- Advanced Materials

- Ultraviolet Curable Resin Market

Ultraviolet Curable Resin Market Size, Share, and Growth Forecast 2026 - 2033

Ultraviolet Curable Resin Market by Resin Type (Acrylated Epoxies, Acrylated Urethanes, Acrylated Polyesters, Acrylated Silicones, Others / Hybrid Resins), Composition (Monomers, Oligomers, Photoinitiators, Additives & Stabilizers), Application (Coatings, Adhesives & Sealants, Printing Inks, 3D Printing Materials, Electronics & Optical), End-user, and Regional Analysis, 2026 - 2033

Ultraviolet Curable Resin Market Size and Trend Analysis

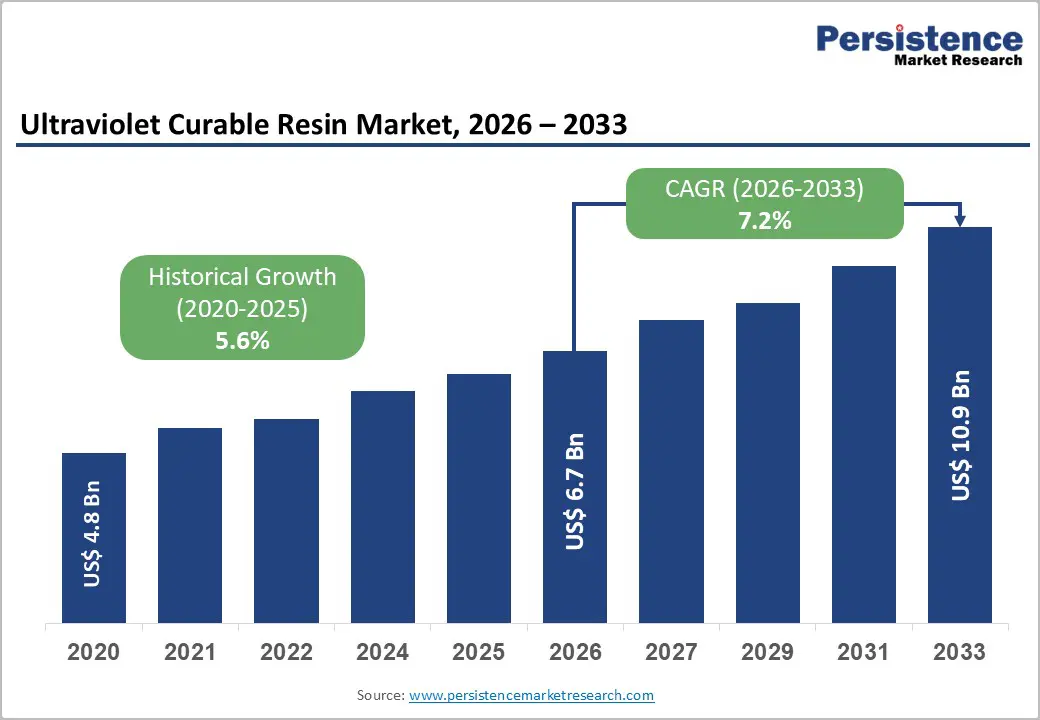

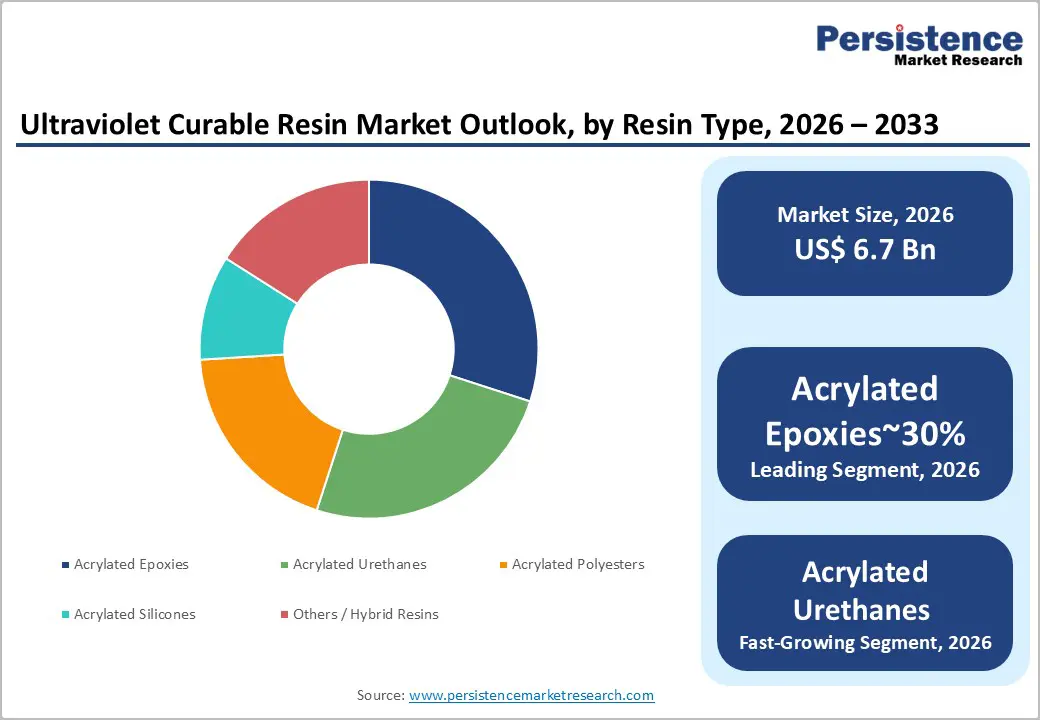

The global ultraviolet curable resin market size is expected to be valued at US$ 6.70 billion in 2026 and is projected to reach US$ 10.90 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

The global market is driven by accelerating industrial adoption of ultraviolet curing technology as a faster, more energy-efficient alternative to thermal and solvent-based processing methods.

Key Industry Highlights:

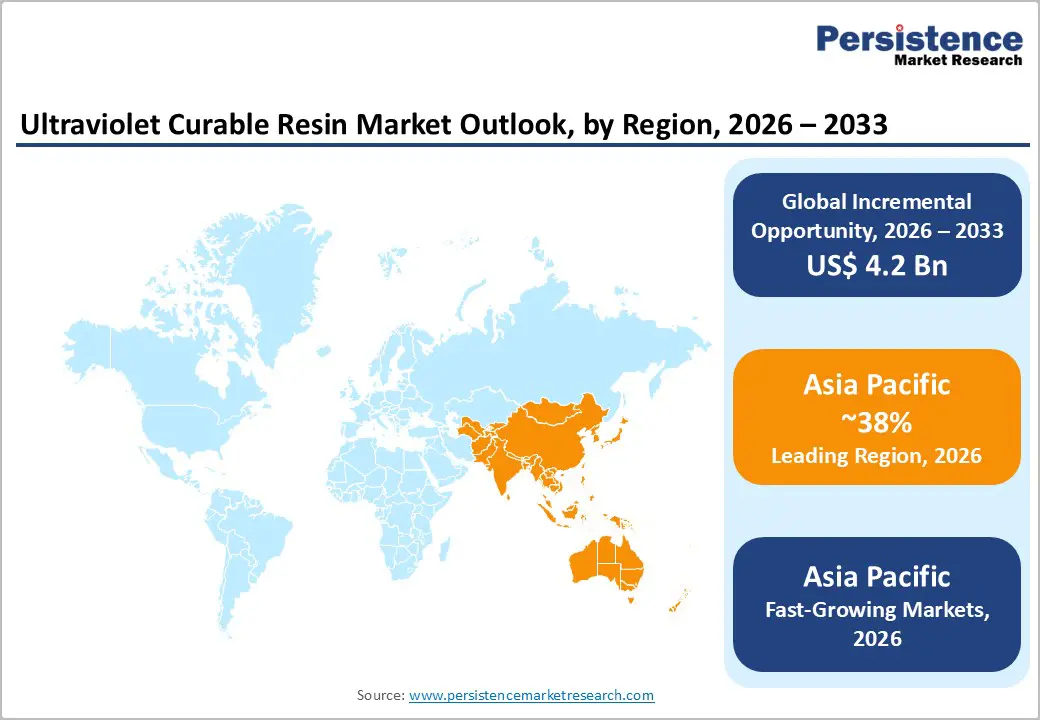

- Leading Region: Asia Pacific leads the global market with a 38% share in 2026, underpinned by the world's largest electronics manufacturing concentration, rapid EV industry expansion, and government-mandated industrial modernisation programmes driving systematic adoption of radiation curing systems across coatings, adhesives, and printing ink applications.

- Fast-Growing Market: Asia Pacific is also the fast-growing market projected at a CAGR of 9.8% by 2033, with China's VOC regulatory enforcement, India's PLI-backed electronics manufacturing growth.

- Leading Segment: Acrylated epoxies dominate the resin type segment with a 30% market share in 2026, driven by their unmatched combination of hardness, chemical resistance, and versatile substrate adhesion.

- Fastest Growing Segment: Acrylated urethanes represent the fast-growing resin type segment, with growth catalysed by surging demand for flexible, impact-resistant UV curing adhesives and coatings in electric vehicle manufacturing, flexible electronics, and premium consumer goods.

- Key Opportunity: The 3D printing photopolymers application represents the most actionable near-term opportunity, as vat photopolymerisation adoption accelerates across dental, industrial, and aerospace sectors, manufacturers that establish specification-locked co-development relationships with hardware OEMs by 2027.

Market Dynamics

Drivers - Regulatory-Driven Shift Toward Low-VOC Ultraviolet Curing Technology

Tightening environmental compliance frameworks across North America, Europe, and major Asia Pacific economies are making low-VOC UV curable resins the default formulation choice for industrial coatings and printing inks producers.

Regulatory bodies in the European Union have progressively lowered permissible VOC thresholds under the Industrial Emissions Directive, directly disqualifying solvent-borne alternatives in an expanding range of applications. UV curing adhesives and coatings satisfy these limits without requiring additional abatement infrastructure, making them economically superior as well as compliant. This regulatory momentum translates into a structural, non-cyclical demand driver that underpins ultraviolet curable resin market growth across the forecast period.

Accelerating Electronics Manufacturing and Miniaturisation Demands

Rapid expansion in consumer electronics, semiconductor packaging, and flexible display manufacturing generates consistent, high-volume demand for precision UV curing adhesives and encapsulants. Electronics manufacturers require curing systems capable of operating at micron-scale tolerances, and free radical polymerization-based UV systems deliver cure speeds and dimensional accuracy that thermal alternatives cannot match.

Based on authenticated market intelligence, the electronics and electrical end-use segment already accounts for nearly 29.0% of the global Ultraviolet Curable Resin Market in 2026, underscoring the sector's foundational importance. Continued investment in 5G infrastructure, wearable devices, and advanced printed circuit board (PCB) assemblies further amplifies what drives growth in the ultraviolet curable resin market over the near and medium term.

Restraints - Raw Material Price Volatility and Supply Chain Concentration Risk

Acrylated epoxies, acrylated urethanes, and specialty photoinitiators rely on petrochemical feedstocks and fine chemical intermediates that exhibit meaningful price volatility across commodity cycles. A significant share of photoinitiator synthesis capacity concentrates in China, exposing global formulators to geopolitically driven supply disruptions and logistics cost spikes.

When feedstock prices escalate, formulators face margin compression unless they can pass costs upstream, a difficult proposition in competitive, price-sensitive packaging and printing markets. This vulnerability slows adoption among cost-constrained small and medium-sized enterprises and introduces forecast uncertainty for ultraviolet curable resin industry participants dependent on stable input economics.

