- Sensors & Controls

- CO2 Sensors Market

CO2 Sensors Market Size, Share, and Growth Forecast 2026 - 2033

CO2 Sensors Market by Product Type (Non-dispersive Infrared CO2 Sensor, Chemical CO2 Sensor), by Application (Industrial, Metal & Mining, Air Purifier, Automotive, Oil & Gas, Others), by Regional Analysis, 2026-2033

CO2 Sensors Market Size and Trend Analysis

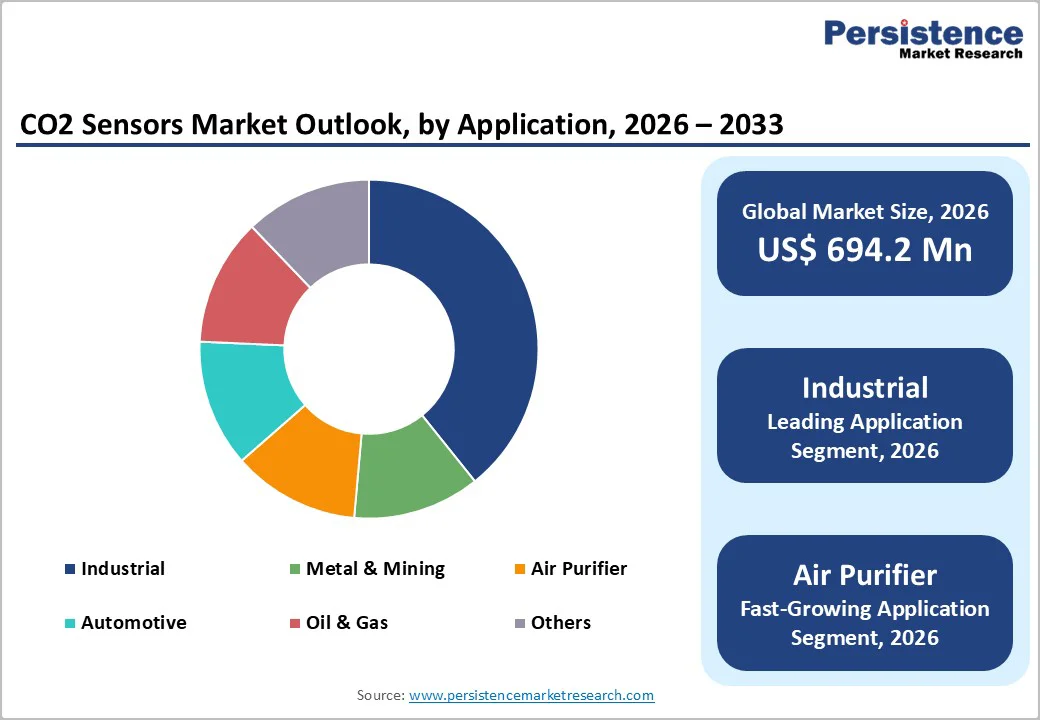

The global CO2 Sensors market size is expected to be valued at US$ 694.2 million in 2026 and projected to reach US$ 1,136.8 million by 2033, growing at a CAGR of 7.3% between 2026 and 2033.

The market is expanding due to rising global focus on indoor air quality, with over 60% of smart building projects in 2023 incorporating CO2 sensors for HVAC optimization, the rapid adoption of IoT-enabled sensors with edge AI for predictive ventilation and automated alerts, and tightening regulatory mandates worldwide, which compel commercial, industrial, and automotive sectors to implement advanced CO2 monitoring for energy efficiency and occupant health.

