- Automotive Components & Materials

- Automotive Coil Spring Market

Automotive Coil Spring Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Automotive Coil Spring Market by Spring Type (Compression Spring, Extension Spring and Torsion Spring), by Sales Channel (Aftermarket and OEM), By Vehicle Type (Passenger Vehicle, Light Commercial Vehicles and Heavy Commercial Vehicles) and Regional Analysis for 2026 - 2033

Automotive Coil Spring Market Size and Trends Analysis

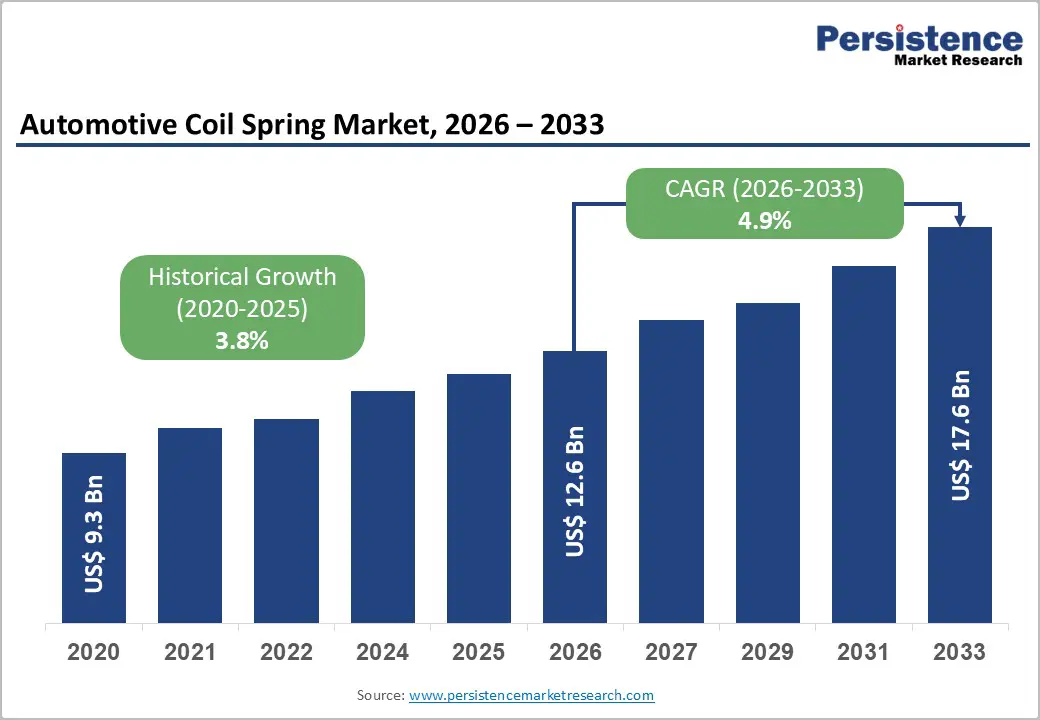

The global automotive coil spring market size is likely to be valued at US$ 12.6 billion in 2026 and is projected to reach US$ 17.6 billion by 2033, growing at a CAGR of 3.8% between 2026 and 2033. The market is driven by a transition toward electric vehicles requiring specialized suspension architectures, regulatory emphasis on emissions reduction mandating weight optimization, and expansion of commercial vehicle segments in emerging markets.

Key Industry Highlights:

