- Processed Food

- Bread Crumbs Market

Bread Crumbs Market Size, Share, and Growth Forecast, 2025 - 2032

Bread Crumbs Market By Product Type (Plain/Dry, Seasoned), Form (Dry, Fresh), End-Use (Food Processing, Foodservice/QSR), Distribution Channel and Regional Analysis for 2025 - 2032

Bread Crumbs Market Size and Trends Analysis

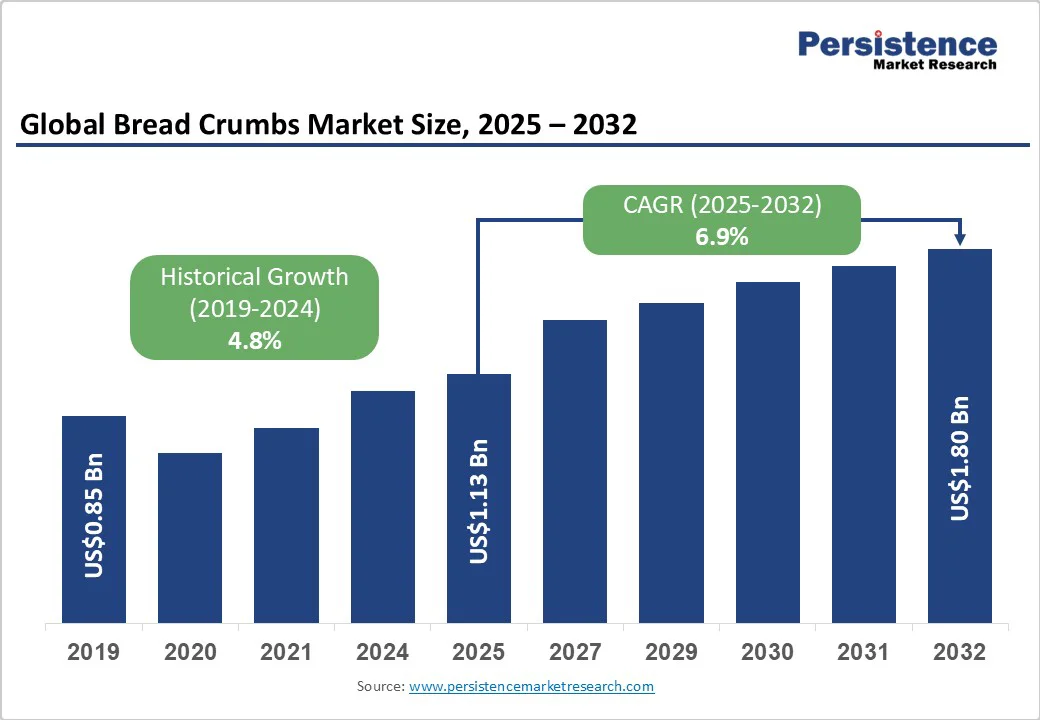

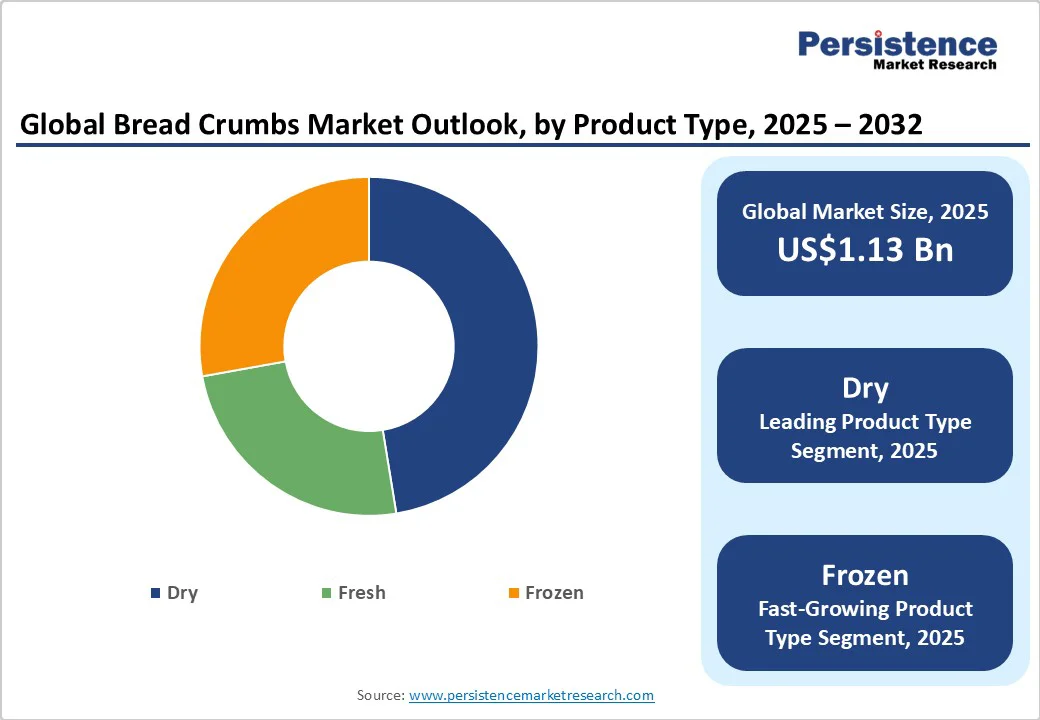

The global bread crumbs market was valued at US$1.13 Bn in 2025 and is projected to reach US$1.80 Bn by 2032, growing at a CAGR of 6.9% between 2025 and 2032.

The bread crumbs market is experiencing steady growth, fueled by increasing consumption of convenience foods and the expansion of foodservice networks globally. The rise of frozen and ready-to-eat meals , coupled with the growing demand for gluten-free, whole-grain, and panko breadcrumbs, is creating higher value opportunities.

Automation in production lines and improved coating technology allow manufacturers to scale efficiently while maintaining consistent quality. Asia Pacific’s large population base and rising urbanization are supporting volume growth, while North America and Europe continue to lead in premium and specialty products.