Key Market Highlights

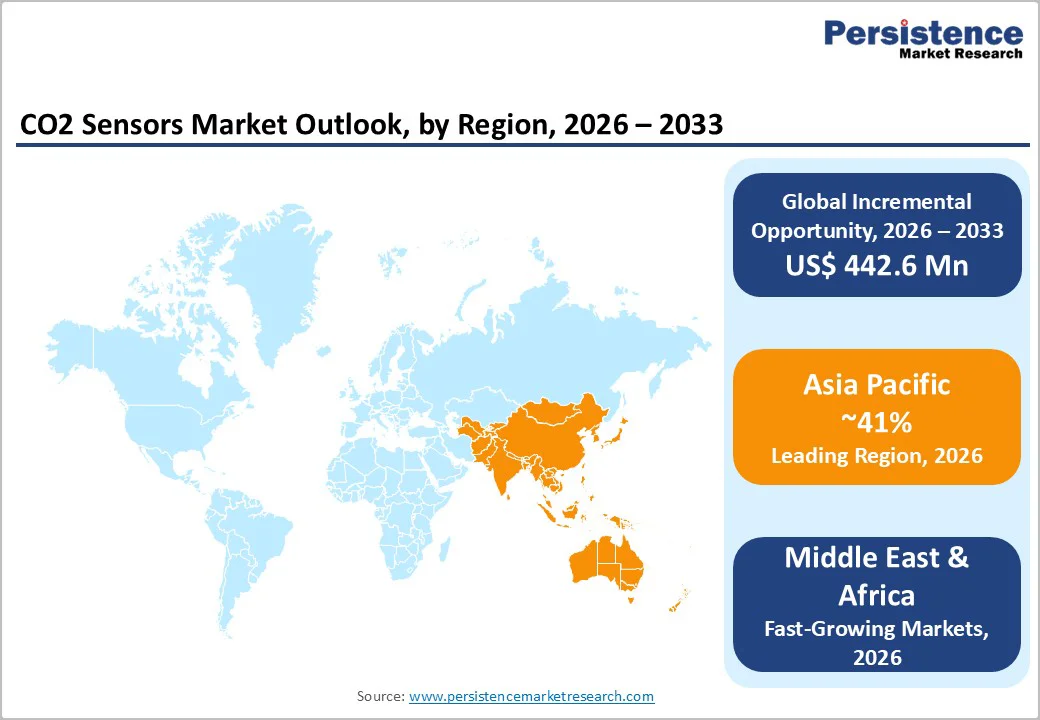

- Leading Region: Asia Pacific dominates the CO2 Sensors market with 41% market share in 2025, driven by rapid urbanization, accelerating air quality awareness.

- Fastest Growing Region: Middle East & Africa is forecast to maintain the strongest expansion at 8.5% CAGR from 2026-2033, fueled by GCC’s smart city expansion at 7% CAGR, and Africa’s growing air pollution awareness.

- Dominant Segment: NDIR CO2 sensors command 67% market share in 2025, supported by superior measurement accuracy, broad operating temperature range compatibility, proven long-term reliability, 4.26-micron wavelength absorption specificity, and integration into smart building HVAC systems.

- Fastest Growing Segment: Air purifier applications represent the fastest-growing segment at 8.4% CAGR from 2026-2033, driven by increasing consumer health consciousness, automotive in-vehicle air purifier market expansion, and government mandates for integrated cabin air quality monitoring in passenger vehicles.

- Key Market Opportunity: The convergence of CO2 sensors with complementary air quality monitoring technologies including PM2.5, VOC, temperature/humidity sensors, and AI-driven building optimization algorithms creates comprehensive environmental intelligence platforms enabling predictive maintenance, occupancy optimization, and dynamic energy management supporting enterprise sustainability and occupant health objectives.

| Global Market Attributes | Key Insights |

|---|---|

| CO2 Sensors Market Size (2026E) | US$ 694.2 million |

| Market Value Forecast (2033F) | US$ 1,136.8 million |

| Projected Growth CAGR (2026-2033) | 7.3% |

| Historical Market Growth (2020-2025) | 6.5% |

Market Dynamics

Market Growth Drivers

Acceleration of Smart Building Initiatives and Demand-Controlled Ventilation Adoption

The global shift toward intelligent building management systems is fundamentally accelerating CO2 sensor deployment, with building automation providers including Siemens, Johnson Controls, and Schneider Electric integrating CO2 sensor modules into comprehensive building management systems (BMS) supporting demand-controlled ventilation (DCV) strategies. The HVAC air quality monitoring market is experiencing exceptional growth at a 7.3% CAGR through 2033, with CO2 sensors representing critical enablers for real-time occupancy detection and ventilation optimization.

Smart buildings utilizing CO2-driven DCV systems achieve energy savings of 20-40% compared to conventional constant air volume ventilation, providing compelling financial justification for sensor deployment investments. The digitization of building management systems resulted in the integration of over 540,000 CO2 sensor units into smart HVAC installations in 2023, while LED lighting controls and occupancy-driven ventilation systems enabled the deployment of 320,000 wireless sensors supporting data sampling rates as fast as 5 seconds. Large technology enterprises, including Microsoft, Google, and IBM, are pioneering the integration of CO2 sensors into their innovation campuses. In November 2024, Google launched Air View+ on Google Maps, providing real-time air quality monitoring across India, using integrated sensor networks and AI-based data processing algorithms.

