- Hardware & Software IT Services

- Asset Performance Management Market

Asset Performance Management Market Size, Share, and Growth Forecast, 2026 - 2033

Asset Performance Management market by Solution Module (Pedictive Asset Analytics, Condition Monitoring, Asset Reliability Management, Asset Integrity Management, Asset Strategy Management, and Misc.), Organisation Size (Small & Medium Enterprises (SMEs), Large Enterprises), Deployment Mode (Cloud/SaaS and On-Premise ), End Use Industry (Energy & Utilities, Oil & Gas, Manufacturing, Power Generation, Chemicals, Mining & Metals, Pharmaceuticals & Life Sciences, and Misc. ), and Regional Analysis for 2026 - 2033

Asset Performance Management Market Size and Trends Analysis

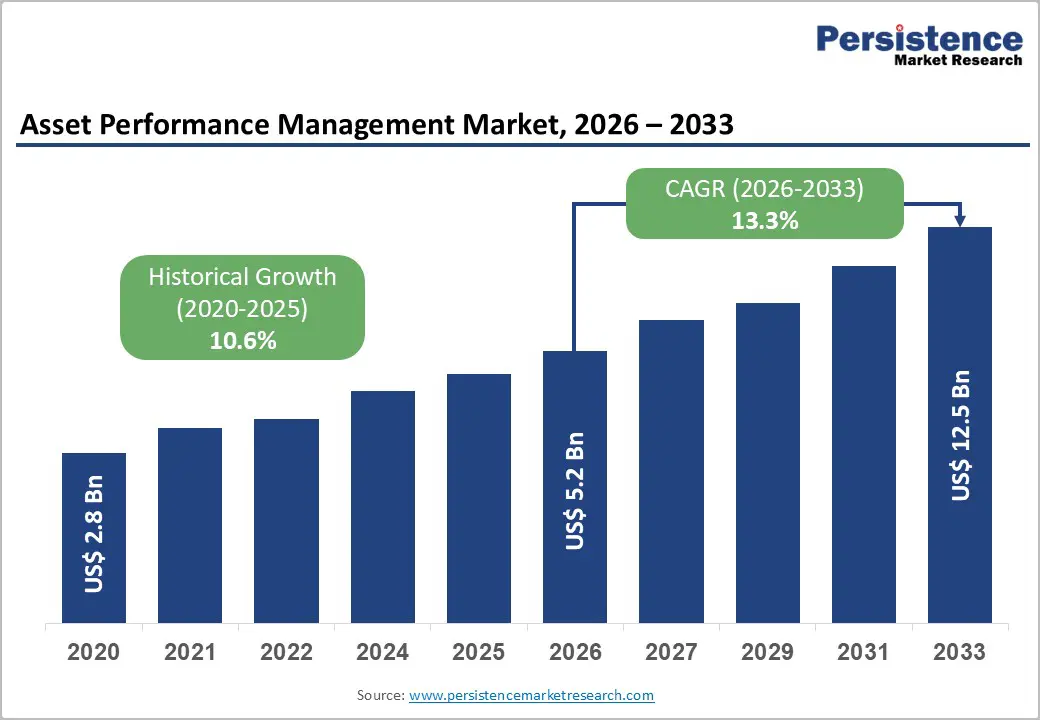

The global asset performance management market size was valued at US$5.2 billion in 2026 and is projected to reach US$12.5 billion by 2033, growing at a CAGR of 13.3% between 2026 and 2033. The historical CAGR from 2020 to 2026 was 10.6%, indicating accelerating growth momentum driven by quantified maintenance-cost reduction achievements, renewable-energy portfolio expansion requiring sophisticated monitoring, and regulatory compliance mandates across energy, utilities, and pharmaceuticals sectors.

Primary growth catalysts include validated predictive-maintenance ROI delivering significant maintenance-cost savings and substantial unplanned-downtime reduction, renewable-energy infrastructure expansion requiring real-time asset monitoring, and pharmaceutical industry compliance automation supporting FDA and EMA regulatory frameworks.

The market is characterised by technological convergence between artificial intelligence analytics, Internet of Things sensor networks, and cloud-based monitoring architectures, enabling autonomous asset-health assessment and predictive failure prevention.

