- Beauty & Personal Care

- K-Beauty Product Market

K-Beauty Product Market Size, Share, and Growth Forecast, 2026 - 2033

K-Beauty Product Market by Product (Skin Care, Hair Care, Makeup, Others), Distribution Channel (Supermarkets & Hypermarkets, Mass Merchandiser, Specialty Retailer, Convenience Stores, Online, Pharmacy & Drug Stores, Others), End-user, and Regional Analysis for 2026 - 2033

K-Beauty Product Market Size and Trends

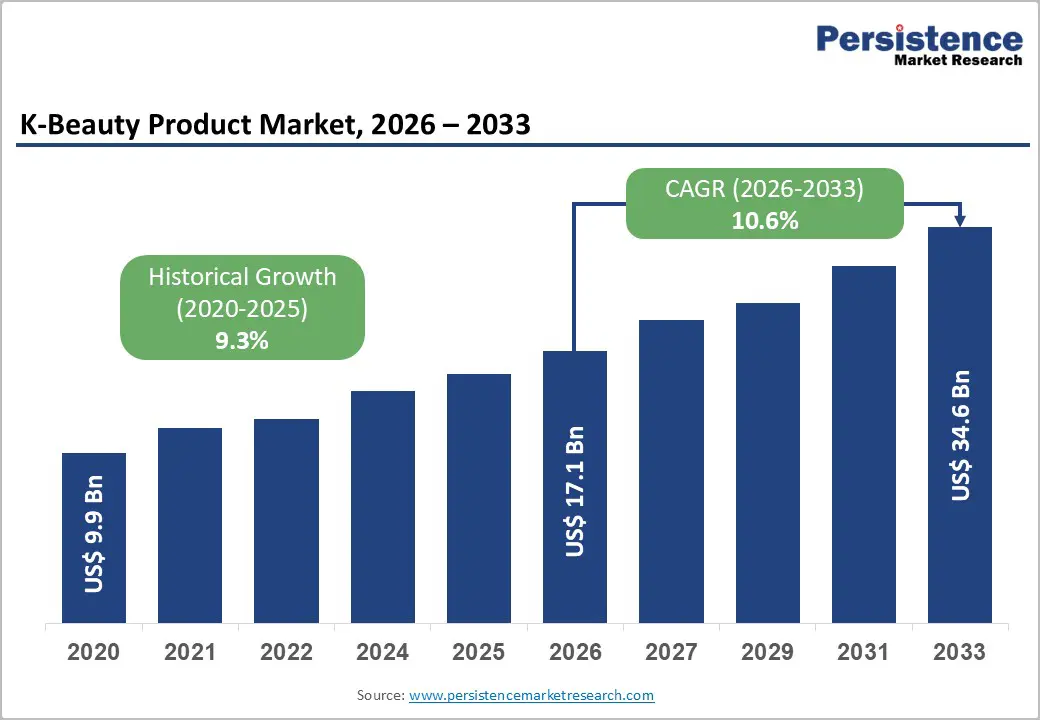

The global K-Beauty product market size is projected to rise from US$17.1 billion in 2026 to US$34.6 billion by 2033, growing at a CAGR of 10.6% during the forecast period from 2026 to 2033, driven by the global influence of Korean pop culture, particularly through K-pop and K-dramas, which have generated substantial consumer interest in authentic Korean skincare and cosmetic products worldwide.

The increasing consumer preference for products featuring natural and organic ingredients, the revolutionary multi-step skincare routines that prioritize hydration and skin health, and the rapid adoption of digital commerce platforms, combined with social media influencer marketing, have transformed K-Beauty from a regional phenomenon into a truly global marketplace.

Key Industry Highlights:

