- Healthcare Services

- Alcohol Addiction Market

Alcohol Addiction Market Size, Share, and Growth Forecast, 2026 – 2033

Alcohol Addiction Market by Treatment Type (Psychotherapy, Pharmacotherapy, Multidisciplinary), Patient Type (Male, Female), Form (Disorder, Addiction), and Regional Analysis 2026 – 2033

Alcohol Addiction Market Size and Trends Analysis

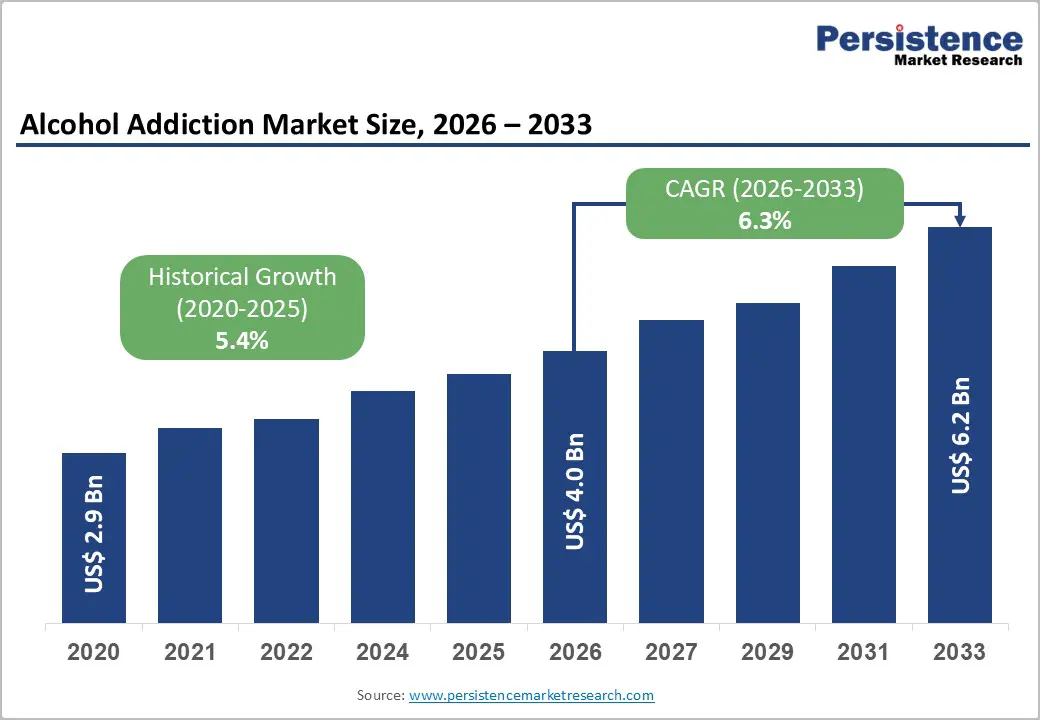

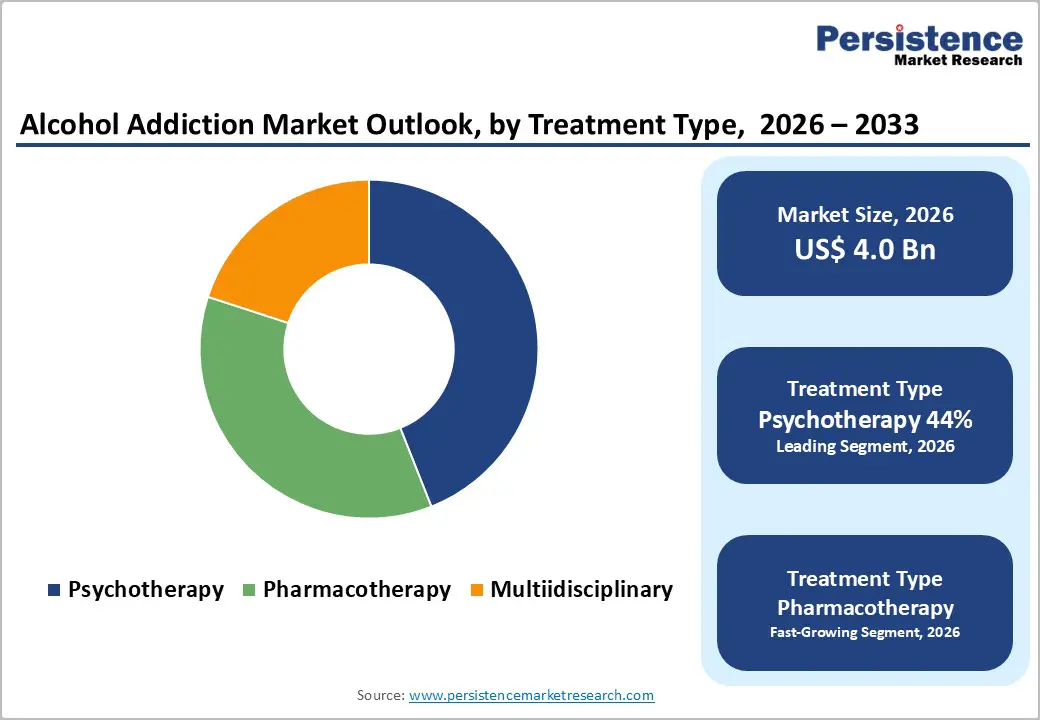

The global alcohol addiction market size is likely to be valued at US$4.0 billion in 2026 and is expected to reach US$6.2 billion by 2033, growing at a CAGR of 6.3% during the forecast period from 2026 to 2033, driven by advancements in pharmacotherapy and psychotherapy, which improve access to treatment. Demographic changes, such as a rise in female diagnoses, are