- Advanced Materials

- Aerogel Market

Aerogel Market Size, Share, and Growth Forecast, 2026 - 2033

Aerogel Market by Product Type (Silica, Carbon, Others), Form (Blanket, Particle, Others), End-user Industry, and Regional Analysis for 2026 - 2033

Aerogel Market Size and Trends Analysis

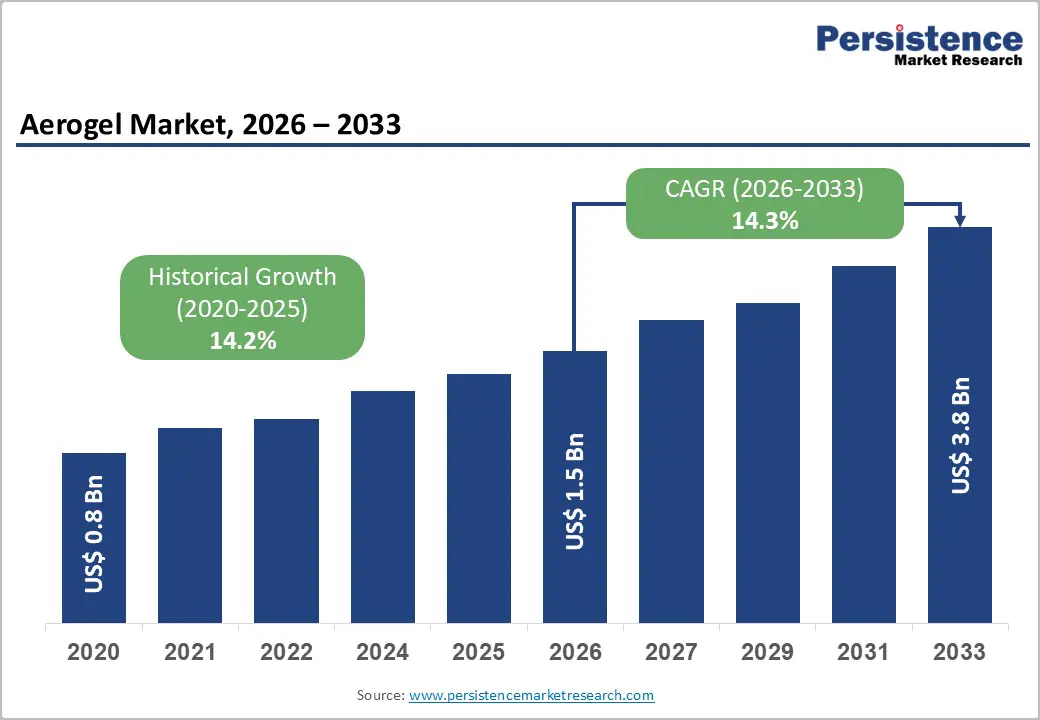

The global aerogel market size is likely to be valued at US$1.5 billion in 2026 and is expected to reach US$3.8 billion by 2033, growing at a CAGR of 14.3% between 2026 and 2033, driven by tightening energy-efficiency regulations, rising demand for high-performance insulation, and increasing adoption in electric vehicle (EV) thermal management systems.

Industrial decarbonization initiatives and infrastructure modernization are reinforcing demand across the oil & gas and construction sectors. Policy frameworks across major economies are accelerating insulation upgrades, positioning aerogel as a critical material for achieving energy efficiency and emission reduction targets.

Key Industry Highlights:

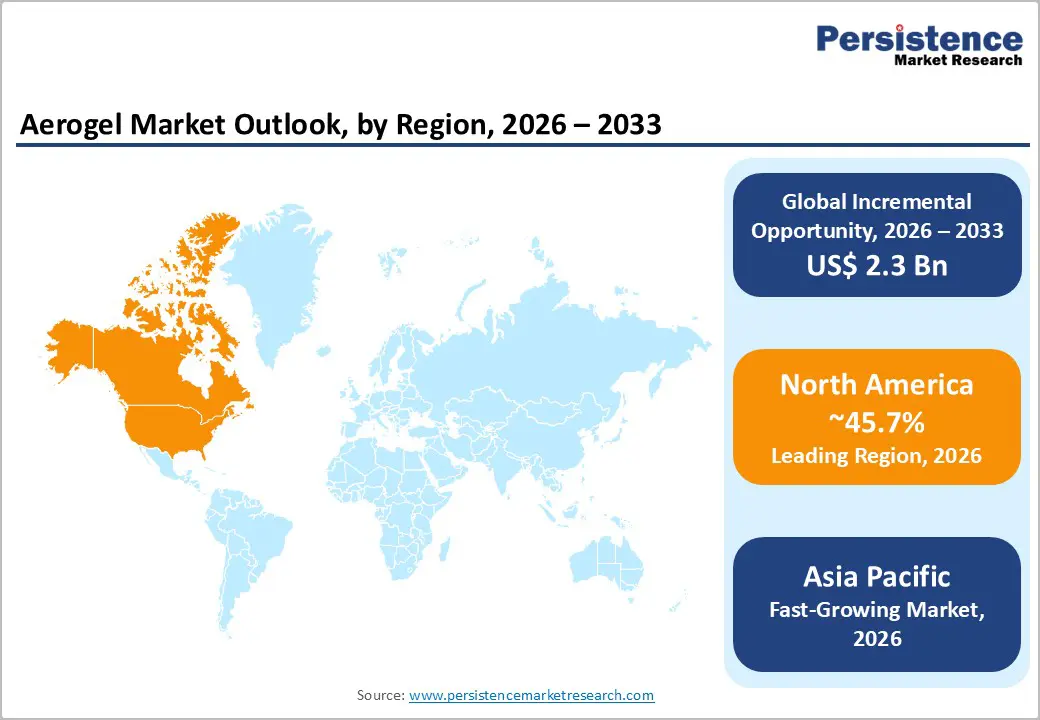

- Leading Region: North America is projected to account for approximately 45.7% of the market share, driven by strong demand across oil & gas, EV, and industrial insulation sectors.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, supported by rapid industrialization and policy-driven energy efficiency initiatives, with growth rates exceeding those of other regions over the forecast period.

- Investment Plans: Market investments are increasingly focused on EV battery thermal management, infrastructure modernization, and regional manufacturing expansion, particularly in Asia Pacific and North America, to enhance supply chain efficiency and meet rising demand.

