- Off-Road Equipment & Machinery

- Concrete Vibrator Market

Concrete Vibrator Market Size, Share, Trends, Growth, Regional Forecasts 2025 - 2032

Concrete Vibrator Market by Product (Internal Concrete Vibrator, External Concrete Vibrator, Others), End-use (Residential Construction, Commercial Construction, Industrial & Industrial & Infrastructure), Power Source (Electric, Pneumatic, Hydraulic, Petrol/Diesel), and Regional Analysis 2025 - 2032

Concrete Vibrator Market Share and Trends Analysis

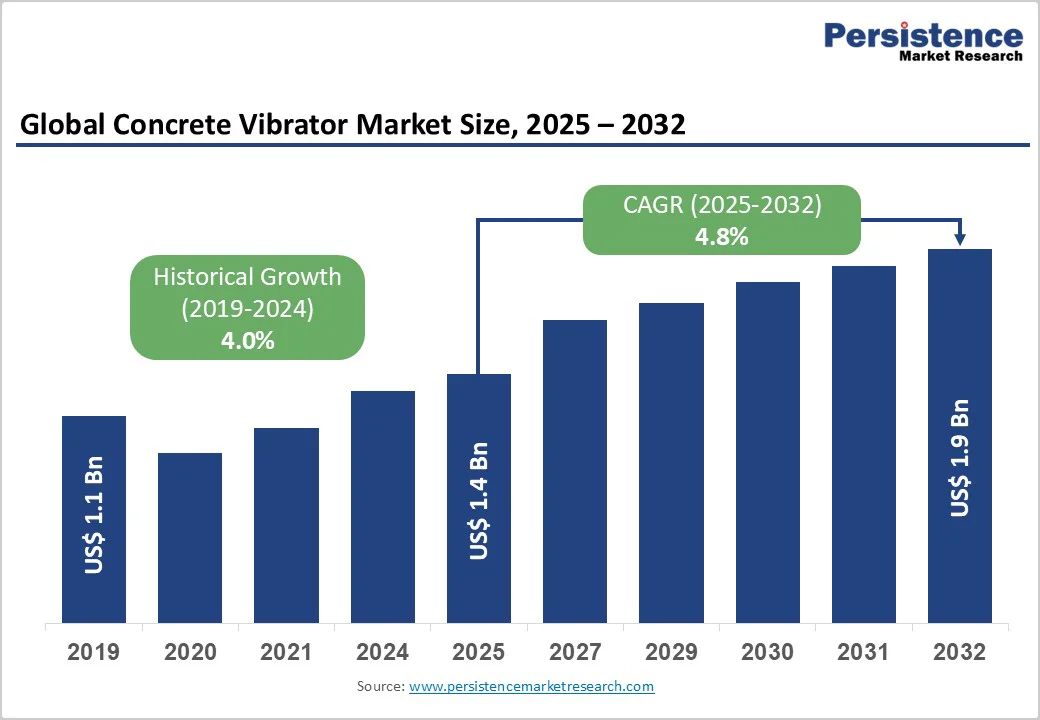

The global concrete vibrator market size is likely to value at US$ 1.4 billion in 2025 and is projected to reach US$ 1.9 billion by 2032, growing at a CAGR of 4.8% between 2025 and 2032. This robust expansion is primarily driven by accelerating urbanization trends, substantial government infrastructure investments, and the escalating demand for high-quality concrete consolidation in construction projects worldwide. The increasing adoption of ready-mix concrete directly correlates with heightened demand for concrete vibrators as essential equipment for ensuring structural integrity and eliminating air pockets during concrete placement.

Key Industry Highlights:

- Internal Concrete Vibrators dominate with 54% market share while simultaneously representing the fastest-growing product type, supported by ready-mix concrete market expansion at 5.1% CAGR.

