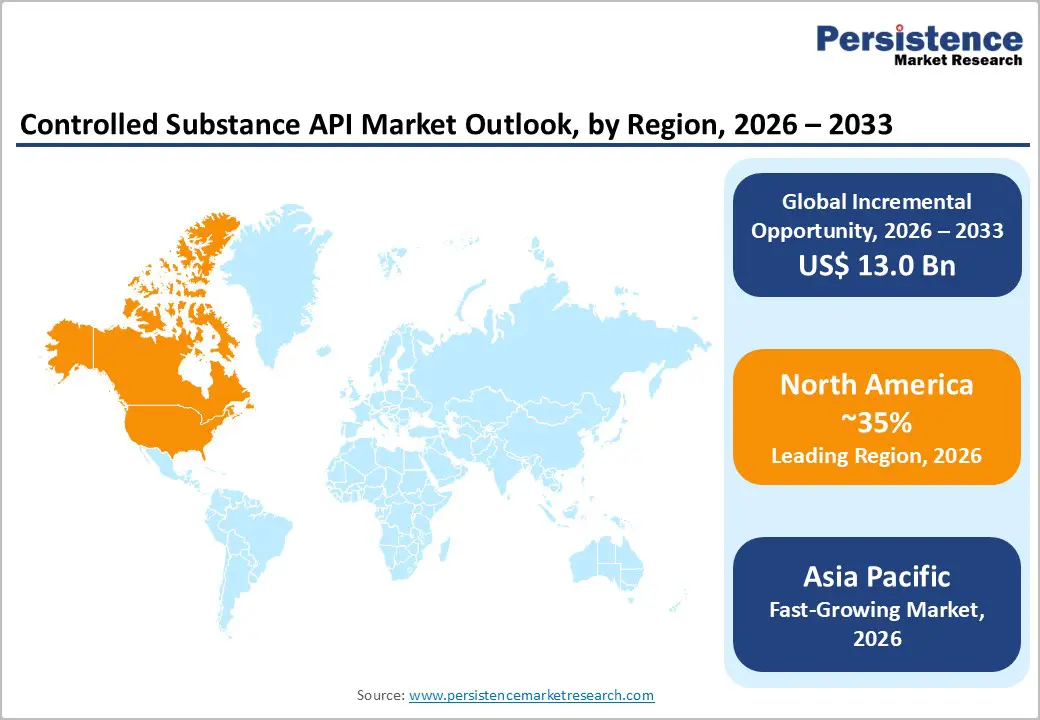

- Regional Dominance: North America is set to dominate in 2026 with a 35% share, driven by strong healthcare systems, advanced manufacturing, and digital prescription management.

- Fastest-growing Market: Asia Pacific is projected to be the fastest-growing market through 2033, supported by expanding healthcare infrastructure and rising chronic pain cases.

- Product Type Leadership: Opioids are likely to lead with about 48% revenue share in 2026, anchored in clinical reliance and standardized treatment protocols.

- Fastest-growing Product Type: Cannabinoids are slated to grow the fastest between 2026 and 2033, fueled by regulatory clarity, clinical trial expansion, and formulation innovation.

| Global Market Attributes | Key Insights |

|---|---|

| Controlled Substance API Market Size (2026E) | US$ 14.9 Bn |

| Market Value Forecast (2033F) | US$ 27.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expansion of Regulated Pharmacotherapy for Pain and Neurological Disorders

The widening clinical adoption of tightly governed drug-based interventions for pain and neurological conditions stands as a structural growth catalyst across pharmaceutical supply chains. Chronic pain syndromes, epilepsy, Parkinson disease, attention-deficit hyperactivity disorder, and refractory psychiatric conditions continue to demand pharmacological agents with high efficacy, predictable pharmacokinetics, and centrally mediated action. Many first-line and second-line therapies within these indications fall under controlled scheduling frameworks due to neuroactive profiles and dependence risk. Health authorities increasingly favor standardized pharmacotherapy pathways over fragmented treatment models, reinforcing consistent prescribing practices within licensed medical settings. This approach elevates demand for high-purity, regulation-compliant active pharmaceutical ingredients that meet stringent traceability, security, and quality benchmarks.

Regulatory normalization further accelerates scale by converting historically restricted compounds into mainstream therapeutic assets under supervised use. Governments and clinical bodies recognize untreated pain and neurological disorders as drivers of disability burden and productivity loss, prompting structured access programs anchored in pharmacotherapy. According to the World Health Organization (WHO), neurological disorders affect more than 3 billion people globally, positioning these conditions among the leading causes of disability worldwide, supported by epidemiological assessments published in global burden studies. This clinical magnitude incentivizes long-term investment in regulated manufacturing pipelines capable of supporting continuous therapy demand. Controlled status reinforces barriers to informal substitution, securing legitimate supply channels while limiting volatility. Pharmaceutical manufacturers respond through capacity expansion, backward integration, and compliance-driven sourcing strategies, reinforcing volume stability.

