- Specialty & Fine Chemicals

- Isononyl Alcohol Market

Isononyl Alcohol Market Size, Share, and Growth Forecast 2026 - 2033

Isononyl Alcohol Market by Production Process (C4 Chemicals Process, ExxonMobil Process, Others), Application (Plasticizers: Di-isononyl Phthalate (DINP), Di-isononyl Cyclohexanoate (DINCH), Di-isononyl Adipate (DINA), Tri-isononyl Trimellitate (TINTM), Others; Surfactants & Detergents, Lubricants & Greases, Solvents, Others), by Regional Analysis, 2026 - 2033

Isononyl Alcohol Market Size and Trend Analysis

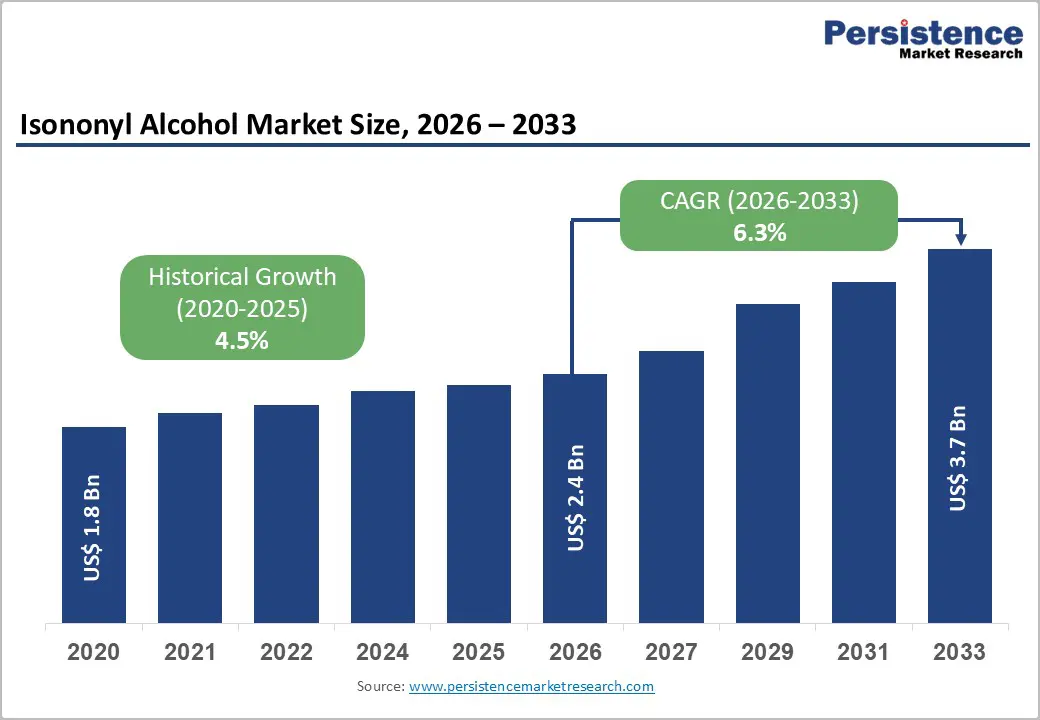

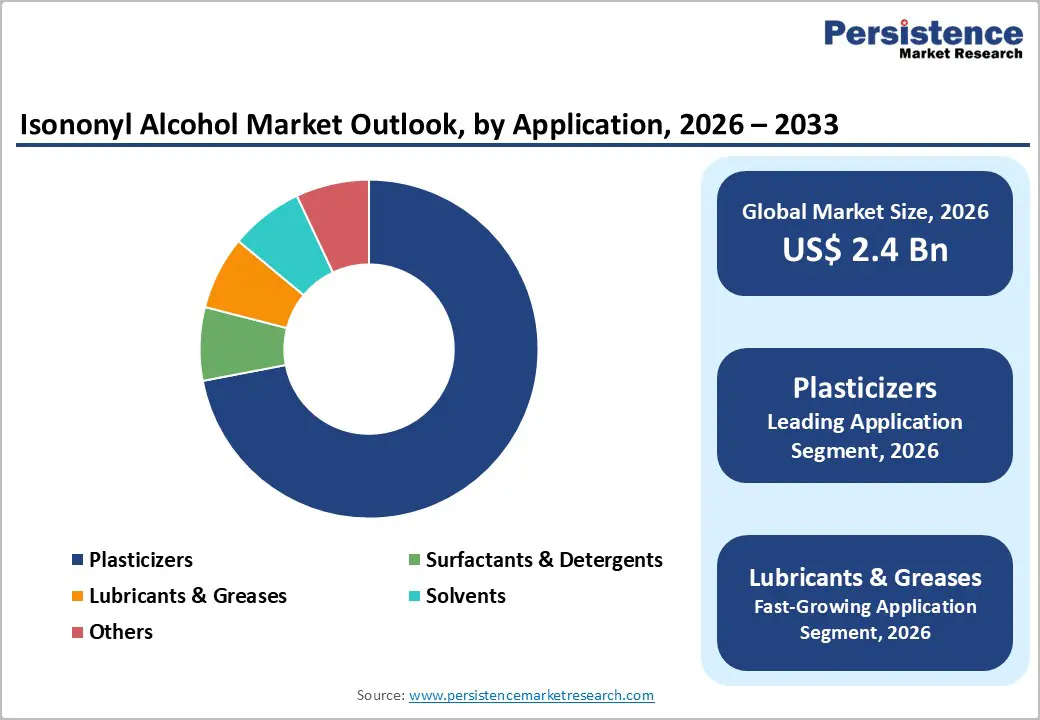

The global isononyl alcohol market size is expected to be valued at US$ 2.4 billion in 2026 and projected to reach US$ 3.7 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

The isononyl alcohol market is poised for sustained growth, primarily driven by escalating demand for non-phthalate and low-toxicity plasticizers across the global PVC and flexible polymer industry. As regulators worldwide restrict legacy phthalate plasticizers, isononyl alcohol, the key feedstock for Di-isononyl Cyclohexanoate (DINCH) and DINP, is experiencing structurally higher demand. Simultaneously, expanding automotive, construction, and consumer goods manufacturing in Asia Pacific, particularly in China and India, is amplifying consumption across plasticizer, lubricant, and solvent application segments.

