- Transportation & Logistics

- Autonomous Cranes Market

Autonomous Cranes Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Autonomous Cranes Market by Crane Type (Static Crane, Mobile Crane), End-user (Building and Construction, Marine and Offshore, Mining and Excavation), Capacity (Up To 50 T, 51 To 150 T, above 150 T), and Regional Analysis for 2026 - 2033

Autonomous Cranes Market Size and Trend Analysis

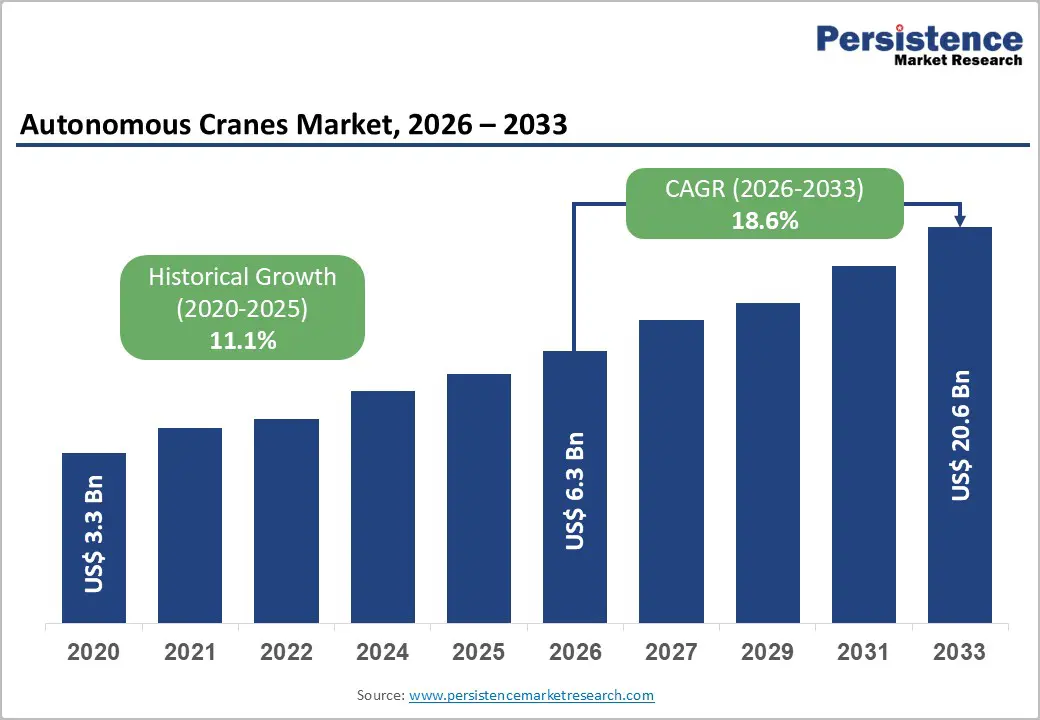

The global autonomous cranes market size is supposed to be valued at US$ 6.3 billion in 2026 and is projected to reach US$ 20.6 billion by 2033, growing at a CAGR of 18.6% between 2026 and 2033.

This exceptional growth trajectory is fundamentally driven by the construction industry's accelerating adoption of artificial intelligence and machine learning technologies to address critical safety concerns.

Key Industry Highlights:

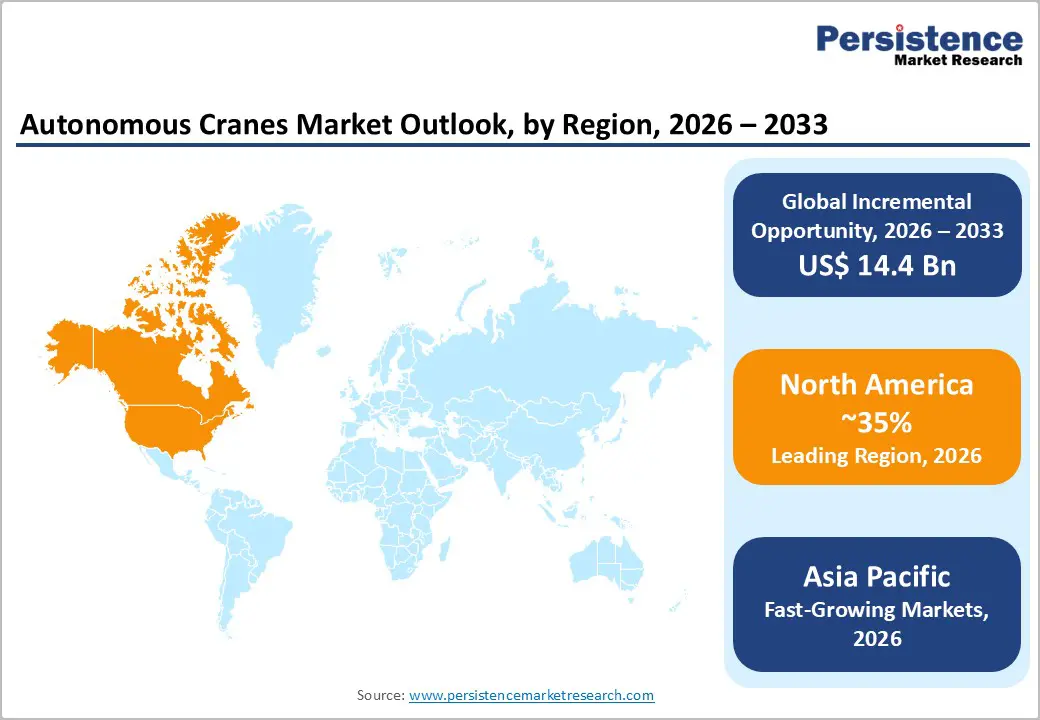

- Dominant Region: North America maintains technology leadership supported by construction workforce requiring 439,000 new workers in 2025 creating urgent automation needs, Bureau of Labor Statistics documenting 42 annual crane-related deaths driving safety technology adoption, advanced 5G connectivity infrastructure enabling real-time operations, and substantial capital investment capacity among large construction firms and port operators.

- Fastest Growing Region: Asia Pacific emerges as fastest-growing regional market driven by massive infrastructure development programs, rapid port automation expansion with US$ 2.15 billion terminal investments delivering 70% labor cost reduction and 50% efficiency improvements, aggressive mining modernization achieving 35% increased daily shifts and 12% fuel savings.

- Dominant Segment: Mobile cranes dominate with approximately 62% market share driven by operational flexibility enabling multi-site deployment, Liebherr LTM 1150-5.4E demonstrating 150-ton capacity with emission-free four-to-five-hour battery operation, and versatility addressing construction, infrastructure, and industrial applications without permanent installation requirements.