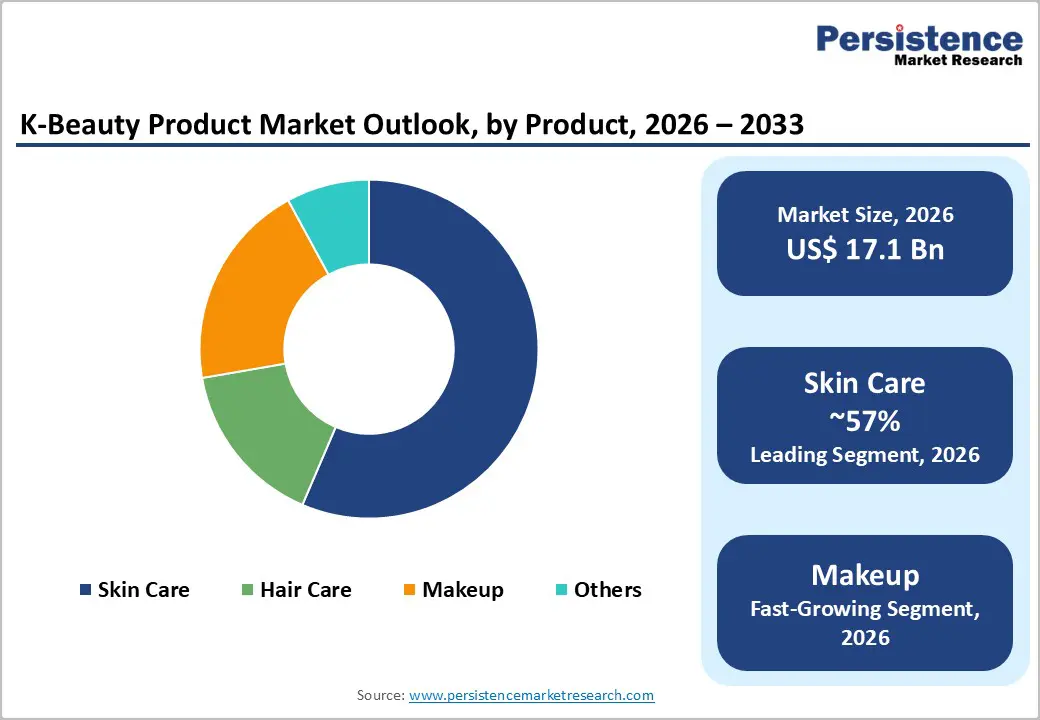

- Leading Product: Skin Care dominates the global K-Beauty market, with an over 57% share in 2026, valued at more than US$9.7 Bn, driven by core consumer needs for hydration, barrier repair, acne control, pigmentation reduction, and anti-aging. Makeup is the fastest-growing category at an 11.4% CAGR, fueled by Gen Z and Millennials seeking quick results, self-expression, and hybrid skin-first cosmetics influenced by K-pop and social media trends.

- Leading Distribution Channel: Online leads with over 45% market share in 2026, valued at more than US$ 7.7 Bn, as consumers increasingly rely on digital content, influencer reviews, and ingredient breakdowns before purchasing. Cross-border e-commerce enables global access to Korean brands, fulfilling the need for convenience, variety, and trend-driven shopping. Specialty Retailers are the fastest-growing channel at a 10.8% CAGR, driven by the need for expert guidance, in-store consultations, sampling, and curated product ranges that support complex multi-step routines.

- Leading End-user: Women account for the largest share at over 76% in 2026, valued at more than US$13Bn, due to higher engagement in multi-step skincare, preventive beauty habits, and strong demand for hydration, brightening, anti-aging, and acne solutions. Men are the fastest-growing segment at a 9.8% CAGR, supported by rising awareness of skincare needs, urban pollution exposure, and growing acceptance of male grooming influenced by Korean pop culture.