Key Industry Highlights:

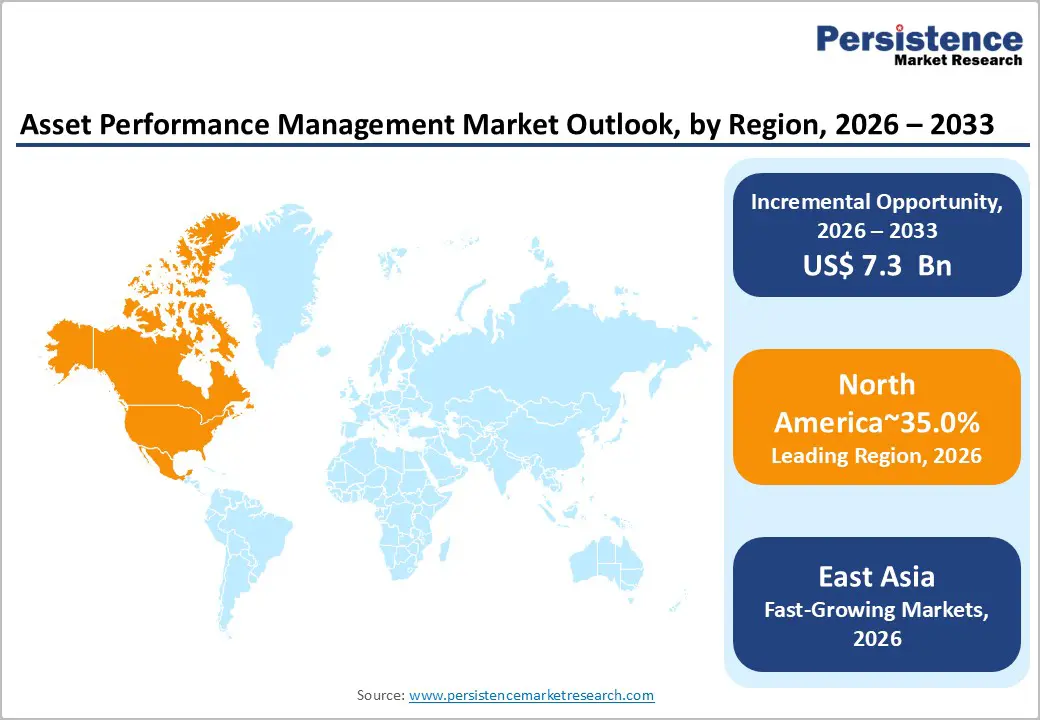

- Regional Leadership: North America dominates the global Asset Performance Management Market with a 35% share in 2026, driven by utility infrastructure modernisation, renewable-energy integration, and significant capital allocation toward predictive and condition-based maintenance.

- Fastest-Growing Region: East Asia captures a 15% share in 2026 and stands as the fastest-growing region, supported by rapid Industry 4.0 adoption, AI-powered predictive maintenance, and government-backed digital transformation initiatives in China and Japan.

- Leading End-Use Segment: Energy & Utilities leads with 20.0% share in 2026, propelled by large fixed-asset portfolios, renewable-energy deployment, and the need for real-time condition monitoring and lifecycle optimisation.

- Fastest-Growing End-Use Segment: Pharmaceuticals & Life Sciences emerges as the fastest-growing segment, driven by regulatory compliance automation, Pharma 4.0 initiatives, and precision asset reliability solutions enhancing production efficiency.

