- Automotive Components & Materials

- Autonomous Emergency Braking (AEB) Market

Autonomous Emergency Braking (AEB) Market Size, Share, and Growth Forecast, 2026- 2033

Autonomous Emergency Braking (AEB) Market by Product Type (Low-speed AEBS and High-speed AEBS), By Technology (Forward Collision Warning, Crash Imminent Braking, Dynamic Brake Support, and Others), By System Composition (Camera, LiDAR, Perception Processor, and ECU), Vehicle Type (Passenger Vehicle, and Commercial Vehicle), Brake Type (Disc and Drum) and Regional Analysis for 2026 - 2033

Autonomous Emergency Braking (AEB) Market Size and Trends Analysis

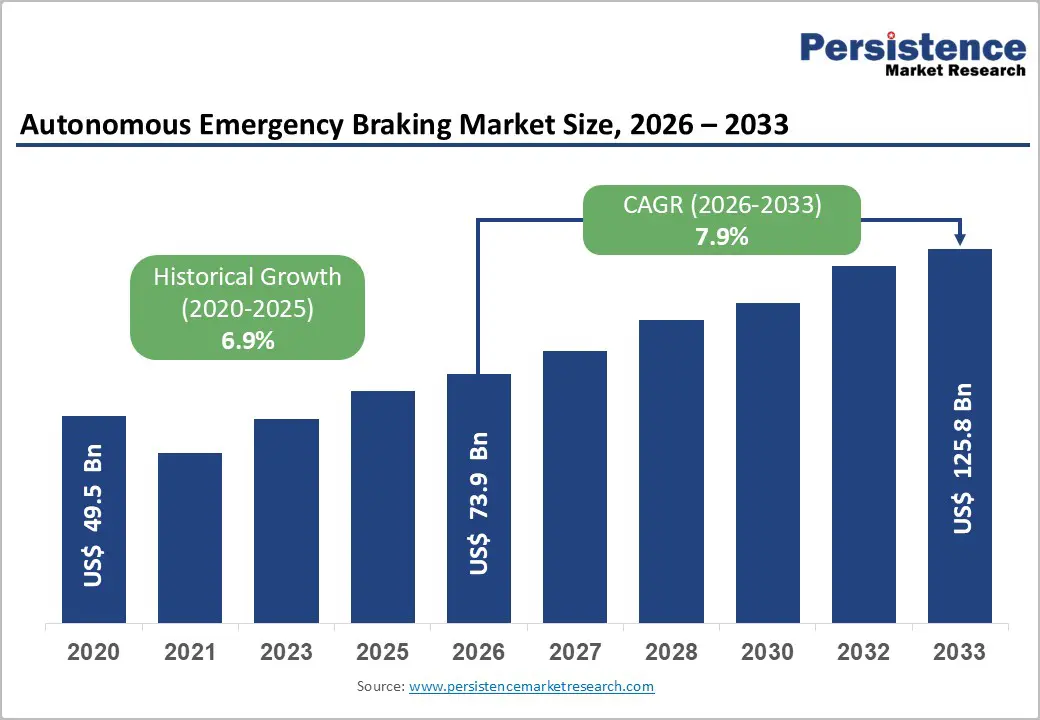

The global autonomous emergency braking (AEB) market size is likely to be valued at US$ 73.9 billion in 2026 and is projected to reach US$ 125.8 billion by 2033, growing at a CAGR of 7.9% between 2026 and 2033.

Strong growth is underpinned by increasingly stringent vehicle safety regulations, rapid integration of AEB into Advanced Driver Assistance Systems (ADAS), and advances in camera, LiDAR, and AI-based perception processors. Rising NCAP safety rating requirements and regulatory mandates in the EU, US, Japan, and other regions are structurally expanding fitment rates across passenger and commercial vehicles. Asia Pacific’s manufacturing strength and accelerating safety adoption further reinforce the market’s long-term expansion trajectory.

AEB systems use camera and LiDAR sensors to measure distance and relative speed to obstacles ahead, automatically activating braking when collision risk or sudden deceleration is detected, materially reducing rear-end collisions and mitigating crash severity. Technically, modern AEB architectures comprise a camera, LiDAR, a perception processor, an ECU, an acousto-optic warning system, and braking actuation, with sensor fusion in the perception processor and decision logic in the ECU that trigger warnings and emergency braking. Compared with traditional sensors, LiDAR delivers a longer range and higher profiling accuracy, enhancing the detection of both moving and stationary objects, including pedestrians and cyclists, and supporting robust 24-hour operation in complex environments.