Key Industry Highlight

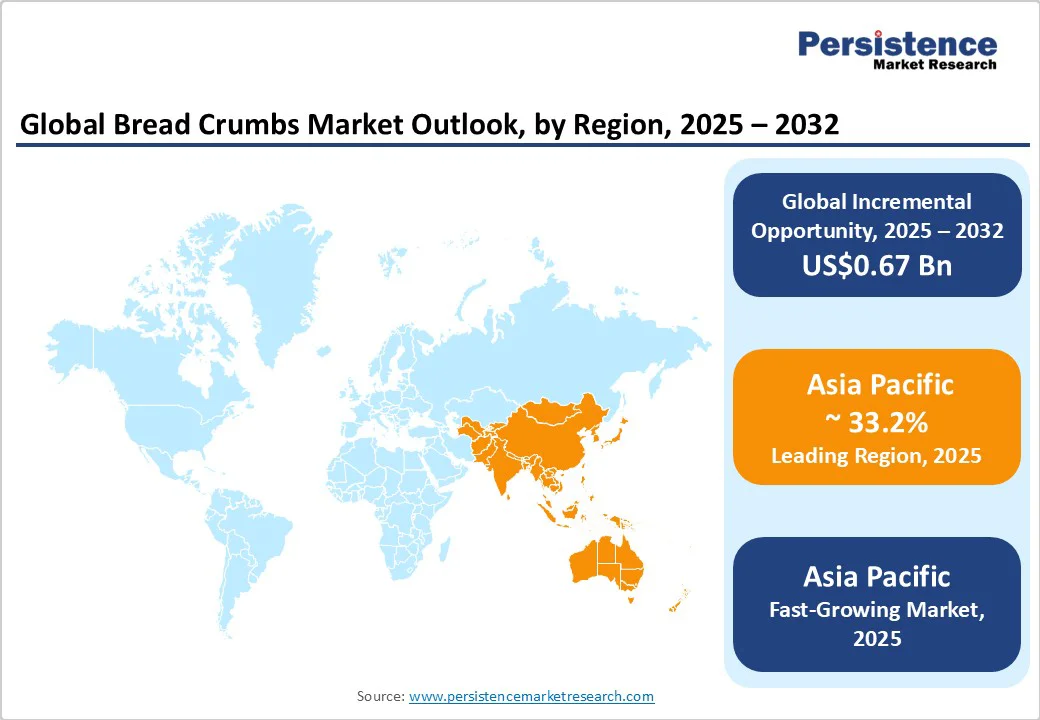

- Leading Region: Asia Pacific holds the largest market share at approximately 33.2%, driven by large-scale food processing, low manufacturing costs, and rising adoption of Western-style convenience foods.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region in terms of value, supported by expanding QSR networks, rising frozen-food consumption, and investment in private-label and specialty breadcrumb production.

- Investment Plans: Major players are investing in automation, allergen-segregated production lines, and functional/flavored breadcrumb development, with expansions in Japan, China, and the U.S. to meet premium and industrial demand.

- Dominant Product Type: Dry/plain breadcrumbs lead the market with a share of over 45.7%, valued for their long shelf life, versatility, and broad use across retail, foodservice, and industrial applications.

- Leading Form: Dry form breadcrumbs dominate due to storage and logistics advantages, accounting for approximately 50% of total market volume, widely used in industrial coating, filling, and bakery applications.

| Key Insights | Details |

|---|---|

| Bread Crumbs Market Size (2025E) | US$1.13 Bn |

| Market Value Forecast (2032F) | US$1.80 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of Foodservice & QSR Channels

Bread crumbs are an essential ingredient for QSR menus, frozen meals, and casual dining offerings. The proliferation of fast-food outlets and frozen-food consumption, especially in emerging markets, has significantly increased institutional demand.

Automation in production lines allows for higher throughput and cost efficiency, helping manufacturers meet the growing requirements of large-scale food processors and QSR chains. The QSR segment alone contributes more than 30% of industrial demand globally, according to recent market data.

Product Premiumization & Specialty Offerings

The introduction of premium breadcrumb varieties, including panko, gluten-free, whole-grain, and flavored options, is driving higher revenue per kilogram. These products cater to consumer preferences for healthier, functional, or texturally unique foods.

For example, gluten-free panko appeals to the growing number of consumers with dietary restrictions, while whole-grain and fiber-rich variants are marketed for health-conscious households. The premium segment is projected to grow at a CAGR of 8% during 2025-2032.

Supply-Side Integration & Efficiency Gains

Bakers and co-packers converting surplus bread into breadcrumbs are investing in dedicated lines and automated coating equipment. This reduces raw material waste, lowers unit costs, and ensures consistent product quality.

Vertical integration allows manufacturers to supply both industrial and retail customers efficiently, strengthening long-term contracts and market presence. Companies investing in integrated production systems have achieved throughput increases of 15-20% without significant increases in labor costs.

Technological Advancements in Processing & Packaging

Innovations in drying, grinding, and coating technology have improved product uniformity, shelf life, and application versatility. Pre-breaded frozen products, such as chicken nuggets and fish sticks, require precise crumb sizing and consistent adherence to ensure quality. Advanced packaging solutions, including vacuum-sealed and modified-atmosphere packaging, have extended shelf life and improved logistics efficiency, particularly in emerging markets with challenging cold-chain infrastructure.

Volatility in Raw Material & Energy Costs

Breadcrumb production depends on wheat and bread by-products. Fluctuating wheat prices and energy costs directly impact production expenses, particularly for small-scale producers. For instance, a 10% spike in wheat prices can translate to a 3-5% increase in finished breadcrumb costs, challenging margin stability for both industrial and retail suppliers.