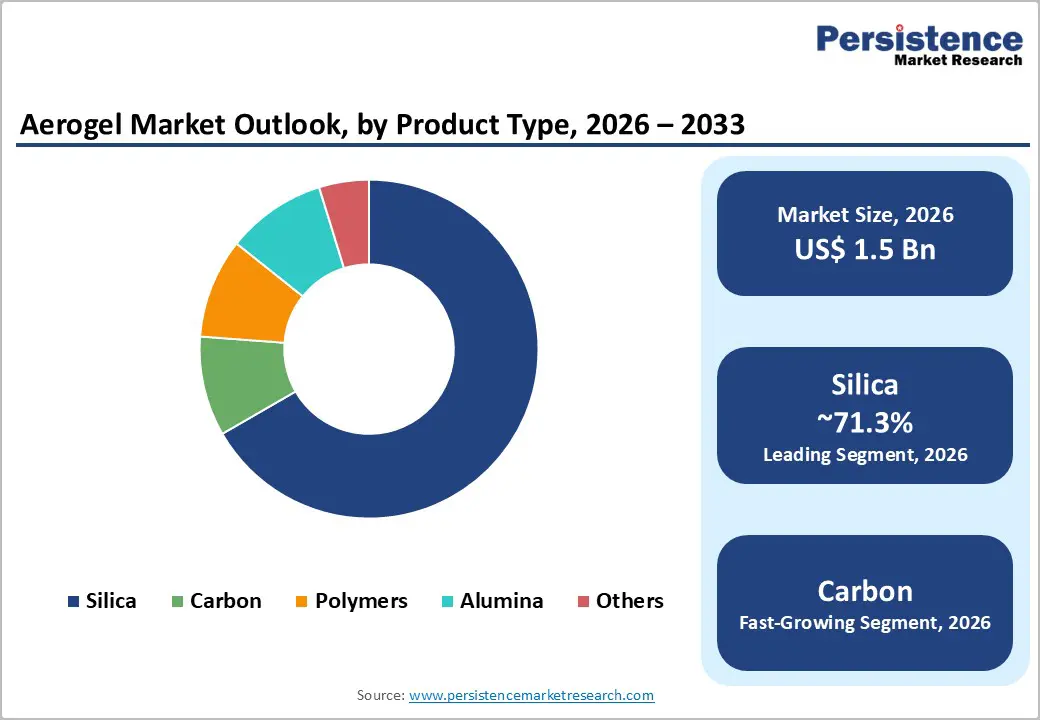

- Dominant Product Type: Silica aerogel dominates, holding an anticipated 71.3% market share, supported by its extensive use in insulation and established commercial scalability.

- Leading Form: Blanket form leads the market with an anticipated 63.4% share, owing to its ease of installation, flexibility, and widespread use in industrial and construction insulation applications.

| Key Insights | Details |

|---|---|

| Aerogel Market Size (2026E) | US$1.5 Bn |

| Market Value Forecast (2033F) | US$3.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 14.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 14.2% |

DRO Analysis

Driver Analysis - Energy-Efficiency Regulations are Expanding the Adoption of Aerogel in Buildings and Industrial Systems

Global regulatory frameworks are increasingly prioritizing low-energy buildings and industrial efficiency, creating a strong demand for advanced insulation materials. Updated building performance standards in Europe and North America emphasize zero-emission and near-zero energy structures, directly increasing the need for high-performance insulation solutions. Aerogel’s ultra-low thermal conductivity allows effective insulation in space-constrained environments, such as retrofitting older buildings or preserving architectural structures. This capability makes it highly suitable for compliance-driven upgrades, where conventional insulation materials fail to meet performance thresholds without increasing wall thickness.

Industrial Decarbonization and Process Efficiency are Sustaining Demand in Oil & Gas and Heavy Industries

Aerogel continues to play a critical role in high-temperature and cryogenic insulation applications, particularly in oil & gas, petrochemicals, and refining industries. Its ability to reduce heat loss and minimize corrosion under insulation (CUI) provides significant lifecycle cost benefits. Industrial facilities are increasingly focusing on energy efficiency to meet emission reduction targets, which enhances demand for aerogel-based insulation. The installed base of pipelines, subsea systems, and processing equipment ensures recurring demand through maintenance and retrofitting cycles, rather than one-time capital expenditure, supporting long-term market stability.

Electrification and EV Battery Safety Requirements are creating a High-Growth Application Segment

The rapid expansion of electric mobility is driving demand for advanced thermal barrier materials to prevent thermal runaway in lithium-ion batteries. Aerogel materials, particularly in thin and flexible formats, are being widely adopted in EV battery packs due to their lightweight structure, thermal resistance, and space efficiency. Government incentives and investments in low-emission vehicles are accelerating EV production, thereby expanding the addressable market for aerogel. This transition marks a strategic shift where aerogel is evolving from a niche insulation material to a critical component in next-generation energy systems.

Restraint Analysis - High Production Costs Limit Widespread Adoption in Cost-Sensitive Applications

Despite its superior performance, aerogel remains significantly more expensive than conventional insulation materials due to complex manufacturing processes and limited economies of scale. Production challenges, including solvent handling and drying techniques, contribute to high capital and operational costs. This restricts adoption in price-sensitive sectors such as residential construction, where upfront cost considerations outweigh long-term efficiency benefits. As a result, aerogel is primarily deployed in high-value applications where performance justifies the premium, limiting its penetration in mass-market segments.

Availability of Substitute Materials Creates Competitive Pressure

The presence of alternative insulation materials such as fiberglass, mineral wool, and polymer foams continues to challenge aerogel adoption. These materials offer lower upfront costs and established supply chains, making them more accessible for large-scale projects. In applications where space constraints are less critical, end users often prioritize cost over performance. This dynamic slows aerogel adoption in conventional construction and industrial applications, confining its use to specialized environments requiring superior thermal efficiency and durability.