also contributing to the increased demand. The expansion of government funding for rehabilitation programs and the integration of digital therapeutics and telemedicine into mainstream care models further accelerate market growth.

Key Industry Highlights:

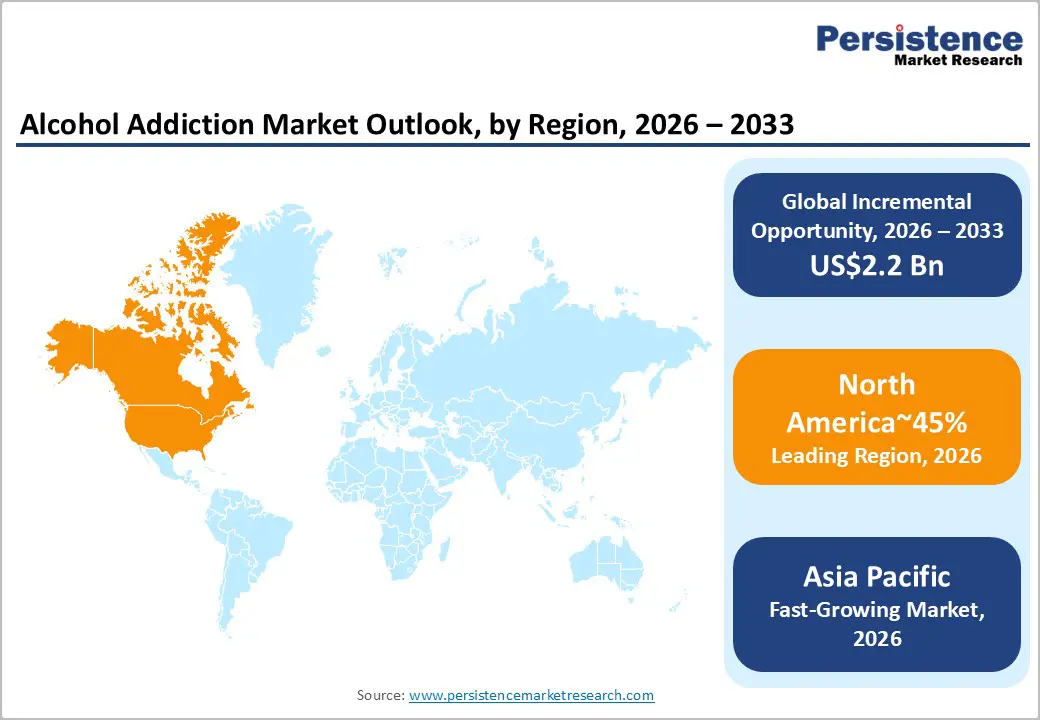

- Leading Region: North America is expected to lead with around 45% share, supported by advanced treatment infrastructure, high diagnosis and reporting rates, strong reimbursement frameworks, and early adoption of pharmacotherapy-based interventions.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by rising alcohol consumption patterns, expanding public health awareness programs, improving access to addiction treatment services, and increasing government focus on mental health and substance abuse management.

