- Clothing, Footwear, & Accessories

- Mineral Wool Market

Mineral Wool Market Size, Share, and Growth Forecast, 2026 - 2033

Mineral Wool Market by Product Type (Glass Wool, Stone Wool, Others), End-use Industry (Building and Construction, Industrial, Others), Product Form, and Regional Analysis for 2026 - 2033

Mineral Wool Market Size and Trends Analysis

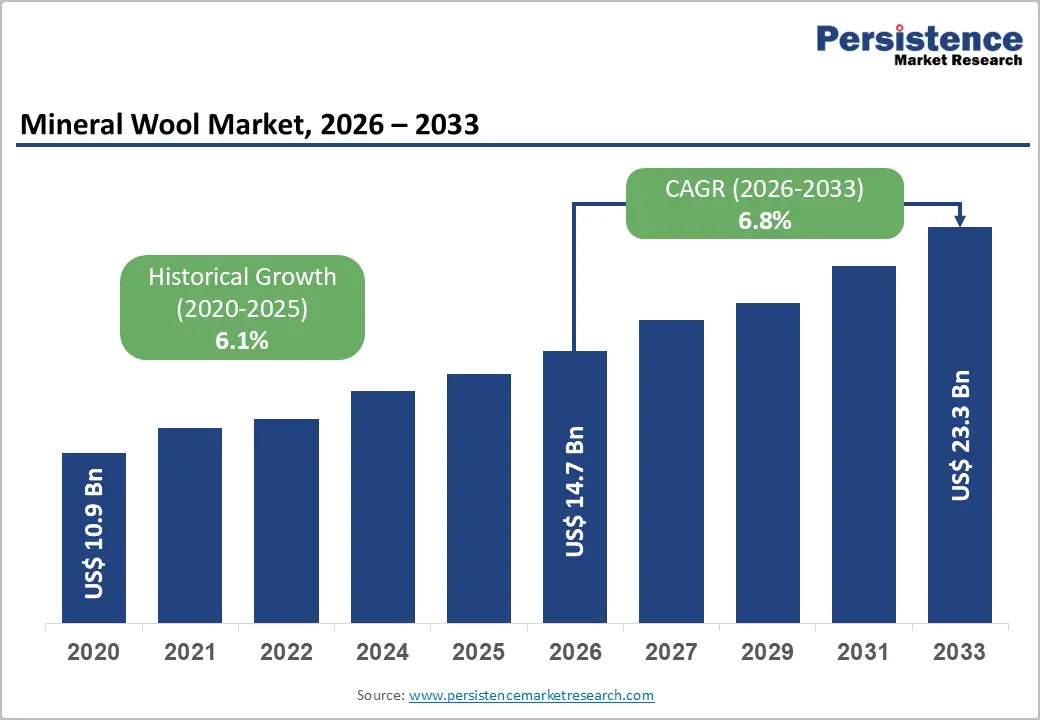

The global mineral wool market size is likely to be valued at US$14.7 billion in 2026 and is expected to reach US$23.3 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033, driven primarily by expanding construction-sector retrofit and new-build activity, tightening building energy-efficiency and fire-safety regulations, and rising industrial insulation requirements.

Cost volatility in raw materials and energy inputs continues to shape supply-side dynamics, while regional capacity expansions influence competitive positioning. Asia Pacific leads global consumption, supported by large-scale construction pipelines, rapid urbanization, and sustained industrialization across major economies.

