- Specialty & Fine Chemicals

- Europe Activated Alumina Market

Europe Activated Alumina Market Size, Share, and Growth Forecast 2026 - 2033

Europe Activated Alumina Market by Application (Catalyst, Desiccant, Adsorbent, Others), End-user (Water Treatment, Oil and Gas, Plastics, Healthcare, Others), and Regional Analysis for 2026 - 2033

Europe Activated Alumina Market Size and Trend Analysis

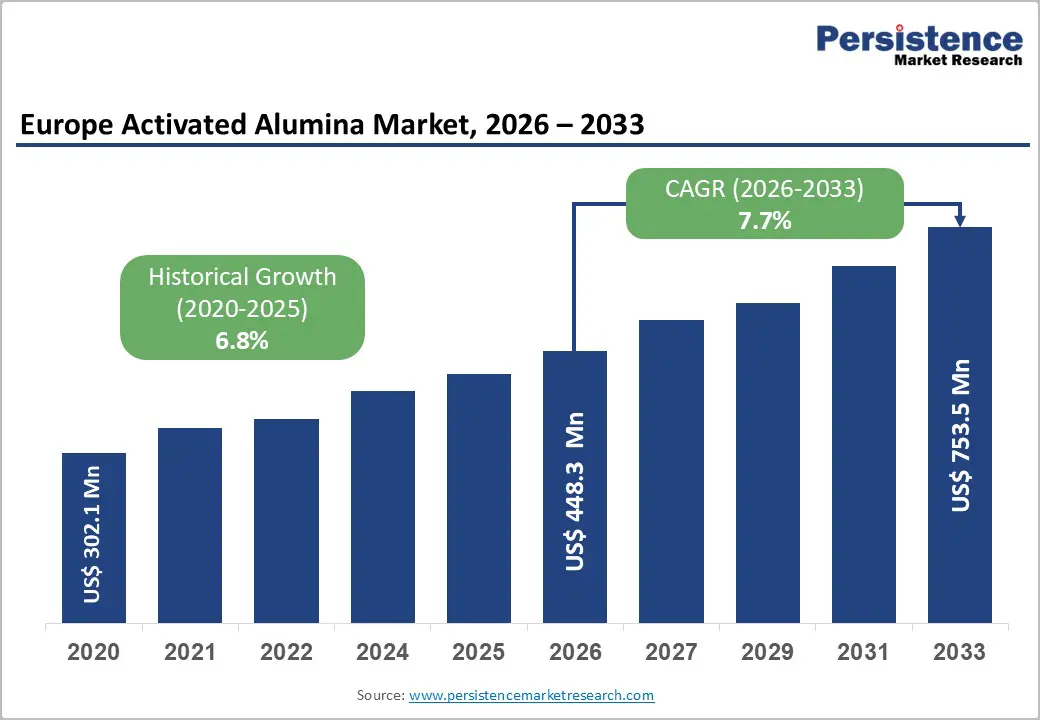

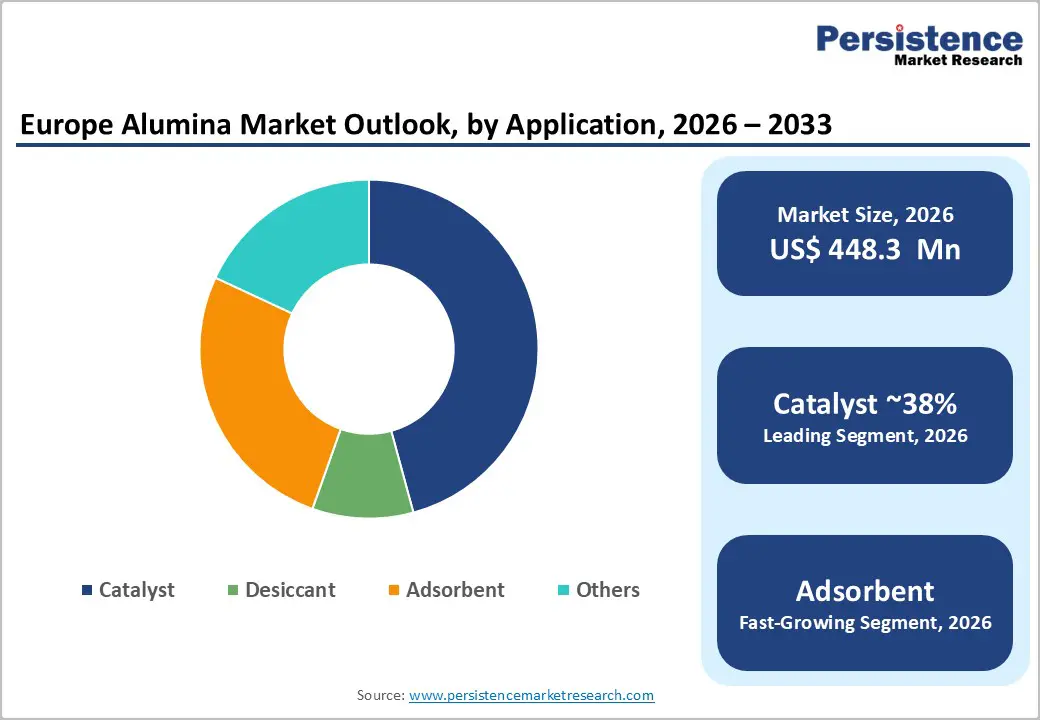

Europe Activated Alumina market size is supposed to be valued at US$ 448.3 Million in 2026 and is projected to reach US$ 753.5 Million by 2033, growing at a CAGR of 7.7% between 2026 and 2033.

The market's robust growth trajectory is fundamentally driven by escalating global demand for advanced water treatment solutions, combined with expanding oil