Expansion of IoT-Enabled Wireless CO2 Sensors and Edge AI Integration

The integration of Internet of Things (IoT) connectivity and artificial intelligence into CO2 sensor platforms is revolutionizing application flexibility and enabling new market segments previously inaccessible to traditional wired sensors. Approximately 35% of newly launched CO2 sensor modules in 2024 include edge AI capabilities for predictive ventilation control, automated environmental alerts, and self-learning optimization algorithms. Manufacturers have achieved significant advances in ultra-low-power operation, with average sensor power consumption declining from 120 mW in 2021 to 85 mW in 2023, enabling deployment of 310,000 wireless CO2 sensors in battery-operated applications (up from 220,000 units in 2022), including portable air quality monitors, wearable environmental trackers, and autonomous environmental sensing networks.

The miniaturization trend toward sensors featuring form factors under 25 mm³ supports integration into diverse applications from smartphone-connected air quality monitors to embedded HVAC controls and portable measurement devices. Advanced sensor technologies including photoacoustic spectroscopy (PAS) and NDIR LED-based detection offer enhanced sensitivity at substantially reduced cost and power consumption compared to traditional infrared lamp-based designs, enabling broader market accessibility and supporting price-competitive offerings across emerging market segments.

Market Restraints

High Initial Capital Costs and Integration Complexity for End-Users

The deployment of advanced CO2 sensor systems, which require sophisticated signal-processing electronics, calibration procedures, and building-automation system integration, remains capital-intensive, particularly for cost-sensitive applications in emerging markets and public-sector infrastructure. Advanced NDIR and photoacoustic sensor technologies command unit prices ranging from US$ 90 to US$ 250, creating significant barriers to adoption in budget-constrained organizations, including public schools, municipal facilities, and small commercial establishments.

Integration with existing Building Management Systems (BMS) requires specialized technical expertise, software development resources, and potentially expensive firmware modifications to support real-time CO2 data ingestion, processing, and actuation of ventilation controls. The sensor and measurement technology industry experienced a 10% revenue decline in Q3 2024 compared to prior year, indicating heightened market sensitivity to capital expenditure restrictions and budget constraints. These cost barriers are particularly acute for developing nations where indoor air quality awareness is rising but financial resources for infrastructure modernization remain constrained relative to developed market opportunities.

Technical Calibration Challenges and Sensor Drift Over Extended Operating Intervals

CO2 sensors require periodic recalibration to maintain measurement accuracy, with zero-point and span calibration procedures required at 12-24 month intervals, depending on operating conditions, application demands, and the sensor technology employed. NDIR sensors using infrared lamp sources exhibit gradual optical performance degradation over operational lifespans, necessitating periodic maintenance and component replacement to maintain target accuracy specifications.

Environmental factors, including ambient temperature variations, humidity fluctuations, and atmospheric pressure changes, can introduce systematic measurement errors requiring sophisticated environmental compensation algorithms to maintain accuracy across diverse operating conditions. Field-deployment data indicate that improperly maintained or calibrated sensors produce misleading data, undermining confidence in sensor-driven ventilation optimization and potentially delaying the justification of return on investment for sensor deployment projects.

Market Opportunities

Integration of Multi-Sensor Environmental Monitoring Platforms and AI-Driven Building Optimization

The convergence of CO2 sensors with complementary air quality monitoring technologies including PM2.5 particulate sensors, volatile organic compound (VOC) detectors, temperature/humidity sensors, and occupancy detection systems creates comprehensive environmental monitoring platforms enabling advanced building optimization algorithms. Enterprise-scale building automation vendors including Cisco (Meraki MT-15 environmental sensor), Microsoft Azure Digital Twins, and IBM Tririga platforms are architecting integrated solutions that combine real-time multi-parameter environmental data with machine learning algorithms for predictive maintenance, optimized occupancy scheduling, and dynamic energy management.

The vehicle interior air quality monitoring market is projected to expand at a 7.2% CAGR through 2033, with automotive OEMs such as Toyota, Ford, Denso, and Valeo pioneering integrated cabin air quality systems that incorporate CO2 sensors alongside particulate filtration, VOC removal, and real-time driver-cabin microclimate optimization. Advanced sensor fusion approaches that combine infrared-based CO2 detection with complementary sensing modalities enable manufacturers to deliver sophisticated, integrated solutions that command premium market valuations and customer loyalty.

Expansion of Portable CO2 Sensors for Consumer Applications and Emerging Market Air Purification Devices

The rapid growth of portable air quality monitoring devices and consumer-grade CO2 sensors is opening mass-market segments previously dominated by professional and industrial applications. Manufacturers, including Sensirion, unveiled the STCC4 miniature CO2 sensor in 2024, specifically designed for low-cost, mass-market applications addressing previous limitations imposed by size constraints and unit economics. Gas Sensing Solutions (GSS) announced the October 2025 Series 2 upgrade to its CozIR-LP CO2 sensor, integrating temperature and humidity sensing as standard features alongside updated electronics packages optimized for energy-harvested and battery-powered IoT applications.