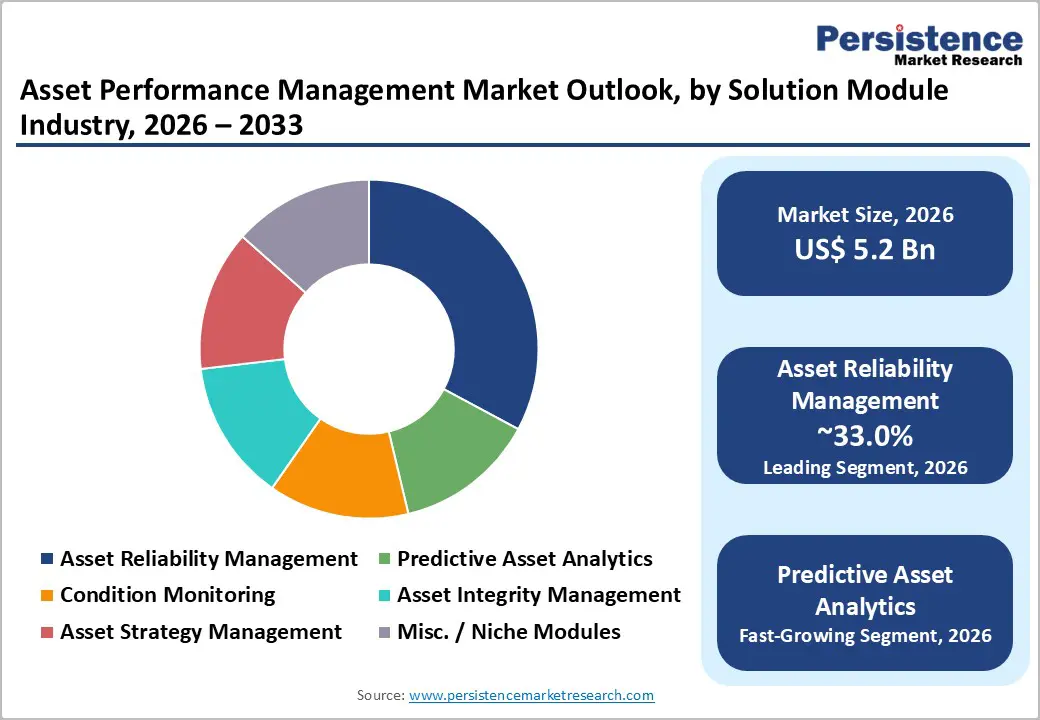

- Leading Solution Module: Asset Reliability Management dominates with a 33.0% share in 2026, reflecting widespread adoption of reliability engineering practices, maintenance strategy optimisation, and root-cause failure analysis.

- Rapidly Growing Solution Module: Predictive Asset Analytics is the fastest-expanding category, fueled by AI-driven failure prediction, digital twins, real-time sensor data, and autonomous maintenance planning.

- Technology & Opportunity: Cloud-based deployment commands 55% share in 2026, enabling scalable, multi-site asset monitoring, centralised fleet visibility, and integration of AI-driven predictive maintenance across manufacturing, energy, and utilities sectors.

| Global Market Attributes | Key Insights |

|---|---|

| Asset Performance Management Market Size (2026E) | US$ 5.2 Bn |

| Market Value Forecast (2033F) | US$ 12.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.6% |

Market Dynamics

Growth Drivers

Quantified Unplanned Downtime Escalation and Predictive Maintenance Financial Validation

Unplanned equipment downtime represents an escalating organisational burden, validating substantial capital allocation to Asset Performance Management solutions. Unplanned downtime costs average US$260,000 per hour across industrial sectors, with automotive manufacturing experiencing hourly costs exceeding US$2.3 million and heavy industry sectors facing costs quadrupling from 2019 levels to US$4 million per hour by 2024.

Manufacturing globally loses approximately US$ 50 billion annually to unplanned downtime, with per-hour costs escalating 113% in automotive and 319% in heavy industry over the past five years due to rising energy prices and operational complexity. Predictive maintenance methodology demonstrates compelling financial returns; organisations implementing predictive maintenance achieve 18-25% maintenance-cost reductions compared to traditional reactive approaches, with 95% of organisations reporting positive ROI and 27% achieving complete payback within 12 months.

Predictive maintenance enables a 30-50% reduction in unplanned downtime while extending equipment lifespan 20-40%, with advanced failure prediction providing 5-7 days' notice for critical components and 2-4 weeks for gradual-degradation systems, enabling scheduled intervention during planned maintenance windows.

The Asset Performance Management Market directly benefits from these documented financial returns, as organisations allocate capital toward condition monitoring, predictive analytics, and asset-reliability optimisation capabilities, enabling data-driven maintenance decision-making. Aberdeen Group research documents organisations implementing APM achieving 22% maintenance-cost reduction, 15% equipment-uptime improvement, and 25% labour-productivity enhancement, establishing APM as operationally essential infrastructure supporting competitive manufacturing performance. This structured financial validation is accelerating organizational acceptance of digital asset-management platforms despite legacy technical-infrastructure barriers and organisational change-management challenges.