and gas refinery catalyst and desiccant applications, the healthcare sector's growing consumption of pharmaceutical-grade alumina in chromatography and drug delivery systems, and the European Green Deal's regulatory mandates for cleaner industrial process emissions and water quality compliance.

Key Industry Highlights:

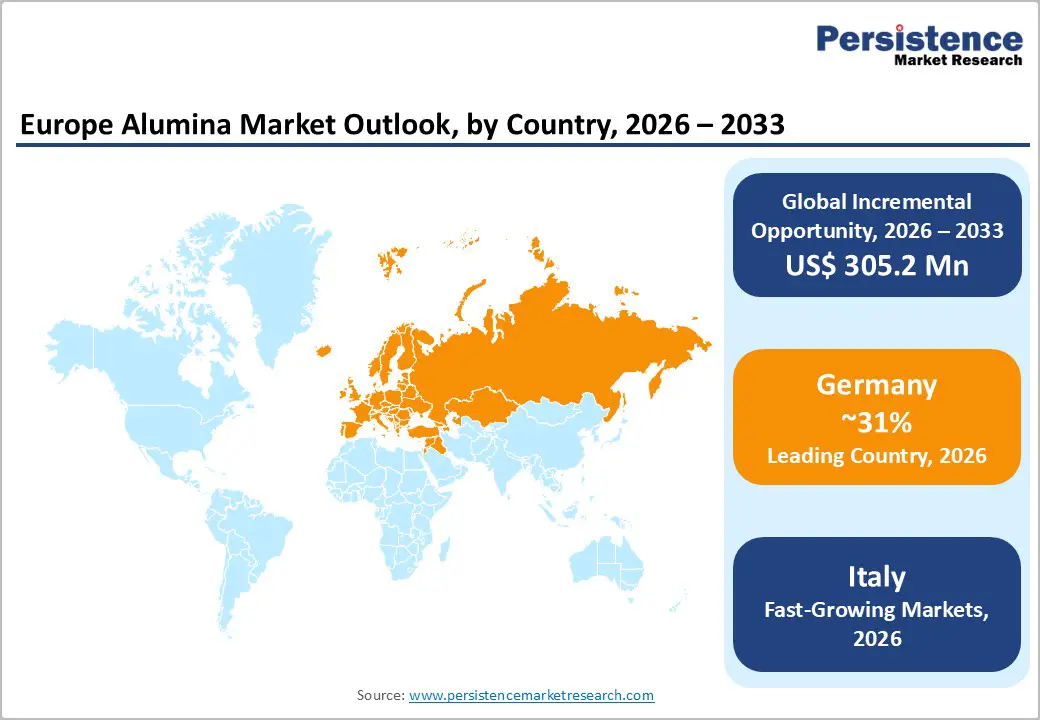

- Leading Country: Germany leads the European Activated Alumina market, anchored by BASF SE's Ludwigshafen world-class catalyst production, Evonik's pharmaceutical-grade alumina leadership, VCI-documented €12 billion annual chemical R&D investment, and the Trinkwasserverordnung (TrinkwV 2023) implementing the EU Drinking Water Directive (EU) 2020/2184 mandating activated alumina fluoride and arsenic removal system deployment across German municipal water utilities.