Stringent Regulatory Oversight and Quota Restrictions

Intensive regulatory supervision combined with production quota controls functions as a structural barrier that limits operational flexibility across controlled active pharmaceutical ingredient supply chains. Oversight frameworks mandate multi-layer licensing, pre-approval of manufacturing volumes, continuous audit readiness, and strict documentation aligned with narcotics control laws. These obligations extend development and scale-up timelines, elevate fixed compliance expenditure, and restrict rapid response to fluctuations in therapeutic demand. Annual quota allocations impose hard ceilings on output volumes independent of downstream requirements, constraining capacity utilization and weakening incentives for long-term investment in advanced manufacturing infrastructure.

Quota administration also introduces friction within international supply networks. Export authorizations, jurisdiction-specific reporting, and treaty-driven reconciliation processes fragment manufacturing and distribution planning, increasing coordination costs across regions. Smaller and mid-sized producers experience amplified pressure as regulatory overhead absorbs a larger share of operating resources, limiting competitive participation and reinforcing supplier concentration. Innovation pathways narrow under such conditions, as process optimization and yield enhancement deliver limited commercial return when production volumes remain capped. The cumulative outcome reflects constrained availability, elongated lead times, and elevated cost structures embedded within regulated compounds.

Emerging Therapeutic Applications and Novel Formulations

Broadening therapeutic scope combined with advanced formulation development represents a structurally strong growth lever within regulated active pharmaceutical ingredients. Clinical research pipelines increasingly focus on complex neurological, psychiatric, and pain-related conditions that require tightly controlled pharmacological profiles. These conditions demand active ingredients with validated efficacy, predictable pharmacokinetics, and regulatory traceability, creating a favorable environment for regulated compounds with established clinical familiarity. Innovation activity in mental health, palliative care, anesthesia optimization, and substance use disorder management aligns with this requirement.

Formulation innovation further amplifies this opportunity through differentiation rather than volume expansion. Novel delivery systems such as extended-release matrices, abuse-deterrent formats, transdermal systems, and precision-dose injectables address safety, adherence, and regulatory expectations simultaneously. These advancements improve therapeutic control while supporting lifecycle extension strategies for pharmaceutical developers. Regulated active ingredients benefit from this shift since formulation science enables repositioning within modern treatment protocols without reliance on new molecular discovery. Regulatory preference for risk-mitigated delivery profiles enhances investment confidence and accelerates adoption across institutional healthcare settings.

Category-wise Analysis

Product Type Insights

Opioids are likely to be the leading segment with a dominant revenue share of approximately 48% in 2026, due to established clinical reliance in pain management and perioperative care. Opioid APIs remain deeply integrated within standardized treatment protocols for acute pain, cancer-related pain, trauma management, and post-surgical recovery across global healthcare systems. Long-standing clinical familiarity supports confident prescribing within regulated settings, supported by predictable pharmacodynamic profiles and well-defined dosing frameworks.

Inclusion within essential medicines listings sustains institutional procurement across public and private healthcare infrastructures. Hospital formularies, surgical centers, and emergency care units continue to require consistent supply to ensure continuity of care.

Cannabinoids are expected to witness the fastest growth between 2026 and 2033, as regulatory acceptance expands for neurological and pain-related indications. Evolving regulatory clarity surrounding medical cannabinoid derivatives strengthens confidence among pharmaceutical developers and healthcare providers. Structured approval pathways enable broader clinical trials, formulation innovation, and standardized dosing development. Increased investment in neurological disorder research and chronic pain therapies accelerates pipeline activity. Physician training programs and updated clinical guidelines improve prescriber comfort within compliant medical frameworks. Rising patient awareness and acceptance further support uptake across targeted indications.

Application Insights

Pain management is poised to lead with a forecasted 40% of the controlled substance API market revenue share in 2026, owing to the high volume of prescriptions for chronic and postoperative conditions. Clinical credibility is reinforced by extensive evidence supporting opioid and other regulated APIs for safe and effective pain relief. Hospitals, surgical centers, and outpatient clinics rely on standardized protocols to manage acute and chronic pain efficiently. Provider referrals remain robust within multidisciplinary care frameworks, integrating physicians, pharmacists, and pain specialists. Digitalization of prescribing enhances treatment monitoring, dosage accuracy, and patient accessibility.