A key competitive advantage of contemporary AEB solutions is sub-150 millisecond detection-to-alarm response time and continuous monitoring of blind spots and surrounding hazards, significantly reducing accidents linked to driver distraction or fatigue. Increasing integration of LiDAR and AI-enabled perception processors is elevating detection precision and expanding use cases beyond basic forward collision warning to include vulnerable road user protection and complex traffic scenarios. As intelligent mobility and software-defined vehicle architectures mature, AEB is rapidly evolving from a premium safety add-on to a standard, often mandated feature, anchoring its role as a cornerstone technology in making driving safer and vehicles smarter over the next decade.

Key Industry Highlights:

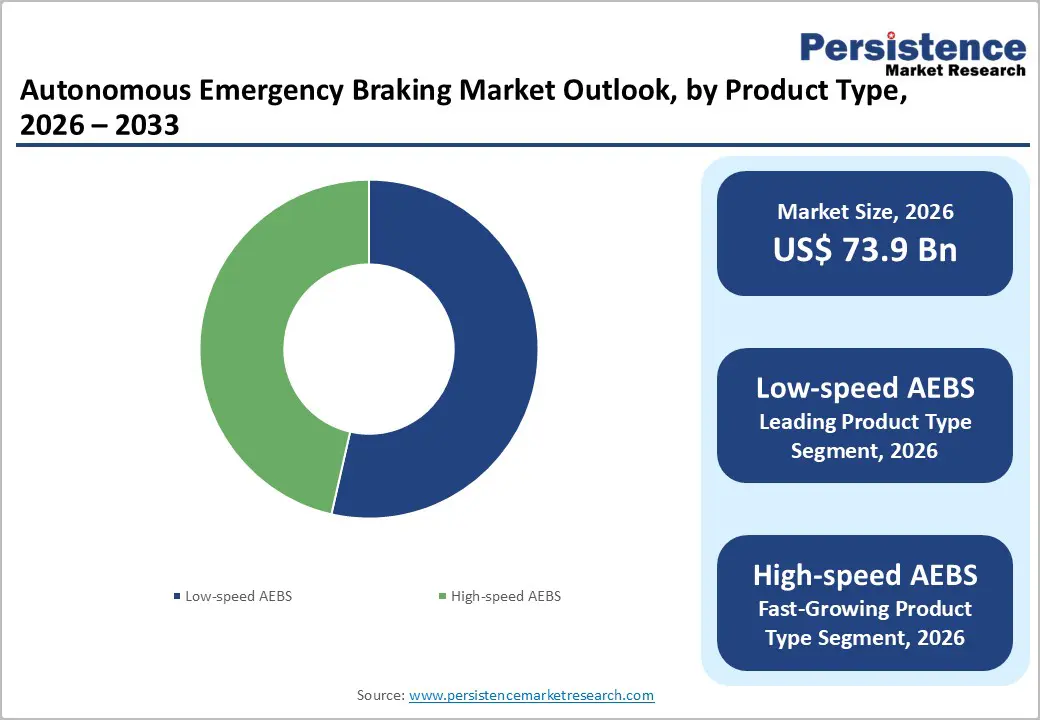

- Product Type Analysis: Low-speed AEBS (>55% share in 2026) and forward collision warning (>35% share) remain the dominant product and technology segments, while high-speed AEBS (8.8% CAGR) and crash imminent braking (≈9.1% CAGR) are the fastest-growing niches.

- Component Analysis: Camera-centric architectures lead with >35% revenue share, while LiDAR-based systems (≈9.5% CAGR) and AI-enhanced perception processors are the primary drivers of technology growth.

- Vehicle Type Analysis: Passenger vehicles account for over 65% of revenues, but commercial vehicles are the higher-growth segment (≈9.1% CAGR), driven by logistics safety, AEBS rules, and fleet economics.