- Dominant Application: Catalyst dominates the Application segment with approximately 38% revenue share, anchored by activated alumina's technically irreplaceable role as a catalyst carrier in petroleum hydrotreating, Claus sulfur recovery, and hydrogen production SMR reactor units, with Axens' Spheralite® and Honeywell UOP's certified catalyst alumina grades commanding premium refinery industry procurement across global processing installations.

- Fastest Growing End-user: Water Treatment is the fastest-growing End Use segment, propelled by EU Directive (EU) 2020/2184 mandating 1.5 mg/L fluoride and 10 µg/L arsenic maximum contaminant levels, EEA's documented 20%+ of European groundwater bodies failing good chemical status, and WHO's reported 200 million people consuming fluoride-contaminated water globally, generating structurally growing activated alumina adsorbent procurement demand.

- Key Market Opportunity: Pharmaceutical-grade activated alumina and EU Global Gateway-funded emerging market water treatment represent the key market opportunity, with EFPIA's €42 billion European pharma R&D investment driving chromatography and drug delivery alumina demand, and EU Global Gateway and EIB water sector financing funding activated alumina fluoride removal system deployment across Sub-Saharan Africa, South Asia, and Southeast Asia through the forecast period.

| Key Insights | Details |

|---|---|

|

Europe Activated Alumina Market Size (2026E) |

US$ 448.3 Million |

|

Market Value Forecast (2033F) |

US$ 753.5 Million |

|

Projected Growth CAGR (2026–2033) |

7.7% |

|

Historical Market Growth (2020–2025) |

6.8% |

Market Dynamics Analysis

Drivers - Stringent EU Drinking Water Directive and Global Safe Water Access Mandates Driving Activated Alumina Adsorption System Deployment

The comprehensive revision and strengthening of the EU Drinking Water Directive through Directive (EU) 2020/2184, which entered full legal force across all 27 EU member states by January 2023, establishes legally binding maximum contaminant levels for fluoride (1.5 mg/L), arsenic (10 µg/L), and emerging organic micropollutants that are compelling European water utilities and municipal treatment plant operators to invest in certified activated alumina-based adsorption treatment systems as technically validated solutions for achieving regulatory compliance across affected groundwater supply areas. The European Environment Agency (EEA)'s 2022 State of Europe's Water report documented that over 20% of European groundwater bodies fail to meet good chemical status, with fluoride and arsenic contamination particularly prevalent in groundwater sources in Germany, Hungary, Slovakia, Finland, and Italy, creating a regulatory compliance investment imperative that directly stimulates activated alumina procurement for point-of-entry water treatment systems and large-scale municipal adsorption unit upgrades.

Honeywell International Inc.'s UOP division and BASF SE's catalyst and adsorbent product lines serve the European water treatment activated alumina market with certified-performance adsorbent grades, with Honeywell UOP's Sorbead® and alumina-based adsorbent products widely specified in European water treatment plant engineering designs. Huber Engineered Materials (a division of J.M. Huber Corporation) supplies activated alumina for water treatment applications globally, documenting consistent demand growth driven by tightening drinking water quality regulations across both developed and developing market regulatory frameworks.

Hydrogen Economy Expansion and Natural Gas Dehydration Applications Sustaining Industrial Activated Alumina Desiccant Demand

The accelerating development of the European hydrogen economy, anchored by the European Commission's Hydrogen Strategy targeting 10 million tonnes of domestic green hydrogen production and 10 million tonnes of hydrogen imports by 2030 under the REPowerEU Plan, is creating a new and structurally growing activated alumina demand category in hydrogen purification, compression drying, and gas dehydration applications where activated alumina spherical desiccant beds are among the most technically and economically established moisture removal solutions for industrial gas processing systems. Activated alumina desiccant beds are widely deployed in pressure swing adsorption (PSA) and temperature swing adsorption (TSA) dryer systems used across compressed air drying, natural gas dehydration, hydrogen purification, and industrial gas processing applications, with the International Gas Union (IGU) documenting sustained investment in European natural gas pipeline dehydration infrastructure as a co-benefit of the transition to hydrogen-natural gas blending programs.