Performance Limitations in Thick-Section and Pigmented Substrate Applications

UV radiation does not penetrate thick or heavily pigmented coatings uniformly, restricting acrylated polyesters and other UV resins in dark-pigmented automotive topcoats, deep-cast components, and opaque industrial assemblies. Formulators address this partly through dual-cure and hybrid cationic curing systems, but these add formulation complexity and cost.

End-users evaluating conversion from thermal curing often encounter incompatibility with existing production line geometries or substrate compositions, raising the switching cost and extending the sales cycle. This technical ceiling effectively locks out the ultraviolet curable resin space from certain high-volume application segments that would otherwise represent attractive growth opportunities.

Opportunity - Rapid Expansion of 3D Printing Photopolymers and Additive Manufacturing Applications

The 3D printing photopolymers segment represents one of the highest-velocity growth pockets within the ultraviolet curable resin industry, as vat photopolymerisation and digital light processing technologies proliferate across dental, aerospace, automotive prototyping, and consumer goods sectors. Formulators with capabilities in customised resin chemistry, particularly around high-modulus and biocompatible acrylated urethanes, stand best positioned to capture premium-priced contracts. Industry studies emphasize that UV resin producers to prioritise co-development partnerships with hardware OEMs in dental and industrial 3D printing, as these relationships create long-duration, specification-locked revenue streams.

Healthcare and Medical Device Manufacturing as an Emerging High-Value Vertical

UV curing adhesives and encapsulants are gaining regulatory acceptance in medical device assembly, driven by the need for precise, rapid, and biocompatible bonding in applications ranging from catheter tip bonding to hearing aid component assembly and ophthalmic device manufacturing. Regulatory frameworks such as ISO 10993 for biocompatibility evaluation are increasingly guiding formulator strategies, with those achieving compliance gaining a durable competitive moat in the healthcare segment.

The healthcare and medical devices end-use vertical commands significantly higher margins than commodity packaging or industrial applications, making it a strategically attractive diversification pathway for established UV resin producers. Market participants with existing relationships in pharmaceutical packaging and medical-grade adhesives should accelerate investment in low-migration, extractable-tested UV formulations to capture this opportunity. As global healthcare expenditure rises and device miniaturisation intensifies demand for micron-level bonding precision.

Category-wise Analysis

Resin Type Insights

Acrylated epoxies hold the leading position in the ultraviolet curable resin market, accounting for 30% in 2026. This segment leads because acrylated epoxies offer a strong combination of hardness, chemical resistance, and excellent adhesion to different substrates, making them the preferred choice for industrial wood coatings, metal coatings, and UV printing inks.

Acrylated epoxy oligomers are the most widely used class in global UV coating formulations, supported by long-term performance validation across demanding applications. Acrylated Urethanes are the fastest growing segment, driven by increasing demand for flexible and impact-resistant coatings and adhesives in automotive refinishing, electronics potting, and premium consumer products. While acrylated epoxies will maintain their strong position in established coating applications, faster growth of urethane acrylates is expected to gradually narrow the market share gap by 2030.

Composition Insights

Monomers dominate the ultraviolet curable resin market by composition, accounting for 45% of the global market in 2026. Their leadership comes from their dual role as reactive diluents and crosslinkers, which allows manufacturers to control viscosity, curing speed, and final coating performance across a wide range of applications. Market data indicate that common reactive monomers such as HDDA and TPGDA are used in over 70% of commercial UV coating formulations worldwide, highlighting their essential role in the value chain.

Oligomers are the fast-growing segment, as they define key performance characteristics such as strength, flexibility, and resistance to yellowing in advanced applications such as 3D printing, optical adhesives, and electronics encapsulation. While monomers will continue to dominate due to their widespread use, oligomers are gaining importance as demand shifts toward high-performance and specialized UV resin formulations.

Application Insights

Coatings represent the largest application segment accounting for 40.0% of global market value in 2026. This dominance is driven by the ability of UV curing technology to deliver fast processing speeds, superior surface hardness, and strong scratch resistance compared to conventional solvent-based and water-based systems, all while maintaining cost efficiency.