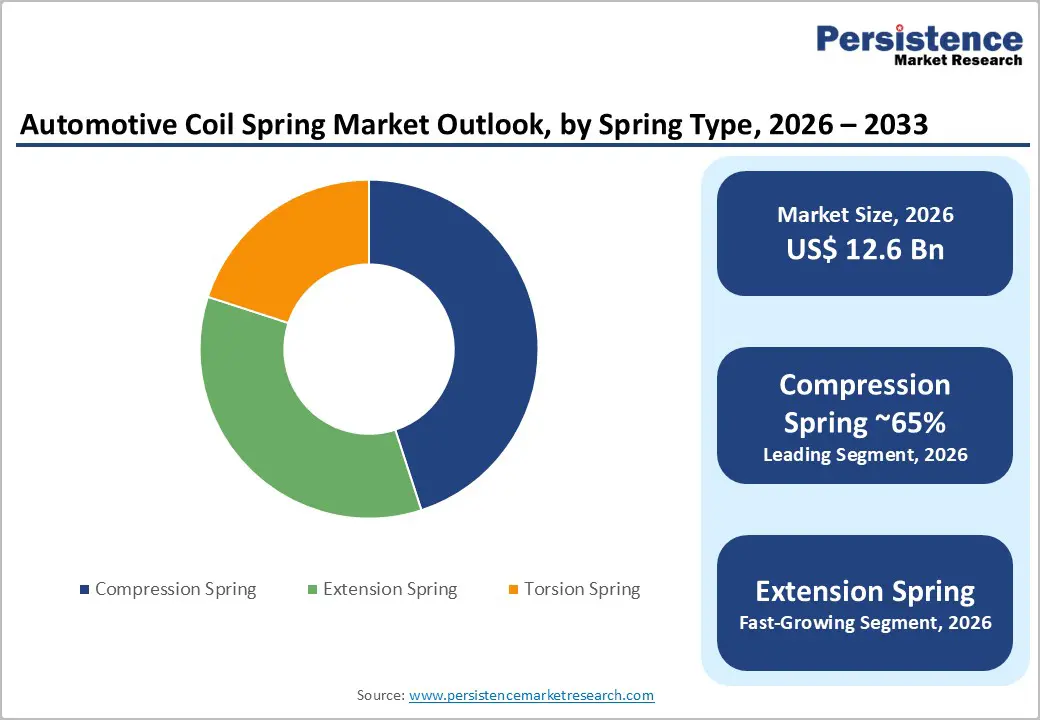

- Leading Spring Type: Compression springs dominate with 65% market share reflecting universal vehicle platform applicability; Extension springs represent fastest growing at 7-11% CAGR, driven by advanced suspension architecture proliferation.

- Dominant Vehicle Segment: Passenger vehicles command 60% market share through massive production scale and technology leadership; Light commercial vehicles represent fastest growing at 10% CAGR, driven by e-commerce logistics expansion and commercial electrification.

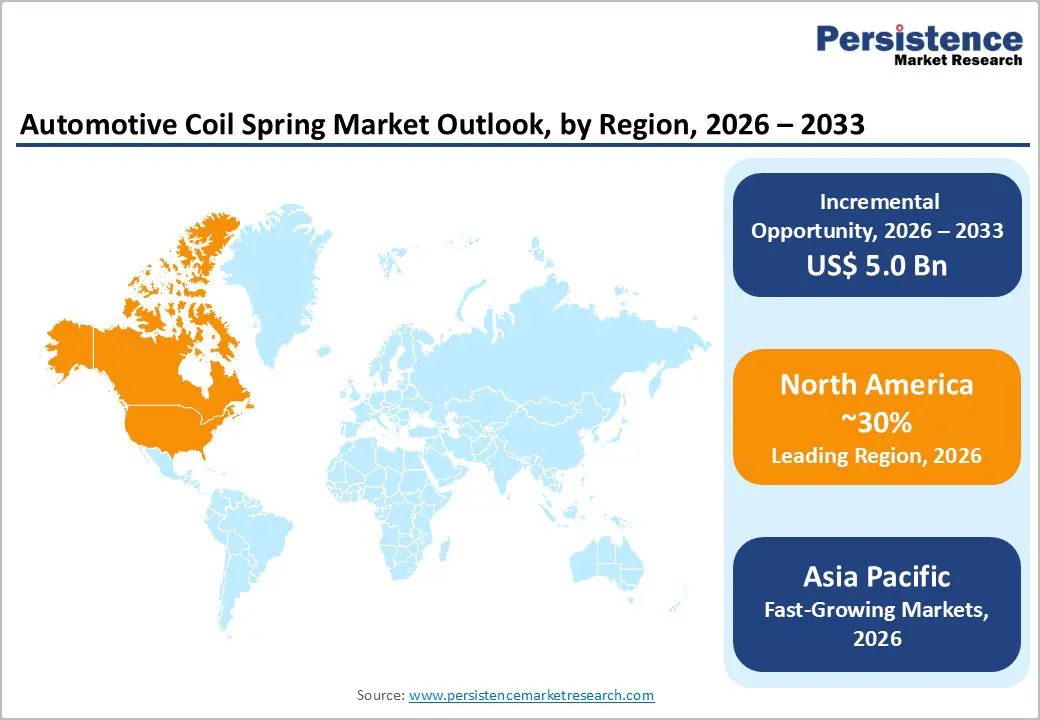

- Regional Market Dominance and Growth: North America maintains 30% global market share, driven by premium vehicle concentration and EV adoption; Asia-Pacific demonstrates the fastest regional growth at a 9% CAGR, expanding from a 25% current share to 42% by 2033 through automotive manufacturing expansion.