Axens (a subsidiary of IFP Energies nouvelles, headquartered in Rueil-Malmaison, France), one of the world's leading process catalysts and adsorbents companies, serves the European oil, gas, and hydrogen processing industry with a comprehensive activated alumina product portfolio including the Spheralite® alumina catalyst carrier and specialty desiccant grades designed for natural gas dehydration and hydrogen purification service conditions in European refinery and gas processing installations.

Restraints - Competition from Alternative Adsorbents Including Zeolites, Silica Gel, and Ion Exchange Resins Constraining Activated Alumina Market Share

Activated alumina faces structured competition from alternative industrial adsorbent and desiccant technologies, particularly molecular sieve zeolites (for deep desiccant applications requiring dew points below -40°C), silica gel (for moderate humidity applications with lower regeneration energy requirements), and ion exchange resins (for competing fluoride and arsenic water treatment applications), each of which offers technically competitive performance profiles in specific operating condition ranges that limit activated alumina's addressable market to applications where its unique combination of amphoteric surface chemistry, high surface area (200–350 m²/g), and certified fluoride/arsenic adsorption selectivity provides genuine performance advantages.

The Adsorbents and Desiccants Council and industrial gas processing engineering literature consistently document that zeolite molecular sieves, produced by Honeywell UOP and BASF SE, command premium market positions in natural gas dehydration applications requiring deep dew point specifications that activated alumina alone cannot achieve economically.

Raw Material Dependency on Alumina Hydrate Feedstock Pricing and Bauxite Supply Chain Vulnerability

Activated alumina production is fundamentally dependent on aluminium hydroxide (Al(OH)3 / gibbsite) as the primary precursor feedstock, which is derived from bauxite ore processing through the Bayer Process, creating a direct supply chain linkage to global bauxite mining production, Bayer alumina refinery operating rates, and alumina hydrate commodity pricing that introduces raw material cost volatility into activated alumina production economics.

The International Aluminium Institute (IAI) documents that global bauxite production is geographically concentrated in Guinea (25%), Australia (26%), and China (22%), with European aluminium producers including Aluminium of Greece (Mytilineos Group) and Norsk Hydro ASA dependent on imported bauxite that exposes them to shipping cost volatility and geopolitical supply disruption risks that constrain stable activated alumina feedstock pricing for European producers.

Opportunities - Fluoride Removal from Drinking Water in Emerging Markets and EU-Funded Water Infrastructure Programs

The United Nations Sustainable Development Goal 6 (SDG 6), targeting universal access to safe and affordable drinking water for all by 2030, combined with the World Health Organization (WHO)'s documented finding that approximately 200 million people globally consume groundwater with fluoride concentrations exceeding 1.5 mg/L safe drinking water guidelines, is creating a structurally compelling commercial opportunity for activated alumina adsorbent producers able to supply certified fluoride removal systems to water treatment investment programs in Sub-Saharan Africa, South Asia, and East Africa where high-fluoride groundwater is a widespread public health challenge.

The European Commission's external development financing, through EU Global Gateway infrastructure investment and European Investment Bank (EIB) water sector lending programs, is funding water treatment infrastructure investment in Africa, Southeast Asia, and Latin America that incorporates activated alumina fluoride removal technology specifications aligned with WHO drinking water quality guidelines. Huber Engineered Materials' Alcan™ activated alumina fluoride removal products and Axens' specialty water treatment adsorbents are commercially positioned to serve EU Global Gateway-funded water treatment infrastructure procurement programs in emerging market geographies, creating an internationally scalable revenue opportunity beyond the mature European domestic water treatment market.

Pharmaceutical and Healthcare Sector Activated Alumina Demand Growth Driven by Chromatography and Drug Delivery Applications

The global pharmaceutical industry's accelerating adoption of activated alumina as a stationary phase in chromatographic purification columns, as a catalyst support in pharmaceutical intermediate synthesis, and as a controlled-release excipient platform in oral drug delivery formulations, combined with the EU's pharmaceutical sector investment in domestic active pharmaceutical ingredient (API) manufacturing stimulated by the European Medicines Agency (EMA)'s medicine supply chain resilience initiatives, is creating a premium-priced, high-growth healthcare application segment that provides meaningful revenue diversification and margin enhancement opportunities for activated alumina producers investing in pharmaceutical-grade product quality certifications.