Opportunity Analysis - Building Retrofit Initiatives are Driving Demand for Thin, High-Performance Insulation Solutions

Global efforts to improve energy efficiency in existing buildings are creating strong opportunities for aerogel. Retrofit projects often face space limitations and structural constraints, making traditional insulation impractical. Aerogel’s ability to deliver high thermal performance in thin layers positions it as an ideal solution for such applications. Public-sector investments in energy-efficient infrastructure and stricter compliance requirements are expected to accelerate adoption, particularly in urban and heritage building renovations.

Asia Pacific Presents Significant Growth Potential Due To Infrastructure Expansion and Policy Alignment

Rapid urbanization, industrial growth, and government-led energy efficiency programs across Asia Pacific are driving demand for advanced insulation materials. Countries such as China, Japan, and India are implementing policies focused on reducing energy intensity and improving building efficiency standards. At the same time, expanding manufacturing capabilities in the region is reducing production costs and enhancing supply chain efficiency. This combination of policy support, industrial expansion, and local manufacturing positions Asia Pacific as a key growth engine for the aerogel market.

Category-wise Analysis

Product Type Analysis

Silica aerogel dominates the market, accounting for an anticipated 71.3% share in 2026, and remains the most widely used product type due to its proven thermal performance, scalability, and versatility across multiple applications. It is extensively utilized in insulation blankets, coatings, panels, and industrial systems, particularly in oil & gas pipelines, LNG facilities, and high-temperature processing units. Its dominance is supported by a well-established supply chain and long commercialization history, enabling consistent product availability and cost optimization over time.

For example, silica aerogel blankets are widely deployed in subsea pipeline insulation and refinery equipment, where minimizing heat loss and preventing corrosion under insulation are critical. In the construction sector, silica aerogel-based plasters and panels are increasingly used in heritage building retrofits and high-performance façades, where space constraints require ultra-thin insulation solutions. Continuous product innovations, such as reinforced blankets and hydrophobic variants, further strengthen its leading position.

Carbon aerogel is the fastest-growing segment, gaining traction due to its expanding role in energy storage, EV battery systems, and advanced electronics. Its unique combination of high electrical conductivity, low density, and superior thermal resistance makes it highly suitable for next-generation technologies. The rapid growth of the EV industry is a primary driver, with carbon aerogel increasingly used in battery thermal management systems to prevent thermal runaway and enhance safety.

For instance, automakers and battery manufacturers are integrating carbon aerogel-based thermal barriers within lithium-ion battery packs to improve performance and safety compliance. Beyond EVs, carbon aerogel is also being explored in supercapacitors, hydrogen storage, and aerospace applications, where lightweight and high-performance materials are essential. This segment reflects a broader market shift toward high-value, innovation-driven applications, positioning carbon aerogel as a critical material in future energy systems.

Form Analysis

Blanket form leads the market with an anticipated 63.4% share in 2026. Aerogel blankets represent the most commercially dominant form due to their flexibility, ease of installation, and compatibility with existing insulation systems. These blankets are widely used in industrial applications such as pipelines, storage tanks, offshore platforms, and process equipment, where rapid installation and durability are essential. Their ability to conform to complex geometries allows for efficient insulation of irregular surfaces, reducing both labor time and operational downtime.

For example, aerogel blankets are commonly deployed in subsea oil & gas projects and LNG infrastructure to maintain thermal stability under extreme conditions. In the construction sector, they are increasingly used in roof insulation and external wall systems, particularly in retrofits where maintaining internal space is critical. The balance between high thermal efficiency and practical usability continues to support the widespread adoption of blanket-based aerogel solutions.

Particle form is the fastest-growing segment, emerging as a highly versatile form, enabling applications across coatings, plasters, composites, and advanced material systems. Their fine granular structure allows them to be integrated into insulating paints, cementitious renders, and lightweight construction materials, enhancing thermal performance without significantly increasing weight or thickness.