Manufacturers targeting institutional clients and QSRs must comply with rigorous food-safety standards, including HACCP, BRC, and FSSC 22000 certifications. Non-compliance can restrict market access, especially in North America and Europe. Smaller producers may face high capital expenditure and recurring compliance costs, limiting their growth potential.

Intense Competition from Private Label & Local Producers

Private-label manufacturers and regional suppliers often compete aggressively on pricing. Large multinational brands face pressure from local players in both retail and industrial channels, particularly in Asia Pacific and Latin America. This limits pricing power and necessitates continuous product innovation and differentiation.

Growth in Gluten-Free & Health-Oriented Segments

Gluten-free and specialty breadcrumbs are gaining traction in both retail and industrial channels. The segment offers higher margins, with premium pricing ranging from 20-40% above standard breadcrumbs. Rising health consciousness and demand for allergen-safe ingredients create a significant market potential, estimated at approximately US$ 120-200 million in additional revenue by 2030 in developed regions.

Expansion of Private-Label & Co-Packing Agreements

Emerging markets are witnessing a surge in local food processors and QSRs requiring cost-effective breadcrumb solutions. Contract baking and private-label partnerships provide a scalable route to supply these markets. Conservative projections suggest a 10-15% increase in private-label penetration across Asia Pacific and Latin America by 2030, translating to significant incremental demand.

Functional & Flavored Breadcrumb Innovations

Manufacturers are exploring functional ingredients, such as fiber-enriched or protein-fortified breadcrumbs, and flavored variants to meet evolving consumer preferences. Functional breadcrumbs can be used in premium frozen meals or ready-to-eat snacks, creating new revenue streams and enhancing brand differentiation in both retail and industrial segments.

Category-wise Analysis

Product Type Insights

Dry or plain breadcrumbs account for the largest market share due to their long shelf life, versatility, and cost-effectiveness. They are extensively used in retail packaged products, industrial coatings, and foodservice applications. For instance, they are a staple ingredient in frozen chicken nuggets, meatballs, and bakery coatings, providing texture and volume while reducing product cost.

Manufacturers like General Mills and Hearthside Food Solutions supply dry breadcrumbs in bulk to QSRs and processed food manufacturers, ensuring consistent quality for large-scale applications. The durability of dry breadcrumbs allows retailers and processors to store them for extended periods without degradation, enhancing supply chain efficiency.

Panko and specialty breadcrumbs are the fastest-growing product types, driven by consumer demand for texture, premiumization, and health-oriented alternatives. Panko, originally popularized in Japanese cuisine, provides a lighter, crispier texture that absorbs less oil, making it ideal for air-fried foods and plant-based proteins.

Specialty variants include gluten-free, whole-grain, flavored, and organic breadcrumbs, which are increasingly used in premium frozen foods, gourmet meal kits, and upscale restaurant applications. For example, Aleia’s Gluten Free Foods offers panko-style breadcrumbs catering to both home cooks and commercial kitchens, while DeLallo’s specialty flavored crumbs target European-style culinary preparations. Rising consumer interest in healthier cooking methods, such as air frying, has also accelerated adoption of these premium segments.

Form Insights

Dry breadcrumbs dominate the market with a share of over 45.7%, due to their logistics and storage advantages, as well as compatibility with diverse industrial applications. Food processors rely on dry crumbs for consistent batter coatings, breaded toppings, and fillers in products like chicken tenders, fish sticks, and snack extrusions.

For example, companies like Kikkoman and 4C Foods supply dry breadcrumbs in large-volume packaging for commercial bakers and frozen-food manufacturers, ensuring standardized crumb size and moisture content. Their longer shelf life and ability to blend with spices or functional food ingredients also make them highly adaptable across different cuisines and product categories.