Emerging market adoption of smart home technologies, portable air quality monitors, and wearable environmental trackers is driving demand for compact, low-cost CO2 sensors compatible with mobile device connectivity, cloud data analytics, and consumer-friendly user interfaces. This democratization of CO2 sensing technology across consumer segments creates substantial volume growth opportunities despite potential margin compression relative to enterprise sensor applications.

Category-wise Insights

Product Type Analysis

NDIR CO2 sensors dominate the product type category with 67% market share in 2025, driven by their superior measurement accuracy, broad temperature range compatibility, and long-term reliability across industrial, commercial, and consumer applications. Operating at the 4.26-micron infrared wavelength, modern NDIR sensors utilize LED sources and MEMS or pyroelectric detectors, enabling miniaturization, lower power consumption, and enhanced optical efficiency. These features make them ideal for integration into IoT-connected smart building systems, portable air quality monitors, and HVAC optimization solutions. The segment is projected to grow at 6.9% CAGR from 2026-2033, supported by continued advancements in sensor miniaturization, cost reduction, and adoption in connected environmental monitoring platforms.

Application Analysis

Industrial applications account for the largest share at 38% in 2025, driven by CO2 monitoring requirements in manufacturing plants, chemical processing, mining, and power generation for worker safety, regulatory compliance, and process optimization. Integration with HVAC and facility management systems enhances energy efficiency, predictive maintenance, and occupancy-responsive ventilation. Growth is supported by increasing industrial infrastructure investments and stricter workplace environmental regulations in emerging markets such as China, India, and Southeast Asia. The segment is projected to grow at 6.8% CAGR from 2026-2033, reflecting rising emphasis on workplace safety and environmental sustainability.

Regional Insights

North America CO2 Sensors Market Trends and Insights

North America commands approximately 28% of the global CO2 Sensors market share in 2025, with the United States representing the dominant contributor driven by mature building automation ecosystem, substantial commercial real estate infrastructure, and regulatory frameworks prioritizing indoor air quality. The U.S. Environmental Protection Agency (EPA) and American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE) have established indoor air quality standards driving adoption of CO2 sensors in commercial buildings, with approximately 60% of smart building projects in 2023 incorporating CO2 sensors into HVAC optimization strategies.

Building automation market leaders including Johnson Controls, Schneider Electric, and Siemens maintain dominant North American positions with integrated CO2 monitoring and demand-controlled ventilation platforms supporting energy optimization and occupant health management. Regulatory initiatives including EPA’s National Ambient Air Quality Standards (NAAQS), OSHA workplace environmental monitoring requirements, and local building code mandates are driving sustained sensor deployment across commercial and institutional facilities. The North American market is projected to grow at 5.8% CAGR from 2026-2033, with growth concentrated in retrofit projects upgrading legacy HVAC systems, IoT-enabled sensor platform deployments, and integration with advanced building management system analytics supporting predictive maintenance and energy efficiency optimization.

Europe CO2 Sensors Market Trends and Insights

Europe with Germany, United Kingdom, France, and Spain as leading markets is characterized by stringent environmental regulations, emphasis on sustainable building practices, and advanced smart city initiatives. European regulatory frameworks including EU Building Energy Efficiency Directive (EPBD), Indoor Air Quality Guidelines, and EN 13779 ventilation standards establish mandatory requirements for CO2 monitoring and demand-controlled ventilation in commercial buildings, schools, and public facilities.

Europe leads globally with strong environmental regulations driving CO2 sensor adoption, accounting for approximately 33% of global demand in 2024 according to industry analysis. The region’s emphasis on green building certification (including LEED, BREEAM, and EU Green Building Council standards) incorporates CO2 sensors as essential components of sustainable building design and operation.

Major cities across Europe including Berlin, London, Paris, and Amsterdam are deploying smart city infrastructure featuring integrated environmental sensor networks, real-time air quality monitoring, and data-driven urban planning initiatives incorporating CO2 monitoring capabilities. The European market is projected to grow at 6.9% CAGR from 2026-2033, driven by regulatory harmonization across EU member states, expansion of smart city initiatives, and increasing adoption of IoT-connected CO2 monitoring platforms supporting centralized environmental management across municipal and commercial facility portfolios.