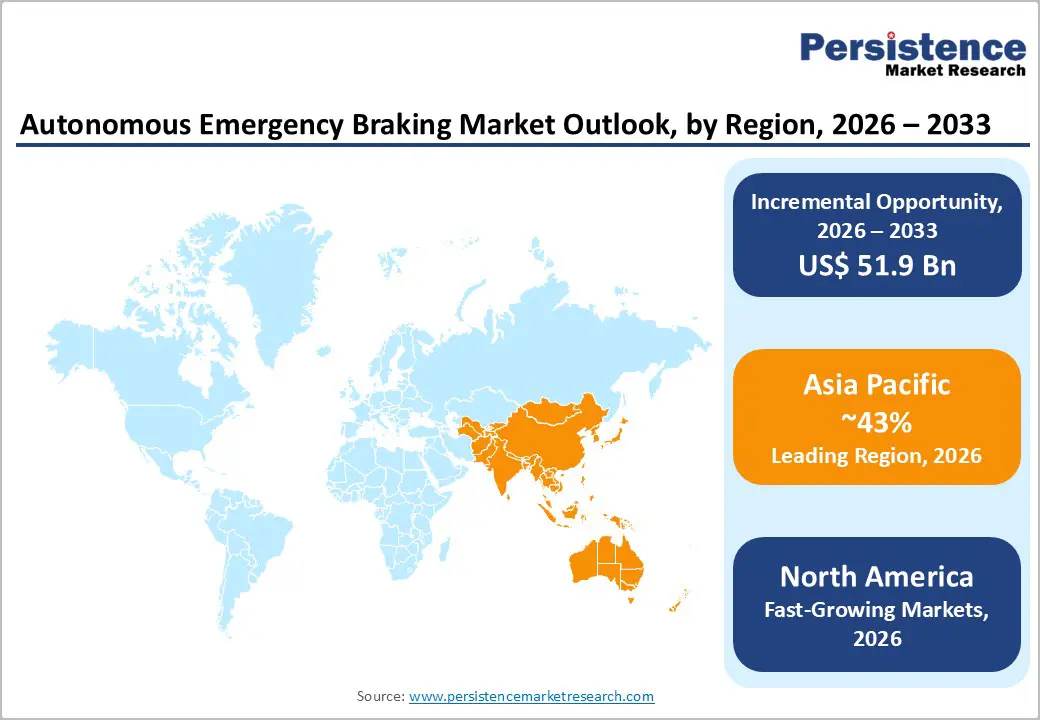

- Regional Analysis: Asia Pacific accounts for more than 40% of global AEB revenues, while North America is the fastest-growing region (~8.9% CAGR) driven by NHTSA’s AEB mandate and a strong innovation ecosystem.

| Key Insights | Details |

|---|---|

| Autonomous Emergency Braking (AEB) Market Size (2026E) | US$ 73.9 Bn |

| Market Value Forecast (2033F) | US$ 125.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.9% |

Market Dynamics

Drivers - Regulatory mandates and NCAP safety incentives

Governments and international bodies are moving decisively toward mandatory AEB fitment, creating structural, non-discretionary demand. The UN Regulation on Advanced Emergency Braking Systems (AEBS) under UNECE sets harmonized technical requirements for vehicle-to-vehicle and vehicle-to-pedestrian AEB, with studies showing a 38% reduction in real-world low-speed rear-end crashes where AEB is deployed.

The EU’s General Safety Regulation and UN R152 make AEBS compulsory for new vehicle types, while Euro NCAP has tightly linked five-star ratings to AEB performance. In the US, NHTSA’s final rule will require AEB to operate up to 90 mph with robust pedestrian detection in darkness, with full compliance expected by 2029, thereby forcing widespread adoption across light vehicles. These measures transform AEB from a differentiating option into a baseline compliance requirement, supporting sustained volume growth.

Technological advances in sensor fusion, LiDAR, and AI processing

Rapid innovation in sensor technologies and perception algorithms is materially improving AEB performance while lowering cost per function. Multi-sensor fusion platforms that combine radar, cameras, and LiDAR are enabling more precise obstacle detection, better classification, and faster response, especially under adverse weather and low-light conditions. Next-generation systems from leading suppliers integrate AI-powered pedestrian and cyclist detection, adaptive braking logic, and predictive trajectory analysis, enhancing effectiveness in dense urban environments and complex traffic.