Evonik Industries AG, headquartered in Essen, Germany and operating one of the world's most comprehensive pharmaceutical excipients and specialty alumina product portfolios, is positioned as the European activated alumina market leader for healthcare applications, with its AEROXIDE® and specialty alumina oxide product families serving pharmaceutical chromatography, drug delivery, and medical device application markets. The European Federation of Pharmaceutical Industries and Associations (EFPIA) documented that European pharmaceutical industry R&D investment exceeded €42 billion in 2022, with biosimilar, oncology, and mRNA-based drug manufacturing capacity investment generating growing demand for pharmaceutical-grade alumina chromatography media and process support materials from European API and drug substance manufacturing facilities.

Category-wise Analysis

By Application Insights

Catalyst leads the Europe activated alumina market by application, accounting for approximately 38% of total application segment revenue in 2026, a commercially dominant position anchored in activated alumina's established and technically irreplaceable role as a catalyst carrier, catalyst support, and direct catalyst in a broad range of industrial chemical processing applications spanning petroleum refinery hydrotreating, Claus sulfur recovery processes, hydrogen production via steam methane reforming, and polyolefin polymer catalyst systems. Activated alumina's exceptionally high surface area (200–350 m²/g), amphoteric surface chemistry enabling both acidic and basic catalytic functionalities, thermal stability up to 1,000°C, and mechanical crush strength for fixed-bed reactor packing applications make it the most technically versatile and commercially established catalyst carrier material in industrial heterogeneous catalysis.

Axens' Spheralite® activated alumina catalyst carrier, BASF SE's catalyst alumina product range, and Honeywell UOP's alumina-based catalyst carrier portfolio collectively represent the dominant commercial platforms in the catalyst application segment, each certified to international refinery and petrochemical process industry performance standards. Desiccant holds the second-largest application share at approximately 28%, driven by natural gas dehydration, compressed air drying, and hydrogen processing applications.

By End-user Insights

Oil and Gas leads the Europe Activated Alumina market by end use, commanding approximately 35% of total end-use segment revenue in 2026, reflecting activated alumina's foundational and technically non-substitutable role across multiple critical oil and gas processing unit operations including natural gas dehydration in pipeline transmission systems, petroleum refinery hydrotreating catalyst support, Claus sulfur recovery unit catalyst beds, naphtha reformer catalyst carrier applications, and gas plant molecular sieve and activated alumina dryer unit installations. The International Energy Agency (IEA)'s World Energy Outlook 2024 projects continued global oil and gas processing infrastructure investment through 2030 despite the energy transition, with Middle Eastern, Asian, and European refinery modernization programs generating sustained activated alumina catalyst and desiccant procurement.

Axens and Honeywell UOP are the two dominant Europe activated alumina suppliers to the oil and gas processing industry, each offering comprehensive product portfolios certified to API and international refinery engineering standards with documented performance references at major global refinery installations. Water Treatment holds the second-largest end-use share at approximately 28% of revenue, and is the fastest-growing end-use segment driven by EU Drinking Water Directive (EU) 2020/2184 compliance investment across European municipal water utilities.

Regional Insights

Germany Activated Alumina Market Trends

Germany leads the European Activated Alumina market, anchored by its concentration of world-class chemical processing, refinery operations, and pharmaceutical manufacturing industries that collectively constitute one of Europe's largest industrial consumers of activated alumina across catalyst, desiccant, and adsorbent application categories. BASF SE (headquartered in Ludwigshafen, Germany), the world's largest chemical company by revenue, operates one of the world's most comprehensive catalyst and adsorbent product portfolios including activated alumina catalyst carriers and support materials serving European and global refinery and petrochemical processing customers, reinforcing Germany's position as the most production-significant and technically influential activated alumina supplier geography in Europe. Evonik Industries AG (headquartered in Essen, Germany) contributes premium pharmaceutical-grade and specialty activated alumina product lines serving chromatography, pharmaceutical excipient, and specialty catalyst applications.

