- Processed Food

- Bread Mixes Market

Bread Mixes Market Size, Share, and Growth Forecast, 2025 – 2032

Bread Mixes Market By Product Type (Gluten-Free Bread Mixes, Organic Bread Mixes), Form (Dry Bread Mixes, Liquid/Ready-to-Use Mixes), End-user, and Regional Analysis for 2025 - 2032

Bread Mixes Market Size and Trends Analysis

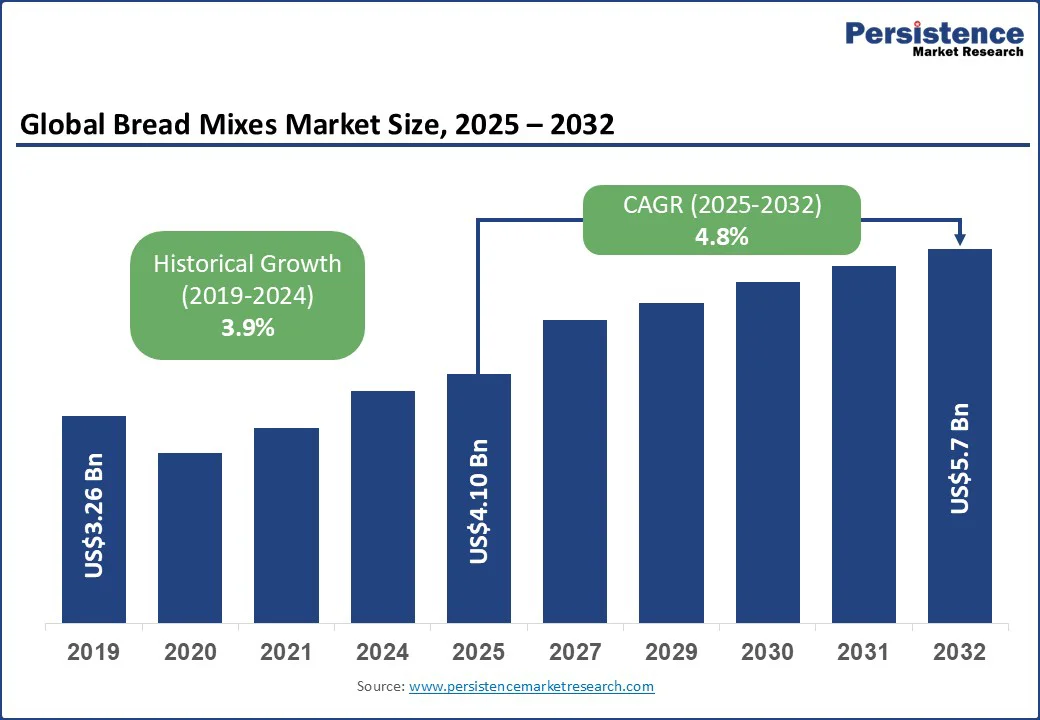

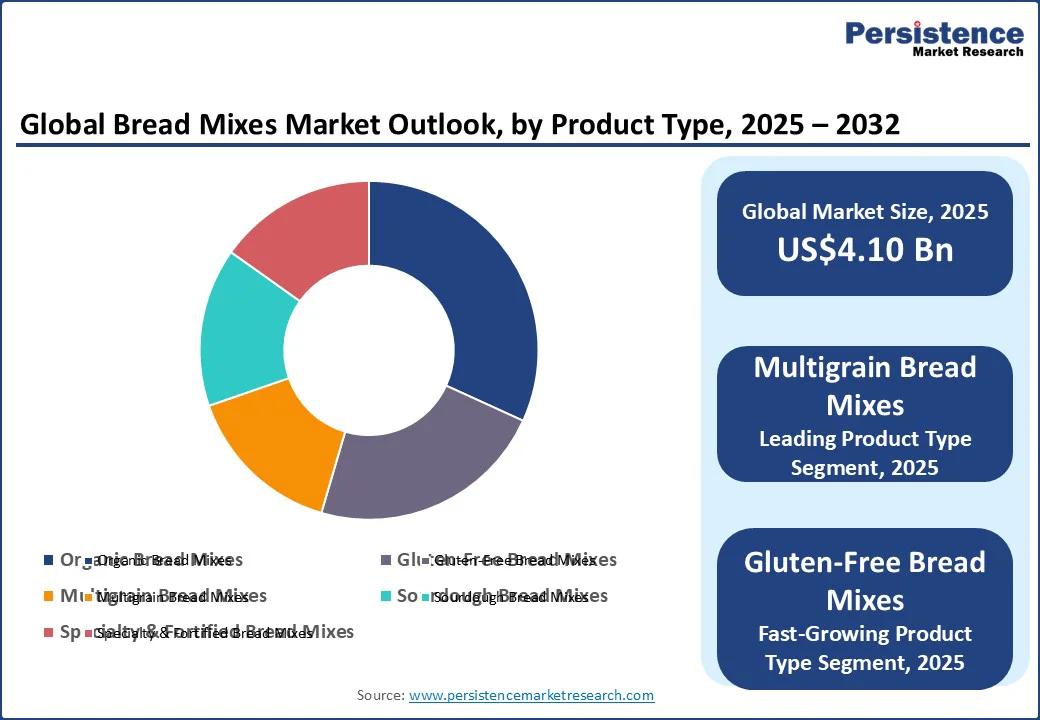

The global bread mixes market size is likely to be valued at US$4.10 Bn in 2025 and is expected to reach US$ 5.7 Bn by 2032, growing at a CAGR of 4.8% during the forecast period from 2025 to 2032, driven by the rising demand for convenient, high-quality solutions that replicate bakery-style results at home.

Key Industry Highlights:

- Leading Region: Europe is anticipated to lead with a 32.6% share in 2025, driven by its strong bread culture and long-standing consumer preference for artisanal and specialty varieties such as sourdough, multigrain, and rye.

- Fastest-growing Region: Asia Pacific is the fastest-growing market, with rapid adoption in India and China, driven by localization of flavors, urban lifestyles, and collaborations such as Puratos’ partnerships with Indian bakeries.

- Investment Plans: Companies are investing in new product lines that focus on gluten-free, organic, and fortified bread mixes, alongside D2C digital platforms. Recent launches by King Arthur Baking and General Mills highlight this shift.

- Dominant Product Type: Multigrain bread mixes are anticipated to dominate, holding a market share of around 21% in 2025, catering to rising consumer demand for healthier and specialty bakery solutions.

- Leading Form: Dry bread mixes are anticipated to lead with over 57% share in 2025, due to their long shelf life, easy storage, and widespread use in both households and commercial bakeries.

| Key Insights | Details |

|---|---|

| Bread Mixes Market Size (2025E) | US$ 4.10 Bn |

| Market Value Forecast (2032F) | US$ 5.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Specialty Formulations and Home Baking Culture Reshape Consumer Demand

The bread mixes market is strongly influenced by innovation in specialty formulations. Consumers are increasingly drawn toward multigrain and ancient-grain bread mixes that incorporate nutrient-rich ingredients such as quinoa, amaranth, and millet. This shift aligns with the popularity of functional nutrition and fuels the demand for gluten-free bread mix for specialty diets. At the same time, the growth of e-commerce platforms offering keto-friendly high-protein bread mixes has opened up wider access for health-conscious buyers, enabling niche products such as allergen-free and keto-adapted bread mixes to reach mainstream retail channels.