- Leading Treatment Type: The psychotherapy and behavioral therapy segment is expected to lead with approximately 44% share, supported by strong patient preference for non-invasive interventions, broad clinical acceptance, and widespread integration into outpatient and inpatient care pathways.

- Leading Patient Type: Male patients are expected to account for around 70% market share, reflecting higher diagnosis rates, greater historical prevalence of alcohol use disorders, and higher clinical reporting across hospital and rehabilitation settings.

| Key Insights | Details |

|---|---|

| Alcohol Addiction Market Size (2026E) | US$4.0 Bn |

| Market Value Forecast (2033F) | US$6.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Government Initiatives and Funding

The government’s reclassification of addiction as a chronic public health condition is structurally expanding the treatment market by integrating care within formal healthcare financing and policy frameworks. This shift has led to increased public-sector prioritization of substance use disorders, resulting in scaled funding for prevention, outpatient programs, and long-term recovery infrastructure. Addiction services are now embedded in national health strategies, with expanded reimbursement eligibility and coverage mandates reducing access barriers and normalizing treatment use across insured populations. This policy change also strengthens institutional accountability for care quality, data reporting, and outcome measurement, boosting compliance across providers.

From a market-structure perspective, sustained public funding is creating a predictable revenue base, reducing the risk associated with capacity expansion and supporting long-term investment in treatment infrastructure and digital platforms. Standardized reimbursement pathways across public payers are reducing demand volatility, while the recognition of addiction as a chronic condition is extending patient engagement and increasing the intensity of long-term care. Together, these dynamics are shifting addiction treatment from episodic care to a managed-care model with consistent funding. In April 2025, Rosecrance merged with North Central Behavioral Health Systems in Illinois, enhancing access to AUD treatment and reducing regional barriers.

Technological Advancements in Treatment

Technological advances in addiction treatment are structurally reconfiguring care delivery by shifting clinical pathways toward pharmacotherapy-supported, digitally mediated models. Medication-assisted interventions are reinforcing clinical efficacy by stabilizing craving control and relapse management, while evolving clinical frameworks that move beyond strict abstinence paradigms are broadening eligibility for sustained engagement. Parallel diffusion of telehealth platforms is embedding remote intake, counseling, and follow-up into routine care pathways, materially reducing access friction across geographies with constrained provider density. AI-enabled triage and decision support are further tightening care coordination, improving treatment matching, and strengthening continuity across multi-episode recovery pathways.

From a market-structure perspective, digitalization and precision-oriented therapeutics are increasing content intensity per patient episode, shifting value capture toward integrated care platforms that combine diagnostics, pharmacotherapy management, and longitudinal monitoring. Remote delivery models are compressing unit service costs while expanding addressable demand in underserved regions, reinforcing utilization elasticity without proportionate physical capacity expansion. Regulatory accommodation of flexible treatment endpoints is extending engagement horizons and stabilizing payer reimbursement exposure, while data-driven care models are elevating compliance and outcomes accountability, reshaping provider economics toward higher-acuity, technology-enabled care delivery.

Barrier Analysis – High Cost and Insurance Barriers

The cost structure of comprehensive addiction treatment continues to impose a structural ceiling on market penetration, as coverage limitations across public and private insurance schemes sustain elevated out-of-pocket exposure for large patient cohorts. Incomplete reimbursement for pharmacotherapy, residential care, and extended behavioral interventions constrains sustained engagement, particularly in price-sensitive populations and under-resourced care settings. The capital intensity of advanced therapeutic regimens and long-duration care pathways further amplifies financial friction, reinforcing discontinuation risk and limiting the effective conversion of diagnosed demand into treated volume. These affordability constraints weaken the transmission of clinical innovation into realized utilization at scale.

From a market-impact perspective, high relapse incidence extends total cost of care across multi-episode treatment cycles, increasing payer sensitivity to long-horizon reimbursement commitments and compressing provider margins in cost-containment environments. The resulting mismatch between therapeutic intensity and coverage adequacy dampens volume scalability in emerging and underinsured markets, where payment elasticity remains acute. Collectively, insurance fragmentation, high lifetime treatment costs, and discontinuous care pathways structurally moderate revenue realization, reinforcing affordability as a binding constraint on sustainable market expansion despite rising clinical need.