Germany's water treatment sector, regulated by the Trinkwasserverordnung (TrinkwV 2023) (German Drinking Water Ordinance) implementing EU Directive (EU) 2020/2184 into national law, mandates fluoride and arsenic maximum contaminant levels consistent with EU and WHO safe drinking water standards, sustaining institutional water utility procurement of activated alumina adsorption systems for compliant drinking water treatment in fluoride-affected groundwater supply areas including parts of Bavaria, Hesse, and Saxony. The German Chemical Industry Association (VCI)'s documented €12 billion+ annual chemical sector R&D investment sustains continuous innovation in activated alumina surface chemistry modification, particle size engineering, and regeneration performance optimization that maintains Germany's competitive advantage in next-generation activated alumina product development.

Italy Activated Alumina Market Trends

Italy is a commercially active European Activated Alumina market, driven by its substantial refinery and petrochemical processing infrastructure concentrated in Sicily (Milazzo, Gela), Sardinia (Sarroch), and the Po Valley industrial corridor, where activated alumina catalyst carrier and desiccant procurement is sustained by ENI S.p.A.'s refinery network, Italy's largest oil and gas company, which operates multiple Italian refinery processing units consuming activated alumina in hydrotreating catalyst beds, Claus unit catalysts, and gas dehydration dryer installations. ENI's strategic commitment to its Enilive biofuel and circular economy refining programs, which are converting Italian conventional refineries to biorefinery operations processing waste-based lipid feedstocks, is generating new activated alumina catalyst procurement requirements for bio-based hydroprocessed renewable fuel (HVO) hydrotreatment reactor unit catalyst systems.

Italy's water treatment sector, regulated by Decreto Legislativo n. 18/2023 implementing EU Directive (EU) 2020/2184 into Italian national law, is accelerating municipal water utility investment in advanced adsorption treatment systems. The Istituto Superiore di Sanità (ISS) has documented arsenic groundwater contamination challenges in Lazio, Tuscany, and Latium regions that mandate activated alumina adsorbent system installation in affected water supply networks to achieve compliant arsenic levels below 10 µg/L. Petrosadid, an international activated alumina and molecular sieve supplier, and Sumitomo Chemical Co., Ltd.'s European distribution network serve Italian industrial and water treatment activated alumina customers through established distributor and direct sales channels across Northern and Southern Italian industrial procurement geographies.

France Activated Alumina Trends

France is a strategically important European Activated Alumina market, anchored by Axens (a subsidiary of IFP Energies nouvelles, headquartered in Rueil-Malmaison, France), one of the world's most technically authoritative activated alumina technology companies, serving global refinery, gas processing, and petrochemical industry customers with its premium Spheralite® activated alumina catalyst carrier and specialty desiccant product portfolio developed through IFP Energies nouvelles' world-leading petroleum and chemical process research programs. TotalEnergies SE (headquartered in Courbevoie, France), one of Europe's largest integrated energy companies, operates French and European refinery processing units consuming activated alumina as catalyst carriers in hydrodesulfurization and hydrogen production units aligned with EU fuel quality standards. Air Liquide (headquartered in Paris, France), the world's largest industrial gas company, consumes activated alumina desiccant in its compressed industrial gas drying systems globally, with French operations sustaining domestic activated alumina procurement.

France's pharmaceutical industry, anchored by Sanofi (headquartered in Paris) and Pierre Fabre, sustains a growing pharmaceutical-grade activated alumina demand base for chromatographic purification of biopharmaceutical drug substances, vaccine adjuvant formulations incorporating aluminium hydroxide chemistry, and pharmaceutical process catalyst applications. The European Medicines Agency (EMA)'s medicine supply chain resilience initiatives, including the Critical Medicines Alliance framework prioritizing domestic European API manufacturing investment, are stimulating French pharmaceutical R&D and manufacturing capacity investment that drives growing pharmaceutical-grade activated alumina procurement.

France's Ministère de la Transition Écologique's national water quality improvement programs, addressing arsenic and fluoride contamination in affected regional water supply systems, are sustaining municipal water treatment activated alumina procurement with institutional investment support from Agence Française de Développement (AFD) water infrastructure financing programs.