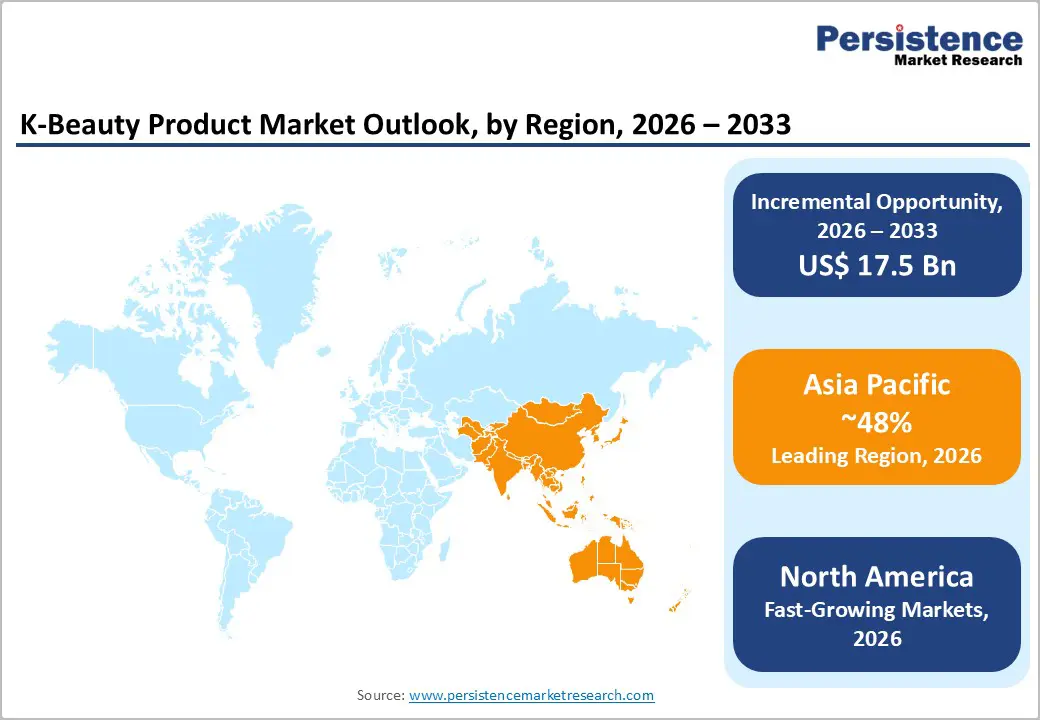

- Leading Region: Asia-Pacific leads the K-Beauty market with over 48% share in 2026, reaching US$8.2B, owing to its large consumer base and a strong source of innovation. North America holds the second-largest share at over 26% in 2026, driven by the glass skin trend and strong digital adoption through TikTok, Instagram, and influencer marketing. Europe is growing strongly at an 8.7% CAGR, supported by demand for clinically proven, dermatologically tested, and clean-beauty products, despite stricter regulatory entry barriers.

| Key Insights | Details |

|---|---|

| K-Beauty Product Market Size (2026E) | US$17.1 Bn |

| Market Value Forecast (2033F) | US$34.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.3% |

Market Dynamics

Driver - Cultural Influence and Digital Virality Through Social Media Platforms

The convergence of Korean pop culture and digital technology has reshaped consumer behavior in the beauty industry, driving global demand for K-Beauty products. More than a million social media posts linking K-Beauty to K-pop and K-dramas have fueled organic brand advocacy and expanded reach beyond traditional demographics. Viral trends such as the glass skin concept have been rapidly adopted by Gen Z and Millennials worldwide, with platforms like TikTok, Instagram, and YouTube accelerating their spread. Single-product demonstrations garner millions of views and trigger instant stock-outs, reflecting the power of digital virality.

Innovation in Formulations and the Premiumization of Skincare Routines

Korean beauty brands have gained a strong competitive edge by continuously innovating ingredients and scientific formulations, blending advanced skincare science with traditionally sourced natural actives like snail mucin, propolis, fermented extracts, and botanical compounds. Their focus on multifunctional products that target multiple skin concerns in a single step appeals to busy, results-driven consumers seeking efficiency. The cultural influence of the multi-step Korean skincare routine has transformed skincare into an aspirational lifestyle practice, raising perceived value and enabling premium pricing in mature markets such as North America and Western Europe. The ongoing release of specialized solutions for concerns like barrier repair, hyperpigmentation, and pollution defense keeps consumers engaged and encourages repeat purchases across diverse demographics.

Restraint - Rise in Trade Tariffs and Supply Chain Cost Pressures

The K-Beauty market is facing rising cost pressures from global trade protectionism and tariffs, affecting both finished products and essential raw materials. US import duties on Korean cosmetics and related components vary by product classification and are subject to unpredictable increases, creating uncertainty for importers and consumers. Tariffs on key ingredients and packaging materials from China have also risen sharply in recent years, significantly raising input costs across the supply chain. Mid-sized and indie brands are particularly vulnerable because they lack the scale to absorb higher costs or negotiate better pricing, putting pressure on retail pricing and market penetration.

Complex Regulatory Compliance and Fragmented Market Entry Requirements

The K-Beauty market faces complex regulatory compliance and fragmented entry requirements across key regions, creating major barriers for smaller players. In the U.S., the FDA’s MoCRA requires extensive product and facility registrations, safety documentation, and adherence to good manufacturing practices, which increases time and costs. Europe’s CPNP framework requires pre-market safety assessments and ingredient approvals, further extending product launch timelines and raising development expenses. These layered compliance obligations protect established brands and limit market access for smaller innovators, as regulatory costs covering lab testing, toxicology, documentation, and legal support consume a significant share of gross margins, reducing funds available for marketing, R&D, and distribution expansion.