Key Industry Highlights

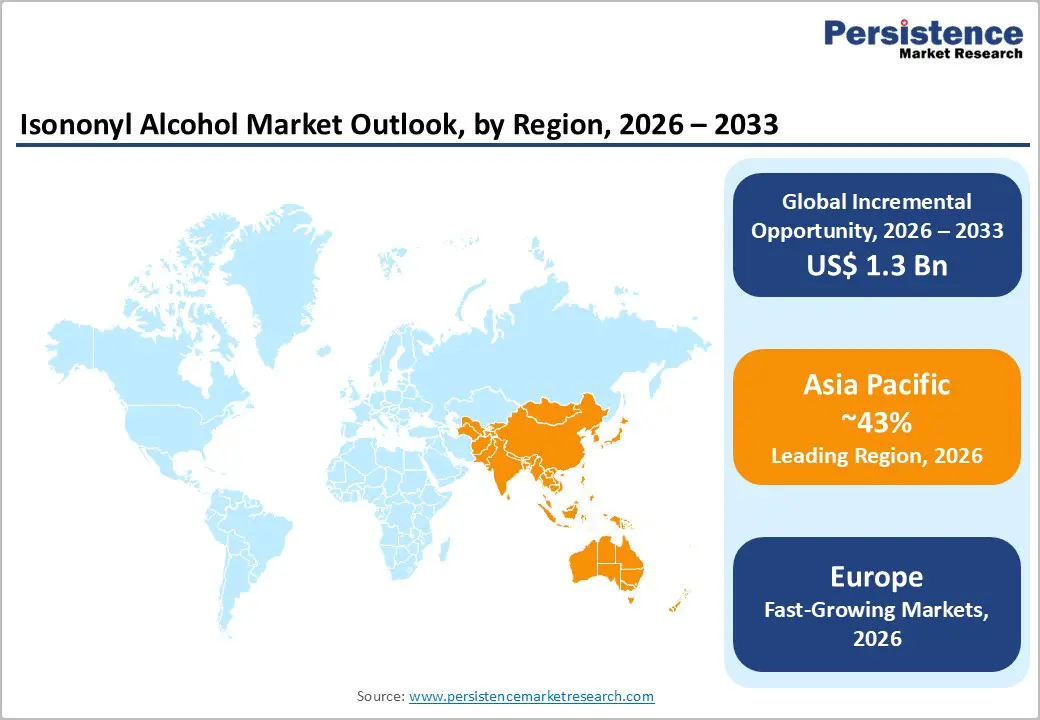

- Leading Region: Asia Pacific dominates the global isononyl alcohol market with approximately 43% share in 2025, anchored by China's position as the world's largest PVC producer with capacity exceeding 30 million tonnes annually and strong C4 chemicals-based production infrastructure.

- Fastest Growing Region: Europe is set to record the highest CAGR of 6.8% through 2033, driven by the EU REACH phthalate restrictions from September 2023 accelerating conversion to DINP and DINCH plasticizers derived from isononyl alcohol across Germany, France, and the U.K.

- Dominant Segment: Plasticizers account for approximately 72% market share in 2025, led by DINP's widespread use in flexible PVC for cables, flooring, and automotive components globally, underpinned by its regulatory clearance from ECHA following comprehensive risk assessment.

- Fastest Growing Segment: DINCH-grade isononyl alcohol demand is projected to grow at the fastest rate through 2033, driven by FDA and EFSA approvals for food-contact and medical device applications and the escalating regulatory shift away from phthalate-based plasticizers across North America and Europe.

- Key Market Opportunity: The EV transition creating demand for isononyl alcohol-derived synthetic esters, combined with the expanding FDA/EFSA-approved DINCH application base in medical devices, represents a dual high-margin specialty opportunity for producers investing in certified, application-specific isononyl alcohol grades.

| Key Insights | Details |

|---|---|

| Isononyl Alcohol Market Size (2026E) | US$ 2.4 Billion |

| Market Value Forecast (2033F) | US$ 3.7 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.3% |

| Historical Market Growth (2020 - 2025) | 4.5% |

Market Dynamics

Market Growth Drivers

Accelerating Regulatory Shift Away from Phthalate Plasticizers Toward Safer Alternatives

The global regulatory transition away from traditional phthalate plasticizers is one of the most consequential structural growth drivers for the isononyl alcohol market. The European Chemicals Agency (ECHA) has included di(2-ethylhexyl) phthalate (DEHP), dibutyl phthalate (DBP), and diisobutyl phthalate (DIBP) under REACH Regulation (EC) No 1907/2006 Annex XIV as substances of very high concern (SVHCs), restricting their use across the European Union. The U.S. Consumer Product Safety Improvement Act (CPSIA) permanently banned certain phthalates in children's products at concentrations above 0.1%. These restrictions are systematically redirecting compounders, film manufacturers, and cable producers toward DINP and DINCH, both derivatives of isononyl alcohol, driving a sustained uptick in isononyl alcohol procurement across North America and Europe and increasingly in Asia Pacific.