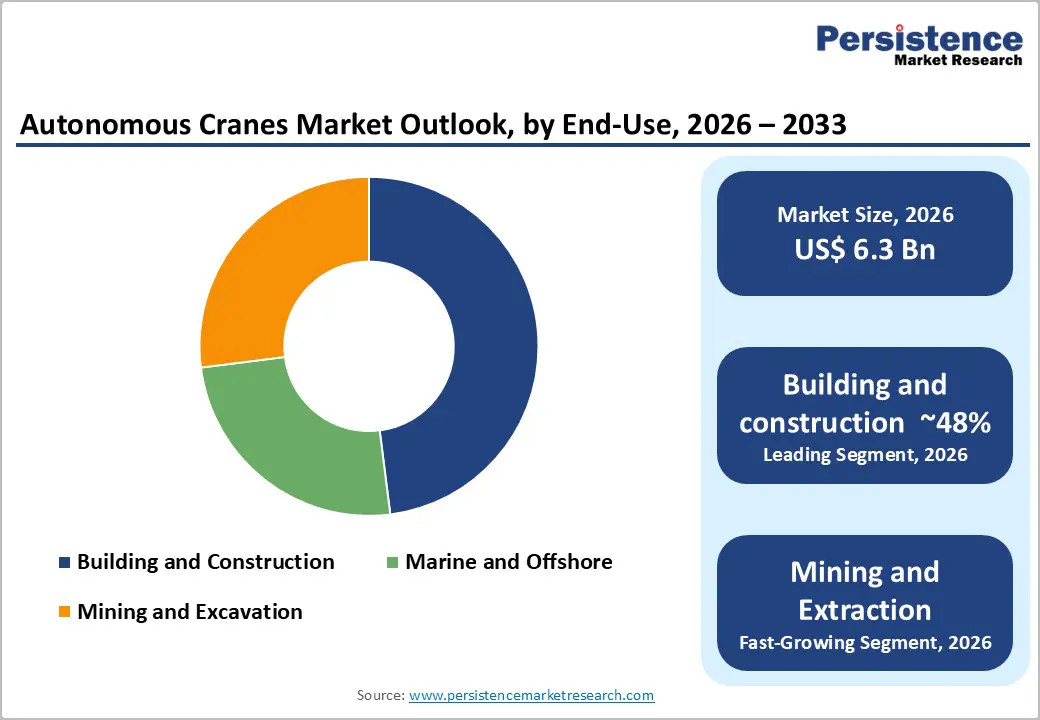

- Fastest Growing Segment: Building and construction leads end-user segments with approximately 48% share, propelled by 43% of crane fatalities occurring in private construction industry, workforce shortage requiring 439,000 workers annually, autonomous systems delivering 90% accident reduction and 24/7 operation capacity, and 37% of businesses adopting AI technology integration with Building Information Modeling platforms.

- Opportunity: Digital construction ecosystem integration presents transformative opportunity as 37% of construction businesses adopt artificial intelligence and nearly half deploy Building Information Modeling on 76% to 100% of projects, enabling autonomous crane coordination with digital twin systems, augmented reality lift planning, and comprehensive project lifecycle optimization through real-time data integration and predictive maintenance capabilities.

| Key Insights | Details |

|---|---|

| Autonomous Cranes Market Size (2026E) | US$ 6.3 Bn |

| Market Value Forecast (2033F) | US$ 20.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 18.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 11.1% |

Market Dynamics

Drivers - Critical Safety Enhancement Requirements and Accident Reduction Imperatives

The construction and heavy lifting industries face persistent safety challenges that are fundamentally driving autonomous crane adoption, with crane-related incidents causing significant worker fatalities and injuries across global operations. According to the Center for Construction Research and Training (CPWR), construction crane incidents resulted in 55 deaths and 99 injuries of construction workers across 88 incidents analyzed, with 39% caused by crane collapses involving 26 deaths and 58 injuries, while 50% of fatalities involved workers being struck by objects or equipment.

The Bureau of Labor Statistics reported 297 deaths involving cranes between 2011 and 2017, establishing an annual average of 42 crane-related deaths, with 43% of fatal work injuries occurring in the private construction industry and 24% in manufacturing. Autonomous crane technology delivers transformative safety improvements through artificial intelligence-powered object detection capabilities that identify workers and obstacles to prevent collisions, real-time sensor data processing enabling immediate operational adjustments, and elimination of human error factors that contribute to accidents.

Severe Labor Shortages and Productivity Enhancement Demands

Global construction and industrial sectors are experiencing acute skilled operator shortages that are accelerating autonomous crane deployment as companies seek technology-driven solutions to maintain operational capacity and productivity levels. The construction industry requires 439,000 new workers in 2025 alone according to Associated Builders and Contractors (ABC), with projections indicating need for 1.9 million workers over the next decade to address both growth demands and retirement attrition.

Autonomous crane systems address these workforce challenges by eliminating dependence on specialized operators while delivering superior performance metrics, with mining operations demonstrating 10% higher efficiency in loading and unloading operations, 33% increased speed limits for empty trucks and 10% for loaded trucks, 35% increase in maximum daily transportation shifts per truck, and 12% fuel consumption savings per ton of minerals produced compared to manual operations.