OpportunityAnalysis – Digital Therapeutics and Remote Monitoring

Digital therapeutics and remote monitoring are emerging as structurally material opportunity layers within addiction care delivery, enabled by regulatory validation of software-based interventions as reimbursable therapeutic modalities. Prescription digital therapeutics are extending clinically supervised care into low-acuity and early-intervention settings, where conventional facility-based models exhibit high access friction and cost intensity. The scalability of software-mediated behavioral therapy, craving management, and adherence support is reshaping service economics by decoupling patient reach from physical capacity constraints, while embedding continuous engagement mechanisms across pre-clinical and maintenance phases of care.

From a market-structure standpoint, digitally delivered interventions expand the addressable population by formalizing treatment pathways for cohorts historically excluded from inpatient or intensive outpatient programs. There is a significant actionable opportunity in FDA-cleared prescription digital therapeutics (PDTs). These software-based treatments can be scaled with near-zero marginal cost compared to physical clinics. Integration of remote monitoring and data-driven behavioral feedback loops strengthens continuity across stepped-care models, reinforcing longitudinal engagement without proportionate infrastructure expansion. Regulatory clearance of digital modalities is also recalibrating reimbursement frameworks and compliance requirements, positioning technology-enabled care layers as complementary revenue streams that reinforce value-chain depth and utilization density across the addiction treatment continuum.

Personalized Medicine & Genetic Biomarkers

The transition from uniform treatment protocols toward precision-oriented addiction care is reconfiguring therapeutic design around genetic and neurobiological stratification. Biomarker-informed patient segmentation is improving clinical matching across pharmacological and behavioral interventions, reducing reliance on empiric sequencing and lowering attrition associated with prolonged trial-and-error cycles. Integration of companion diagnostics into treatment pathways is elevating evidence thresholds and reinforcing the role of data governance, assay validation, and clinical pathway standardization within regulated care environments. This shift is also aligning treatment architecture with outcome-linked accountability frameworks, increasing the relevance of longitudinal response tracking within managed-care models.

From a market-structure perspective, precision medicine is increasing development complexity and regulatory engagement, extending commercialization timelines while raising per-patient value capture through higher-acuity, targeted interventions. The requirement for diagnostic-therapeutic co-validation is reinforcing compliance intensity across the value chain, favoring operators with integrated clinical development, regulatory affairs, and real-world evidence capabilities. As personalized modalities mature, differentiation is increasingly anchored in biomarker integration depth and pathway interoperability rather than scale of physical delivery networks alone.

Category-wise Analysis

Treatment Type Insights

Psychotherapy is expected to lead the Alcohol Addiction market, accounting for approximately 44% share, underpinned by its entrenched role in first-line care across outpatient clinics, residential programs, employer EAPs, and public health settings. Adoption remains anchored by non-invasive delivery, dual-diagnosis coverage for co-occurring depression and anxiety, and strong retention in CBT-led programs, with providers prioritizing continuity of care and workflow integration in high-volume treatment environments. Ongoing platform evolution, including AI-supported clinical decision tools, teletherapy at scale, VR-assisted exposure modules, and measurement-based care using wearables, is reinforcing utilization intensity and repeat engagement. Vendors such as Hazelden Betty Ford Foundation, American Addiction Centers, and Lyra Health are expanding hybrid care models and enterprise platforms to lock in referral pathways and long-term payer contracts.

Pharmacotherapy is projected to be the fastest-growing segment within the Alcohol Addiction market, driven by unmet needs around adherence, relapse prevention, and scalability in primary care settings. Growth is being catalyzed by long-acting injectables and implants, precision-medicine approaches informed by genomics, and repurposed metabolic agents that materially improve craving control and treatment persistence. Companies including Alkermes, Adial Pharmaceuticals, and BioCorRx are scaling injectable, genotype-targeted, and implantable platforms to capture early-cycle demand and embed switching costs across clinic networks. As regulatory fast-track pathways mature and clinical validation broadens, this segment is expected to outpace overall market growth over the forecast period.