Robust Growth of PVC End-Use Applications in Construction and Automotive Sectors

Isononyl alcohol is the critical upstream building block for the plasticizer segment, which overwhelmingly serves the polyvinyl chloride (PVC) industry. The European PVC industry association (VinylPlus) reported that over 6.5 million tonnes of PVC are consumed annually in Europe alone, with flexible PVC accounting for approximately 35% of total PVC usage across applications including flooring, roofing membranes, cables, and automotive interior parts. Globally, construction sector output is expected to grow by over 85% to reach US$ 15.5 trillion by 2030 according to the Oxford Economics Global Construction Outlook. Each new infrastructure project consuming flexible PVC for pipes, cables, and membranes translates into incremental demand for plasticizers derived from isononyl alcohol, adding more reliability in the construction sector.

Restraint - Feedstock Dependency on Butene and Propylene, Petrochemical Price Volatility

Isononyl alcohol is synthesized via the oligomerization of butene (C4 olefins) followed by hydroformylation (oxo synthesis) and hydrogenation. This production chain creates a direct cost dependency on butene and propylene prices, which are intrinsically linked to crude oil and natural gas feedstocks. The U.S. Energy Information Administration (EIA) reported crude oil price fluctuations exceeding 40% in 2022 alone, creating significant margin pressure for isononyl alcohol producers. Supply concentration, with ExxonMobil, BASF Petronas, and Evonik controlling significant global capacity, further amplifies exposure to feedstock disruptions and limits pricing flexibility for downstream buyers.

Growing Competition from Bio-Based Plasticizer Feedstocks

The emergence of bio-based plasticizers derived from vegetable oils, citric acid, and succinic acid presents a longer-term competitive threat to petroleum-derived isononyl alcohol. The European Bioplastics Association reported that bio-based plasticizer volumes in Europe are growing at over 8% annually, incentivized by sustainability mandates under the EU Green Deal and Circular Economy Action Plan. While bio-based alternatives currently face cost and performance limitations at commercial scale, increasing regulatory incentives and corporate ESG commitments may erode isononyl alcohol's market share in select premium applications over the medium term, particularly in food-contact and medical device flexible PVC applications.

Opportunity - Expanding Demand for DINCH in Medical and Food-Contact Flexible PVC Applications

Di-isononyl Cyclohexanoate (DINCH), produced exclusively from isononyl alcohol, represents a high-growth, high-value opportunity for market participants. DINCH has received approvals from the European Food Safety Authority (EFSA), U.S. FDA, and Health Canada for use in food-contact materials and medical devices, applications where the toxicological profile of the plasticizer is subject to the most rigorous scrutiny. The global medical plastics market, which heavily relies on flexible PVC for IV bags, tubing, and blood bags, is projected to grow significantly through 2033, creating a premium, specification-driven demand stream for isononyl alcohol that commands higher margins than commodity plasticizer grades. Companies that secure regulatory certifications and supply agreements with medical and food packaging converters stand to capture disproportionate value in this specialized, high-barrier segment.

Growth in Lubricant and Synthetic Ester Markets Driven by Electric Vehicle (EV) Transition

The global transition to electric vehicles (EVs) is creating a previously underappreciated opportunity for isononyl alcohol in lubricant and synthetic ester formulations. EV powertrains require advanced thermal management fluids, dielectric coolants, and gear lubricants with superior high-temperature stability and low-volatility characteristics, properties delivered by isononyl alcohol-derived synthetic esters. The International Energy Agency (IEA) reported global EV sales surpassed 14 million units in 2023 and are projected to reach 45 million units annually by 2030. As automakers and fluid formulators develop next-generation EV-compatible lubricant chemistries, the demand for specialty C9 alcohol-based esters including isononyl adipate and isononyl trimellitate is expected to increase materially, offering lubricant and additive manufacturers a differentiated growth avenue beyond traditional internal combustion engine (ICE) applications.