Restraints - High Capital Investment and Implementation Costs

The deployment of autonomous crane systems requires substantial upfront capital expenditure that creates significant adoption barriers, particularly for small and medium-sized construction firms and operators with limited investment capacity. Autonomous container terminals exemplify implementation costs, with Victorian International Container Terminal in Melbourne requiring AUD 650 million investment for development including five Neo-Panamax ship-to-shore cranes with 65-ton lift capacity and 20 automatic stacking cranes, while automated port facilities have demonstrated development costs reaching US$ 2.15 billion for comprehensive infrastructure transformation. Beyond initial equipment acquisition, companies must undertake multiple infrastructure changes including control center establishment, maintenance facility modifications, communication system upgrades, specialized training programs for technical personnel, and ongoing software licensing and system maintenance expenses.

Technical Complexity and Regulatory Uncertainty

Autonomous crane deployment faces significant technical challenges related to real-time collision avoidance in dynamic environments, sensor integration reliability across diverse weather conditions, and standardization gaps across equipment manufacturers and industrial applications. Crane-lift automation research categorizes implementation into four levels spanning Operator Assistance, Partial Automation, High Automation, and Full Automation, with current technology predominantly achieving partial automation while full autonomy remains relatively rare in typical construction environments. The technology requires multi-sensor integration for real-time collision-free path re-planning, advanced artificial intelligence algorithms processing extensive data from cameras, GPS, and operational logs, and robust communication infrastructure enabling coordinated fleet operations. Additionally, regulatory frameworks governing autonomous industrial equipment operation remain fragmented across jurisdictions, with unclear liability standards, incomplete safety certification processes, and varying approval requirements creating implementation uncertainty.

Opportunities - Marine and Port Automation Expansion

The maritime and offshore sector presents substantial growth opportunities as global ports pursue automation strategies to enhance throughput capacity, reduce operational costs, and improve competitiveness within increasingly demanding shipping logistics networks. Port automation deployments demonstrate compelling business cases, with automated container terminals targeting US$ 80,000 savings in terminal operation costs per vessel through 70% labor cost reduction and 50% handling efficiency increase, while achieving 10% carbon emissions decrease and 24/7 operational capability independent of human shift constraints.

ABB reports that artificial intelligence deployment in container terminal operations increases automation levels for autonomous crane operations while assisting operators with workload management through improved graphical guidance interfaces and enhanced safety via better risk detection and responsive warning systems. The uniformity of container dimensions and repetitive handling processes create natural fit for automation, with yard operations achieving high automation levels through minimal manual intervention and remote supervision, while AI technology integration in yard crane interactions with external chassis further reduces manual interventions.

Integration with Digital Construction Ecosystems and Building Information Modeling

The construction industry's accelerating digital transformation creates significant opportunities for autonomous crane integration with Building Information Modeling platforms, digital twin systems, and comprehensive project management software, enabling optimization across entire project lifecycles. Research indicates 37% of construction businesses now utilize artificial intelligence and machine learning technology in 2025, up from 26% in previous surveys, while nearly half of survey respondents report Building Information Modeling deployment on between 76% and 100% of their projects, with 23% incorporating BIM processes across all projects. Digital construction technologies, including BIM, AI, data analytics, and cloud management software are transforming industry operations, with BIM expanding from design and build phases into downstream project lifecycle stages, including handover, operations, and maintenance, and eventually decommissioning and reuse.

Category-wise Analysis

Crane Type Insights

Mobile cranes command approximately 62% market share within the crane type category, establishing segment dominance through operational flexibility enabling deployment across diverse project sites without permanent installation infrastructure requirements. Mobile autonomous cranes deliver critical versatility for construction projects requiring frequent repositioning, temporary lifting operations, and multi-site service capabilities that static installations cannot economically provide. Liebherr introduced the LTM 1150-5.4E hybrid mobile construction crane combining diesel and electric drive systems, enabling emission-free operation with powerful battery packs providing four to five hours of unplugged operation, 150-ton lifting capacity across five-axle configuration, and operator flexibility switching between drive types based on site requirements and environmental regulations.