Key Industry Highlights

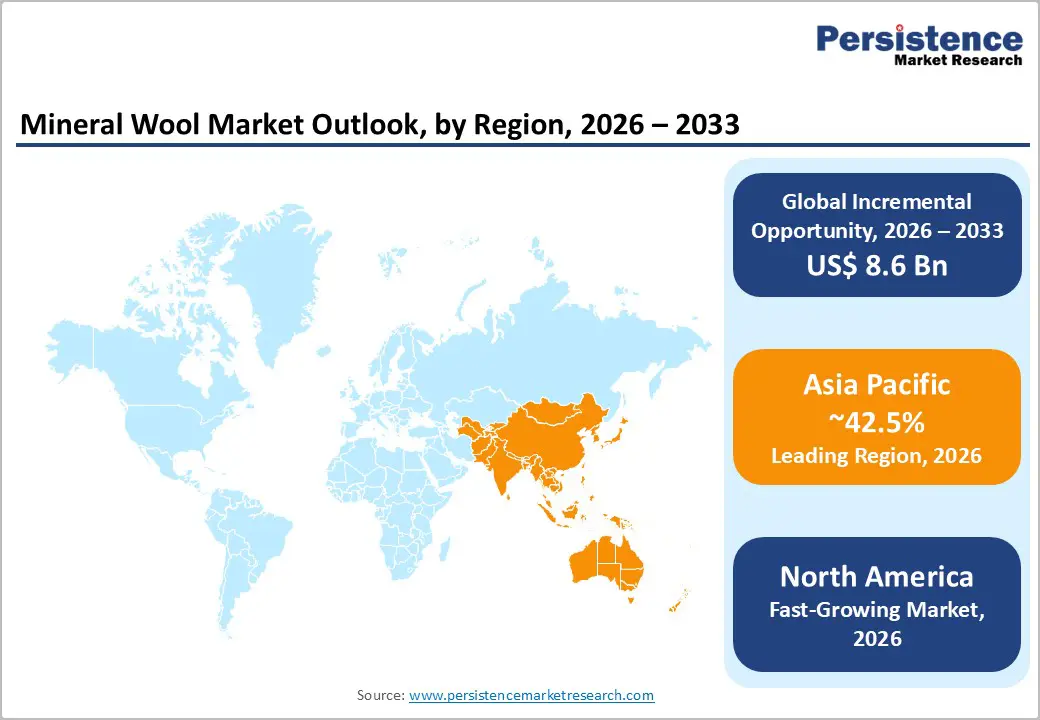

- Leading Region: Asia Pacific is projected to hold 42.5% share in 2026, driven by large-scale construction activity in China, India’s affordable housing programs, and infrastructure development across Southeast Asia.

- Fastest-Growing Region: North America, to be supported by premium product demand, aggressive building retrofit programs, and higher penetration of stone wool in fire-rated and industrial applications.

- Investment Plans: Capacity expansion and modernization concentrated in Asia Pacific and North America, with a strong focus on stone wool boards, recycled-content products, and low-energy manufacturing processes to serve higher-margin façade and industrial segments.