Renewable Energy Portfolio Expansion and Real-Time Asset Monitoring Requirements

The exponential deployment of renewable-energy infrastructure is creating unprecedented demand for advanced Asset Performance Management solutions supporting asset-health optimisation across geographically distributed solar, wind, hydro, and battery-storage portfolios. Renewable energy assets produce substantially elevated data volumes, solar installations generating approximately 5x more data than conventional generation assets, with battery-storage systems producing up to 100x more monitoring data, requiring sophisticated AI-driven analytics platforms consolidating heterogeneous data streams.

Fluence Energy expanded its Nispera™ cloud-based APM software in February 2023 to encompass energy storage alongside existing solar, wind, and hydro asset monitoring, providing real-time performance analysis and optimization across 8.5 GW of global renewable and storage assets.

IBM's October 2024 acquisition of Prescinto, a leading renewable-energy APM SaaS provider, enhanced IBM Maximo Application Suite with specialised AI-driven monitoring and automation capabilities for solar, wind, and energy-storage assets, exemplifying competitive positioning within renewable-energy sectors. GE Vernova introduced advanced AI-driven anomaly detection, failure prediction, digital-twin monitoring, and robotics-enabled autonomous inspections within its Asset Performance Management platform in December 2025, addressing renewable-energy operators' requirements for fleet-wide visibility across diversified solar, wind, hydro, and battery-storage portfolios.

Market captures substantial revenue from renewable-energy operators requiring unified monitoring platforms enabling centralised fleet visibility, performance benchmarking across geographically dispersed installations, and integrated market-signal analysis. Organisations managing renewable-energy portfolios require platforms supporting predictive maintenance planning for bearing failures, temperature-related battery-storage degradation prevention, and solar-panel soiling identification, specialised capabilities that drive Asset Performance Management platform adoption within renewable sectors.

Market Restraining Factors

Organisational Change Management and User Adoption Complexity

Asset Performance Management implementation encounters substantial organisational resistance rooted in workforce transition anxiety, skill-gap barriers, and established maintenance cultural norms. Approximately 35–45% of digital-transformation initiatives fail to achieve adoption targets within 18 months due to inadequate change-management planning and insufficient user engagement. Maintenance technicians perceive predictive analytics and autonomous asset-management systems as potential employment threats, creating organisational friction that slows Asset Performance Management platform deployment momentum.

Legacy maintenance engineering centres, particularly within large utilities and manufacturing enterprises, often resist decentralisation of analytical authority toward frontline operations, viewing distributed asset monitoring as a loss of expertise and centralisation. User scepticism regarding AI-generated predictive insights remains substantial, with organisational resistance to autonomous decision-making recommendations without human validation limiting adoption velocity.

Comprehensive implementation timelines extend 12–24 months when including organisational change management, workforce training, and operational process redesign. These adoption barriers create prolonged deployment cycles and require substantial professional services investment in change-enablement and capability building, materially increasing total-cost-of-ownership and limiting deployment velocity within smaller enterprises and cost-constrained segments.

Key Market Opportunities

Pharmaceutical and Life-Sciences Manufacturing Compliance Automation and Precision Asset Reliability

Pharmaceutical manufacturing requires FDA, EMA, and WHO GMP (Good Manufacturing Practice) compliance architectures mandating comprehensive documentation, deviation tracking, and audit-trail transparency requirements increasingly embedded within advanced Asset Performance Management platforms. Europe's regulatory and quality compliance solution market for pharma presents significant growth opportunities, reflecting accelerating investment in compliance automation.

European pharmaceutical firms face stringent EMA mandates and GDP/GMP enforcement requirements, compelling investment in real-time compliance solutions and digital transformation initiatives. AI-driven predictive analytics and natural language processing are transforming pharmacovigilance and automated risk detection, with cloud-native platforms enabling seamless regulatory updates with minimal IT overhead. Integration of IoT for real-time manufacturing monitoring is enhancing data integrity and quality traceability, supporting faster compliance validation and reduced regulatory risk.