End-user Insights

Building and construction applications dominate with approximately 48% share, driven by the sector's massive project volumes, acute safety improvement requirements, labor shortage pressures, and substantial economic benefits from operational efficiency enhancements through autonomous technology adoption. Construction crane incidents cause significant fatalities and injuries, with 43% of fatal work injuries involving cranes occurring in the private construction industry according to Bureau of Labor Statistics data, creating strong regulatory and liability pressure for safety technology investments. The construction workforce shortage requiring 439,000 new workers in 2025 according to Associated Builders and Contractors and projections of 1.9 million workers needed over the next decade intensify automation adoption as companies seek technological solutions maintaining operational capacity despite skilled operator scarcity.

Capacity Insights

The 51-to-150-ton capacity segment commands approximately 44% market share, reflecting optimal balance between lifting capability sufficient for majority of construction, marine, and industrial applications while maintaining equipment mobility, site accessibility, and operational cost efficiency compared to heavier capacity alternatives. This capacity range addresses core requirements across building construction projects involving structural steel placement, precast concrete installation, and mechanical equipment positioning, while serving container terminal operations, offshore platform maintenance, and mid-scale mining equipment handling applications. Liebherr's LTM 1150-5.4E five-axle mobile construction crane exemplifies this segment with 150-ton lifting capacity, demonstrating that electric mobility and autonomous capabilities function effectively in heavy-duty applications beyond smaller specialized equipment.

Regional Insights

North America Autonomous Cranes Market Trends

North America demonstrates strong market fundamentals driven by advanced technology adoption culture, stringent workplace safety regulations, and significant construction industry investment in productivity-enhancing automation solutions addressing persistent labor shortage challenges. The United States leads regional demand supported by construction workforce requirements of 439,000 new workers in 2025 according to Associated Builders and Contractors, with 78% of construction companies reporting critical staff shortages creating urgent need for autonomous equipment alternatives maintaining operational capacity.

Innovation leadership characterizes the North American market, with major ports pursuing automation strategies enhancing competitiveness within global shipping networks, while construction firms integrate autonomous equipment with Building Information Modeling platforms achieving operational optimization. The region benefits from established technology infrastructure including 5G connectivity enabling real-time data transmission, cloud computing platforms supporting artificial intelligence processing, and skilled technical workforce facilitating complex system implementation and maintenance.

Europe Autonomous Cranes Market Trends

Europe exhibits robust market growth driven by stringent environmental regulations promoting electrification and emission reduction, comprehensive workplace safety frameworks incentivizing automation adoption, and advanced manufacturing capabilities supporting technology development and deployment. Germany leads regional adoption supported by strong industrial base, engineering expertise in crane manufacturing with companies including Liebherr headquartered in the country, and construction industry commitment to digital transformation and automation technologies.

Liebherr showcased European innovation leadership presenting the Liebherr Autonomous Operations system at Bauma 2025, featuring advanced development solutions enabling completely driverless operation suited for monotonous activities and hazardous area operations, while the LTM 1150-5.4E hybrid mobile crane demonstrates emission-free capabilities with 150-ton capacity and four to five hour battery operation addressing environmental regulations in Netherlands and Scandinavia requiring emission-free construction machinery.

Asia Pacific Autonomous Cranes Market Trends

Asia Pacific represents the fastest-growing regional market driven by massive infrastructure development programs, rapid port automation expansion supporting export-oriented economies, and aggressive mining sector modernization initiatives across resource-rich nations. China dominates regional growth through government-supported industrial automation policies, substantial construction activity associated with urbanization programs, and world-leading port throughput volumes creating compelling business cases for container terminal automation. Japan demonstrates advanced technology adoption leveraging robotics expertise, automation cultural acceptance, and aging workforce demographics necessitating productivity-enhancing equipment investments maintaining industrial competitiveness.