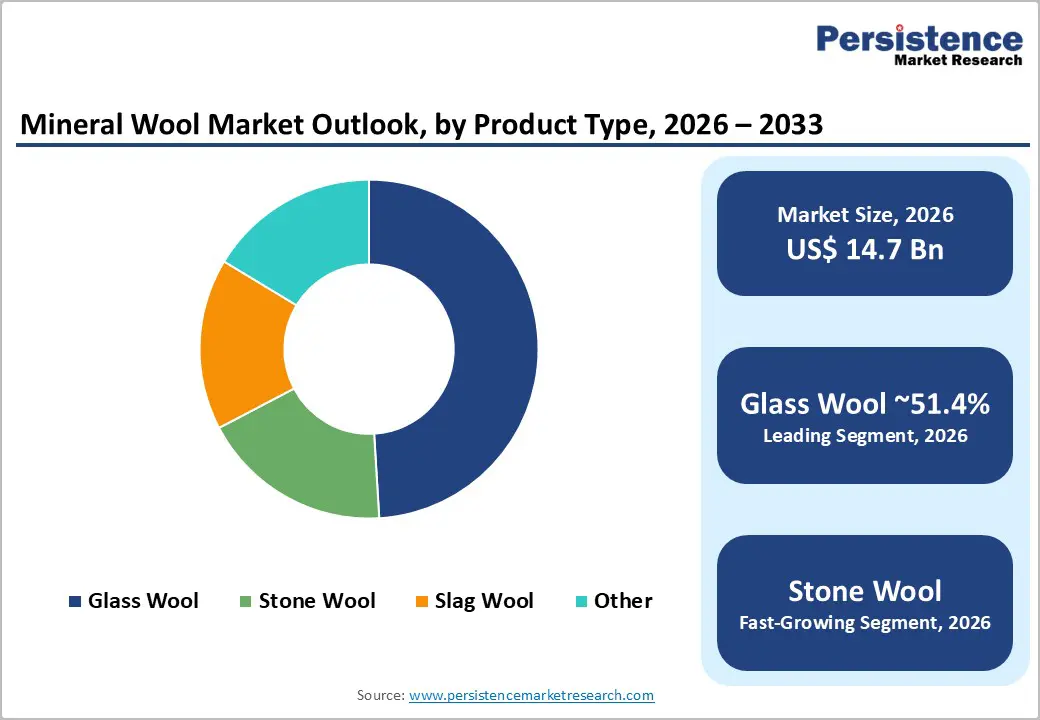

- Dominant Product Type: Glass wool is anticipated to hold 51.4% market share in 2026, maintaining its leadership position due to its cost competitiveness, lightweight handling, and widespread use in residential and commercial insulation.

- Leading End-use Industry: Building & construction is estimated to account for 56.7% of the market in 2026, driven by building code upgrades, energy-efficiency retrofits, and sustained residential and commercial construction activity.

| Key Insights | Details |

|---|---|

| Mineral Wool Market Size (2026E) | US$14.7 Bn |

| Market Value Forecast (2033F) | US$23.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory tightening on building energy performance

Stricter energy-efficiency standards and carbon-reduction targets across major economies are increasing insulated-envelope requirements for residential, commercial, and industrial buildings, thereby directly supporting mineral wool demand. Governments and regulatory authorities are strengthening minimum thermal performance benchmarks, façade fire-resistance requirements, and material safety standards, favoring non-combustible insulation materials over organic alternatives. Updated building codes and façade regulations in China, India, and several European countries have increased specification rates for mineral wool in both new construction and retrofit projects. These regulatory shifts are translating into measurable incremental demand, with policy-driven insulation upgrades contributing meaningfully to medium-term growth expectations for mineral wool products.

Retrofit Wave and Building Stock Decarbonization

A substantial global retrofit opportunity exists as aging building stock in developed and emerging economies requires insulation upgrades to meet energy-efficiency and emissions-reduction objectives. Public stimulus programs, green building incentives, tax credits, and performance-based subsidies are accelerating retrofit activity across residential and commercial segments. Mineral wool is frequently specified in retrofit applications due to its combined thermal insulation, acoustic performance, and fire resistance. Retrofit demand provides a steady, recurring revenue stream that is less cyclical than new construction, improving market stability and supporting long-term investment in capacity expansion, product innovation, and manufacturing modernization.

Industrial and Transport Insulation Growth

Industrial energy-efficiency initiatives and stricter safety regulations are driving increased adoption of high-performance mineral wool products, particularly stone wool, in high-temperature and high-risk environments. Applications include process insulation, sound attenuation in industrial facilities, fire-rated partitions, and equipment enclosures. The transport sector, including marine and rail infrastructure, is also expanding the use of mineral wool for thermal management, fire protection, and noise reduction in both new-builds and refurbishment projects. Growth in industrial and transport applications supports higher-margin product categories and diversifies demand beyond construction-driven cycles.

Barrier Analysis - Feedstock and Energy Cost Volatility

Mineral wool manufacturing is energy-intensive, relying on high-temperature melting and fiberization processes that are sensitive to fluctuations in electricity, natural gas, and coke prices. Volatility in energy and raw material costs can compress producer margins and lead to higher product prices, particularly in regions with limited energy cost pass-through. In price-sensitive markets, elevated costs may slow adoption, especially in residential projects where alternative insulation materials are permitted.

Competitive Substitution and Perception Barriers

Mineral wool competes with alternative insulation materials such as polyurethane, expanded polystyrene, cellular glass, and composite insulation panels. In certain markets, lower upfront costs for materials or integrated panel systems are preferred due to faster installation and simplified logistics. Misconceptions regarding handling characteristics, dust generation, and end-of-life disposal can deter adoption, particularly in regions with limited installer training and waste-management infrastructure. These structural challenges can constrain market share expansion despite mineral wool’s superior fire resistance and acoustic performance, potentially reducing growth in price-sensitive segments by 1-2 percentage points of CAGR.