Asia Pacific CO2 Sensors Market Trends and Insights

Asia Pacific dominates the global CO2 Sensors market with approximately 41% market share in 2025, propelled by rapid urbanization, accelerating air quality awareness, and explosive growth of smart building infrastructure across China, India, Japan, and Southeast Asian economies. China commands approximately 40-42% of Asia Pacific regional demand, supported by government mandates for smart city development, green building initiatives, and accelerating adoption of advanced building automation systems across commercial, residential, and industrial facilities.

India represents the fastest-growing major market within Asia Pacific with rapidly growing awareness of air pollution impacts on human health, increasing deployment of smart city infrastructure across major metropolitan areas, and government investment in smart building technologies supporting occupant health and energy efficiency. Japan maintains technological leadership in CO2 sensor design and deployment, with manufacturers including Sensirion, Vaisala, and Figaro advancing miniaturization, ultra-low-power operation, and integration with sophisticated HVAC control algorithms.

Southeast Asian markets including Vietnam, Thailand, Indonesia, and Malaysia are experiencing rapid commercial building development with emerging adoption of smart HVAC systems incorporating CO2 sensors and occupancy-responsive ventilation controls. Asia Pacific is forecast to grow at 8.1% CAGR from 2026-2033, driven by China’s smart city expansion, India’s growing air quality concerns, Japan’s technological innovation leadership, and emerging market adoption of portable CO2 sensors and consumer air quality monitoring devices.

Competitive Landscape

Market Structure Analysis

The global CO2 sensors market is moderately consolidated, with 25–30 key manufacturers collectively capturing a sizable market revenue, while fragmentation persists in niche applications such as industrial monitoring, automotive cabin air quality, and portable consumer devices. Competitive strategies focus on vertical integration of sensor components, geographic expansion into high-growth regions like China, India, and Southeast Asia, and technology differentiation through miniaturized NDIR designs, AI-enabled edge processing, low-power wireless sensors, and multi-sensor fusion.

Companies also pursue M&A to acquire specialized technology, and form ecosystem partnerships with building automation, HVAC, and IoT platform providers. Emerging business models include sensor-as-a-service solutions offering cloud-based analytics, predictive maintenance, and subscription-based environmental intelligence platforms, enabling manufacturers to provide integrated, value-added solutions while capturing recurring revenue streams and strengthening market positioning in commercial, industrial, and consumer segments.

Key Market Developments

- August 2024: Renesas has launched the RRH62000, an ultra-compact multi-sensor module for smart air quality monitoring in homes, schools, and public buildings. Measuring PM, TVOC, eCO2, IAQ, temperature, and humidity in a 10.5x10.5x2.7mm package, it enables precise IAQ assessment with low power and I2C interface.

- April 2025: Sensirion has launched the upgraded SCD43 photoacoustic CO2 sensor, enhancing the SCD4x platform. It delivers ±(30ppm + 3% m.v.) accuracy, ASHRAE 62.1 and WELL v2 compatibility, compact 10.1x10.1x6.5mm size, and 5,000ppm range for precise indoor air quality monitoring, available summer 2025.

October 2025: Gas Sensing Solutions Ltd. has launched the upgraded CozIR-LP Series 2 CO2 sensor with integrated temperature and humidity sensing. It offers ultra-low power (1.3–1.5 mA active, 0.01 mA sleep), ±45ppm accuracy, 3.25–5.5 V supply, UART/I2C interfaces, and <45s response time for IoT, smart buildings, and IAQ applications.

Companies Covered in CO2 Sensors Market

- Siemens AG

- Honeywell International

- Vaisala Oyj

- SenseAir (Asahi Kasei)

- Amphenol Corporation

- Cubic Sensor and Instrument Co.

- ELT SENSOR Corp.

- Sensirion AG

- Trane

- E + E ELEKTRONIK

- Figaro

- Gas Sensing Solutions

- Digital Control System Inc

- Zhengzhou Winsen Electronics Technology Co.

- Cubic Sensor and Instrument Co. Ltd.

Frequently Asked Questions

The global CO2 Sensors market is projected to reach US$ 694.2 million in 2026, growing from US$ 475.8 million in 2020.

Demand is driven by smart building adoption, DCV systems, IoT-enabled sensors, miniaturized NDIR technology, and rising consumer air quality awareness.

Asia Pacific leads with 41% market share, led by China, India, Japan, and expanding Southeast Asian smart infrastructure.

Integrated multi-sensor platforms combining CO2, PM2.5, VOC, and occupancy sensing with AI-driven building optimization present the primary opportunity.

Leading players include Siemens, Honeywell, Vaisala, Amphenol, and Sensirion, focusing on component integration, miniaturization, AI processing, and multi-sensor solutions.