In the automotive and EV sectors, particle aerogels are increasingly used in battery packs as thermal barrier fillers, improving heat resistance and safety. For instance, particle-based aerogels are being incorporated into coatings applied to battery modules to prevent heat propagation. In addition, their use in consumer products such as high-performance apparel and footwear insulation is gaining traction. This adaptability across industries positions particle aerogels as a key growth driver, particularly in applications where traditional blanket or panel forms are less practical.

Regional Insights

North America Aerogel Market Trends - EV Thermal Management & Industrial Insulation Leadership

North America is projected to lead the aerogel market, commanding approximately 45.7% of market share in 2026. The U.S. drives regional growth, supported by strong demand across oil & gas, aerospace, construction, and EV sectors. The region benefits from a well-established innovation ecosystem, with significant investments in advanced materials and energy efficiency technologies. Companies such as Aspen Aerogels, Inc. and Cabot Corporation are at the forefront of commercialization, supplying aerogel solutions for both industrial insulation and EV battery thermal management. For instance, Aspen Aerogels’ expansion of its PyroThin thermal barrier platform for EV batteries has strengthened its positioning within North America’s rapidly evolving electric mobility supply chain.

Regulatory frameworks promoting energy efficiency and emission reduction remain key growth drivers. Industrial decarbonization initiatives and updated building performance standards are increasing the adoption of high-performance insulation materials. The U.S. Department of Energy’s continued emphasis on insulation upgrades as a cost-effective energy-saving measure reinforces aerogel demand in both residential and commercial construction. In parallel, the region’s oil & gas sector continues to adopt aerogel insulation for subsea pipelines and LNG infrastructure, where durability and thermal efficiency are critical. The presence of leading manufacturers, combined with strong R&D capabilities and ongoing product innovation, further strengthens the region’s competitive advantage.

Investment trends indicate a growing focus on EV supply chains and infrastructure modernization, creating new opportunities for aerogel applications. For example, Cabot Corporation’s development of aerogel-based thermal barrier materials for lithium-ion batteries highlights the increasing integration of aerogel into next-generation mobility solutions. At the same time, ongoing upgrades in aging industrial infrastructure across the U.S. and Canada are driving demand for retrofit insulation solutions, ensuring steady and recurring market growth.

Europe Aerogel Market Trends - Regulation-Driven Retrofit Insulation & Sustainable Construction Focus

Europe represents a significant market for aerogel, driven by stringent regulatory policies and strong sustainability initiatives. Countries such as Germany, the U.K., France, and Spain are leading adoption due to robust industrial bases and active construction sectors. The region’s focus on energy-efficient buildings and carbon neutrality targets has made advanced insulation materials a priority, particularly in urban redevelopment and retrofit projects.

The regulatory environment plays a central role in shaping demand. Policies aimed at achieving zero-emission buildings and improved energy performance standards are accelerating the adoption of aerogel in construction. Retrofit projects are a major growth driver, especially in historic urban centers where space constraints limit the use of traditional insulation materials. Aerogel-based plasters and panels are increasingly being used in heritage building renovations to meet energy efficiency requirements without altering structural aesthetics.

Europe also demonstrates strong innovation capabilities, supported by companies such as Armacell International S.A., Svenska Aerogel Holding AB, and ENERSENS. For instance, Armacell’s launch of advanced aerogel insulation solutions for cryogenic and dual-temperature applications has expanded its product portfolio for industrial use. Similarly, Svenska Aerogel’s commercialization of Quartzene material in insulation and coatings applications reflects the region’s push toward next-generation materials. ENERSENS is advancing continuous production technologies to reduce aerogel manufacturing costs, which could improve market accessibility over time. Investments in renewable energy infrastructure, district heating systems, and sustainable construction continue to create long-term growth opportunities across Europe.