Patient Insights

The male patient segment dominates the alcohol addiction market, holding around 70% of the share, driven by demand in employer-funded programs, court-mandated diversion pathways, and veteran care networks. Clinical development has increasingly focused on male-centric precision enrollment, addressing serotonin- and dopamine-mediated craving profiles. Workplace screenings in male-dominated sectors are shifting from punitive measures to sponsored pharmacotherapy and brief interventions. Treatment for this group skews toward intensive inpatient and structured outpatient pathways, increasing revenue density. Providers have adapted by offering gender-specific tracks, strength-based psychotherapy, and hybrid models that combine facility care with digital follow-ups. The growth of executive rehabilitation and men-only programs is further boosting referral capture and payer alignment, while anonymous digital peer groups enhance engagement by reducing access friction. These factors maintain predictable inflow and high-acuity cases, ensuring continued leadership for the male segment.

The female patient segment is the fastest-growing, fueled by accelerating disease progression, rising high-intensity drinking among professionals, and the rapid adoption of telehealth, which accommodates caregiving responsibilities. Regulatory emphasis on gender stratification and maternal health screening is expanding early detection, while trauma-informed care is directing funding toward specialized psychiatric services. Providers are scaling women-only facilities and developing cycle-aware protocols, complemented by holistic and discreet digital care options to reduce stigma. Pharmaceutical offerings now emphasize anxiolytic benefits aligned with coping-driven use. The "sober curious" trend is increasing screening and referrals, accelerating treatment initiation. Despite being smaller than the male cohort, these dynamics are expected to sustain growth rates above the market average.

Regional Insights

North America Alcohol Addiction Market Trends

North America is expected to lead the alcohol addiction market with roughly 45% share in 2026, anchored in a highly monetized care ecosystem where addiction medicine is institutionalized as a chronic condition. Market depth is reinforced by rapid clinical adoption, payer coverage parity, and the reuse of opioid-response infrastructure to scale alcohol-focused pathways. Long-acting injectables are gaining procedural share as clinics expand cold-chain capacity, while continuous alcohol monitoring wearables are being integrated into provider dashboards to support relapse prevention and compliance workflows. Provider delivery models are shifting toward hybrid care, combining facility-based stabilization with telehealth-enabled continuity. High per-patient spend in residential and structured outpatient care continues to inflate regional value relative to state-funded systems elsewhere.

The regulatory environment supports rapid diffusion of pharmacotherapy and digital-first pathways, with expanded prescriptive access in primary care and sustained telehealth flexibilities maintaining market throughput. Vivitrol remains a cornerstone of long-acting pharmacotherapy utilization, while provider networks such as Hazelden Betty Ford and American Addiction Centers shape clinical standards and referral capture across inpatient and continuum-of-care models. Precision-medicine development activity led by Adial Pharmaceuticals reflects the region’s early-mover posture in targeted therapeutics. Together, these dynamics underpin North America’s durable leadership through infrastructure maturity, payer alignment, and accelerated technology adoption.

Europe Alcohol Addiction Market Trends

Europe is positioned as a structurally mature but policy-intensive market for alcohol use disorder management, shaped by public health system dominance, harm-reduction treatment philosophies, and deep integration of digital therapeutics into formal care pathways. Adoption of reimbursable digital therapeutics such as Vorvida is projected to normalize hybrid care models that combine behavioral therapy with pharmacological support, while the harm-reduction orientation is expected to sustain demand for reduction-focused therapies such as Selincro alongside established options from Ethypharm and Indivior. The region’s care delivery model is likely to emphasize high patient throughput and standardized pathways, reinforcing volume-led utilization across public systems rather than high per-patient monetization.

Growth momentum is expected to be supported by the gradual expansion of early screening funnels, digital engagement channels, and outsourced care delivery, with the UK and Germany likely to remain reference markets for blended public–private service models. Private operators such as the Priory Group are projected to deepen their role in long-term behavioral care, complementing hospital-based pathways and community services. The market is likely to see broader use of AI-enabled screening within primary care and population health programs, improving identification of heavy episodic drinking patterns and channeling patients into formal treatment. Overall, Europe is likely to sustain steady, system-led expansion driven by policy alignment, digital integration, and the normalization of reduction-oriented treatment paradigms.