These advantages make UV coatings highly suitable for wood, plastic, metal, and paper applications in industrial production. Stricter VOC emission regulations across major regions such as Europe, the United States, and China have further accelerated the shift toward UV-curable coatings, strengthening this segment’s position.

Adhesives and sealants are the fast-growing application, supported by rising demand in electric vehicle battery assembly, electronics display bonding, and medical device manufacturing. As innovation continues, companies must balance their focus between coatings and high-growth adhesive applications.

End-user Insights

Electronics and electrical manufacturing leads by end-use, accounting for 29% of total market value in 2026, equivalent to US$ 1.94 billion. This is driven by the need for high precision, fast curing, and clean processing conditions, which are essential in applications such as printed circuit boards, display panel bonding, optical components, and semiconductor encapsulation.

Global electronics production has surpassed US$ 3 trillion, with a growing share requiring UV-cured materials as devices become smaller and more complex. The automotive sector is the fast- growing end-use segment, mainly due to the rapid expansion of electric vehicles. UV resins are increasingly used in battery systems, lightweight bonding, sensor coatings, and interior applications. While electronics will remain dominant in the near term, the automotive segment is expected to grow rapidly and become a major contributor to future market expansion.

Regional Insights

North America Ultraviolet Curable Resin Market Trends and Insights

North America accounts for 25.0% of the global ultraviolet curable resin market in 2026, representing US$ 1.68 billion. The region benefits from a mature industrial base in automotive coatings, electronics assembly, and packaging that actively converts toward radiation curing systems under the dual pressures of VOC regulation and production efficiency mandates.

Strong investment in additive manufacturing infrastructure and semiconductor fabrication, amplified by the CHIPS and Science Act, generates sustained demand for high-performance 3D printing photopolymers and electronics-grade UV resins. Looking ahead, North America's UV curable resin industry stands to accelerate further as domestic EV production scales and reshoring of electronics manufacturing intensifies through 2033.

- United States Ultraviolet Curable Resin Market Size

The United States commands an estimated 78% of the North America ultraviolet curable resin market share, equivalent to approximately US$ 1.31 billion in 2026, driven by its concentration of advanced electronics OEMs, tier-one automotive coatings facilities, and a highly active 3D printing photopolymers ecosystem. Regulatory enforcement by the U.S. Environmental Protection Agency (EPA) continues to accelerate the displacement of solvent-borne systems in industrial coatings. As domestic semiconductor and EV battery manufacturing capacity expands through 2030, the United States will deepen its position as the region's primary UV resin demand engine.

Europe Ultraviolet Curable Resin Market Trends and Insights

Europe is likely to account for 20% global share in 2026, representing US$ 1.34 billion. The region's regulatory architecture, anchored by the EU REACH regulation, the Industrial Emissions Directive, and the Green Deal framework, creates a structurally favourable environment for low-VOC UV curable resin adoption across coatings, printing inks, and adhesives applications. European manufacturers place a premium on performance sustainability, driving demand for aliphatic acrylated urethanes and bio-derived acrylated polyesters that align with circular economy mandates. The region's ultraviolet curable resin industry analysis points to healthcare, premium automotive, and specialty packaging as the highest-growth subsectors through the forecast horizon.

- Germany Ultraviolet Curable Resin Market Size

Germany commands an estimated 28% of the Europe ultraviolet curable resin market, representing approximately US$ 375 million in 2026. The country's dominant automotive manufacturing base, anchored by Volkswagen Group, BMW AG, and Mercedes-Benz AG, drives substantial demand for UV curing adhesives and surface coatings used in both conventional and electric vehicle production. Germany's established chemicals industry and proximity to major oligomer and monomer producers further support supply chain efficiency. With the German automotive industry accelerating EV platform investments, UV resin demand in this market is projected to grow above the European regional average through 2033.