Category-wise Analysis

Production Process Insights

The ExxonMobil Process holds the leading share of approximately 52% of the global isononyl alcohol market by production process in 2025. This proprietary hydroformylation technology, developed and commercialized by ExxonMobil Chemical Company, is favored for its high selectivity toward the isononyl isomer blend, operational efficiency, and the ability to produce consistent product quality at very large scales. The ExxonMobil process leverages mixed butene (C4) feedstocks through a proprietary oxo catalysis pathway, yielding an isononyl alcohol product profile well-suited for DINP and DINCH plasticizer synthesis. The technology's integration with ExxonMobil's global refining and petrochemical assets provides significant feedstock cost advantages. While C4 Chemicals-based processes remain widely used by Asian producers, the ExxonMobil Process dominates output from the highest-capacity Western European and North American facilities, underpinning its market leadership in 2025.

Application Insights

Plasticizers represent the dominant application segment, accounting for approximately 72% of total isononyl alcohol consumption in 2025. Within this segment, Di-isononyl Phthalate (DINP) is the single largest end product, widely used as a general-purpose plasticizer in flexible PVC for cables, flooring, wall coverings, and automotive interior components. DINP has been assessed and confirmed as safe for its authorized uses by the European Chemicals Agency (ECHA) following a comprehensive risk assessment, making it the preferred phthalate plasticizer in markets where stricter alternatives such as DEHP are banned. The sheer scale of global flexible PVC production, combined with DINP's regulatory acceptance, cost-performance balance, and established supply chains with converters, ensures that plasticizers remain the unchallenged leading application for isononyl alcohol, with DINCH serving as the fastest-growing sub-segment.

Regional Insights

North America Isononyl Alcohol Market Trends and Insights

North America represents a significant and mature market for isononyl alcohol, underpinned by stringent regulatory frameworks governing plasticizer safety and robust demand from the automotive, construction, and healthcare sectors. The U.S. Consumer Product Safety Improvement Act (CPSIA) and U.S. EPA's Design for the Environment (DfE) program have actively accelerated the substitution of restricted phthalates with DINP and DINCH, directly supporting isononyl alcohol demand. ExxonMobil Chemical Company operates one of the world's largest isononyl alcohol production facilities in the region, supported by integrated C4 feedstock availability from domestic refining.

The U.S. construction industry, a major flexible PVC consumer, is benefiting from a residential and commercial building expansion supported by the Infrastructure Investment and Jobs Act, driving sustained plasticizer demand. The medical device sector, one of the fastest-growing end users of DINCH-plasticized flexible PVC, is anchored by FDA compliance requirements that favor DINCH, creating a premium demand stream. Innovation investment in bio-based and specialty ester derivatives of isononyl alcohol is also concentrated in North American R&D centers, reflecting the region's sophisticated chemical innovation ecosystem.

Europe Isononyl Alcohol Market Trends and Insights

Europe occupies a pivotal position in the global isononyl alcohol market, simultaneously serving as a major production hub and the world's most regulatory-driven demand market. BASF Petronas Chemicals Sdn. Bhd. (through the BASF-Petronas joint venture's European distribution) and Evonik Industries AG are key regional suppliers. Germany, the U.K., France, and Spain are leading consuming nations, driven by strong flexible PVC downstream industries in cable manufacturing, automotive, and construction materials. The EU REACH regulation's restriction on four high-concern phthalates from September 2023 has materially accelerated the demand for DINP and DINCH, both sourced from isononyl alcohol.

The VinylPlus 2030 Voluntary Commitment of the European PVC industry commits to recycling 900,000 tonnes of PVC annually and progressively reducing legacy plasticizer content, indirectly driving conversion to isononyl alcohol-based alternatives in new PVC formulations. EFSA's positive assessment of DINCH for food-contact applications is accelerating its adoption in packaging films across France and Germany. Regulatory harmonization under REACH ensures consistent product specifications across member states, simplifying cross-border supply and procurement of isononyl alcohol-derived plasticizers throughout the region.