Opportunity - Growing Awareness of Sun Protection & Anti-Aging

Consumers increasingly understand the long-term damage caused by UV exposure, and demand for daily sunscreen and UV-shielding skincare is rising sharply. Anti-aging awareness is prompting consumers to adopt preventive skincare early, rather than treatment-focused routines. K-Beauty’s emphasis on layering, gentle actives, and hydration-based formulations fits well with this trend, encouraging higher product adoption and repeat purchases. Brands capitalize on the trend by launching combined sun protection and anti-aging products, such as SPF creams containing antioxidants, peptides, or collagen-boosting ingredients. This creates cross-selling opportunities and supports premiumization, as consumers are willing to pay more for products that offer both protection and age-defying benefits.

Rising Focus on Sensitive Skin and Dermatologist-Approved Products

Consumers are becoming more aware of skin barrier health and are shifting toward gentle, low-irritant formulations that reduce redness and inflammation. This pushes brands to develop hypoallergenic, fragrance-free, and pH-balanced products, driving innovation in soothing ingredients like centella asiatica, madecassoside, and ceramides. Dermatologist-backed products also build trust and credibility, encouraging higher purchase frequency and premium pricing. Retailers and online platforms are expanding dedicated sensitive-skin ranges, making it easier for consumers to discover and trial these products. K-Beauty’s reputation for advanced formulations and clinical skincare strengthens its position in this segment.

Category-wise Analysis

Product Insights

Skin care dominates the global market, capturing more than 57% share in 2026 with a value exceeding US$ 9.7 billion, as it directly addresses core consumer needs like hydration, barrier repair, acne control, pigmentation reduction, and anti-aging. The K-Beauty philosophy emphasizes prevention and long-term skin health over quick cosmetic fixes, making daily skin care a necessity rather than an occasional purchase. Multi-step routines drive repeat usage across cleansers, toners, serums, and sunscreens, increasing overall consumption. Rising sensitivity to pollution, stress, and climate conditions pushes consumers toward gentle, functional skin care solutions as an essential part of self-care.

Makeup demonstrates a significant 11.4% CAGR, driven by shifting consumer needs toward fast, visible results and self-expression, particularly among Gen Z and younger millennials. K-Beauty makeup emphasizes a skin-first approach, with hybrid products that meet demand for lighter textures, natural finishes, and multifunctionality. The surge of social media, K-pop, and K-drama influence is accelerating experimentation with color cosmetics and trend-led launches. Rising demand for customizable, inclusive, and clean-label makeup aligns strongly with evolving beauty routines and daily-use needs.

Distribution Channel Insights

Online holds a 45%+ share in 2026, with a value exceeding US$7.7B, as it directly meets how consumers want to discover, compare, and buy beauty products today. K-Beauty buyers rely heavily on digital content, social media, influencer tutorials, reviews, and ingredient breakdowns, which seamlessly link to instant online purchasing. Online platforms also provide wider product variety, faster access to new launches, and authentic brand storytelling that physical stores cannot match on scale. Cross-border e-commerce makes Korean brands easily accessible globally, fulfilling the need for convenience, transparency, and trend-driven shopping.

The specialty retailer is expected to grow at a significant rate, with a CAGR of 10.8%, driven by consumers' increasing need for expert guidance, product education, and skin-type-specific solutions that mass channels can’t deliver effectively. K-Beauty routines are multi-step and ingredient-driven, making in-store consultation, sampling, and demonstrations highly valuable. These retailers also curate authentic, trend-led brands and launch products more quickly, thereby addressing trust and freshness concerns. Their strong omnichannel presence matches how K-Beauty shoppers discover and experiment with new products.

End-user Insights

Women account for the largest market share at over 76% in 2026, with a value exceeding US$13Bn, owing to their skincare and beauty needs being more routine-driven, multi-step, and prevention-focused. K-Beauty strongly emphasizes hydration, brightening, anti-aging, acne care, and sensitive-skin solutions that women actively incorporate into their daily regimens. Higher engagement with layered skincare naturally increases product usage frequency and category depth. Strong interest in ingredient transparency, skin health, and long-term results aligns closely with K-Beauty’s formulation philosophy, reinforcing sustained adoption among women.

Men segment is expected to grow at a CAGR of 9.8% due to rising demand for simple, effective, and preventive skincare solutions. Urban lifestyles, pollution exposure, and longer screen time are increasing concerns around acne, sensitivity, and premature aging among men. K-Beauty brands address these needs with multi-functional, lightweight, and routine-friendly products such as all-in-one lotions, essences, and sun care. Growing social acceptance of male grooming, driven by Korean pop culture and workplace appearance norms, further accelerates adoption.