Another key driver is the continued momentum of home baking in the COVID-19 pandemic, which has now evolved into a sustained lifestyle trend. Many households are seeking ready-to-bake artisan sourdough bread mix kits, which deliver gourmet quality with minimal preparation. Busy urban consumers also favor convenient pre-measured clean-label bread-mix solutions that reduce baking time while offering transparency in ingredients. This has encouraged brands to expand their portfolios with organic bread mix packs with simplified preparation, meeting the dual demand for convenience and healthier eating options.

Ingredient Volatility and Traditional Preferences Hinder Market Penetration

A key restraint in the market is the issue of ingredient-supply volatility impacting bread mix consistency. Fluctuations in wheat yields and the availability of alternative grains can result in noticeable variations in flavor, texture, and quality across different batches. This inconsistency reduces consumer trust, particularly among experienced bakers who value predictable outcomes. At the same time, many consumers remain loyal to from-scratch family recipes, preferring the control and personalization of mixing their own ingredients rather than relying on pre-blended solutions. In regions where traditional baking culture is deeply rooted, this preference slows down the adoption of packaged bread mixes.

Another challenge comes from rising competition with bakery alternatives. Many consumers are increasingly opting for fresh artisan bakery loaves over packaged bread mixes, drawn by the texture, aroma, and immediate convenience of ready-to-eat products. Shifting dietary preferences are creating new substitutes for conventional mixes, with a growing number of people turning to low-carb cauliflower-based bread alternatives or diets that favor ketogenic and paleo-friendly options.

Functional Gut-Health Mixes and Customization Open New Growth Paths

One major opportunity in the bread mixes market lies in developing premium gut-health functional bread mixes with prebiotics and probiotics. As consumers become more conscious of digestive wellness, there is a growing demand for convenient products that combine traditional baking with added health benefits. Another promising direction is the introduction of AI-customized artisan sourdough starter bread mix offerings, where technology can help tailor flavor, fermentation styles, and ingredient blends to meet niche consumer preferences. This approach enhances personalization and also creates new ways for brands to differentiate in a competitive marketplace.