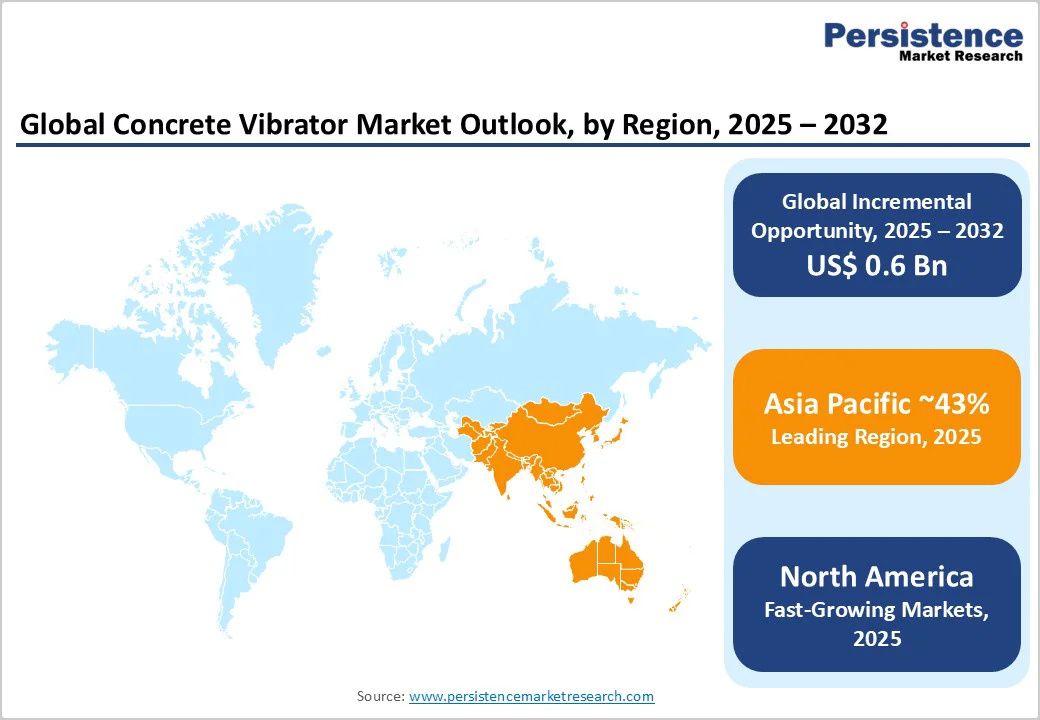

- Asia Pacific leads regional markets with 43% global share, reflecting massive infrastructure spending and robust construction market growth.

- Electric power sources command 45% market share and the fastest growth trajectory, driven by electrification trends, with the electric construction equipment market growing at 10.1% CAGR

- Industrial & Infrastructure Projects emerge as fastest-growing end-use segment at 5.2% CAGR, fueled by government mega-investments including U.S. Infrastructure Act's US$ 1.2 trillion and China's Belt and Road US$ 124 billion H1 2025 engagement.

- North America demonstrates strong regional growth at 5.4% CAGR, supported by infrastructure modernization requirements estimated at US$ 4.5 trillion by 2025 and sustained construction equipment market expansion.

- Ready-mix concrete market's explosive growth from US$ 566.3 billion in 2025 to US$ 802.2 billion by 2032 directly correlates with heightened concrete vibrator demand for quality consolidation.

| Key Insights | Details |

|---|---|

| Concrete Vibrator Market Size (2025E) | US$ 1.4 billion |

| Market Value Forecast (2032F) | US$ 1.9 billion |

| Projected Growth CAGR (2025-2032) | 4.8% |

| Historical Market Growth (2019-2024) | 4.0% |

Market Dynamics Analysis

Driver - Unprecedented Global Infrastructure Investment and Urbanization

Global infrastructure spending is experiencing transformative growth, with projections indicating the global economy will need to invest nearly 3.5% of GDP per year (US$ 4.2 trillion) over the next decade to future-proof social, transport, energy, and digital infrastructure. This massive capital deployment is fundamentally driven by urbanization trends, with the United Nations projecting that nearly 68% of the world's population will live in cities by 2050, creating unprecedented demand for residential, commercial, and infrastructure construction.

