- Metals & Minerals

- Alumina Trihydrate Market

Alumina Trihydrate Market Size, Share, and Growth Forecast, 2026 - 2033

Alumina Trihydrate Market by Application (Flame Retardant, Catalyst, Filler, Others), End-use Industry (Water Treatment, Building & Construction, Paints & Coatings, Glass, Plastic, Pharmaceutical, Others), and Regional Analysis for 2026 – 2033

Alumina Trihydrate Market Size and Trends Analysis

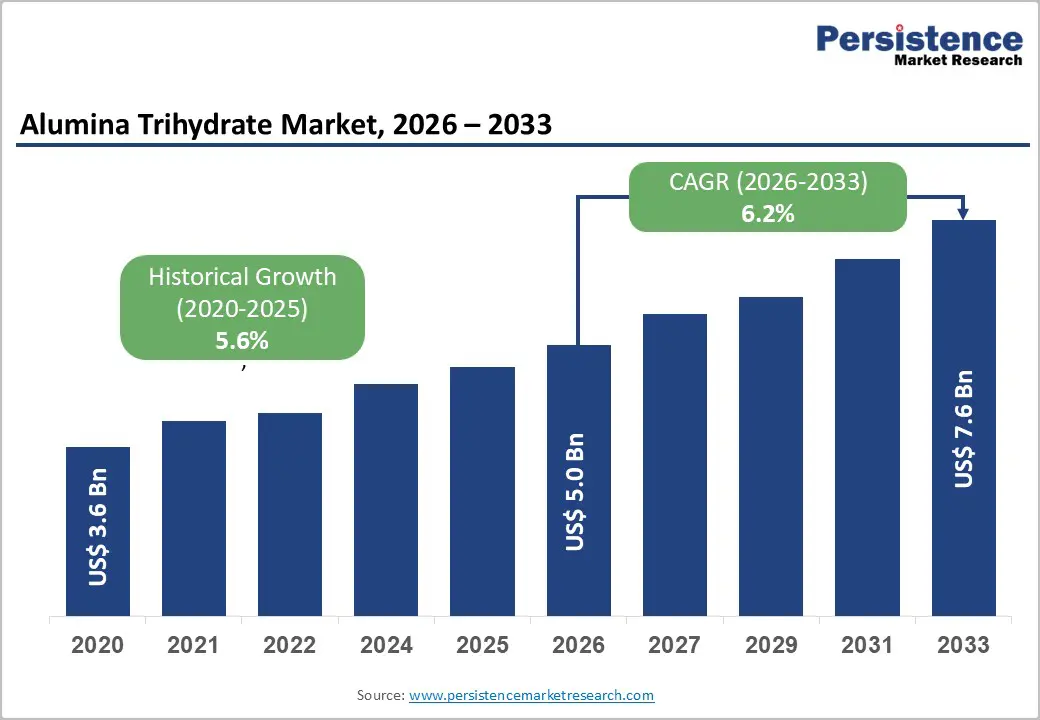

The global alumina trihydrate market size is likely to be valued at US$5.0 billion in 2026, and is expected to reach US$7.6 billion by 2033, growing at a CAGR of 6.2% during the forecast period from 2026 to 2033, driven by the increasing prevalence of stringent fire safety regulations, rising demand for non-halogenated flame retardants in plastics and building materials, and growing consumption of alumina trihydrate as a cost-effective filler in paints, coatings, and composites.

Growing demand for high-purity, fine-particle alumina trihydrate, especially for flame retardant and filler applications in wire & cable and construction, is accelerating adoption across end-use industries. Advances in surface-treated and nano-engineered grades are further boosting uptake by offering better dispersion, lower loading levels, and improved mechanical properties. Increasing recognition of alumina trihydrate as a critical halogen-free, smoke-suppressant solution in emerging regulatory-driven markets remains a major driver of market growth.