At the architectural level, high-performance perception processors and consolidated ECUs enable real-time data fusion and decision-making, while software-defined platforms enable over-the-air upgrades and feature scaling. These advances increase OEM willingness to standardize AEB across trims and vehicle classes, supporting higher content per vehicle and richer monetization opportunities

Restraint - Cost, regulatory complexity and liability concerns constrain AEB market scalability

High system costs and integration complexity remain major restraints in the Autonomous Emergency Braking (AEB) market. Advanced AEB systems that incorporate multi-camera setups, radar, and LiDAR significantly increase bill-of-materials and integration expenses, particularly for mass-market vehicles and price-sensitive emerging economies. Commercial-vehicle solutions such as ZF’s OnGuardMAX and heavy-duty braking technologies from Bosch rely on high-performance sensors and processing units, raising component costs and calibration requirements. As a result, OEMs targeting lower-vehicle-segment must carefully balance safety performance with affordability. This often delays the adoption of premium LiDAR-based systems and restricts advanced AEB features to mid- and high-end trims.

At the same time, stringent regulatory standards add compliance challenges. UNECE and EU regulations mandate rigorous testing across a range of speeds and driving scenarios, while the upcoming US FMVSS 127 is expected to introduce even tougher benchmarks. Achieving reliable pedestrian and cyclist detection in low-light conditions demands extensive validation, software optimization, and engineering investment. Any performance gap may increase liability risks, prompting cautious deployment strategies.

Opportunity - Heavy Commercial Expansion and Software-Driven Evolution in AEB

Heavy trucks and buses are becoming a major growth frontier for Autonomous Emergency Braking (AEB) as regulators and fleet operators focus on reducing severe rear-end and tail-end collisions. Advanced systems such as ZF’s OnGuardMAX and Bosch’s emergency braking solutions for heavy vehicles can detect stationary and moving vehicles, motorcycles, bicycles, and pedestrians, bringing trucks to a full stop even at highway speeds. With stricter AEBS regulations in Europe and proposed mandates in the United States, both factory-installed and retrofit systems could create a multi-billion-dollar opportunity by the early 2030s, offering higher revenue per vehicle than passenger cars.

Simultaneously, the transition toward software-defined vehicles, centralized ECUs, and over-the-air updates is reshaping AEB monetization. Collaborations like ZF-NVIDIA and AI-powered ADAS platforms such as Mobileye’s Surround ADAS enable predictive perception, continuous learning, and scalable deployment. This evolution supports subscription models, tiered performance features, and data-driven safety services built around AEB capabilities.

Category-wise Analysis

Product Type Insights

Low-speed AEB systems account for over 55% of market revenue in 2026, reflecting their critical role in urban driving, stop-and-go traffic, and parking-lot scenarios where low-speed rear-end collisions are most prevalent. This dominance aligns with Euro NCAP and similar programs, which emphasize low-speed crash prevention and have documented substantial reductions in rear-end crashes when low-speed AEB is fitted. OEMs prioritize low-speed AEBS for volume models due to clearer regulatory expectations, lower sensor performance requirements, and significant insurance and safety benefits.

High-speed AEB, while a smaller base today, is the fastest-growing product segment with an expected CAGR of 8.8% between 2026 and 2033, driven by regulations such as the US rule requiring effective braking up to highway speeds and robust pedestrian detection in darkness. High-speed AEBS relies more heavily on advanced radar, long-range camera, and increasingly LiDAR, and is closely tied to highway ADAS features like adaptive cruise control and automated lane change. As sensor costs decline and software-defined platforms proliferate, high-speed AEB adoption will expand rapidly across mid- and high-segment vehicles.

Technology Insights

Forward Collision Warning (FCW) remains the leading technology, contributing more than 35% of revenue in 2026, as it represents the foundational layer of most AEB architectures and has been in production the longest. FCW systems leverage camera and radar to detect relative speed and distance, warning drivers of imminent collisions and often pre-charging brakes to shorten stopping distances. Its comparatively lower cost and compatibility with existing braking systems make FCW the default step for many OEMs and markets as they move up the safety technology curve.

Crash Imminent Braking (CIB) is projected to be the fastest-growing technology segment, with a CAGR of about 9.1% over 2026-2033, as regulations and NCAP protocols increasingly reward automatic braking intervention rather than warnings alone. CIB requires more sophisticated perception and decision logic to autonomously initiate full or partial braking when driver response is inadequate, often integrating AI-based object classification and trajectory prediction. As OEMs seek to maximize safety ratings and differentiate on real-world crash-avoidance performance, CIB-centric solutions will gain share, while dynamic brake support and other assist functions will continue as complementary layers.