The Asia Pacific construction market is growing at a CAGR of 6.8%, reflecting the region's rapid urban expansion and government-led infrastructure initiatives. In the United States, the Infrastructure Investment and Jobs Act allocates US$ 550 billion to transport, utilities, and broadband through 2030, while China's Belt and Road Initiative reached record engagement of US$ 124 billion in the first half of 2025, nearly doubling year-over-year investment. These infrastructure megaprojects require extensive concrete construction, directly stimulating demand for concrete vibrators as indispensable tools for achieving proper concrete compaction, structural durability, and quality standards across residential towers, commercial complexes, transportation networks, and industrial facilities.

Exponential Growth in Ready-Mix Concrete Adoption

The rapid growth of the ready-mix concrete market is significantly driving the demand for concrete vibrators. Ready-mix concrete has emerged as the preferred construction material because it offers superior quality control, shorter construction timelines, reduced waste on-site, and consistent performance from batch to batch. The construction industry's shift toward off-site batching and transit-mixed delivery systems creates inherent demand for concrete vibrators to ensure proper consolidation upon placement.

Government mega-infrastructure pipelines, including the U.S. Infrastructure Investment and Jobs Act directing major investments toward transportation and utilities rehabilitation, mandate quality-controlled concrete with ISO 9001-certified batching that reinforces preference for ready-mixed solutions. Furthermore, rapid urbanization in emerging economies continues to absorb large rural populations, lifting multistory residential construction and driving higher ready-mix concrete demand, with the market offering predictable quality, faster floor-cycle times, and fewer on-site labor inputs, advantages that resonate as contractors face persistent skilled-worker shortages estimated at 439,000 workers needed in 2025 alone in the U.S. construction industry. This structural shift toward ready-mix concrete directly translates into sustained demand for internal and external concrete vibrators essential for achieving air-free, high-strength concrete structures.

Restraint - Construction Labor Shortages and Skilled Worker Scarcity

The construction industry faces a critical skilled labor shortage that poses significant challenges to market expansion, with 92% of construction firms reporting difficulty finding qualified workers to hire. The U.S. construction industry must attract an estimated 439,000 net new workers in 2025 to meet anticipated demand, while the aging workforce compounds this challenge, with roughly one in five construction workers over age 55 approaching retirement.

This labor scarcity impacts concrete vibrator utilization in two dimensions - first, fewer available workers limit the number of concurrent construction projects, potentially constraining equipment demand. Second, the shortage of experienced operators who are skilled with vibration techniques, duration, and insertion depths result in suboptimal equipment performance or reluctance to invest in advanced systems requiring specialized training.

The skilled labor shortage causes 45% of firms to report labor shortages as the leading cause of project delays, while the aggregate annual economic impact reaches US$ 10.8 billion in lost home building production alone, constraining overall construction activity and indirectly limiting concrete vibrator market growth potential.

Economic Uncertainty and Construction Material Cost Volatility

Construction material cost volatility and economic headwinds present substantial restraints to market growth, particularly in developed markets experiencing inflationary pressures. Germany's construction sector, Europe's largest, is projected to decline by 1.8% in real terms in 2025, marking the fifth consecutive year of contraction due to high material costs, weak external demand, and reduced building permits. Construction input costs, including copper pipe prices and copper wire increasing since early 2025, creating budgetary pressures that force contractors to defer equipment upgrades or postpone projects entirely.

Elevated interest rates, while moderating in 2025, continue to impact construction financing, with nonresidential building spending projected to increase only 1.7% in 2025 and 2.0% in 2026, indicating sluggish growth momentum. Supply chain disruptions, regulatory compliance costs, and geopolitical tensions contribute to cost unpredictability, with Euro 7 emission standards indirectly affecting construction equipment affordability. These economic headwinds create risk-averse behavior among construction firms, prioritizing essential expenditures over discretionary equipment purchases and potentially extending replacement cycles for existing concrete vibrator fleets.