Frozen breadcrumbs, often integrated into pre-breaded products like chicken nuggets, fish fillets, and plant-based protein alternatives, are experiencing rapid growth due to convenience-driven consumer demand and foodservice expansion. This segment commands higher unit prices and often involves co-packing arrangements where manufacturers prepare breaded, ready-to-cook products for retailers or QSRs.

For instance, frozen breaded fish sticks or vegan nuggets from brands such as Gonnella Baking Company and 4C Foods are increasingly supplied to both retail and foodservice chains. The frozen form allows for precise portioning, better adherence of coatings, and reduced food waste, supporting the scaling of menu innovation in QSR and frozen-food categories.

End-Use Insights

Industrial food processing is the largest end-use segment, accounting for the majority of volume demand. Bread crumbs are used as binders, coatings, and fillers across products including frozen chicken, meatballs, snack extrusions, and bakery coatings.

Major food processors like Nestlé and Tyson Foods rely on standardized breadcrumbs to maintain consistency, texture, and flavor across large production batches. Dry and specialty crumbs are blended into pre-mix formulations, allowing processors to innovate with new flavors or functional properties while ensuring uniform performance in frying, baking, or extrusion processes.

The foodservice and QSR segment is the fastest-growing due to menu diversification, premiumization, and expansion in emerging markets. Chains like McDonald’s, KFC, and Burger King utilize bread crumbs in items such as chicken nuggets, fish sandwiches, and vegetarian patties. The trend toward plant-based proteins and air-fried menu options has further increased demand for premium breadcrumbs, including panko and gluten-free variants.

In emerging markets, rapid urbanization and adoption of Western-style QSRs are driving new breadcrumb consumption for localized menu innovations. Additionally, smaller independent restaurants and cloud kitchens increasingly adopt pre-breaded frozen solutions, creating incremental demand for co-packing partnerships and specialty products.

Regional Insights

North America Bread Crumbs Market Trends - Growth Driven by QSR Expansion and Health-Focused Innovation

North America represents a mature and highly competitive market, led by the United States, which dominates both industrial and premium retail segments. The region’s growth is driven by high QSR penetration, frozen-food consumption, and evolving consumer preferences for convenience foods. Major players like General Mills, Hearthside Food Solutions, and Gonnella Baking Company have invested in automation and allergen-segregated production facilities to meet stringent FDA and FSMA compliance standards.

The U.S. market also sees strong private-label growth, with large retailers such as Walmart and Kroger offering branded and private-label breadcrumb products, including gluten-free and panko variants. Frozen and pre-breaded product demand is rising due to the popularity of frozen chicken nuggets, fish sticks, and plant-based protein products. In March 2025,

General Mills launched a new line of whole-grain breadcrumbs for foodservice and retail channels, emphasizing health-oriented product positioning. In January 2024, Hearthside Food Solutions expanded its U.S. production facilities to include a dedicated panko line with automated coating technology, enabling higher output and consistency.

Europe Bread Crumbs Market Trends - Culinary Heritage Meets Innovation in Premium and Functional Crumbs

Europe’s breadcrumb market is diverse and innovation-driven, with Germany, the U.K., France, and Spain leading both industrial and premium retail segments. Growth is underpinned by culinary traditions, foodservice expansion, and increasing adoption of premium and organic breadcrumbs. Companies like DeLallo, Kerry Group, and local artisanal bakers are focusing on traceable supply chains, functional ingredient integration, and flavored or specialty crumbs.

EU-wide food-safety harmonization, including BRCGS and ISO certifications, ensures high-quality standards but increases the entry barrier for smaller producers. The market has seen growing demand for panko, whole-grain, and gluten-free variants, particularly in urban centers where Western-style convenience and fast-casual dining are popular.

In June 2024, Kerry Group launched a line of plant-based breadcrumb coatings for QSR chains in Germany and the U.K., targeting healthier and vegan menu options. In September 2023, DeLallo introduced artisan-style flavored breadcrumbs in France and Spain to cater to premium home cooking trends.

