- Industrial Goods & Service

- Autonomous Off-road Vehicle and Machinery Market

Autonomous Off-road Vehicle and Machinery Market Size, Share, and Growth Forecast, 2026 - 2033

Autonomous Off-road Vehicle and Machinery Market by Equipment Type (Tractors, Harvesters, Haul Trucks, Excavators, Loaders and Dozers, Drills and Drill Rigs, Compactors, Shuttles, Forklifts and Cranes), By End User (Construction, Mining and Quarrying, Defense and Military, Agriculture, Airport Handling and Logistics and Transportation) and Regional Analysis for 2026 - 2033

Autonomous Off-road Vehicle and Machinery Market Size and Trends Analysis

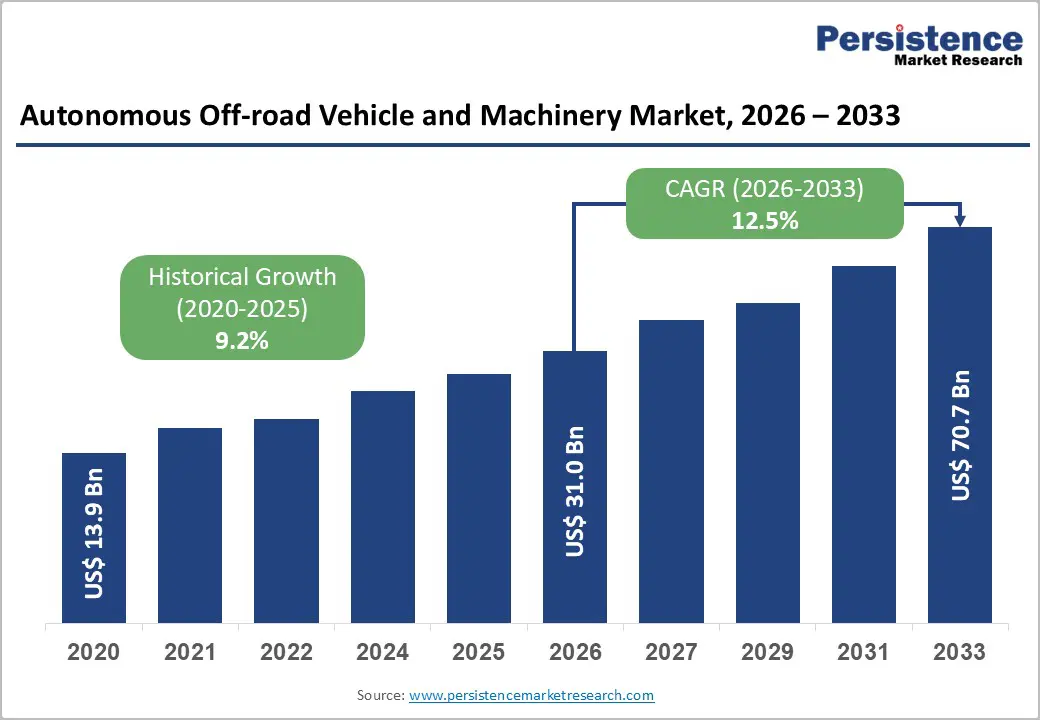

The global autonomous off-road vehicle and machinery market size is likely to be valued at US$ 31.0 billion in 2026 and is projected to reach US$ 70.7 billion by 2033, growing at a CAGR of 12.5% between 2026 and 2033.

The market is driven by the replacement of human-operated equipment with autonomous systems, addressing critical workforce gaps, improved safety outcomes, reducing occupational hazards, and enhanced operational efficiency, enabling 24/7 productivity.

Key Industry Highlights:

- Leading Equipment Type: Loaders and dozers dominate with 27.3% market share through broad construction and mining applicability; Compactors represent fastest growing at 16% CAGR, driven by infrastructure project expansion and precision compaction requirement.