- Technology and Material Innovation Momentum: Top 10 suppliers control 60% market share (Sogefi, Mubea, BBS leading); Lightweight material integration advancing with 35% weight reduction through composite and advanced alloy adoption; Adaptive suspension system development establishing differentiated positioning; Electric vehicle platform specialization creating specialized demand for optimized suspension systems.

- Competitive Dynamics: Emerging Asian manufacturers establishing 20-30% cost advantages, threatening established suppliers in price-sensitive markets; Premium supplier differentiation through technology and specialization, maintaining margin positioning.

| Key Insights | Details |

|---|---|

|

Automotive Coil Spring Market Size (2026E) |

US$ 12.6 Bn |

|

Market Value Forecast (2033F) |

US$ 17.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.9% |

|

Historical Market Growth (CAGR 2020 to 2024) |

3.8% |

Market Dynamics

Drivers - Global Vehicle Production Expansion and Emerging Market Automotive Penetration

Global vehicle production reached approximately 77 million units annually in 2024-2025, representing 9% growth in emerging markets including India, Vietnam, and Southeast Asia. Automotive industry economic contribution, with global automotive sector valued at US$ 2.5-3.0 trillion annually and expanding 5.5% year-over-year, establishes proportionate coil spring demand for trajectory. Emerging market vehicle ownership, with a middle-class population in Asia-Pacific expanding to 1.5+ billion consumers and automotive penetration increasing 15-20% annually, drives production capacity requirements.

Commercial vehicle segment expansion, with light commercial vehicle sales in emerging markets growing 12% annually, supports e-commerce and logistics expansion and establishes incremental coil spring demand. Aftermarket replacement demand, with global vehicle fleet exceeding 1.4 billion units and suspension component replacement cycles requiring 8–10-year intervals, creates a recurring revenue opportunity.

Electric Vehicle Adoption and Lightweight Suspension Technology Requirements

Electric vehicle sales momentum, with global EV penetration reaching 10-14 million units in 2024 and growing at 40-50% annually through 2033, establishes proportionate demand for lightweight suspension components. Battery pack weight considerations, with EV battery systems comprising 400-600 kg of vehicle curb weight and compromising driving range, necessitate suspension system weight optimization of 15%. Lightweight material integration, using high-strength steel alloys and composite materials, enables a 25-30% reduction in suspension weight compared to conventional systems, aligning with EV efficiency mandates.

Advanced suspension architectures, with independent suspension systems increasingly adopted in EV platforms and requiring precision-engineered coil springs, establish technical differentiation opportunities. Ride quality optimization, with consumer preferences emphasizing smooth, controlled ride characteristics, drives demand for customized spring solutions. Performance-vehicle segment growth, with premium EV manufacturers such as Tesla, BMW iX, and Mercedes EQS emphasizing adaptive suspension capabilities, establishes specialized coil-spring requirements.

Restraints - Raw Material Price Volatility and Steel Supply Chain Disruptions

Steel price fluctuations, with coil spring feedstock commodity prices fluctuating 20-30% quarterly based on global supply-demand dynamics, compress manufacturer margins and create pricing uncertainty. Chromium and molybdenum alloy constraints, along with limited availability of specialized high-strength steel alloys due to limited production capacity and geopolitical sourcing risks, disrupt supply continuity. Semiconductor shortage legacy effects, with manufacturing equipment microcontroller availability remaining constrained through the 2026-2027 period, delay production facility modernization.

Supply chain fragmentation, with coil spring production requiring coordination across steel mills, forging operations, heat treatment facilities, and final assembly locations, creates logistics complexity. Lead time extension, with component sourcing timelines expanding from 8-12 weeks to 16-24 weeks during supply disruptions, impairs production flexibility. Inventory management challenges, with manufacturers balancing raw material stockpiling costs against supply disruption risks, pressure working capital management.