Market captures substantial pharmaceutical-sector demand through solutions embedding regulatory compliance controls, integrated batch documentation, deviation management, and comprehensive audit trails supporting FDA Form 483 compliance and pre-approval inspection readiness. Asset-performance optimisation is critical to pharmaceutical production, where equipment failures directly impact batch consistency and product quality. Organisations deploying integrated asset-management systems achieve quantified benefits, including reduced unplanned downtime, improved overall equipment effectiveness (OEE) supporting pharmaceutical production targets, and optimised total-cost-of-ownership through evidence-based maintenance strategies aligned with equipment criticality classification.

Asia-Pacific Manufacturing Digital Transformation and Predictive Maintenance Adoption

The Asia-Pacific region is poised for substantial Asset Performance Management expansion through rapid industrialisation, increasing IoT and AI technology adoption, and smart manufacturing initiatives. Over 60% of Asia-Pacific manufacturers have either adopted or plan to adopt predictive maintenance solutions by 2026, reflecting accelerating Industry 4.0 implementation and connected device-ecosystem expansion.

China's AI-manufacturing roadmap emphasises accelerating adoption of AI-powered robotics, predictive maintenance, quality inspection, and digital twins across manufacturing sectors. India is experiencing rapid manufacturing expansion through government digital-transformation initiatives, and MSMEs are increasingly deploying AI-driven predictive maintenance. Bharat Forge, Bosch India, and Tata Steel case studies demonstrate 25-30% maintenance-cost savings and 10-12% energy-consumption improvements through predictive-maintenance implementation, validating strong financial viability and ROI.

ABB Motion's March 2025 strategic investment in UptimeAI exemplifies market opportunity evolution, combining AI/ML algorithms and expert systems to deliver predictive maintenance and optimised asset performance across cement, metals, and water-pipe sectors in India. The Asian regional market is positioned to capture substantial revenue growth through vendor positioning aligned with government digital-transformation initiatives and manufacturing-modernisation mandates. This opportunity addresses unmet organizational needs for specialized predictive-maintenance expertise and affordable Asset Performance Management solutions supporting MSME segments historically constrained by technology adoption barriers and capital constraints.

Category-wise Analysis

Solution Module Insights

Asset Reliability Management represents the dominant solution-module segment within the Asset Performance Management Market in 2026, capturing 33.0% of global revenue. This solution module encompasses reliability engineering practices, maintenance strategy optimization, spare-parts management, and root-cause failure analysis that enterprise customers prioritise when implementing comprehensive asset-management platforms. Asset Reliability Management solutions address organizational imperatives to maintain equipment performance, extend asset lifespan, and reduce unplanned failure frequency through data-driven maintenance decision-making aligned with equipment criticality and failure-consequence severity. ABB's ABB Ability™ Genix APM Suite exemplifies advanced asset-reliability capabilities, offering AI-driven predictive maintenance, asset monitoring, and lifecycle analysis, enabling users to reduce unplanned downtime by nearly 50% and improve overall operational efficiency.

Predictive Asset Analytics represents the fastest-expanding solution module within the Asset Performance Management Market, driven by machine-learning algorithm maturation, real-time sensor-data availability, and organizational demand for autonomous failure-prediction capabilities. Predictive Analytics capabilities integrate historical equipment-failure patterns, operational condition data, environmental factors, and maintenance-intervention outcomes to develop machine-learning models forecasting equipment failure probability.

Fluence Energy's Nispera™ platform demonstrates advanced predictive analytics functionality, including predictive maintenance alarms anticipating bearing failures in wind turbines, temperature-related battery-degradation prediction, and AI-based solar-soiling detection. GE Digital's recognition as a Leader in the 2022 Verdantix Green Quadrant for APM solutions supporting 40,000+ global users and delivering 292% ROI over five years for energy companies underscores market validation of advanced predictive-analytics capabilities. This solution-module segment will experience sustained growth acceleration as organisations increasingly transition from reactive maintenance toward proactive failure prevention enabled by AI-driven predictive analytics.

End Use Industry Insights

Energy and utilities sectors represent the largest end-use industry segment for the Asset Performance Management Market revenue in 2026, capturing 20.0% of global sales. Energy and utilities companies operate substantial fixed-asset portfolios including generation facilities, transmission and distribution infrastructure, and ancillary equipment requiring continuous operational reliability and maintenance optimization. U.S. investor-owned utilities are projecting substantial capital expenditure with accelerating investment in generation modernisation, transmission expansion, distribution improvements, and advanced technologies like battery energy storage and automated metering.