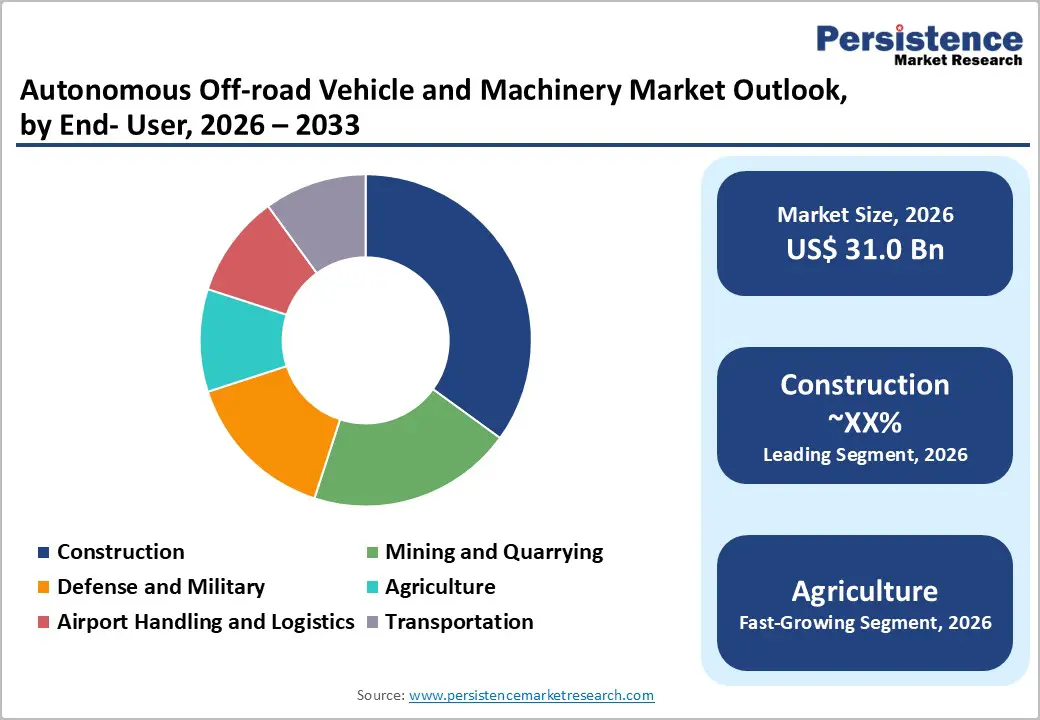

- Dominant End-Use Application: Mining and quarrying maintain 35% market share through hazardous operation automation priority; Agriculture represents fastest growing at 15% CAGR, driven by labor shortage severity and farm consolidation acceleration.

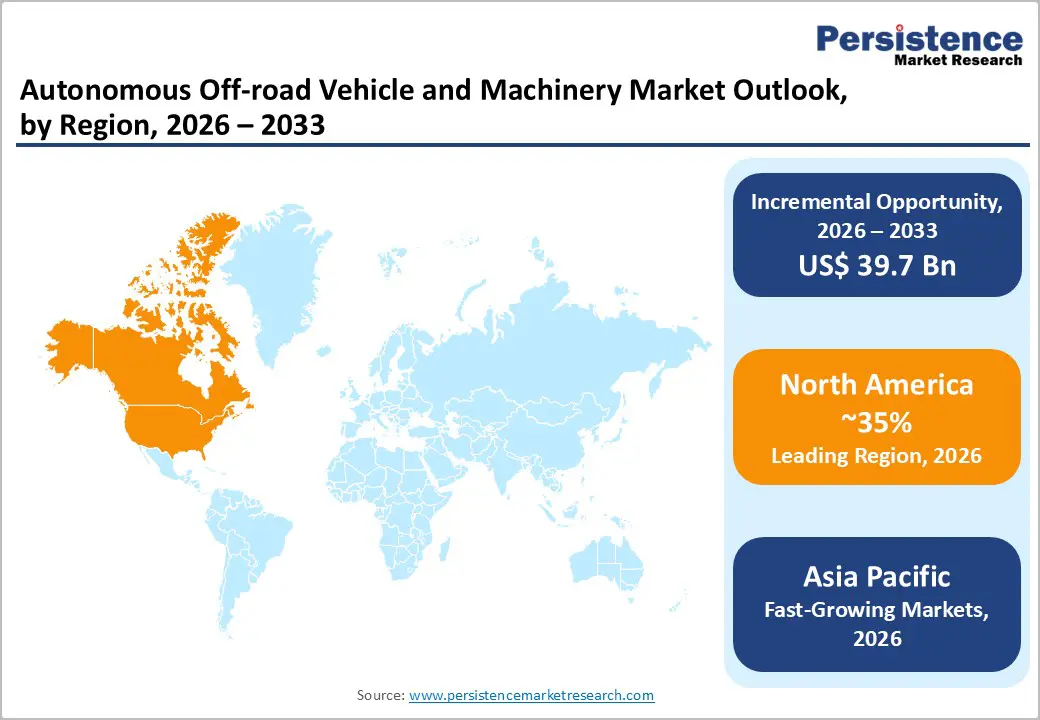

- Regional Market Dominance and Growth: North America maintains 35% global market share driven by technology innovation and labor shortage pressure; Asia-Pacific demonstrates fastest regional growth at 14% CAGR, expanding from 30% current share to 45% by 2033.