Opportunity Analysis - High-Value Specialty Products and Circular Manufacturing

Significant growth potential exists in premium mineral wool products incorporating low-dust formulations, bio-based binders, and higher recycled content. These innovations align with sustainability-focused procurement criteria and occupational health requirements, particularly in public-sector and large commercial projects. Manufacturers that successfully reduce production energy intensity and increase circular material usage can command green-spec premiums and secure long-term supply contracts. Premium and specialty mineral wool products could generate 8-12% incremental average selling price uplift and account for 5-8% of total market value by 2030 in advanced regulatory environments.

Emerging Markets and Affordable Housing Programs

Rapid urbanization and government-led affordable housing initiatives across Asia and parts of Latin America present a large addressable market for cost-effective glass wool insulation. Volumetric housing, mass residential developments, and public infrastructure projects favor insulation solutions that balance performance with affordability. Even conservative adoption scenarios indicate that affordable housing programs could add several percentage points to annual global volume demand over the next decade. Strategic investments in local manufacturing, long-term supply agreements, and optimized product formulations can unlock scale efficiencies and logistics advantages.

Category- wise Analysis

Product Type Insights

Glass wool is anticipated to remain the leading product type by volume and value, accounting for approximately 51.4% of market share. Its leadership is supported by cost competitiveness, lightweight handling characteristics, and broad applicability across building insulation systems, including cavity walls, suspended ceilings, pitched roofs, and HVAC ducting. Large-scale continuous manufacturing processes enable high output efficiency and stable pricing, particularly in Asia Pacific and Europe, where established players operate integrated production and distribution networks. Ongoing product enhancements, such as low-dust binders, formaldehyde-free formulations, and improved thermal conductivity per unit thickness, continue to strengthen adoption in both new construction and retrofit projects. For example, glass wool is widely specified in residential energy-efficiency retrofits under European building renovation programs and in mass-housing developments across India and Southeast Asia, where ease of installation and cost control remain critical procurement criteria.

Stone wool is projected to be the fastest-growing product type, driven by its non-combustible nature, higher density, and superior acoustic and thermal performance. These attributes make stone wool increasingly preferred for fire-sensitive façades, high-rise buildings, industrial facilities, and high-temperature insulation environments. Regulatory tightening around fire safety, particularly following façade fire incidents in Europe and parts of Asia, has accelerated material substitution toward stone wool in external wall insulation systems. Stone wool’s higher average selling prices and performance-driven demand support above-market revenue growth, especially in applications such as industrial pipe insulation, petrochemical plants, and commercial façades. As safety compliance and lifecycle performance become central to specification decisions, stone wool continues to capture a rising share of market value, gradually shifting the overall revenue mix toward higher-margin mineral wool products.

End-use Industry Insights

The building and construction sector is anticipated to remain the dominant end-use segment, accounting for approximately 56.7% of market share. This segment utilizes a wide range of mineral wool forms, including boards, blankets, and rolls, for thermal insulation material, acoustic control, and passive fire protection across residential, commercial, and institutional buildings. Demand is underpinned by stricter building energy codes, façade fire-safety regulations, and large-scale retrofit initiatives aimed at reducing operational energy consumption. Residential renovation programs in Europe, commercial office developments in China, and urban housing projects across India exemplify sustained volume demand. Mineral wool is increasingly specified in external wall insulation systems, roofing assemblies, and interior partitions, where compliance with fire, sound, and energy-efficiency standards is mandatory. These factors contribute to predictable procurement cycles and stable long-term consumption patterns.

The industrial segment is anticipated to be the fastest-growing end-use category, driven by expanding applications in power generation, petrochemical processing, manufacturing facilities, marine engineering, and shipbuilding. Industrial insulation requirements demand high technical performance, including resistance to extreme temperatures, fire containment, corrosion protection, and sound attenuation. Mineral wool, particularly stone wool, is increasingly specified for boilers, furnaces, pipelines, and offshore installations. These applications support higher average selling prices and favor suppliers capable of delivering engineered insulation systems and technical installation support. Longer project lifecycles, combined with regulatory enforcement of workplace safety and energy-efficiency standards, create durable, high-margin growth opportunities. Industrial demand is especially strong in the Asia Pacific and the Middle East, where capacity expansions in energy-intensive industries continue to drive insulation investments.