Opportunities - Electrification and Sustainable Construction Equipment Adoption

The transition toward electrified construction equipment presents a transformative opportunity for concrete vibrator manufacturers, driven by stringent emission regulations, corporate sustainability mandates, and technological advancements in battery systems. The electric construction equipment market is rapidly growing, with battery-electric equipment leading over hybrids thanks to better duty cycles, low noise, zero emissions, and lower lifecycle costs. Tightening government regulations, such as EU Stage V and US Tier 4 Final standards, are driving this growth.

Battery-powered concrete vibrators provide advantages like cordless portability and reduced operator vibration, making them ideal for indoor use where exhaust is a concern. Innovations like Milwaukee Tool's MX FUEL Backpack system are gaining traction in urban construction projects focused on sustainability. The Sweden-US Green Transition Initiative's successful demonstration of fully electrified construction sites, utilizing electric equipment exclusively for EV charging station installation and achieving 258 kg CO? savings over four weeks, validates the commercial viability and environmental benefits of electrified concrete vibrators, creating compelling opportunities for manufacturers investing in lithium-ion battery technology and smart diagnostics.

Digitalization and Smart Construction Technology Integration

The convergence of construction digitalization and smart equipment connectivity creates lucrative opportunities for concrete vibrator manufacturers embracing Industry 4.0 capabilities. The integration of IoT modules, wireless connectivity, and real-time performance monitoring enables contractors to optimize equipment utilization, track maintenance schedules, and ensure quality compliance across multiple jobsites simultaneously. Construction site management platforms increasingly incorporate wireless-connected concrete vibrators that provide data on vibration frequency, duration, battery status, and operator performance, enabling project managers to verify proper consolidation procedures and maintain quality documentation for structural certification.

The construction industry's digital transformation, with Building Information Modeling (BIM) and digital twins becoming standard practice, creates opportunities for equipment manufacturers offering connected devices that integrate seamlessly into broader construction technology ecosystems. Telematics-enabled concrete vibrators allow fleet operators to monitor equipment health, predict component failures before breakdowns occur, and optimize deployment across project portfolios, reducing downtime and maximizing return on equipment investments. The rental equipment sector, which provides accessible pathways for contractors to utilize advanced equipment without major capital investments, increasingly demands smart, connected tools that enable remote monitoring and usage-based billing models, creating additional distribution channels for manufacturers offering digitally-enabled concrete vibrators with enhanced traceability and operational analytics.

Category-wise Analysis

Product Type Insights

The internal concrete vibrator segment dominates the product type category, commanding 54% market share in 2025 while simultaneously representing the fastest-growing segment. Internal vibrators, also known as poker or immersion vibrators, consist of a vibrating head attached to a flexible shaft connected to an electric motor, internal combustion engine, or pneumatic power source. Their market leadership stems from versatility across diverse applications, including narrow retaining walls, wide concrete columns and beams, and other structural elements requiring deep penetration for air bubble elimination. The segment's prominence is reinforced by the ready-mix concrete market's 5.1% CAGR growth, as transit-mixed deliveries require immediate, effective consolidation upon placement, favoring internal vibrator systems.

External concrete vibrators represent a significant complementary segment, growing at an impressive 4.5% CAGR despite a smaller absolute market share. External vibrators attach to formwork exterior surfaces, transmitting vibrations through molds to consolidate concrete, particularly effective for precast manufacturing, thin wall sections, and applications where internal vibrator access is restricted. The external vibrator market benefits from the precast and prefabricated construction trend, with manufacturers increasingly adopting factory-controlled production environments that favor external vibration systems for consistent, repeatable quality outcomes across standardized components.