Asia Pacific Isononyl Alcohol Market Trends and Insights

Asia Pacific is the largest and most dynamic regional market for isononyl alcohol with approximately 43% market share in 2025, anchored by China's enormous flexible PVC and plasticizer manufacturing ecosystem. China is the world's largest producer and consumer of PVC, with the China Chlor-Alkali Industry Association reporting PVC production capacity exceeding 30 million tonnes annually. The country's C4 chemicals process-based isononyl alcohol production underpins the vast majority of regional DINP supply. Chinese environmental regulations under the Ministry of Ecology and Environment (MEE) are progressively restricting legacy phthalate applications, driving domestic demand toward DINP and specialty grades.

India's rapidly expanding construction, automotive, and packaging sectors are creating new volume demand for plasticized flexible PVC, stimulating isononyl alcohol imports and investments in domestic derivative manufacturing. LG Chem Ltd. of South Korea and Japan-based specialty chemical producers maintain established positions in high-purity isononyl alcohol grades for electronics and automotive applications. ASEAN nations, including Thailand, Vietnam, and Indonesia, are attracting PVC compounding investments as global manufacturers diversify supply chains away from China, creating new greenfield demand centers for isononyl alcohol procurement across the Asia Pacific region through 2033.

Competitive Landscape

The global isononyl alcohol market exhibits a moderately consolidated structure, dominated by a limited number of vertically integrated petrochemical producers with strong upstream olefin and oxo-alcohol integration. High capital intensity, process technology barriers, and regulatory compliance requirements create significant entry constraints, reinforcing the position of established manufacturers. Competitive dynamics are shaped by production scale, feedstock security, and proprietary hydroformylation technologies that enable cost efficiency and consistent product quality.

Strategically, leading players prioritize specialty-grade positioning, particularly for DINCH and high-purity applications in medical and food-contact flexible PVC, where regulatory approvals and technical certifications provide pricing power and switching barriers. Business strategies increasingly emphasize long-term supply contracts, global distribution reach, and technical collaboration with plasticizer formulators. Sustainability credentials, including lower-carbon production pathways and responsible sourcing certifications, are emerging as additional differentiators. Meanwhile, regional producers primarily compete on price within commodity plasticizer segments, leveraging localized supply chains to maintain competitiveness in cost-sensitive markets.

Key Developments:

- March 2025: Exxon said it is investing US $100 million to build a new facility to produce cleaning alcohol used in semiconductor chip manufacturing, aiming to support domestic supply and advanced technology production.

- October 2023: BASF signed a technology license agreement with Ningbo Refining and Chemical Co. Ltd (NZRCC) to provide its proprietary oxo-technology for a world-scale isononyl alcohol production facility in Zhenhai, China, expected to start in 2026.

Companies Covered in Isononyl Alcohol Market

- Arkema Group

- BASF Petronas Chemicals Sdn. Bhd.

- Bax Chemicals

- DowDuPont, Inc.

- Eastman Chemical Company

- Evonik Industries AG

- ExxonMobil Chemical Company

- INEOS Group

- LG Chem Ltd.

- Oxea Corporation

- Mitsubishi Chemical Corporation

- Sasol Limited

- Perstorp Group

- KH Neochem Co., Ltd.

- Nan Ya Plastics Corporation

Frequently Asked Questions

The market is valued at US$ 2.4 billion in 2026, supported by 4.5% historical CAGR and strong DINP and DINCH plasticizer demand.

Regulatory shifts away from restricted phthalates and steady PVC demand in construction and automotive sectors drive growth.

Asia Pacific leads with ~43% share, while Europe is the fastest-growing due to regulatory-led plasticizer substitution.

Opportunities lie in DINCH-grade medical and food-contact PVC and INA-based synthetic esters for EV lubricants.

Key players include ExxonMobil Chemical Company, BASF Petronas Chemicals, Evonik Industries AG, Oxea Corporation, LG Chem Ltd., Eastman Chemical Company, Arkema Group, INEOS Group, Mitsubishi Chemical Corporation, and Perstorp Group.