Asia Pacific Alcohol Addiction Market Trends

Asia Pacific is expected to be the fastest-growing region for alcohol use disorder treatment, driven by the formalization of care delivery in large, historically underserved populations and the growing presence of multinational healthcare and wellness companies in emerging markets. Market expansion will be supported by the increasing availability of generic pharmacotherapies from regional manufacturers such as Cipla and Sun Pharma. Diversified conglomerates such as Asahi Group and Suntory are shifting their portfolios toward moderation, wellness, and recovery-oriented services. The rise of digital therapeutics and local-language treatment platforms is anticipated to scale in urban and peri-urban areas, particularly as digitally advanced provider networks integrate AI-enabled screening and remote counseling into primary care.

China and India are poised to lead regional growth as healthcare systems expand mental health capacities and private operators build specialty clinic networks in tier-two and tier-three cities. Cross-border care models, such as medical tourism hubs such as Siam Rehab, will gain prominence. The region’s treatment ecosystem will deepen with the integration of herbal and adjunct recovery solutions from brands such as The Himalaya Drug Company, alongside evidence-based pharmacotherapy, creating a hybrid care model tailored to local needs. Overall, Asia Pacific is set to sustain its rapid growth through expanded provider capacity, localized digital health solutions, and increased involvement from major pharmaceutical and wellness brands.

Competitive Landscape

The market is moderately fragmented, with leadership concentrated among pharmacotherapy specialists such as Alkermes and Indivior, alongside large behavioral health chains that dominate residential treatment networks. These players matter because branded therapies, clinical relationships, and payer access shape treatment pathways and referral flow across care settings. At the product layer, leaders compete on innovation, differentiated formulations, and evidence-backed outcomes, while services emphasize network expansion, standardized protocols, and payer integration. Industry behavior points toward continued clinic roll-ups, platform building, and tighter drug-service alignment, signaling rising consolidation alongside persistent fragmentation in localized care markets.

Key Industry Highlights

- In January 2026, Adial published an international PCT patent for AD04, extending IP until 2045. This secures long-term exclusivity for genetically targeted AUD therapy, attracting investment for Phase 3 trials and solidifying its foundation in Precision Medicine.

- In December 2025, Clearmind Medicine completed the second cohort of its CMND-100 Phase I/IIa clinical trial. The non-hallucinogenic MEAI compound showed critical safety data, positioning it as a scalable, outpatient-friendly treatment bridging traditional medicine and psychedelic therapy.

- In November 2025, Oar Health launched Clutch, a fast-acting naltrexone mint for AUD. This discreet, quick-dissolving mint targets cravings and improves adherence, offering a convenient alternative to pills and potentially reducing binge drinking rates.

- In March 2025, Tempero Bio secured USD 70 million in Series B funding for TMP-301 Phase II trials. This breakthrough targets the glutamate system, addressing chronic stress and habit loops in alcohol and cocaine use disorders, advancing crucial pharmacological interventions.

Companies Covered in Alcohol Addiction Market

- Alkermes PLC

- Indivior PLC

- Omeros Corporation

- Adial Pharmaceuticals, Inc.

- BioXcel Therapeutics

- BioCorRx Inc.

- Addex Therapeutics

- Orexo AB

- Merck & Co., Inc.

- Lundbeck

- Teva Pharmaceutical Industries Ltd.

- Viatris Inc.

- Sun Pharmaceutical Industries Ltd.

- Acadia Healthcare

- Universal Health Services, Inc.

- Zydus Pharmaceuticals

Frequently Asked Questions

The global alcohol addiction market is projected to be valued at US$4.0 billion in 2026 and is expected to reach US$6.2 billion by 2033, driven by government funding, technological advancements, and greater access to pharmacotherapy and psychotherapy.

Reclassifying addiction as a chronic public health condition has boosted government funding, integrated treatment into healthcare systems, lowered access barriers, and provided a stable revenue stream for care providers, fueling market growth.

The alcohol addiction market is forecast to grow at a CAGR of 6.3% from 2026 to 2033, reflecting the impact of technological integration, demographic shifts, and increasing public health prioritization.

North America is expected to lead, accounting for approximately 45% share in 2026, supported by advanced treatment infrastructure, high diagnosis rates, strong reimbursement systems, and early adoption of innovative pharmacotherapies.

The alcohol addiction market is moderately fragmented, with leaders such as Alkermes, Indivior, Hazelden Betty Ford, and American Addiction Centers. They compete through innovative drug formulations, vast clinical networks, and integrated care models.