Key Industry Highlights:

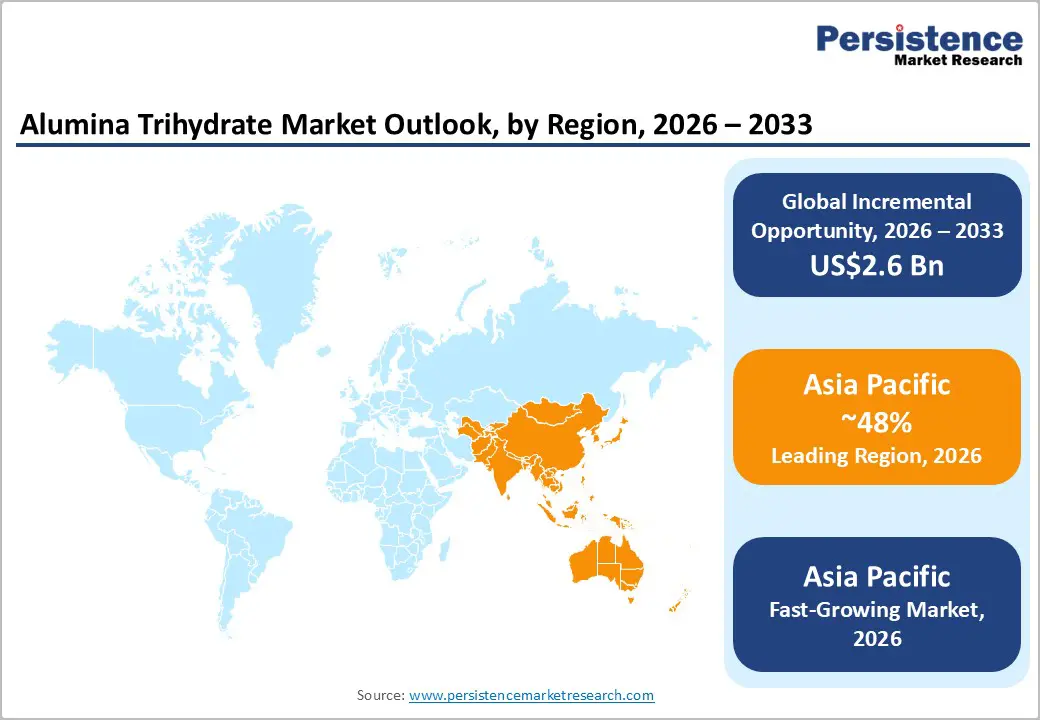

- Leading Region: Asia Pacific, anticipated to account for a 48% market share in 2026, driven by massive plastics & rubber production, rapid construction growth, and strong demand in China and India.

- Fastest-growing Region: Asia Pacific, fueled by expanding wire & cable manufacturing, rising building & construction activity, and growing investments in halogen-free FR compounds.

- Dominant Application: Flame retardant, to hold approximately 58% of the market share, as it remains the largest volume application globally.