Port automation exemplifies Asia Pacific leadership, with automated container terminals demonstrating US$ 2.15 billion development investments delivering 70% labor cost reduction, 50% handling efficiency improvements, and 10% carbon emissions decreases, while achieving 24/7 operational capacity and US$ 80,000 savings in terminal operation costs per vessel. Mining sector automation shows substantial progress, with autonomous operations achieving 10% higher efficiency in loading operations, 35% increase in daily transportation shifts, 12% fuel consumption savings per ton of minerals, and continuous operation eliminating two-hour shift change requirements characteristic of manual operations.

Competitive Landscape

The global autonomous cranes market exhibits moderate consolidation with established crane manufacturers leveraging existing market positions, technical expertise, and customer relationships to lead autonomous technology development and commercial deployment. Leading companies pursue differentiation through proprietary automation software platforms, artificial intelligence algorithm sophistication, sensor integration capabilities, and comprehensive service offerings spanning equipment supply, installation, training, and ongoing technical support.

Research and development investments focus on advancing autonomy levels from operator assistance and partial automation toward high automation and full autonomy capabilities, improving multi-sensor integration for collision-free path planning, and developing digital twin technologies enabling real-time performance monitoring and predictive maintenance.

Key Developments:

- April 2025: Liebherr presented the Liebherr Autonomous Operations system at Bauma 2025, featuring advanced development solutions enabling completely driverless crane operation primarily suited for monotonous standard activities and operations in hazardous areas, while showcasing the hybrid LTM 1150-5.4E mobile construction crane combining diesel and electric drive with 150-ton capacity and four to five hours battery operation for emission-free construction sites.

- 2024: Liebherr focused maritime crane development on decarbonization measures and automation adoption, introducing offshore crane prototypes with LiMain remote maintenance and control systems minimizing on-site operations and carbon emissions, while enhancing the LHM 800 mobile harbour crane with longer boom improving handling efficiency and flexibility, with future product development prioritizing electrification, automation, and climate adaptation capabilities.

Companies Covered in Autonomous Cranes Market

- Liebherr Group

- Konecranes

- Manitowoc

- Zoomlion

- Tadano Ltd.

- XCMG

- Terex Corporation

- SANY Group

- Palfinger AG

- Cargotec

- Komatsu Ltd

- AIDrivers Ltd

- Schneider Electric

- SMIE

- Other Key Players

Frequently Asked Questions

The global Autonomous Cranes Market is projected to reach US$ 20.6 Bn by 2033, growing from US$ 6.3 Bn in 2026 at a compound annual growth rate of 18.6% during the forecast period, driven by safety enhancement requirements, labor shortage pressures, and operational efficiency demands.

Market demand is primarily driven by critical safety improvement requirements with crane incidents causing 42 worker deaths annually according to Bureau of Labor Statistics and autonomous systems delivering 90% accident reduction, combined with severe labor shortages requiring 439,000 new construction workers in 2025 according to Associated Builders and Contractors and autonomous operations achieving 35% increased daily shifts and 12% fuel savings in mining applications.

Mobile cranes command approximately 62% market share, dominating through operational flexibility enabling deployment across diverse project sites without permanent installation infrastructure, with Liebherr LTM 1150-5.4E demonstrating 150-ton capacity with emission-free four-to-five-hour battery operation, and versatility addressing construction, infrastructure, and industrial applications requiring frequent repositioning and multi-site service capabilities.

Asia Pacific constitutes the fastest-growing regional market driven by massive infrastructure development programs, rapid port automation expansion with US$ 2.15 billion terminal investments delivering 70% labor cost reduction and 50% handling improvements, aggressive mining modernization achieving 10% higher loading efficiency and 12% fuel consumption savings.

Leading market participants include Liebherr Group, Konecranes, Manitowoc (United States), SANY Group, Terex Corporation, Tadano Ltd., ABB, and other established crane manufacturers and automation technology providers.