Regional Insights

North America Mineral Wool Market Trends - Code-Driven Retrofits, Industrial Fire Protection, and Premium Specifications

North America is likely to be the fastest-growing market, driven by accelerated retrofit activity, widespread green building adoption, and rising industrial insulation demand. Although Asia Pacific leads global consumption by volume, North America records strong revenue growth per unit, reflecting its premium product mix, higher performance specifications, and compliance-driven procurement. The U.S. dominates regional demand, supported by federal and state-level energy-efficiency programs, infrastructure modernization, and continuous updates to building and fire safety codes. Canada contributes incremental demand, particularly from industrial facilities and cold-climate residential construction. In the U.S., updated International Energy Conservation Code (IECC) requirements and state-level energy codes, such as California’s Title 24, have increased the use of mineral wool in wall assemblies, façades, and roofing systems. These regulations favor materials offering combined thermal performance, acoustic insulation, and fire resistance, positioning mineral wool ahead of combustible alternatives. Leading manufacturers such as Owens Corning, Johns Manville (a Berkshire Hathaway company), and ROCKWOOL North America have expanded certified product portfolios to meet evolving code requirements for high-rise residential and mixed-use developments.

Industrial demand is strengthening alongside public infrastructure investment and reshoring trends in manufacturing. Mineral wool is increasingly specified for power plants, LNG terminals, refineries, and advanced manufacturing facilities, where fire containment and high-temperature resistance are critical. ROCKWOOL’s industrial insulation solutions and Johns Manville’s engineered systems are frequently specified in energy and process industries, reinforcing the region’s shift toward higher-margin applications. Manufacturers offering technical design support and pre-certified façade assemblies are particularly well positioned to secure public-sector, healthcare, and large commercial projects, sustaining North America’s above-average revenue growth trajectory.

Europe Mineral Wool Market Trends - Regulatory Compliance, Façade Fire Safety, and Decarbonized Production

Europe represents a mature, regulation-intensive market, characterized by high per-capita insulation consumption, advanced technical standards, and strong policy alignment with energy efficiency and fire safety objectives. Germany leads the region in industrial insulation demand and manufacturing sophistication, while large-scale building retrofit programs and façade compliance requirements heavily drive the U.K. and France. Spain exhibits steady growth, supported by residential renovation activity and construction in the hospitality sector.

European Union directives, such as the Energy Performance of Buildings Directive (EPBD), and post-Grenfell fire safety reforms in the U.K. have significantly increased demand for non-combustible insulation materials, reinforcing mineral wool’s role in façades, external wall insulation systems, and public buildings. Countries such as Germany and France enforce strict fire classification and acoustic performance standards, which consistently favor stone wool and high-density glass wool products.

Major European producers, including ROCKWOOL Group, Saint-Gobain (ISOVER), Knauf Insulation, and URSA, play a central role in shaping market dynamics. These companies have invested heavily in product certification, digital design tools, and system-based insulation solutions to align with national and EU-wide compliance frameworks. Harmonized EN standards facilitate cross-border trade, yet the high cost of compliance and certification favors large, well-capitalized manufacturers over smaller entrants.

Sustainability has become a defining investment theme across Europe. Leading producers are prioritizing manufacturing decarbonization, the electrification of melting processes, the use of recycled raw materials, and waste-heat recovery systems. These initiatives support alignment with EU climate targets while enhancing brand positioning in publicly funded retrofit programs. Export opportunities remain strong for certified façade and acoustic systems that meet government-backed renovation schemes, particularly in Northern and Western Europe, reinforcing Europe’s role as a technology and standards benchmark for the global mineral wool industry.

Asia Pacific Mineral Wool Market Trends - High-Volume Construction, Glass Wool Dominance, and Regional Manufacturing Scale

Asia Pacific leads the market with approximately 42.5% share, driven by sustained construction activity in China, rapid urbanization in India, and infrastructure expansion across Southeast Asia. High construction volumes, price sensitivity, and fast project execution timelines favor glass wool adoption for mass residential and commercial applications, while stone wool penetration continues to rise in premium, fire-sensitive, and industrial projects. China remains the region’s largest consumer, supported by urban redevelopment programs, public infrastructure investment, and green building certification initiatives. Large domestic and multinational players, including Saint-Gobain, Knauf Insulation, and ROCKWOOL, operate manufacturing bases in China to serve both domestic demand and regional exports. Glass wool dominates residential and commercial insulation, while stone wool is increasingly specified in public buildings, transport infrastructure, and industrial facilities where fire resistance is mandatory.