Germany is Europe’s largest breadcrumb consumer, accounting for approximately 25% of the regional market. Its demand is largely driven by industrial food processing and growing QSR penetration, particularly in urban areas. The trend toward gluten-free and organic breadcrumbs is especially strong in retail channels.

Asia Pacific Bread Crumbs Market Trends - Rapid Expansion Fueled by Export Demand and Westernized Consumption

Asia Pacific dominates holding a market share of around 33.2% globally and is the fastest-growing region. Key markets include China, Japan, India, and ASEAN countries, driven by large-scale food processing, low manufacturing costs, and rising adoption of Western-style convenience foods.

The region benefits from both domestic consumption and export opportunities, with manufacturers producing panko, frozen pre-breaded products, and specialty breadcrumbs for international clients. Foodservice expansion, particularly the growth of QSR chains such as KFC, McDonald’s, and local fast-food outlets, is fueling breadcrumb consumption.

Functional and flavored breadcrumbs are increasingly adopted for frozen snacks, plant-based proteins, and ready-to-eat meals. Private-label production is also gaining traction to serve growing demand in both retail and institutional channels.

In April 2025, Kikkoman Corporation expanded its panko production facility in Japan to meet increasing demand for export markets and domestic QSR chains. In December 2024, a leading Indian co-packer launched gluten-free breadcrumbs catering to both retail and frozen-food segments, aligning with health-conscious trends.

China is the largest volume contributor in Asia Pacific, accounting for nearly 40% of the regional market, with rapid urbanization, growth of frozen food processing, and Western QSR adoption driving robust expansion. Premium breadcrumbs, such as panko and flavored varieties, are increasingly popular in metro cities, reflecting rising consumer preference for high-quality convenience foods.

Competitive Landscape

The global bread crumbs market is moderately fragmented among regional producers. Leading players dominate retail and industrial contracts, while private-label manufacturers serve large food processors. Key strategies include product innovation, vertical integration, co-packing partnerships, and premium SKU development. Differentiation arises from allergen segregation, functional product lines, and premiumized packaging.

Key Industry Developments

- In July 2025, Bon Food Industries Sdn Bhd introduced a new line of plant-based breadcrumbs in Malaysia, tapping into the rising trend of plant-based diets and catering to vegetarian and vegan consumers.

- In August 2025, Ripon Select Foods Limited partnered with a leading global QSR chain to supply custom-formulated breadcrumbs for their new product line, showcasing the increasing collaboration between ingredient suppliers and foodservice providers.

Companies Covered in Bread Crumbs Market

- Kikkoman Corporation

- General Mills, Inc.

- Hearthside Food Solutions

- Gonnella Baking Company

- DeLallo

- 4C Foods Corporation

- Vigo Importing Co.

- Edward & Sons Trading Co.

- Aleia’s Gluten Free Foods

- Kerry Group

- Nisshin Flour Milling

- Bon Food Industries Sdn Bhd

- Newly Weds Foods

- Sysco Corporation

- McCain Foods Limited

- J.R. Simplot Company

- Bimbo Bakeries USA

- ConAgra Foods, Inc.

- Rich Products Corporation

- Grupo Bimbo S.A.B. de C.V.

Frequently Asked Questions

The global bread crumbs market size was valued at US$ 1.13 Bn in 2025.

The market is projected to reach US$ 1.80 Bn by 2032, growing at a CAGR of 6.9% between 2025 and 2032.

Key trends include the growth of panko and specialty breadcrumbs for air-fried and plant-based foods and the expansion of QSR and foodservice channels, particularly in the Asia Pacific.

The dry/plain breadcrumbs segment is the market leader, accounting for over 45.7% of total market share, due to its versatility, long shelf life, and broad usage across retail, industrial, and foodservice applications.

The market is expected to grow at a CAGR of 6.9% from 2025 to 2032.

Major players include Kikkoman Corporation, General Mills, Inc., Hearthside Food Solutions, Gonnella Baking Company, and DeLallo.