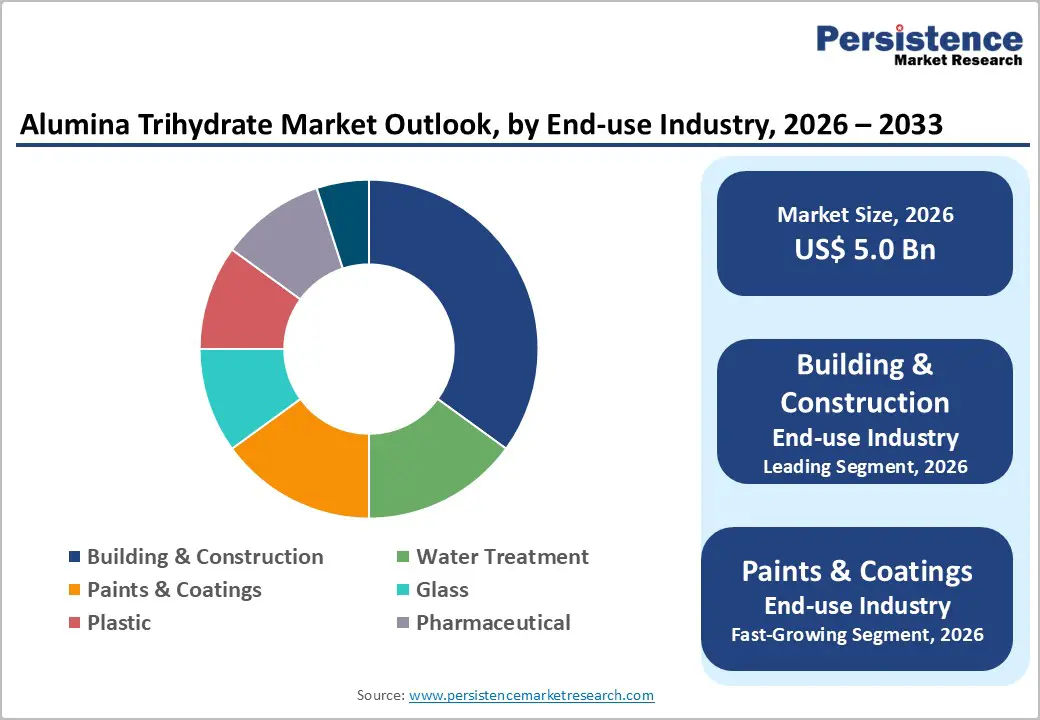

- Leading End-use Industry: Building & construction accounts for over 32% of the market revenue, due to widespread use in insulation, panels, and sealants.

| Key Insights | Details |

|---|---|

| Alumina Trihydrate Market Size (2026E) | US$5.0 Bn |

| Market Value Forecast (2033F) | US$7.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Stringent Fire Safety Regulations and Halogen-Free Flame Retardants

Increasingly strict fire safety regulations across construction, transportation, electrical, and consumer goods industries are playing a decisive role in influencing material choices and product development worldwide. Governments and regulatory bodies are enforcing tougher standards to minimize fire-related hazards, reduce smoke generation, and limit the release of toxic gases during combustion. These regulations are particularly strong in public infrastructure, residential buildings, mass transit systems, and electronic applications, where fire incidents can lead to severe loss of life and property.

Manufacturers are under growing pressure to adopt materials that meet higher fire performance benchmarks without compromising safety or compliance. There is a clear shift away from traditional halogen-based flame retardants due to concerns over their environmental persistence, toxicity, and harmful emissions when exposed to fire. Halogen-free flame retardants are increasingly favored as they offer effective fire resistance while producing lower smoke density and fewer corrosive or toxic by-products.

This transition aligns closely with broader sustainability goals, stricter chemical regulations, and rising consumer awareness around health and environmental impact. These trends are accelerating demand for halogen-free solutions in polymers, cables, coatings, and building materials.

High Energy Intensity and Raw Material Price Volatility

High energy intensity combined with frequent fluctuations in raw material prices poses a significant challenge for industries dependent on energy-heavy manufacturing processes and mineral-based inputs. The production of materials such as alumina and related derivatives requires substantial amounts of electricity and thermal energy for extraction, refining, and calcination. As global energy markets remain unstable due to geopolitical tensions, supply constraints, and the ongoing transition toward renewable power, manufacturers are exposed to rising and unpredictable energy costs.

This directly impacts operating margins, particularly for producers in regions with high electricity tariffs or limited access to stable energy supplies. Raw material prices are subject to significant fluctuations driven by changes in mining output, environmental regulations, transportation costs, and demand from downstream industries. Factors such as stricter mining regulations, weather disruptions, and logistical bottlenecks can quickly tighten supply and push prices upward. These fluctuations make long-term cost planning difficult and increase financial risk for producers and end-users alike.

Opportunities in Surface-Treated and Nano-Engineered Grades

Opportunities in surface-treated and nano-engineered grades are expanding as industries demand higher-performing, more specialized materials that deliver enhanced functionality beyond conventional formulations. Surface treatment technologies allow materials to be tailored for improved compatibility with polymers, better dispersion, and stronger interfacial bonding. These enhancements enable manufacturers to achieve superior mechanical strength, flame retardancy, and durability while using lower material loadings, which helps reduce overall product weight and cost.

As end-users seek performance optimization without sacrificing process efficiency, surface-treated grades are gaining strong traction across plastics, coatings, adhesives, and composite applications. Nano-engineered grades offer even greater potential by unlocking unique properties derived from controlled particle size and morphology. Reduced particle dimensions increase surface area, leading to improved reactivity, enhanced thermal stability, and better barrier properties.