Japan’s market is shaped by strict fire safety regulations, seismic-resilient construction standards, and high-quality building practices. Mineral wool is widely used in high-rise residential towers, commercial developments, and industrial facilities, with a strong emphasis on system performance and long-term durability. Domestic manufacturers and global brands focus on high-specification products rather than volume-driven growth. India represents one of the fastest-growing markets within Asia Pacific, driven by urban housing programs, expanding commercial real estate, and tightening energy-efficiency norms. Demand is supported by government-backed construction initiatives and rising awareness of thermal comfort in hot climates. Southeast Asian countries, including Indonesia, Vietnam, and Thailand, are emerging growth hubs, benefiting from manufacturing investments and export-oriented industrial development.

Across the Asia Pacific, manufacturers continue to expand regional capacity, localize production, and optimize logistics to capture volume growth and reduce cost volatility. The region’s scale advantages, combined with rising regulatory standards, ensure Asia Pacific remains both the largest consumption base and a critical manufacturing hub for the global mineral wool market.

Competitive Landscape

The global mineral wool market is moderately consolidated, with a limited number of global leaders accounting for a significant share of premium product revenues, alongside a broad base of regional and local manufacturers serving cost-sensitive segments. The top tier of producers collectively holds a substantial portion of the market, while niche players compete in specialized applications. Competitive advantage increasingly depends on system-level solutions, sustainability credentials, and the ability to meet stringent certification and performance requirements.

Recent strategic activity includes capacity expansions focused on stone wool boards in high-growth regions, technology partnerships to improve sustainability and installer safety, and regional consolidation through acquisitions that enhance distribution reach and product portfolios. These initiatives reflect an industry-wide emphasis on premiumization, local supply resilience, and operational scale.

Leading companies emphasize product innovation, regional cost leadership, and integrated system offerings. Differentiation is achieved through circular manufacturing, technical service capabilities, and rapid project support. Emerging business models include long-term service agreements for industrial insulation maintenance.

Key Industry Developments

- In November 2025, Sarda Metals & Alloys Limited launched RHINO, India’s greenest rock mineral wool insulation, at the Green Building Congress 2025. Designed to deliver high fire safety, energy efficiency, and reduced CO2 emissions for building, industrial, and marine applications, it addresses rising sustainability demands.

- In August 2025, Kingspan launched its K-Roc™ mineral wool insulated wall and ceiling panels, locally produced in Australia to reduce lead times and serve regional construction needs with high thermal and fire performance.

Companies Covered in Mineral Wool Market

- ROCKWOOL Group

- Saint-Gobain (ISOVER)

- Owens Corning

- Knauf Insulation

- Johns Manville

- Paroc Group

- URSA Insulation

- Izocam

- USG Boral

- TechnoNICOL

- Kingspan Group

- NICHIAS Corporation

- KCC Corporation

- Beijing New Building Material (BNBM)

- Uralita Group

- Rock Wool Manufacturing Company (RWM)

- Superglass Insulation

- GAF Materials

Frequently Asked Questions

The global mineral wool market size is valued at US$14.7 billion in 2026.

By 2033, the mineral wool market is expected to reach US$23.3 billion.

Key trends include rising adoption of non-combustible insulation materials, increased focus on building retrofits for energy efficiency, growing use of stone wool in fire-sensitive and industrial applications, and investment in low-carbon and recycled-content mineral wool products.

Glass wool is the leading product type, accounting for approximately 51.4% market share, owing to its cost efficiency, lightweight properties, and widespread use in residential and commercial building insulation.

The mineral wool market is projected to grow at a CAGR of 6.8% between 2026 and 2033.

Major players include ROCKWOOL Group, Saint-Gobain (ISOVER), Knauf Insulation, Owens Corning, and Johns Manville (Berkshire Hathaway).