End-user Analysis

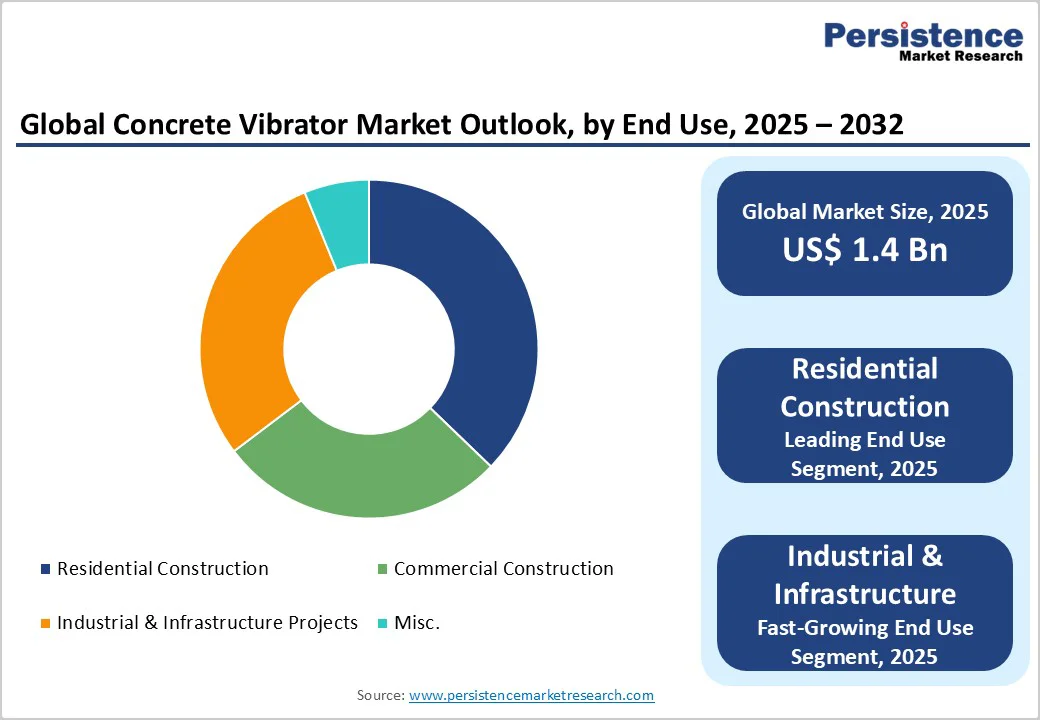

Residential Construction leads the end-use segmentation with 37% market share in 2025, reflecting global housing demand driven by population growth and urbanization. The United Nations estimates that nearly two-thirds of the world's population will shift to urban dwellings by 2050, creating sustained residential construction momentum. U.S. privately-owned dwelling units approved by building permits reached a seasonally adjusted annual rate of 1,397,000 in June 2025, representing 0.2% growth compared to May, demonstrating resilient housing construction activity despite economic headwinds.

However, Industrial & Infrastructure Projects emerge as the fastest-growing end-use segment with 5.2% CAGR through 2032, outpacing residential construction growth rates. This acceleration is driven by government infrastructure investments, including the U.S. Infrastructure Investment and Jobs Act's US$ 1.2 trillion allocation, China's Belt and Road Initiative's record US$ 124 billion engagement in H1 2025, and global infrastructure requirements estimated at US$ 4.2 trillion annually. Industrial construction benefits from manufacturing reshoring initiatives, data center construction for AI infrastructure, and renewable energy installations, with Germany allocating 12 GW of new gas-fired power stations to be tendered from 2025, exemplifying large-scale industrial projects requiring extensive concrete consolidation equipment.

Power Source Analysis

Electric power sources dominate with 45% market share while simultaneously representing the fastest-growing segment, though Hydraulic systems follow closely with 4.6% CAGR. Electric vibrators' market leadership reflects multiple advantages: widespread electricity availability on construction sites, zero direct emissions enabling indoor usage, lower operating costs compared to fuel-powered alternatives, and reduced noise levels compared to pneumatic systems. The battery-operated subsegment is experiencing particularly rapid adoption, with the electric construction equipment market growing at a significant pace, driven by lithium-ion battery advancements offering higher energy density, shorter charging times, and longer operational lifespans.