There is also significant potential in direct-to-consumer global subscription boxes focused on exotic heritage bread mix kits. These offerings could feature unique blends such as millet-and-herb loaves or Mediterranean spiced breads, paired with step-by-step instructions for an authentic baking experience. By blending cultural exploration with the convenience of pre-measured ingredients, such kits appeal to food enthusiasts looking for creativity at home.

Category-wise Analysis

Product Type Insights

Multigrain bread mixes are anticipated to lead with a share of 21% in 2025. Consumers are increasingly prioritizing health-conscious choices, and multigrain options offer the perceived benefit of nutrient diversity, fiber content, and lower glycemic impact. Ancient grains, including quinoa, millet, amaranth, and spelt, have gained popularity due to their association with traditional, less-processed diets. These mixes cater to both mainstream and health-oriented consumers. They are positioned as balanced options, neither too niche nor overly restrictive, making them appealing to a broad demographic, from families to fitness enthusiasts.

For instance, King Arthur Baking Company offers a Whole Grain Bread Mix that includes ancient grains such as spelt and millet, popular among home bakers seeking hearty and nutritious alternatives to white bread.

Gluten-free bread mixes are the fastest-growing segment, driven by the rising number of people with celiac disease, gluten sensitivity, and those choosing a gluten-free lifestyle for perceived health benefits. Even though only a small percentage of the population requires a gluten-free diet for medical reasons, there is a widespread belief that gluten-free products are healthier, easier to digest, or beneficial for weight management. This perception, along with better formulations and improved taste and texture of gluten-free mixes, has fueled rapid adoption.

Bob’s Red Mill Gluten Free Homemade Wonderful Bread Mix is a leading example, widely praised for producing a soft, flavorful loaf that rivals traditional bread, helping to normalize gluten-free baking at home.

Form Insights

The largest segment by form is dry bread mixes, which are likely to account for over 57% share in 2025. These mixes dominate owing to their longer shelf life, ease of storage, and wide adoption by both households and commercial bakeries. Dry formulations are also versatile, allowing consumers to customize recipes while still enjoying the convenience of pre-measured blends. Their popularity in supermarkets and online platforms has further cemented their market leadership.

Ready-to-use bread mixes are the fastest-growing segment. These products combine the convenience of quick preparation with the rising demand for organic, health-oriented solutions. For example, ready-to-use organic bread mix kits sold via e-commerce platforms are increasingly popular among busy urban consumers who want to enjoy homemade baking without compromising on health or quality. This blend of convenience and wellness makes the segment highly attractive for future growth.

Regional Insights

Europe Bread Mixes Market Trends - Artisanal Heritage and Modern Nutrition and Premiumization

Europe is anticipated to account for the leading position in the bread mixes market with a share of 32.6% in 2025. This dominance is largely due to the region’s strong bread culture, where consumers have long preferred artisanal and specialty varieties such as sourdough, multigrain, and rye.

The U.K. is witnessing notable structural shifts within its bakery industry. The acquisition of Hovis by AB Foods highlights the trend toward consolidation, giving the company a greater scale while also providing opportunities to expand into healthier and more premium categories. This change reflects the broader shift in consumer behavior, as more households move away from mass-packaged loaves in favor of higher-quality alternatives.

In Germany, consumer loyalty to traditional bread-making remains strong, with products like artisanal rye and multigrain loaves continuing to dominate. Brands such as Mestemacher are thriving by combining these traditional baking practices with modern health trends, particularly organic and whole-grain options, making them highly relevant to today’s wellness-focused consumers.

North America Bread Mixes Market Trends - Health-Conscious Innovation and Direct-to-Consumer Expansion

North America is undergoing steady transformation for bread mixes. It is driven by innovation from both established brands and emerging niche players. Companies such as General Mills have recently expanded their Gold Medal and Betty Crocker lines with gluten-free bread mixes, catering to the growing population of health-conscious consumers. Similarly, ADM is introducing high-protein bakery blends that meet the demand for functional foods, where nutrition and convenience come together in everyday staples.

Another notable example is the King Arthur Baking Company, which has made significant strides in the direct-to-consumer space. Through its online platform, the company now offers premium sourdough kits and custom baking solutions, building stronger consumer loyalty while bypassing traditional retail distribution.

In the U.S., the market is seeing a clear push toward healthier formulations. Bob’s Red Mill continues to expand its gluten-free product portfolio, while Pillsbury has launched an organic ready-to-bake mix that reflects consumer interest in both convenience and clean-label foods. At the same time, larger companies such as Dawn Foods are adopting digital solutions such as AI-driven analytics to enhance consistency in production, ensuring that quality remains uniform across all batches.