Market Consolidation and Competitive Pricing Pressure

OEM cost reduction mandates, with automotive manufacturers imposing 3-5% annual component cost reduction targets on suppliers, constrain industry profitability. Supplier concentration risk, with top 10 suppliers controlling 65-75% market share, creates procurement dependency and pricing vulnerability. Alternative suspension technology competition, with air spring systems and adaptive suspension technologies offering premium capabilities and competing for OEM specifications, threaten coil spring volume.

Aftermarket price competition, with independent retailers and regional manufacturers offering 15-25% cost savings versus OEM components, cannibalizes OEM-driven demand. Margin compression dynamics, with average gross margins declining from 20-25% to 15-20% through the forecast period, reduce investment capacity. Import competition, with low-cost manufacturers in India, Vietnam, and Thailand offering competitive pricing, pressures established supplier positioning in price-sensitive markets.

Opportunity - Advanced Material Technology and Lightweight Composite Spring Development

Composite spring adoption, with carbon-fiber-reinforced polymer (CFRP) and glass-fiber-reinforced polymer (GFRP) materials enabling 40-50% weight reduction compared to steel springs, establishes premium market positioning. Titanium alloy springs, with beta-titanium materials offering 60-70% weight reduction and superior fatigue characteristics, command 25-40% price premiums, establishing a profitability opportunity. Manufacturing scale advancement, with injection molding and fiber-winding technologies achieving production maturity and reducing per-unit composite spring costs 30-40%, expanding addressable market. EV-specific application development, with specialized lightweight spring systems optimized for EV battery thermal management and performance characteristics, creates differentiated product opportunities.

Adaptive and Semi-Active Suspension System Integration

Adaptive suspension technology convergence, with continuously variable damping and electronically adjustable spring rate systems achieving production readiness and cost parity with passive systems approaching 2027-2028, establishes market acceleration opportunity. Smart manufacturing integration, with IoT sensors enabling real-time suspension performance monitoring and predictive maintenance optimization, creates recurring service revenue opportunities. Autonomous vehicle platform requirements, which mandate advanced suspension systems for safety and comfort, create specialized demand. Performance customization market, with aftermarket enthusiasts and the performance vehicle segment showing willingness to invest in advanced suspension systems, commanding 50-100% price premiums, establishes a profitability opportunity.

Category-wise Analysis

Spring Type Insights

The compression spring segment accounts for 65% market share, driven by its universal use across passenger, commercial, and specialty vehicles. Helical compression springs offer simple manufacturing, reliable load-bearing performance, and 30–40% lower production costs than alternative spring types. More than 95% of vehicle platforms use compression springs in front and rear suspension systems, creating consistent OEM demand. Standardized designs and industry specifications enable interchangeability across platforms, while easy serviceability supports strong after-market replacement demand. These advantages reinforce market maturity and dominance.

In contrast, the extension spring segment is the fastest-growing, projected to expand at a 7% CAGR through 2033. Growth is fueled by adoption in advanced suspension architectures such as MacPherson struts and multi-link systems, rising vehicle platform diversification, lightweight requirements in electric vehicles, and increasing use in premium and adaptive suspension systems. Expansion reflects evolving suspension design complexity and performance-focused vehicle development.

Vehicle Type Insights

The passenger vehicle segment holds 60% market share, driven by high global production volumes and the complexity of suspension systems. Annual passenger vehicle output exceeds 60 million units, accounting for 75–80% of total vehicle production, creating a strong demand base for automotive coil springs. Broad market coverage—from economy to premium and performance models—supports diverse spring specifications. Growing consumer focus on ride comfort and handling refinement accelerates adoption of advanced suspension technologies, with passenger vehicles leading innovation that later migrates to commercial platforms.

The light commercial vehicle (LCV) segment is the fastest-growing, expanding at a 6.2% CAGR through 2033. Growth is fueled by rapid e-commerce-driven demand for last-mile delivery, strong commercial vehicle sales in emerging markets, accelerating electrification of vans and trucks, fleet replacement cycles, and increasing demand for customized suspension solutions tailored to payload and usage requirements.

Regional Insights

North America Automotive Coil Spring Market Insights

Market Scale and Performance: North America commands approximately 30% of the global automotive coil spring market share, valued at approximately US$ 3.53 billion in 2026 with projections approaching US$ 4.8 billion by 2033. The United States represents dominant regional market contributor, accounting for 80% of the North American market value, driven by advanced vehicle technology adoption and premium vehicle segment penetration.