Asia Pacific Aerogel Market Trends - Rapid Industrialization & Policy-Backed Energy Efficiency Growth

Asia Pacific is the fastest-growing region in the aerogel market, supported by rapid industrialization, urbanization, and policy-driven energy efficiency initiatives. China, Japan, India, and ASEAN countries are key contributors to regional growth, with increasing demand across construction, industrial insulation, and transportation sectors. The region’s expanding infrastructure and manufacturing base are creating a strong foundation for aerogel adoption.

Government policies focused on reducing energy consumption and improving building efficiency are significant growth drivers. For example, China’s energy conservation programs and industrial efficiency mandates are encouraging the use of advanced insulation materials in manufacturing and construction. India’s push toward energy-efficient commercial buildings and infrastructure modernization is also contributing to rising demand. Japan’s emphasis on high-performance buildings and advanced materials further supports adoption in both construction and industrial applications.

The region benefits from cost-effective manufacturing capabilities and growing domestic production, which are improving supply chain efficiency and reducing dependence on imports. Companies such as Nano Tech Co., Ltd., IBIH Advanced Materials Co., Ltd., and Guangdong Alison Hi-Tech Co., Ltd. are expanding production capacity and strengthening regional supply networks. For instance, Armacell’s expansion of aerogel manufacturing capacity in Pune, India, highlights the strategic importance of Asia Pacific as both a production hub and a consumption market. Additionally, IBIH’s large-scale deployment of aerogel materials in EV battery systems demonstrates the region’s growing role in electric mobility and advanced materials integration.

Investment trends across Asia Pacific highlight increasing adoption in EV manufacturing, construction, and industrial insulation, supported by government incentives and infrastructure spending. The region’s strong alignment between policy, manufacturing, and demand positions it as a major growth hub for the aerogel market, with significant long-term potential.

Competitive Landscape

The global aerogel market is moderately consolidated, with leading players accounting for approximately 65-70% of market share. These companies benefit from strong technological capabilities, established distribution networks, and extensive application expertise. Smaller players operate in niche segments, focusing on specialized products and regional markets. Competition is driven by innovation, cost optimization, and application-specific solutions.

Leading companies are focusing on product innovation, regional expansion, and cost reduction strategies. Emphasis is placed on developing application-specific solutions, strengthening supply chains, and leveraging partnerships to expand market reach. Companies are also investing in next-generation aerogel technologies to enhance performance and reduce production costs.

Key Industry Developments

- In February 2026, Svenska Aerogel Holding AB entered into a distribution agreement with KRAHN Chemie GmbH in Germany, aiming to expand its presence in Europe’s construction and process industries through advanced aerogel-based coatings and insulation solutions.

- In January 2026, Svenska Aerogel Holding AB announced an increase in its commercial customer base from 10 to 15 active clients, highlighting growing adoption of its Quartzene® material across building, industrial, and advanced applications.

Companies Covered in Aerogel Market

- Aspen Aerogels, Inc.

- Cabot Corporation

- Armacell International S.A.

- Nano Tech Co., Ltd.

- IBIH Advanced Materials Co., Ltd.

- Svenska Aerogel Holding AB

- ENERSENS

- aerogel-it GmbH

- Aerogel Technologies, LLC

- Guangdong Alison Hi-Tech Co., Ltd.

- Zhejiang UGOO Technology Co., Ltd.

- JIOS Aerogel Corporation

- Active Aerogels

- Green Earth Aerogel Technologies

- BASF SE

- Dow Inc.

Frequently Asked Questions

The global aerogel market size is estimated to be US$1.5 billion in 2026.

The aerogel market is projected to reach US$3.8 billion by 2033.

Key trends include rising adoption in EV battery thermal management, growing demand for thin insulation in building retrofits, advancements in aerogel manufacturing technologies, and increasing use in industrial decarbonization applications.

The silica aerogel segment is the leading product category, accounting for an anticipated 71.3% market share, due to its widespread use across industrial, construction, and energy applications.

The aerogel market is expected to grow at a CAGR of 14.3% from 2026 to 2033.

Some of the major players include Aspen Aerogels, Inc., Cabot Corporation, Armacell International S.A., Svenska Aerogel Holding AB, and ENERSENS.