- Technology and Market Innovation Momentum: Top 10 suppliers control 58% market share (Caterpillar, Komatsu, Volvo, John Deere leading); Autonomous haul truck deployment at 75+ mining sites globally; 5th-generation autonomous systems incorporating advanced AI and predictive maintenance; 24/7 operational capability enabling continuous productivity.

- Operational Efficiency and Safety Gains: Mining efficiency improvement of 35% through autonomous deployment; 24/7 continuous operation enabling uninterrupted production; Fuel reduction of 12% per ton of output through optimized autonomous operations; Fatality elimination of 80-90% in autonomous operations; 4.1+ million kilometers of proven autonomous operational data accumulated globally.

| Key Insights | Details |

|---|---|

| Autonomous Off-road Vehicle and Machinery Market Size (2026E) | US$ 31.0 Bn |

| Market Value Forecast (2033F) | US$ 70.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 12.5% |

| Historical Market Growth (CAGR 2020 to 2024) | 9.2% |

Market Dynamics

Drivers - Critical Labor Shortages and Aging Workforce Pressures

Global workforce composition shifts, with construction, mining, and agricultural sectors experiencing 30% labor shortages in developed economies and 15% in emerging markets, create proportionate autonomous equipment demand. Aging rural workforce phenomenon, with agricultural workers aging 8-12 years faster than general population and young workforce participation declining 20% annually, establishes systematic equipment demand. Construction industry labor constraints, with skilled operator availability declining 15% annually and wage escalation exceeding 8-12% year-over-year, justify autonomous equipment investment.

Occupational hazard avoidance motivation, with hazardous duty positions attracting limited workforce participation and autonomous equipment eliminating operator exposure to dangerous conditions, drive adoption incentive. Immigration policy restrictions, with developed countries implementing immigration constraints affecting construction and agricultural labor availability, establish autonomous equipment deployment necessity.

Revolutionary Advances in Sensor Technology, AI, and Autonomous Driving Systems

Autonomous driving technology maturation, with operational autonomous fleets now exceeding 600 heavy-duty vehicles deployed at 25 commercial mine sites globally and accumulating 4.1 million kilometers of operational data, providing proof of technology reliability. Sensor technological advancement, with LiDAR, radar, GPS, and machine vision achieving 99.2% precision in real-world operational environments versus 85% five years prior, enables safe autonomous operation. Machine learning capability expansion, with AI-enabled predictive maintenance reducing equipment downtime by 25% and autonomous scheduling optimizing operational efficiency by 20%, justifying premium equipment investment.

Real-time processing improvements, with edge computing and onboard processing reducing decision latency to <100ms enabling immediate hazard response, establish safety confidence. Cooperative operation frameworks, with vehicle-to-vehicle and vehicle-to-infrastructure communication enabling coordinated fleet operations and collision avoidance, reduce incident rates by 40-50% and support deployment expansion.

Restraints - High Capital Investment Barriers and Infrastructure Requirements

Autonomous equipment acquisition costs, with autonomous tractors, loaders, and haul trucks commanding 25% price premiums versus conventional equipment, restrict adoption to well-capitalized operators. Infrastructure modification requirements, with autonomous equipment requiring GPS networks, communication infrastructure, and control centers representing 15-25% additional capital investment, increase total deployment cost. Workforce transition challenges, with current operators requiring retraining or displacement creating political and social barriers affecting adoption decisions. Interoperability complexity, with non-standardized autonomous systems across manufacturers, limits fleet flexibility and requires vendor-specific support infrastructure investment. Financing accessibility constraints: limited agricultural and construction equipment financing programs for autonomous equipment in emerging markets, constraining adoption.