Premium vehicle segment dominance, with luxury and performance vehicle manufacturers such as BMW, Mercedes-Benz, and Tesla concentrating manufacturing and product development in North America, establishes leadership in technology advancement. Electric vehicle adoption is accelerating, with US EV penetration reaching 12% of new vehicle sales by 2033, driven by federal incentives and consumer preference, necessitating specialized suspension systems. Commercial vehicle modernization, with North American truck manufacturers including Ford, General Motors, and Daimler, prioritizing suspension technology advancement and drive coil spring specification enhancement.

Europe Automotive Coil Spring Market Insights

Europe represents approximately 22% of the global automotive coil spring market share, valued at approximately US$ 3.28 billion in 2026. Germany, Italy, France, and Spain collectively represent 70% of the European market value, reflecting established automotive manufacturing presence and precision engineering expertise.

Environmental regulatory leadership, with EU emissions standards and circular economy directives driving lightweight vehicle design and suspension technology innovation. Automotive manufacturing excellence tradition, with Germany's automotive sector employing 500,000+ workers in manufacturing and supplier operations. Premium vehicle concentration, with European luxury brands prioritizing suspension refinement and driving advanced spring design specifications. Commercial vehicle leadership, with European truck manufacturers including Volvo, MAN, and Scania pioneering advanced commercial suspension systems, establishes technology advancement momentum.

Asia Pacific Automotive Coil Spring Market Insight

Asia Pacific demonstrates robust growth dynamics, commanding approximately 25% market share with projections increasing to 35% by 2033. The region valued at approximately US$ 4.03 billion in 2026 is anticipated to reach US$ 7.0 billion by 2033, representing the fastest-growing regional market with an estimated CAGR of 7% through the forecast period.

Automotive manufacturing expansion, with China, India, and Vietnam attracting 150-250 billion annually in automotive facility investments, drives proportionate coil spring demand. Vehicle production scaling, with Asia-Pacific vehicle production expanding from 50-55 million units (2026) to 65-75 million units (2033), establishes a fundamental demand trajectory. Commercial transportation growth, with logistics infrastructure expansion and fleet electrification, is creating 50-100 million incremental commercial vehicles, establishing specialized demand.

Competitive Landscape

A mix of established players and emerging manufacturers characterizes the competitive landscape of the automotive coil spring market. Key companies, such as Tenneco Inc., Eibach Springs, and Hyperco, dominate the market with their extensive product offerings and innovative solutions tailored for electric and hybrid vehicles. These companies invest significantly in research and development to enhance the performance and sustainability of their coil springs.

Regional players like Lesjofors and Owen Springs are gaining traction by focusing on localized production and customization to meet specific market needs. The competition is further intensified by strategic collaborations and partnerships between coil spring manufacturers and automotive OEMs to develop advanced suspension systems that cater to evolving consumer demands and regulatory requirements.

Key Industry Developments:

- In January 2024, Owen Springs announced a strategic partnership with a major electric vehicle manufacturer to supply custom coil springs for their upcoming models to enhance the vehicle's suspension performance and cater to specific design requirements, further establishing Owen Springs as a key player in the EV segment.

- In June 2023, Eibach announced an expansion of its manufacturing facilities to increase production capabilities for coil springs tailored for electric vehicles. This expansion reflects the company's commitment to supporting the growing electric mobility market and meeting the increasing demand for high-quality suspension components.

Companies Covered in Automotive Coil Spring Market

- Betts Company

- Clifford Springs

- Draco Spring Mfg. Co.

- Hendrickson USA, L.L.C.

- Jamna Auto Industries Ltd

- Kilen Springs

- Emco Electronics

- Sogefi Group

- NHK Nasco

- Mubea

- Others Key Players

Frequently Asked Questions

The Automotive Coil Spring market is estimated to be valued at US$ 12.6 Bn in 2026.

The key demand driver for the Automotive Coil Spring market is the global growth in vehicle production combined with rising demand for improved ride comfort, load-bearing capability, and suspension durability.

In 2026, the North America region will dominate the market with an exceeding 30% revenue share in the global Automotive Coil Spring market.

Among the Spring Type, Compression Spring holds the highest preference, capturing beyond 65% of the market revenue share in 2026, surpassing other Spring Type.

The key players in Automotive Coil Spring are Betts Company, Clifford Springs, and Draco Spring Mfg. Co. and Hendrickson USA, L.L.C.