These characteristics are particularly valuable in high-value applications such as electric vehicles, electronics, advanced building materials, and specialty coatings, where precision performance and reliability are critical. Nano-engineered materials also support innovation in lightweight and multifunctional components, aligning with broader trends in energy efficiency and miniaturization.

Category-wise Analysis

Application Insights

Flame retardant is expected to lead the market, holding 58% of the share in 2026, driven by its widespread use across construction, electrical, automotive, and consumer goods applications. Increasing safety regulations and stricter fire performance standards are encouraging manufacturers to incorporate effective flame-retardant materials into products and building components. Rising demand for halogen-free and environmentally safer solutions is further strengthening this segment’s dominance.

Hindalco Industries Ltd, a major global producer of alumina trihydrate (ATH), markets ATH grades specifically engineered for halogen-free flame retardant applications in cables, plastics, and composites. Its ATH products help materials meet stringent fire and smoke resistance standards such as UL94 V0 and EN45545, which are required in electrical wiring, building materials, and transportation systems to enhance fire safety and reduce toxic emissions during a fire.

Filler is likely the fastest-growing application, driven by its ability to enhance material performance while reducing overall formulation costs. As industries such as plastics, rubber, paints, and coatings seek cost-effective solutions, fillers are increasingly used to improve mechanical strength, opacity, surface finish, and dimensional stability. Growing demand for lightweight and durable materials in construction, automotive, and packaging further supports this trend.

Fillers help manufacturers optimize raw material usage without compromising quality, making them attractive in price-sensitive markets. Shandong Xiangsong Chemical Co., Ltd. produces ATH alumina trihydrate filler that is supplied for applications such as solid surface materials, composite products, SMC/BMC moulding, and filler in plastics and engineered materials. Their ATH grades are used to enhance mechanical properties, improve surface finish, and reduce formulation costs while also contributing flame-retardant characteristics when needed.

End-use Industry Insights

The building & construction segment is expected to dominate the market, contributing nearly 32% of revenue share in 2026, propelled by rising infrastructure development and increasing emphasis on fire safety and material durability. Rapid urbanization, growth in residential and commercial construction, and renovation of aging infrastructure are boosting demand for high-performance materials. The sector increasingly relies on materials that offer fire resistance, smoke suppression, and improved mechanical strength to meet stricter building codes.

Huber Engineered Materials (part of J.M. Huber Corporation) supplies alumina trihydrate (ATH) grades used in construction materials such as fire-resistant coatings, insulation panels, roofing systems, and cable sheathing to improve fire safety and compliance with building codes. Huber’s halogen-free ATH products serve as flame retardants and smoke suppressants in a range of construction applications, from roof coatings to composite construction materials, helping builders meet stringent fire performance and safety requirements.

The paints & coatings segment represents the fastest-growing end-use industry, driven by increasing demand for fire-resistant, durable, and eco-friendly surface finishes. ATH is widely used as a flame-retardant filler in decorative and protective coatings, enhancing thermal stability, corrosion resistance, and smoke suppression. Rapid industrialization, urban development, and stricter fire safety regulations in commercial and residential buildings are driving the adoption of ATH-based coatings.

Growing emphasis on halogen-free and environmentally safe materials aligns with sustainability goals, encouraging manufacturers to incorporate ATH. TOR Specialty Minerals, which supplies ALUPREM alumina trihydrate (ATH) for powder coatings, roof coatings, industrial paints, and primers. Their ATH products improve surface performance and can also help control properties such as gloss in coatings, showing real application beyond just flame retardancy into standard coatings markets.

Regional Insights

North America Alumina Trihydrate Market Trends

The growth of the North American market is driven by the region's well-established plastics and coatings industry, robust research and development capabilities, and heightened public awareness of fire safety benefits. Production systems in the U.S. and Canada play a key role in supporting alumina trihydrate programs, ensuring broad accessibility across flame retardants, fillers, and paints & coatings sectors. The rising demand for surface-treated, convenient, and easily dispersible forms is further boosting adoption, as these formats enhance performance and overcome challenges associated with traditional fillers.