Opioid dependence therapy is anticipated to be the fastest-growing segment between 2026 and 2033, driven by public health initiatives addressing addiction crises. Treatment protocols increasingly utilize controlled APIs for substitution therapy, maintenance programs, and relapse prevention. Structured programs improve cost efficiency by optimizing dosing schedules and reducing hospitalization rates. Integration of long-acting formulations and technology-enabled delivery systems supports patient adherence and real-time monitoring. Public health campaigns, combined with clinical training and updated regulatory guidance, strengthen adoption across healthcare facilities.

End-User Insights

Pharmaceutical manufacturers are positioned as the leading segment with nearly 50% market share in 2026, supported by in-house integration of APIs into final dosage forms. Direct control over quality, compliance, and supply chain processes strengthens clinical credibility and ensures adherence to regulatory standards. Vertical integration allows streamlined coordination between API production and formulation, reducing lead times and minimizing production risks. Operational efficiency benefits from economies of scale, optimized resource allocation, and predictable procurement cycles. Ownership of intellectual property and proprietary processes supports differentiated product offerings.

Contract manufacturing organizations (CMOs) are expected to emerge as the fastest-growing segment between 2026 and 2033, driven by outsourcing trends among innovators seeking specialized expertise.

Increasing demand for scalable, flexible manufacturing solutions supports expansion across diverse therapeutic areas. CMOs provide access to advanced technology platforms, regulatory compliance frameworks, and specialized formulation capabilities without requiring capital-intensive infrastructure from innovators.

Global networks enhance accessibility, supply chain resilience, and geographic reach. Technology-enabled service delivery, including secure API handling, real-time tracking, and integrated quality monitoring, improves operational efficiency.

Regional Insights

North America Controlled Substance API Market Trends

North America is estimated to hold over 35% of the controlled substance API market share in 2026, reflecting strong integration of controlled therapies within established healthcare systems and robust regulatory oversight. High prevalence of chronic pain, neurological disorders, and perioperative requirements drives steady demand for opioids, stimulants, and other regulated APIs. Advanced manufacturing infrastructure, coupled with in-house production by leading pharmaceutical companies, ensures consistent quality, compliance, and supply chain reliability.

Adoption of digital prescription management and electronic health record systems enhances monitoring, reduces diversion risk, and reinforces clinical confidence. Investment in research and development for novel therapeutic applications further strengthens utilization and market stability, positioning the regional market as a central hub for controlled substance APIs.

Clinical familiarity and sophisticated care networks amplify dominance by sustaining baseline utilization across hospitals, surgical centers, and outpatient programs. Structured treatment protocols, combined with long-term procurement agreements, ensure predictable consumption of regulated therapies. Reimbursement frameworks across public and private healthcare segments support widespread adoption of chronic and acute pain management solutions. Integration of advanced formulation technologies, including extended-release and abuse-deterrent systems, increases treatment efficacy and adherence. Collaborative initiatives among research institutions, pharmaceutical developers, and contract manufacturers accelerate innovation while maintaining regulatory compliance.

Europe Controlled Substance API Market Trends

Europe holds a significant position in the market for controlled substance APIs, driven by stringent regulatory frameworks, advanced healthcare infrastructure, and high clinical adoption of controlled therapies. Governments enforce comprehensive scheduling, monitoring, and compliance protocols, ensuring safe production, distribution, and prescription of opioids, stimulants, and other regulated APIs. Hospitals, specialty clinics, and research institutions maintain structured treatment pathways for chronic pain, perioperative care, and neurological disorders, supporting consistent demand.

Integration of electronic prescription systems and prescription drug monitoring programs enhances safety, adherence, and accountability in clinical use. Established pharmaceutical manufacturers benefit from well-defined regulatory pathways, which reduce uncertainty in product development and market entry.

Innovation and targeted therapeutic adoption further reinforce market relevance. Investment in abuse-deterrent formulations, extended-release delivery systems, and precision-dosing technologies addresses safety, regulatory compliance, and patient adherence requirements. Public health initiatives targeting opioid dependence and chronic pain management expand structured use of controlled APIs within hospital and outpatient networks.

Strategic collaborations between research institutions, pharmaceutical developers, and contract manufacturing organizations accelerate clinical development and rollout of novel therapeutic applications. Cross-border regulatory harmonization within the European Union facilitates broader access and supports multi-country clinical studies.