Regulatory Uncertainty and Liability Framework Gaps

Autonomous equipment liability framework gaps, with undefined insurance and accident responsibility creating legal uncertainty affecting manufacturer and operator adoption decisions. Regulatory compliance complexity, with varying international safety standards and autonomous vehicle regulations creating certification burden requiring region-specific equipment modifications. Cybersecurity vulnerabilities in autonomous equipment create potential attack vectors and data security risks, requiring comprehensive mitigation strategies. Data privacy regulations, including GDPR and CCPA, and emerging regulations restricting operational data collection and sharing, limiting system optimization capabilities. Standardization delays, with autonomous equipment industry standards development proceeding slowl, arey affecting procurement consistency and interoperability. Safety certification requirement burden, with independent testing and validation protocols requiring 12-24 months and significant expense limiting market entry velocity.

Opportunity - Developing Economy Infrastructure and Construction Expansion

Infrastructure investment acceleration, with India, Southeast Asia, and South America allocating US$ 300-500 billion annually for infrastructure development through 2033, establishes substantial equipment deployment opportunities. Construction equipment demand surges, with developing economy urbanization driving 20-30% annual construction equipment demand growth, creating a systematic market opportunity. Manufacturing localization advantages, with emerging market equipment manufacturers achieving 25-35% cost advantages enabling market penetration at accessible price points. Government infrastructure mandate alignment, with national infrastructure development plans mandating advanced equipment deployment for efficiency and safety, establish purchasing drivers.

Mining Automation and Hazardous Environment Expansion

Mining automation maturation, with proven autonomous systems deploying at 30+ mine sites globally and achieving 10% efficiency improvements and 12% fuel reduction, establishing technology confidence. Hard-to-reach mining site expansion, with remote mining operations in Arctic regions, deep-sea mining, and extreme altitude locations enabling autonomous deployment eliminating human hazard exposure, create specialized deployment opportunity. Commodity price volatility management, with autonomous equipment reducing marginal mining costs by 20-30% enabling profitable operation at lower commodity prices, support equipment adoption. Environmental remediation automation, with autonomous equipment enabling mining site reclamation and environmental restoration without human presence, support sustainability alignment.

Category-wise Analysis

Equipment Type Insights

The loaders and dozers segment holds 27.3% market share, driven by broad applicability across construction, mining, and material handling operations. These machines perform core tasks such as grading, earthmoving, and material placement, creating consistent demand across project types. Loaders and dozers also represent the most mature autonomous deployments, with proven operating histories exceeding 10,000 hours, reinforcing reliability and user confidence. Favorable labor-replacement economics and strong cost-benefit performance further support widespread adoption, while large-scale mining operations rely heavily on autonomous loaders and dozers for continuous ore and waste handling.

The compactor segment is the fastest growing, projected to expand at 16-21% CAGR through 2033. Growth is driven by large infrastructure projects requiring consistent soil and aggregate compaction. Autonomous compactors improve density accuracy by 15-20%, reduce rework and delays by 20%, and enhance safety by removing operators from dusty, noisy environments.

Application Insights

The mining and quarrying sector holds 35% market share, driven by the need to automate hazardous operations. Autonomous equipment deployment is well established across 30+ mining sites globally, delivering productivity improvements of around 35% and validating operational reliability. Safety remains the primary adoption driver, as removing personnel from high-risk environments accelerates automation faster than in other industries. Continuous 24/7 operations further favor autonomous machinery, while cost pressures from volatile commodity prices make automation attractive by reducing marginal mining costs 20%.

The agriculture segment is the fastest growing, projected to expand at 15% CAGR through 2033. Growth is driven by severe labor shortages, rapid farm consolidation, and adoption of precision agriculture. Autonomous machinery enables yield improvements of 15-25%, supports sustainability compliance, and benefits from strong government investment in smart farming, accelerating adoption across large-scale agricultural operations.

Regional Insights

North America Autonomous Off-road Vehicle and Machinery Market Insights

Market Scale and Performance: North America commands approximately 35% of global Autonomous Off-road Vehicle and Machinery market share, valued at approximately US$ 9.68 billion in 2026 with projections approaching US$ 19.0 billion by 2033. The United States represents dominant regional market contributor, accounting for 80% of North American market value, driven by advanced technology deployment and labor shortage pressure.