Innovation in alumina trihydrate technology, including stable nano-engineered, improved flame-retardant delivery, and targeted low-smoke enhancement, is attracting significant investment from both public and private sectors. Government initiatives and NFPA campaigns continue to promote use against fire risks, regulatory pressure, and emerging sustainability threats, creating sustained market demand. The growing focus on paints & coatings grades and specialty uses, particularly for building & construction and others, is expanding the target applications for alumina trihydrate.

Europe Alumina Trihydrate Market Trends

Europe's growth is driven by rising awareness of the benefits of non-halogenated materials, strong regulatory frameworks, and government-led initiatives promoting sustainable materials. Countries such as Germany, France, Italy, and the U.K. have established plastics industries that support the regular use of alumina trihydrate and encourage the adoption of innovative additive delivery methods. These fire-safe formulations are especially attractive to the building and construction sectors, regulation-focused manufacturers, and paints & coatings users, as they enhance compliance and coverage rates.

Technological advancements in alumina trihydrate development, such as enhanced surface treatment, application-targeted delivery, and improved fine-particle grades, are further boosting market potential. European authorities are increasingly supporting research and trials for alumina trihydrate against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, low-smoke options is aligned with the region’s focus on preventive fire safety and reducing toxic emissions. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while suppliers are investing in processing and novel variants to increase efficacy.

Asia Pacific Alumina Trihydrate Market Trends

Asia Pacific is projected to dominate and be the fastest-growing market, capturing the 48% revenue in 2026, propelled by rising plastics awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting alumina trihydrate campaigns to address construction growth and emerging wire & cable needs. Alumina trihydrate is particularly attractive in these regions due to its cost-effective administration, ease of compounding, and suitability for large-scale plastics drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-incorporate alumina trihydrate, which can withstand challenging compounding conditions and minimize loading dependence. These innovations are critical for reaching domestic producers and improving overall additive coverage. Growing demand for flame retardants, fillers, and paints & coatings applications is contributing to market expansion. Public-private partnerships, increased plastics expenditure, and rising investments in alumina trihydrate research and processing capacity are further accelerating growth. The convenience of alumina trihydrate delivery, combined with improved flame resistance and reduced risk of toxic gases, positions it as a preferred choice.

Competitive Landscape

The global alumina trihydrate market features competition between established specialty chemical leaders and emerging cost-competitive suppliers. In North America and Europe, Huber Engineered Materials and Nabaltec AG lead through strong R&D, distribution networks, and industrial ties, bolstered by innovative surface-treated and fine-particle programs.

In Asia Pacific, Aluminum Corp. of China Ltd. advances with localized solutions, enhancing accessibility. Surface-treated delivery boosts dispersion, cuts loading risks, and enables mass integrations across compounds. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Nano-engineered formulations solve performance issues, aiding penetration in high-end applications.

Key Industry Developments:

In May 2025, J.M. Huber Corporation acquired the Alumina Trihydrate (ATH), Antimony-Free Flame Retardant, and Molybdate-Based Smoke Suppressant assets from The R.J. Marshall Company. The assets were integrated into Huber Advanced Materials (HAM), a strategic business unit of Huber Engineered Materials, a division of J.M. Huber Corporation. This acquisition enhanced HAM's product portfolio and strengthened its position as a leader in the North American market for flame-retardant and smoke suppressant technologies.

Companies Covered in Alumina Trihydrate Market

- Sumitomo Chemical Co. Ltd.

- Aluminum Corp. of China Ltd.

- Nabaltec AG

- National Aluminium Company Ltd.

- Huber Engineered Materials

- SCR Sibelco NV

- R.J. Marshall Company

- Alteo

- Southern Ionics Incorporate

Frequently Asked Questions

The global alumina trihydrate market is projected to reach US$5.0 billion in 2026.

Stringent fire safety regulations and demand for halogen-free flame retardants are the key drivers.

The alumina trihydrate market is poised to witness a CAGR of 6.2% from 2026 to 2033.

Surface-treated and nano-engineered grades are the key opportunities.

Huber Engineered Materials, Nabaltec AG, Sumitomo Chemical Co., Ltd., Aluminum Corp. of China Ltd., and Alteo are the key players.