Vehicle Type Insights

Passenger vehicles account for over 65% of AEB revenue in 2026, driven by high light-vehicle production volumes, strong consumer safety awareness, and the central role of AEB in securing top safety ratings in Europe, North America, and parts of Asia. Regulatory mandates for AEB in passenger cars in regions such as the EU and Japan, along with voluntary commitments by OEMs in the US, anchor this dominance and ensure continued penetration growth into lower-priced segments.

Commercial vehicles-trucks and buses-represent a smaller but fastest-growing segment, with an expected CAGR of around 9.1% over 2026-2033, supported by high accident severity, fleet safety goals, and tightening regulations for heavy vehicles. Solutions like ZF’s OnGuardMAX and Bosch’s advanced emergency braking for heavy commercial vehicles, which autonomously stop vehicles from significant speeds and detect vulnerable road users, showcase the value proposition for logistics operators and public transport agencies. As total cost of ownership calculations increasingly factor in accident reduction and downtime avoidance, AEB fitment in commercial fleets will accelerate.

Brake Type Insights

Disc brake-equipped vehicles command over 65% of AEB-related revenues in 2026, reflecting the dominance of disc braking systems in passenger cars and many light commercial vehicles. Disc systems offer superior heat dissipation, more consistent performance under repeated braking, and precise controllability, which align well with the rapid, modulated braking interventions required by AEB algorithms. As regulators and NCAP continue to tighten stopping-distance and stability criteria under AEB activation, disc-based platforms maintain their preferred status for most new vehicle designs in both mature and many emerging markets.

Drum brakes, while structurally more prevalent in lower-cost and certain heavy-duty applications, represent the faster-growing brake type segment, with an expected CAGR of about 8.9%, as suppliers and OEMs adapt AEB solutions to cost-sensitive markets and specific axle configurations. Engineering efforts focus on ensuring that AEB actuation delivers predictable, stable braking on drum-equipped axles, particularly in rear axles of small cars and in selected commercial vehicles. This creates incremental opportunities for tailored actuation, control algorithms, and system integration for drum-dominant platforms.

System Composition Insights

Camera-Centric Architectures Dominate as Lidar Investment Accelerates Sensor Fusion Roadmap

Camera-centric architectures hold over 35% revenue share in 2026, reflecting their central role in recognizing vehicle and pedestrian attributes, traffic signs, and lane markings at comparatively low hardware cost. Forward-looking high-resolution cameras, often coupled with radar, already meet many regulatory and NCAP requirements, and are widely deployed across mainstream passenger cars and light commercial vehicles. Improvements in image sensors and computer vision algorithms continue to enhance performance in challenging lighting and weather conditions, supporting their dominance.

LiDAR, however, is the fastest-growing system component with an estimated CAGR of 9.5% from 2026 to 2033, thanks to its superior range, depth resolution, and ability to accurately localize both moving and stationary objects. As prices decline and solid-state LiDAR solutions mature, OEMs and Tier-1s are integrating LiDAR into premium AEB and ADAS packages, particularly for high-speed and urban intersection scenarios. In parallel, investments in high-performance perception processors and centralized ECUs are enabling advanced sensor fusion, real-time decision-making, and functional consolidation, amplifying the strategic importance of LiDAR-enabled architectures

Regional Insights

Manufacturing scale and safety mandates drive Asia-Pacific AEB demand expansion

Asia Pacific holds over 40% of global AEB revenues in 2026, reflecting its role as the world’s largest vehicle manufacturing hub and rapid adoption of safety technologies in China, Japan, South Korea, India, and ASEAN. Japan has already mandated automatic braking for new and remodeled passenger cars, with existing models required to be equipped by 2025, demonstrating a strong regulatory commitment. China and other markets are tightening safety norms and NCAP-like rating regimes, which increasingly include AEB performance in their scoring frameworks.

Growth prospects are particularly strong in mid-segment passenger cars and light commercial vehicles as domestic automakers move to align with export-market standards and global OEMs scale localized ADAS platforms. Regional suppliers and global Tier-1s are investing heavily in localized development, sensor manufacturing, and system integration to balance cost and performance, often tailoring AEB for congested urban environments and mixed-traffic conditions. Asia Pacific’s combination of volume scale, rising safety expectations, and manufacturing cost advantages positions it as the critical battleground for both price-competitive and high-end AEB solutions over the forecast horizon.