Utilities prioritise Asset Performance Management solutions supporting condition-based maintenance of aging equipment while managing transitions toward renewable-energy integration and grid-modernisation initiatives. Hitachi Energy launched its next-generation Lumada Asset Performance Management software in October 2023, integrating health, reliability, and optimization modules to provide unified asset views with AI-driven predictive maintenance, addressing utilities' requirements for comprehensive asset-lifecycle management.

Pharmaceuticals and life-sciences manufacturing sectors represent the fastest-expanding end-use industry segment within the Asset Performance Management Market, driven by FDA compliance modernization, quality-assurance intensification, and production-efficiency optimization imperatives. Pharmaceutical manufacturing is undergoing Pharma 4.0 digital transformation, integrating automation, robotics, and artificial intelligence to optimize production processes while ensuring regulatory compliance.

Deployment Mode

Cloud-based deployment represents the dominant deployment-mode segment within the Asset Performance Management Market in 2026, commanding 55.0% of global revenue. Cloud deployment eliminates heavy upfront capital expenditure for infrastructure, enables rapid deployment across geographically distributed facilities, and provides standardized compliance controls supporting multi-site enterprise management.

Cloud-based Asset Performance Management platforms provide elasticity enabling organizations to scale computational resources dynamically based on analytical workload demands. Renewable-energy operators managing geographically distributed assets leverage cloud-based Asset Performance Management platforms for centralized fleet monitoring, performance benchmarking across dispersed installations, and integrated market-signal analysis supporting dispatch optimization. Yokogawa Electric Corporation entered a global reseller agreement with Power Factors in December 2020 to market the Drive platform, a cloud-based APM solution for renewable power facilities, enabling optimization of solar, wind, and energy storage assets.

Regional Insights and Trends

North America Market Trend

North America represents the largest geographic Asset Performance Management Market region, commanding approximately 35% of global revenue. U.S. investor-owned energy and water utilities are committing record capital for infrastructure modernization, representing accelerating infrastructure-investment trends. The pressing need to replace aging infrastructure, expand renewable-energy generation capacity, and modernize distribution systems for reliability and safety is catalyzing substantial utility Asset Performance Management adoption.

Schneider Electric's November 2025 unified Asset Performance Management service model launch in the U.S., targeting 75% electrical-failure reduction and 40% downtime-cost reduction, exemplifies competitive positioning within North American utility infrastructure modernization. North American asset-intensive enterprises demonstrate substantial willingness to allocate capital toward preventive and predictive maintenance initiatives, with 46% of companies planning to introduce or change maintenance strategies and 32% seeking to expand monitoring capabilities.

Siemens Energy and Bentley Systems' October 2020 launch of APM4O&G, an Asset Performance Management solution combining oil and gas sector expertise with digital-twin diagnostics, demonstrates vendor positioning targeting North American oil and gas infrastructure optimization. The regional concentration of major Asset Performance Management vendors, including GE Digital, Aspen Technology, and IBM, creates competitive innovation intensity, driving continuous capability enhancement and feature expansion.

East Asia Market Trend

East Asia represents the second-largest Asset Performance Management Market region, accounting for approximately 15% of global revenue with the fastest projected growth rates through 2033. Over 60% of Asia-Pacific manufacturers have adopted or plan to adopt predictive maintenance solutions by 2026, reflecting accelerating Industry 4.0 implementation.

China's AI-manufacturing roadmap emphasizes accelerating the adoption of AI-powered robotics, predictive maintenance, and digital twins across manufacturing sectors. GE Vernova partnered with Fujitsu in December 2021 to launch EnergyAPM, an asset performance management solution tailored for Japan's transmission and distribution sector, enabling operators to enhance grid reliability and reduce ownership costs.

ABB Motion's strategic investment in UptimeAI in March 2025 demonstrates vendor positioning within heavy asset industries, including cement, metals, and water pipes, addressing regional requirements for affordable predictive-maintenance expertise supporting manufacturing modernization. The region's combined rapid industrialisation and government-backed digital-transformation initiatives position East Asia as the fastest-expanding Asset Performance Management market through 2033.

Europe Market Trend

Europe represents approximately 28% of the global Asset Performance Management Market revenue, with distinct emphasis on regulatory compliance, sustainability reporting, and energy-transition infrastructure modernization.