Regional Insights

North America K-Beauty Product Market Trends

North America is expected to hold a share of more than 26% by 2026, driven by trends such as the glass skin aesthetic, particularly among Gen Z and Millennials. Korean skincare products, including hydrating serums, essences, and sleeping masks, have gained widespread popularity, supported by influential brands that have achieved significant market penetration. Digital commerce and social media platforms like TikTok and Instagram, along with influencer marketing, have become primary drivers of adoption and conversion. Regulatory requirements in the region are manageable for established Korean brands due to their compliance capabilities and strong retail partnerships. Major beauty retailers and upcoming Korean retail expansions are further strengthening the market infrastructure and signaling long-term confidence in North America’s growth potential.

Asia Pacific K-Beauty Product Market Trends

Asia Pacific holds over 48% share in 2026, reaching US$ 8.2 Bn value, serving as both the largest consumer base and the main source of global innovation. While China remains a major export destination, the market is facing challenges such as tariff complexity, evolving regulations, and a shift toward premium and direct-to-consumer models, which have reduced export volumes. India is the fastest-growing market in the region, driven by rising awareness of Korean skincare, increasing disposable income in cities, and strong e-commerce expansion that improves accessibility. Southeast Asian countries like Vietnam, the Philippines, Indonesia, and Thailand are also showing fast adoption, supported by dominant regional online platforms and a growing middle class.

Europe K-Beauty Product Market Trends

Europe is expected to grow at a significant rate with a CAGR of 8.7%, driven by strong regional variation in consumer preferences and regulations. Germany leads Europe, supported by demand for dermatologically tested, clinically proven, and clean-beauty products. The UK and France are major secondary markets, with premium positioning and selective distribution through specialty retailers and department stores. EU Cosmetics Regulation (EC) No 1223/2009 imposes strict pre-market safety and ingredient requirements, creating barriers to entry but conferring a competitive advantage on compliant brands. Despite Europe’s proximity to Korean manufacturing, penetration remains lower than in Asia and North America, owing to strong local heritage brands and greater consumer skepticism toward non-traditional beauty origins.

Competitive Landscape

The K-Beauty product market is highly fragmented, with numerous brands competing across skincare, makeup, and haircare etc. segments. Manufacturers primarily differentiate through innovation in formulations and rapid product launches to match fast-moving consumer trends. They also focus on brand storytelling and influencer-driven marketing, leveraging social media and K-culture appeal to build loyalty. To compete in pricing, many adopt tiered offerings while maintaining consistent quality. Strong distribution networks, online marketplaces, specialty beauty stores, and cross-border e-commerce help them scale quickly and capture global demand.

Key Industry Developments :

- In January 2026, Sephora and CJ Olive Young formed a strategic partnership to bring top Korean beauty and health products to Sephora’s global customers. The collaboration will launch as an omnichannel offering in the US, Canada, Hong Kong, and Southeast Asia, with expansion to more regions in 2027. The partnership will feature dedicated Olive Young-curated zones in Sephora stores and online, combining Sephora’s retail expertise with Olive Young’s trend-driven product selection.

- In November 2025, Only teamed up with Korean beauty brand Laneige to launch a Gen Z-focused fashion and skincare collection called The Vibe Shift, available online and in stores from November 12. The collaboration combines casual wear with Laneige skincare products and aims to create an immersive cultural experience for young Indian shoppers, with the collection launching exclusively on Myntra and at Only’s Palladium Mall store in Mumbai.

Companies Covered in K-Beauty Product Market

- CJ OliveYoung

- Laneige

- Sulwhasoo

- Etude House

- LG Household & Health Care

- Amorepacific Corporation

- The Face Shop

- Nature Republic

- COSRX

- Clio Cosmetics

- Missha

- Dr. Jart+

- Banila Co

- Holika Holika

- Peripera

- Others

Frequently Asked Questions

The global K-beauty product market is projected to be valued at US$17.1 Bn in 2026.

The demand for innovative, science-backed skincare solutions that deliver visible results, along with a growing focus on natural, gentle ingredients and personalized beauty routines, are key drivers of the market.

The market is expected to witness a CAGR of 10.6% from 2026 to 2033.

Expansion through affordable and travel-friendly formats, and AI-driven personalization to offer tailored skincare routines, is creating strong growth opportunities.

CJ OliveYoung, Laneige, Sulwhasoo, Etude House, LG Household & Health Care, Amorepacific Corporation, The Face Shop are among the leading key players.