Regulation-led adoption and ADAS innovation underpin North American AEB momentum

North America is one of the largest AEB markets globally and, within this study, is projected to be the fastest-growing region, with a CAGR of about 8.9% between 2026 and 2033, supported by strong US leadership in regulation and innovation. NHTSA’s final rule mandating AEB with pedestrian detection, effective at speeds up to 90 mph and in darkness, by 2029 for new light vehicles, will materially lift penetration. Voluntary commitments by major OEMs in the US and Canada to equip nearly all new light vehicles with AEB further reinforce this trajectory.

The region benefits from a deep ADAS innovation ecosystem, including technology suppliers such as Mobileye, NVIDIA, and leading Tier-1s collaborating with US and Canadian OEMs on software-defined ADAS platforms that embed advanced AEB functions. Competitive dynamics are moderately consolidated around global Tier-1s with strong local engineering presence, while investment trends focus on AI-driven perception, highway automation, and cloud-connected ADAS features. As regulatory clarity extends to heavy-duty vehicles and insurance incentives strengthen, North America will remain a priority market for high-performance AEB deployments and premium safety packages.

Competitive Landscape

The Autonomous Emergency Braking (AEB) market is moderately consolidated, dominated by leading Tier-1 suppliers delivering integrated braking systems, sensors, perception software, ECUs, and full ADAS platforms to global OEMs. These companies provide end-to-end architectures combining precise object detection, rapid sensor fusion, real-time data processing, and controlled braking performance-core elements of modern AEB systems. Key players such as Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Denso Corporation, Autoliv Inc., Valeo SA, and Mobileye hold a substantial share of global revenues, especially in passenger and premium vehicle segments. Their leadership stems from strong R&D, scalable electronic platforms, and advanced sensor technologies enabling sub-150 millisecond response times. Meanwhile, Asia Pacific manufacturers and specialized LiDAR and AI chip developers are intensifying competition through cost-effective modules and enhanced detection capabilities.

Key Industry Developments:

- On May 13, 2024, Plus launched PlusProtect™, an AI-based software designed to enhance next-generation vehicle safety systems with high-performance automatic collision mitigation. According to National Highway Traffic Safety Administration, nearly 60,000 annual rear-end crashes involve heavy vehicles striking others.

- In October 2024, Lynred introduced an ultra-compact 8.5µm thermal imaging sensor designed for next-generation AEB systems, enhancing night-time and low-visibility pedestrian detection while enabling smaller, high-performance automotive integration.

- In July 2024, NIO Inc. released Banyan 2.6.5 CN for NT 2.0 vehicles, introducing AI-enhanced AEB with improved object recognition and braking accuracy for vehicles, cyclists, and pedestrians.

- In April 2024, the National Highway Traffic Safety Administration finalized a rule mandating automatic emergency braking, including pedestrian detection, in all new U.S. passenger cars and light trucks by September 2029.

- In May 2023, Tesla, Inc. updated its Automatic Emergency Braking (AEB) system via a software release that enables the system to operate while the vehicle is in reverse, in addition to forward driving.

Companies Covered in Autonomous Emergency Braking (AEB) Market

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Delphi Automotive LLP

- Hyundai Mobis

- Aisin Seiki Co. Ltd

- Hitachi Automotive System Ltd.

- Mando Corporation

- Netradyne

- Valeo S.A.

- Other Market Players

Frequently Asked Questions

The Autonomous Emergency Braking (AEB) market is estimated to be valued at US$ 73.9 Bn in 2026.

The key demand driver for the Autonomous Emergency Braking (AEB) market is stringent government safety regulations mandating advanced driver assistance systems (ADAS) in new vehicles.

In 2026, the Asia Pacific region will dominate the market with an exceeding 40% revenue share in the global Autonomous Emergency Braking (AEB) market.

Among technologies, forward collision warning has the highest preference, capturing beyond 35% of the market revenue share in 2026, surpassing other technologies.

Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Delphi Automotive LLP Hyundai Mobis, and Aisin Seiki Co. Ltd a few leading players in the Autonomous Emergency Braking (AEB) market.