In Canada, this shift toward health and wellness is equally evident. Brands such as Arrowhead Mills are gaining popularity among consumers who prioritize transparency and natural sourcing, signaling the importance of clean-label positioning in the region.

Asia Pacific Bread Mixes Market Trends - Fast-Paced Growth Anchored in Hybrid Flavors and Localization

Asia Pacific is emerging as the fastest-growing region, fueled by rapid urbanization, changing dietary habits, and increasing adoption of Western-style baked goods. The market for bread mixes is characterized by its ability to merge global bakery trends with strong local flavors. A prime example comes from Puratos, which has partnered with Indian bakery chains to co-develop bread mixes that reflect traditional regional tastes.

By combining international expertise with local food preferences, the company is broadening its consumer reach and reinforcing the cultural relevance of its products. Building on this trend, Puratos India has launched its “Easy Curry Masala Bread Mix,” which infuses everyday Western bread formats, such as loaves, buns, and pizza bases, with Indian spice blends. This approach is resonating particularly with younger consumers, who are open to experimenting with bold, hybrid flavors.

In China, bread mixes have become widely accepted as urban lifestyles drive demand for convenient bakery solutions. The country’s rapidly expanding bakery culture has encouraged global and domestic suppliers to design products tailored to local tastes, while also adopting sustainable packaging practices to align with consumer expectations.

India presents a slightly different picture, where bread mix consumption is expanding rapidly due to a mix of tradition and modern convenience. Collaborations between international players and local bakeries have introduced products that strike a balance between familiar Indian flavors and the practicality of ready-to-use mixes. These products have found strong appeal among millennials and Gen Z consumers who are both adventurous with food and mindful of convenience.

Competitive Landscape

The global bread mixes market is highly competitive, with a mix of global food giants and specialized baking brands shaping the landscape. Established players such as General Mills, ADM, and Puratos are leveraging their extensive distribution networks and R&D capabilities to diversify offerings into gluten-free, multigrain, and fortified categories. Their strategies focus on catering to the rising demand for healthier formulations, while also expanding portfolios through innovation in convenience-driven formats like ready-to-use and liquid bread mixes. These companies often rely on collaborations with local bakeries and retailers to strengthen regional market presence and meet specific consumer preferences.

Niche and premium-focused brands, including King Arthur Baking Company, Bob’s Red Mill, and Mestemacher, are carving out space by emphasizing authenticity, clean-label sourcing, and artisanal quality. Many of these players are adopting direct-to-consumer (D2C) models and e-commerce channels to build stronger brand-consumer relationships, particularly in North America and Europe. Startups and regional firms are also entering the scene with innovative, flavor-infused mixes tailored to local tastes, adding competitive pressure to legacy brands. This blend of scale-driven multinationals and agile niche players is fostering a dynamic environment where innovation, transparency, and adaptability are key to sustaining growth.

Key Industry Developments

- In May 2025, Arabian Mills introduced its new premium brand Master Mills, designed for both commercial and consumer markets. The launch included a portfolio of specialty flours, bread mixes, and baking solutions tailored to meet rising demand for convenience and consistent quality in the bakery and foodservice sectors.

- In March 2025, Birch Benders introduced its first line of organic bread and muffin mixes, with flavors such as Organic Blueberry and Organic Chocolate Chip. These mixes use real, organic ingredients and are designed for quick preparation, offering a healthier yet convenient option for consumers seeking bakery-quality results at home.

Companies Covered in Bread Mixes Market

- Cargill Inc.

- ADM

- Lesaffre SA

- Puratos Ltd.

- Bakels Worldwide

- Allied Mills Pty Ltd.

- Watson Inc.

- King Arthur Flour Company, Inc.

- Enhance Proteins Ltd.

- Swiss Bake Ingredients Pvt. Ltd.

- Pillsbury Company, LLC

- Echema Technologies, LLC

- Pamela’s Products Inc.

- Others

Frequently Asked Questions

The global bread mixes market size is estimated at US$4.10 Bn in 2025.

The bread mixes market is projected to reach US$5.69 Bn by 2032, reflecting steady growth.

Key trends include rising demand for gluten-free and organic bread mixes, growing adoption of multigrain and ancient-grain formulations, increasing preference for sourdough bread mixes, and expanding direct-to-consumer (D2C) bakery kits.

Multigrain bread mixes dominate the market, holding a significant share due to increasing consumer demand for healthier and allergen-free baking solutions.

The bread mixes market is expected to grow at a CAGR of 4.8% from 2025 to 2032, driven by rising health-conscious consumer behavior and innovation in specialty mixes.

Some leading companies with a strong product portfolio include General Mills (Gold Medal, Betty Crocker), King Arthur Baking Company, Puratos Group, Bob’s Red Mill Natural Foods, and Archer Daniels Midland Company.