Hydraulic concrete vibrators' strong growth trajectory reflects their suitability for heavy-duty applications, particularly in infrastructure projects utilizing hydraulic excavators and other earthmoving equipment that can power-take-off vibrator attachments. The global hydraulic equipment market is projected to grow at a CAGR of 6.1%, with construction applications contributing around 31% of market revenue in 2024. Hydraulic systems offer high power density, reliable performance under extreme conditions, and integration capabilities with existing construction equipment fleets, making them preferred choices for large-scale civil engineering and infrastructure projects requiring sustained, high-intensity vibration.

Regional Market Insights

North America Concrete Vibrator Market Trends

North America is experiencing robust growth at a CAGR of 5.4% through 2032, driven by substantial infrastructure modernization initiatives and sustained residential construction activity. The region benefits from the Infrastructure Investment and Jobs Act's US$ 1.2 trillion allocation with the American Society of Civil Engineers estimating the U.S. requires US$ 4.5 trillion in infrastructure investments by 2025 to maintain and improve existing infrastructure.

The U.S. construction equipment market grew rapidly, reflecting strong equipment demand correlating with the concrete vibrator market growth. The U.S. construction sector saw spending exceed around US$ 2 trillion in 2024, with total construction expenditures reaching this figure at a seasonally adjusted annual rate, primarily driven by both private residential and nonresidential projects.

Government initiatives promoting electrification and sustainable construction practices are reshaping market dynamics, with several states proposing tight emission regulations to support electric construction equipment and meet zero-emission goals. The rental equipment sector provides significant market support, offering accessible pathways for contractors to utilize advanced concrete vibrators without major capital investments, particularly benefiting small to medium contractors facing budgetary constraints. Technological innovation remains a key differentiator, with North American manufacturers and distributors emphasizing telematics integration, battery-powered systems, and ergonomic designs that reduce operator fatigue and enhance productivity. Regional challenges include persistent labor shortages, with the construction industry needing ~439,000 net new workers in 2025, potentially constraining project timelines and equipment utilization rates.

Europe Concrete Vibrator Market Trends

Europe holds a significant 24% global market share in 2025, anchored by mature construction markets including Germany, the United Kingdom, France, and Spain. The region allocated US$375 billion in 2025 toward infrastructure, focusing on energy efficiency and climate resilience under the European Green Deal, creating sustained demand for construction equipment, including concrete vibrators. Germany, Europe's largest construction market despite near-term headwinds, allocated a transformative €500 billion off-budget fund for infrastructure and expanded defense infrastructure funding without specified limitations, positioning the market for recovery from 2026 with 3.1% annual growth anticipated from government investments.

The European Union's stringent emission standards, including Euro 7 regulations entering force in 2026, are driving the adoption of electric and low-emission construction equipment, creating opportunities for manufacturers offering battery-powered and hybrid concrete vibrators compliant with evolving regulatory frameworks.

The construction equipment market in Europe is growing at a CAGR of 6.96% from 2025 to 2032, supported by ongoing urbanization in densely populated areas requiring efficient construction solutions and sustainable building practices. Key players like Wacker Neuson Group (Germany) dominate the market with high-frequency internal vibrators and durable external motors. Their strong presence in Europe and North America is supported by German engineering and extensive dealer networks. Regulatory harmonization in the EU promotes equipment standardization and cross-border trade, while government initiatives foster green building technologies.

Asia Pacific Concrete Vibrator Market Trends

Asia Pacific dominates the global concrete vibrator market with 43% market share in 2025, driven by unprecedented urbanization rates, massive infrastructure investments, and robust construction equipment manufacturing capabilities. The region's construction market is growing at a CAGR of 6.8%, reflecting strong government funding, sustainability goals, and digital innovation adoption. China leads infrastructure spending with around US$ 1.6 trillion in 2025, directing 50% toward renewable energy and 30% toward transportation and rail, while India allocates US$ 110 billion with approximately 20% dedicated to renewable energy capacity.