Asia Pacific Controlled Substance API Market Trends

Asia Pacific is forecasted to be the fastest-growing regional market for controlled substance APIs between 2026 and 2033, powered by expanding healthcare infrastructure, rising prevalence of chronic pain and neurological disorders, and evolving regulatory frameworks. Rapid urbanization and increased public and private healthcare investment enable wider adoption of advanced therapeutic protocols, driving demand for controlled APIs across perioperative care, pain management, and opioid dependence therapy.

Government-led initiatives and mental health programs integrate these APIs into structured treatment pathways, while growing physician and patient awareness supports clinical acceptance. Entry of multinational pharmaceutical manufacturers and contract organizations into regional production hubs ensures supply reliability and cost-efficient distribution.

Technological adoption and formulation innovation further reinforce rapid growth in the region. Implementation of digital prescription management, telemedicine integration, and adherence monitoring enhances safe, efficient utilization of controlled APIs. Development of long-acting, abuse-deterrent, and precision-dose formulations addresses safety and compliance concerns, improving provider confidence and patient outcomes. Outsourcing trends allow pharmaceutical innovators to leverage contract manufacturing organizations for scalable production and regulatory support, reducing capital expenditure and operational risk. Rising healthcare expenditure, expanding insurance coverage, and growing patient access increase consumption of advanced therapies.

Competitive Landscape

The global controlled substance API market structure reflects moderate concentration with a limited number of compliance-capable manufacturers controlling a substantial share. Companies with proven expertise in producing controlled substance APIs dominate due to the high regulatory and operational barriers associated with manufacturing. Production requires strict adherence to scheduling, traceability, and quality standards, which limits participation to manufacturers with robust compliance infrastructure.

Key players including Noramco Inc., Johnson Matthey Plc, Mallinckrodt Pharmaceuticals, Pfizer Inc., and Sun Pharmaceutical Industries Ltd. maintain vertically integrated operations or specialized contract capabilities, ensuring consistent supply and quality control. Their established presence in hospitals, research institutions, and pharmaceutical development pipelines reinforces market dominance, while the high cost of entry and regulatory scrutiny discourages new entrants.

Competitive positioning emphasizes regulatory track record, manufacturing scale, and long-term supply reliability as critical differentiators. Companies leverage experience in handling controlled APIs to secure approvals, certifications, and partnerships with global pharmaceutical developers. Large-scale production capabilities enable optimization of operational efficiency, reduce unit costs, and support development of advanced formulations such as extended-release or abuse-deterrent systems.

Long-term supply agreements and robust logistics networks mitigate risk of shortages, ensuring continuity for critical therapies. Innovation pipelines are supported by strong compliance frameworks, allowing integration of APIs into emerging therapeutic applications without regulatory delays.

Key Industry Developments

- In January 2026, Khona Scientific and Benuvia Operations signed a Letter of Intent to collaborate on biosynthetic pathway development for controlled substance active pharmaceutical ingredients, aiming to evaluate scalable, compliant manufacturing approaches that strengthen pharmaceutical supply chain resilience.

- In December 2025, Supriya Lifescience commissioned Module E at its Indore facility, adding 335 KL of multipurpose API capacity, a 50%+ total increase, featuring advanced automation and safety systems for regulated, high-value markets such as anti-histamines and anesthetics.

The export-driven firm is targeting 33-35% EBITDA margins, aiming to launch 3-4 complex products yearly via dual R&D centers. - In October 2025, Cambrex invested US$ 120 million to expand API manufacturing at its Charles City, Iowa facility by 40%, nearing 1 million liters capacity for small molecule and peptide therapeutics.

This supports U.S. supply chain reshoring amid strong customer demand, building on prior expansions in high-potent APIs, rare disease manufacturing, and peptide production.

Companies Covered in Controlled Substance API Market

- Noramco Inc.

- Johnson Matthey Plc

- Mallinckrodt Pharmaceuticals

- Pfizer Inc.

- Sun Pharmaceutical Industries Ltd.

- Renaissance Lakewood, LLC

- Cambridge Isotope Laboratories, Inc.

- Siegfried Holding AG

- Lannett Company, Inc.

- Alkermes plc

Frequently Asked Questions

The global controlled substance API market is projected to reach US$ 14.9 billion in 2026.

Rising clinical demand for pain management, neurological and psychiatric therapies, combined with regulatory-compliant manufacturing advancements, drives the market.

The market is poised to witness a CAGR of 9.4% from 2026 to 2033.

Expansion of healthcare access in emerging economies and development of controlled-release or abuse-deterrent formulations represent key opportunities in the market.

Noramco Inc., Johnson Matthey Plc, Mallinckrodt Pharmaceuticals, Pfizer Inc., and Sun Pharmaceutical Industries Ltd. are a few of the key players in the market.