- United Kingdom Ultraviolet Curable Resin Market Size

The United Kingdom holds an estimated 18% in 2026. Demand concentrates in the packaging, printing inks, and healthcare end-use segments, where the UK's strong consumer goods and pharmaceutical manufacturing base sustains consistent UV resin consumption. Post-Brexit regulatory alignment continues to track closely with EU VOC standards, preserving the structural demand incentive for low-emission UV curing formulations. Growth in UK-based medical device manufacturing and sustainable packaging innovation positions this market for above-average ultraviolet curable resin market growth through the forecast period.

- France Ultraviolet Curable Resin Market Size

France represents an estimated 16% in 2026The French market draws demand primarily from luxury goods coatings, automotive refinishing, and advanced packaging, sectors where surface quality and finish durability justify premium UV resin formulations. France's proactive industrial decarbonisation agenda under the Plan de Relance further accelerates conversion from solvent-based to UV curable systems in manufacturing. As French industry deepens investment in sustainable production technologies, UV curable resin adoption is expected to broaden into industrial manufacturing and construction-related coating applications through 2033.

Asia Pacific Ultraviolet Curable Resin Market Trends and Insights

Asia Pacific accounts for 38.0% of the global market in 2026, and is the fast-growing market. The market here includes the world's largest electronics manufacturing complex, a rapidly expanding automotive industry transitioning toward EV platforms, and an accelerating shift toward premium, low-VOC coatings in industrial and consumer applications across China, Japan, South Korea, and India. Government-backed industrial modernisation initiatives across the region prioritise energy-efficient production technologies, directly favouring radiation curing systems over thermal alternatives. Asia Pacific is projected to widen its share advantage over North America and Europe by 2033.

- China Ultraviolet Curable Resin Market Size

China represents an estimated 55% of the Asia Pacific ultraviolet curable resin market. The country's commanding position reflects its role as the world's largest electronics assembly hub, its massive automotive manufacturing footprint, and its domestic UV resin production capacity led by companies such as Wanhua Chemical Group Co., Ltd. and Jiangsu Litian Technology Co., Ltd. Stringent VOC regulations enforced under China's Action Plan for the Prevention and Control of Air Pollution continue to accelerate coating conversion. As Chinese manufacturers upgrade to higher-value production, particularly in EVs, optical films, and 5G components, demand for precision UV curable resin formulations.

- India Ultraviolet Curable Resin Market Size

India accounts for an estimated 12% of the Asia Pacific Ultraviolet Curable Resin Market, representing approximately US$ 306 million in 2026. Rapid industrialisation, the expansion of domestic electronics assembly under the Production-Linked Incentive (PLI) Scheme, and a booming packaging sector collectively drive UV resin demand across printing inks, coatings, and adhesive applications. India's cost-competitive manufacturing environment attracts investment from global UV resin formulators seeking lower-cost production bases for the regional market. The country's UV curable resin sector is projected to grow at one of the highest rates in the Asia Pacific, supported by infrastructure investment, rising consumer goods output, and tightening environmental standards.

- Japan Ultraviolet Curable Resin Market Size

Japan holds an estimated 18% of the Asia Pacific ultraviolet curable resin market, representing approximately US$ 459 million in 2026. Japan's demand profile concentrates in high-precision electronics, optical coatings, and advanced adhesives, segments that require the most technically sophisticated UV resin formulations and where Japanese chemical companies such as Toagosei Co., Ltd. and Resonac Holdings Corporation maintain strong domestic supply positions.

The country's ultraviolet curable resin industry analysis highlights a structural demand shift toward LED-UV compatible formulations as energy efficiency requirements tighten across manufacturing. Japan's focus on quality-differentiated UV resin innovation positions it as a technology leadership market even as volume growth migrates toward China and India.

Competitive Landscape

The global ultraviolet curable resin market exhibits a moderately consolidated competitive structure at the top tier, with a small number of large, vertically integrated chemical groups, including BASF SE, Arkema Group (Sartomer), Allnex Group, and Covestro AG, commanding disproportionate market share through formulation breadth, global supply chain infrastructure, and sustained R&D investment. Below this tier, the ultraviolet curable resin competitive landscape fragments across regional specialists, application-focused niche players, and emerging producers concentrated in Asia Pacific.