Competitive Landscape

Europe Activated Alumina market is moderately consolidated at the high-performance product tier, with Axens, BASF SE, Honeywell UOP, and Evonik Industries AG commanding leading positions through proprietary activated alumina formulation technologies, extensive refinery and petrochemical industry customer references, and vertically integrated quality management systems certified to ISO 9001 and ASTM performance standards. Huber Engineered Materials and Sumitomo Chemical compete through specialized water treatment and pharmaceutical application grade portfolios. CHALCO Shandong Co., Ltd. leads in volume-driven cost-competitive standard grades serving Asian and commodity markets.

Emerging trends include surface-functionalized activated alumina with enhanced selectivity for emerging contaminants, regenerable fluoride/arsenic adsorbent systems with extended service life economics, and pharmaceutical excipient-grade activated alumina certified to USP/EP pharmacopoeial standards targeting the growing biopharmaceutical purification market.

Key Developments:

- In January 2025, Axens announced a strategic technology licensing agreement for its next-generation activated alumina-based Claus sulfur recovery catalyst system, targeting expanding Middle Eastern and Asian refinery sulfur management compliance requirements under progressively tightening sulfur content regulations for refined petroleum products in export market destinations.

- In September 2024, BASF SE expanded its Ludwigshafen catalyst and adsorbent production capabilities with the introduction of a new series of high-surface-area activated alumina catalyst carrier grades, featuring enhanced pore volume distribution and improved hydrothermal stability for application in green hydrogen production steam methane reforming and renewable fuel hydroprocessing reactor systems.

- In April 2024, Honeywell International Inc. announced expansion of its UOP Sorbead® adsorbent product line, incorporating advanced activated alumina formulations targeting the rapidly growing hydrogen economy gas drying application segment, aligning with European REPowerEU hydrogen infrastructure development programs and industrial gas processing customer demand for certified high-performance desiccant solutions.

Companies Covered in Europe Activated Alumina Market

- Axens

- BASF SE

- CHALCO Shandong Co. Ltd.

- Evonik Industries AG

- Honeywell International Inc.

- Huber Engineered Materials

- Petrosadid

- Sumitomo Chemical Co. Ltd.

Frequently Asked Questions

Europe Activated Alumina market is estimated to be valued at US$ 448.3 Million in 2026 and is projected to reach US$ 753.5 Million by 2033, registering a forecast CAGR of 7.7% from 2026 to 2033. The market recorded a historical CAGR of 6.8% between 2020 and 2025, driven by EU Drinking Water Directive (EU) 2020/2184 compliance investment, industrial catalyst and desiccant demand growth, and pharmaceutical-grade activated alumina procurement expansion across European healthcare manufacturing.

The primary drivers are EU Directive (EU) 2020/2184 mandating 1.5 mg/L fluoride and 10 µg/L arsenic maximum contaminant levels compelling water utility activated alumina adsorption system investment, documented by the EEA as required for 20%+ of European groundwater bodies, and the European Commission's Hydrogen Strategy targeting 10 million tonnes of green hydrogen production by 2030 under REPowerEU, generating new activated alumina desiccant demand in hydrogen purification and gas dehydration processing systems.

Catalyst leads the Application segment with approximately 38% revenue share in 2026, anchored by activated alumina's technically irreplaceable role as a catalyst carrier in petroleum hydrotreating, Claus sulfur recovery, and hydrogen production SMR reactor applications, with the IEA's continued global refinery investment projections sustaining large-scale industrial procurement. Axens' Spheralite® catalyst alumina and Honeywell UOP's certified alumina catalyst carrier grades represent the leading commercial platforms in this dominant application segment.

Germany leads the European Activated Alumina market, anchored by BASF SE's world-class Ludwigshafen catalyst and adsorbent production, Evonik Industries AG's pharmaceutical-grade alumina leadership in Essen, the VCI's documented €12 billion annual German chemical sector R&D investment, and the Trinkwasserverordnung (TrinkwV 2023) mandating activated alumina fluoride and arsenic removal system deployment across German municipal water supply networks serving fluoride-affected groundwater areas.

Significant opportunities are pharmaceutical-grade activated alumina for chromatography and drug delivery, with EFPIA's €42 billion European pharma R&D investment driving demand from Evonik's AEROXIDE® and specialty alumina platforms, and EU Global Gateway and EIB-funded emerging market water treatment programs deploying fluoride removal systems for WHO-reported 200 million people consuming fluoride-contaminated groundwater across Sub-Saharan Africa, South Asia, and Southeast Asia through the forecast period.