The European Union's Corporate Sustainability Reporting Directive (CSRD), Sustainability Disclosure Requirements (SDR), and asset-integrity-management mandates are driving substantial Asset Performance Management investment within energy utilities, manufacturing enterprises, and regulated sectors requiring comprehensive compliance documentation and risk-based asset-lifecycle planning. European utilities are modernising ageing infrastructure while integrating renewable-energy capacity, with European wind-power capacity expansion reaching 270 GW through 17 GW annual deployment, creating substantial demand for advanced asset-monitoring and turbine-optimisation platforms.

The European regulatory emphasis on data-governance excellence and privacy protection drives preference for Asset Performance Management vendors demonstrating comprehensive data-residency controls, transparent algorithmic design, and compliance certifications addressing GDPR and emerging AI Act requirements.

German Industrie 4.0 initiatives and European government support for digital-infrastructure development are supporting domestic Asset Performance Management vendors and European cloud-infrastructure alternatives to North American platform dominance. European organizations demonstrate sophisticated maintenance-engineering maturity and emphasis on structured asset-lifecycle planning aligned with sustainability reporting frameworks and long-term infrastructure modernization strategies.

Competitive Landscape

The Global Asset Performance Management (APM) market is moderately consolidated, characterized by a limited group of technologically advanced vendors that collectively influence product innovation, pricing, and digital transformation strategies.

The market is shaped by strong competition among leading companies such as ABB, IBM, GE Vernova, Schneider Electric, Aspen Technology, and Hitachi Energy, each offering comprehensive AI-driven asset health, predictive maintenance, and reliability optimization platforms. These players dominate due to their deep industrial presence, integrated software ecosystems, and expanding capabilities in AI, digital twins, cloud analytics, and condition monitoring.

Continuous enhancements such as generative AI copilots, autonomous inspections, and energy-specific APM modules strengthen their market positions and raise barriers for new entrants. Strategic acquisitions, technology partnerships, and vertical-specific solutions further reinforce the oligopolistic nature of the market, enabling these leaders to capture large enterprise clients across power, manufacturing, oil & gas, and utilities.

Key Industry Developments

- December 02, 2025, GE Vernova introduced new AI-driven capabilities within its APM platform, including enhanced anomaly detection, digital-twin–based monitoring, autonomous robotics inspections, and cloud-based fleet analytics, helping renewable energy operators improve asset reliability, minimise downtime, and optimize solar, wind, hydro, and battery storage portfolios.

- Nov. 18, 2025, Schneider Electric launched its unified Asset Performance Management service model in the U.S., offering an integrated platform to reduce electrical failures and unplanned downtime by up to 75%, cut planned maintenance costs by up to 40%, and address ageing infrastructure and rising electrification demands across critical industries.

- May 5, 2025, ABB expanded generative AI capabilities in its Genix APM solution with the launch of Genix APM Copilot, delivering role-specific predictive and prescriptive analytics, automated contextualised data flow, and actionable insights to enhance asset reliability, reduce downtime, and improve operational efficiency across industrial operations.

Companies Covered in Asset Performance Management Market

- ABB

- Aspen Technology Inc

- AVEVA Group Limited

- Bentley Systems, Incorporated

- DNV GLAS

- GE Vernova

- IBM Corporation

- Rockwell Automation

- SAP SE

- SAS Institute, Inc.

- Siemens Energy

Frequently Asked Questions

The global Asset Performance Management market is projected to be valued at US$ 5.2 Bn in 2026.

The Asset Reliability Management segment is expected to account for approximately 33.0% of the global Asset Performance Management market by Solution Module in 2026.

The market is expected to witness a CAGR of 13.3% from 2026 to 2033.

The Asset Performance Management market is driven by escalating unplanned downtime costs, validated financial returns from predictive maintenance, and the growing need for real-time monitoring and optimization of renewable-energy and industrial assets.

Key market opportunities in the Asset Performance Management market include pharmaceutical and life-sciences compliance automation, AI-driven predictive analytics, IoT-enabled real-time monitoring, and Asia-Pacific manufacturing digital transformation with predictive-maintenance adoption.

The key players in the Asset Performance Management market include ABB, IBM, GE Digital, Siemens, Schneider Electric, AVEVA, Aspen Technology, and Bentley Systems.