Labor shortage severity, with construction workforce declining 8% annually and agricultural workforce aging 12-15 years faster than general population, establish proportionate autonomous equipment demand. Technology innovation leadership, with North American companies leading autonomous vehicle development and AI technology advancement, support rapid market scaling. Infrastructure investment expansion, with US federal government allocating US$ 150-200 billion annually for infrastructure modernization, establish systematic equipment deployment foundation. Mining sector automation priority, with North American mining companies operating globally and prioritizing hazardous environment automation, support equipment adoption.

Europe Autonomous Off-road Vehicle and Machinery Market Insights

Europe represents approximately 22% of global Autonomous Off-road Vehicle and Machinery market share, valued at approximately US$ 6.82 billion in 2026. Germany, United Kingdom, France, and Spain collectively represent 70% of European market value, reflecting advanced automation tradition and regulatory support.

Labor shortage pressure, with European workforce participation declining 15% and regulatory support favoring technology adoption, establish systematic equipment demand. Environmental regulation mandate compliance, with EU emission standards and circular economy directives mandating advanced equipment deployment for efficiency and emissions reduction, establishing purchasing requirement. Construction sector growth, with European infrastructure modernization and urban development driving 8% annual equipment demand growth, create market opportunity.

Asia Pacific Autonomous Off-road Vehicle and Machinery Market Analysis

Asia Pacific demonstrates robust growth dynamics, commanding approximately 30% market share with projections increasing to 40% by 2033. The region, valued at approximately US$ 11.78 billion in 2026 is anticipated to reach US$ 32.0 billion by 2033, representing fastest-growing regional market with estimated CAGR of 14%.

Infrastructure investment acceleration, with China, India, and Southeast Asia allocating US$ 500-800 billion annually for infrastructure development through 2033, establishes a substantial equipment deployment opportunity. Manufacturing capability dominance, with Chinese, South Korean, and Japanese equipment manufacturers leading autonomous technology development and producing 60-70% of global off-road equipment, establish competitive advantage. Labor shortage pressure, with developing economy workforce participation shifting from agricultural to service sectors, and construction labor becoming scarce, establishes proportionate equipment demand.

Competitive Landscape

The global autonomous off-road vehicle and machinery market demonstrates moderate consolidation with established heavy equipment manufacturers and specialized autonomous technology companies maintaining competitive positions. The top 10 suppliers, including Caterpillar, Komatsu, Volvo, John Deere, Hitachi, Case IH, CNH Industrial, XCMG, Liebherr, and Sany, collectively control approximately 58% of global market share, reflecting technology leadership, manufacturing scale, and established customer relationships.

Market structure reflects bifurcation between large multinational equipment conglomerates offering comprehensive autonomous solutions and specialized autonomous technology startups providing retrofit systems and operating software.

Key Industry Developments

- In May 2024, Hitachi Construction Machinery Co., Ltd. developed a “Real-Time Digital Twin Platform,” creating a virtual version of a construction site using real-time data. This platform allowed the monitoring and management of construction activities and the operation of autonomous machinery from a remote location via the Internet.

- In August 2023, New Holland, a subsidiary of CNH Industrial, launched T4 Electric Power, an electric utility tractor with autonomous features. The tractor had a 110-kWh lithium-ion 7/12 battery pack with 74 horsepower. The tractor had a travel range of 8 hours on a single charge and could recharge up to 100% in just 1 hour using fast charging.

Companies Covered in Autonomous Off-road Vehicle and Machinery Market

- Caterpillar Inc.

- Komatsu Ltd.

- Sandvik AB

- John Deere

- Yanmar Co., Ltd.

- Volvo Construction Equipment

- Liebherr Group

- Jungheinrich AG

- Daifuku Co. Ltd

- Toyota Industries Corporation

- Others Key Players

Frequently Asked Questions

The Autonomous Off-road Vehicle and Machinery market is estimated to be valued at US$ 31.0 Bn in 2026.

The key demand driver for the Autonomous Off-road Vehicle and Machinery market is the need to improve productivity, safety, and operating efficiency in labor-intensive and hazardous environments, driven by workforce shortages and cost pressures.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Autonomous Off-road Vehicle and Machinery market.

Among end- use, construction holds the highest preference, capturing beyond 43.2% of the market revenue share in 2026, surpassing other End- use type.

The key players in Autonomous Off-road Vehicle and Machinery are Caterpillar Inc., Komatsu Ltd., Sandvik AB, John Deere and Yanmar Co., Ltd.