Asia Pacific region boasts strong local manufacturing capabilities, with China and India as key production hubs offering cost-competitive equipment across various vibrator categories. Chinese manufacturers leverage economies of scale to sell products at lower prices, while India has gained recognition for competitive manufacturing, with 50% of CNH's construction equipment produced there being exported to over 100 countries, including the U.S. and Europe, highlighting its quality and cost advantages.

Urbanization in the Asia Pacific region is strong, with 60% of the world's 4.3 billion urban residents driving demand for residential towers, commercial complexes, and infrastructure needing concrete consolidation equipment. Government initiatives such as China's Belt and Road Initiative, India's "Make in India," and ASEAN projects support ongoing construction, boosting concrete vibrator demand. The rapid adoption of construction technologies, including BIM and smart city development focused on sustainability, presents opportunities for advanced vibrator systems featuring digital connectivity and performance monitoring.

Competitive Landscape

The global concrete vibrator market is moderately fragmented, with top players holding around 30 to 35% share. Leading firms such as Wacker Neuson Group, Exen Corporation, and Multiquip Inc. dominate through innovation, distribution strength, and brand reliability. Market concentration is highest in Europe and North America, while Asia leads in production and consumption due to cost-efficient manufacturing. Regional players in China and India compete via pricing and agility, with competition centered on quality, durability, service, and performance reliability over price.

Strategic Developments

Epiroc Acquisition of STANLEY Infrastructure (Completed April 2024)

Epiroc completed the acquisition of STANLEY Infrastructure for US$ 760 million (SEK 8.2 billion) in April 2024, strengthening its infrastructure and construction business segment. This strategic transaction expands Epiroc's product portfolio into complementary construction equipment categories, enhances North American market presence where the vast majority of revenues are generated, and positions the company for growth in infrastructure-driven construction segments aligned with government spending initiatives.

Husqvarna Acquisition of Atlas Copco Concrete and Compaction Business (Completed February 2018)

Husqvarna Group's Construction division completed the acquisition of Atlas Copco's concrete and compaction business in February 2018, adding approximately 200 employees and revenues of MEUR 57 (MSEK 570) in 2016. The transaction included complete product ranges for concrete and compaction such as plate compactors, tandem rollers, and concrete vibrators, along with the production facility in Ruse, Bulgaria, and production assets in Nashik, India, plus sales and service operations worldwide.

Business Strategies

Key competitive strategies in the concrete vibrator market center on innovation, cost efficiency, and market expansion. Manufacturers focus on battery-powered and smart-connected systems, ergonomic designs, and controlled frequency vibration (CFV) technology for performance optimization. Sustainability drives investment in lithium-ion, zero-emission, and compliant solutions. Expanding rental participation, bundled service contracts, and digital fleet management enhance customer retention, while Industry 4.0 tools like telematics and predictive maintenance strengthen differentiation and long-term value creation.

Companies Covered in Concrete Vibrator Market

- Husqvarna Group

- Atlas Copco

- Wacker Neuson Group

- Badger Meter Inc

- Hyundai Power Products

- Greaves Cotton

- Wamgroup

- Multiquip Inc

- Enarco Group

- EARTHQUAKE INDUSTRIES

- Exen Corp

- Denver Concrete Vibrator

- Minnich Manufacturing, Inc

- Emil Laier GmbH & Co. KG

- Vibtec

- Foshan Yunque Vibrator Co, Ltd

- webac holding ag

- OLI SpA

- Cleveland Vibrato

- Oztec Business Machines Inc

Frequently Asked Questions

The global Concrete Vibrator Market was valued at US$ 1,384.1 Billion in 2025 and is projected to reach US$ 1,923.8 Billion by 2032.

The market is primarily driven by accelerating global urbanization with 68% of the world's population projected to live in cities by 2050, massive infrastructure investments, and the ready-mix concrete market's growth requiring efficient consolidation equipment, alongside technological innovations in battery-electric systems and smart connectivity features.

The Concrete Vibrator Market is projected to grow at a CAGR of 4.82% from 2025 to 2032.