The primary bases of competition are technological differentiation in oligomer and monomer chemistry, speed of regulatory compliance documentation, and application engineering support capabilities. Strategic priorities across leading participants include backward integration into specialty monomer production, co-development of bio-based and low-migration formulations, and geographic capacity expansion in high-growth Asia Pacific markets. Consolidation activity is expected to intensify through 2027 as tier-one players acquire niche innovators in high-value verticals, including 3D printing photopolymers and medical-grade UV adhesives.

Key Developments

- March, 2025: Allnex Group announced the commercial launch of a new series of aliphatic urethane acrylate oligomers specifically engineered for LED-UV curing systems in flexible electronics and optical bonding applications, targeting automotive display and wearable device OEMs across Asia Pacific and North America.

- November, 2024: Arkema Group (Sartomer) expanded its Nanoresins product line with the introduction of nanosilica-modified UV curable oligomers, delivering a 40% improvement in scratch resistance for premium wood and furniture coatings, reinforcing the company's leadership in high-performance surface coating formulations.

- July, 2024: Covestro AG disclosed a strategic partnership with a leading European automotive tier-one supplier to develop next-generation UV curable structural adhesives for electric vehicle battery module assembly, positioning the company at the intersection of the automotive electrification and ultraviolet curing technology growth vectors.

Ultraviolet Curable Resin Market -Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 4.83 Billion |

| Current Market Value (2026) | US$ 6.70 Billion |

| Projected Market Value (2033) | US$ 10.90 Billion |

| CAGR (2026 - 2033) | 7.2% |

| Leading Region | Asia Pacific (38%) |

| Dominant Resin Type | Acrylated Epoxies (30.0%) |

| Top-Ranking Composition | Monomers (45.0%) |

| Top-Ranking Application | Coatings (40.0%) |

| Top-Ranking End-Use | Electronics & Electrical (29.0%) |

| Incremental Opportunity (2026 - 2033) | US$ 4.20 Billion |

Companies Covered in Ultraviolet Curable Resin Market

- BASF SE

- Arkema Group

- Allnex Group

- Covestro AG

- Royal DSM

- IGM Resins B.V.

- Dymax Corporation

- DIC Corporation

- Toagosei Co., Ltd.

- Wanhua Chemical Group Co., Ltd.

- Resonac Holdings Corporation

- Miwon Specialty Chemical Co., Ltd.

- Eternal Materials Co., Ltd.

- Jiangsu Litian Technology Co., Ltd.

- Nippon Gohsei (Mitsubishi Chemical Group)

- Evonik Industries AG

- Rahn AG

- Cytec Industries Inc. (Solvay)

- Shin-Nakamura Chemical Co., Ltd.

- Nuplex Industries Ltd.

Frequently Asked Questions

The ultraviolet curable resin market size is valued at US$ 6.70 Billion in 2026 and is projected to reach US$ 10.90 Billion by 2033, growing at a CAGR of 7.2%.

Growth is driven by strict VOC regulations and rising demand from electronics and EV manufacturing, where UV curing offers faster processing, precision, and efficiency compared to traditional solvent-based systems.

Acrylated Epoxies hold the largest share at 30.0% in 2026 due to superior hardness, chemical resistance, and adhesion, making them essential for coatings, printing inks, and electronics protection applications.

Asia Pacific leads with 38.0% share in 2026, driven by strong electronics manufacturing, semiconductor production, and expanding automotive industry, especially EV growth across China, Japan, South Korea, and India.

Key opportunities lie in customized UV resins for 3D printing and medical adhesives, where high growth and early product specification create strong competitive advantages and long-term customer retention.

Leading companies include BASF, Arkema, Covestro, Allnex, and DSM. The market is competitive, with focus on innovation, product performance, and strategic partnerships to capture high-growth application segments.