- Advanced Materials

- FGD Gypsum Market

FGD Gypsum Market Size, Share, and Growth Forecast 2026 – 2033

FGD Gypsum Market by Application (Wallboard/Drywall, Cement, Soil Amendments, Water Treatment, Others), by End-Use Industry (Construction, Agriculture, Others), and Regional Analysis for 2026–2033

FGD Gypsum Market Size and Trend Analysis

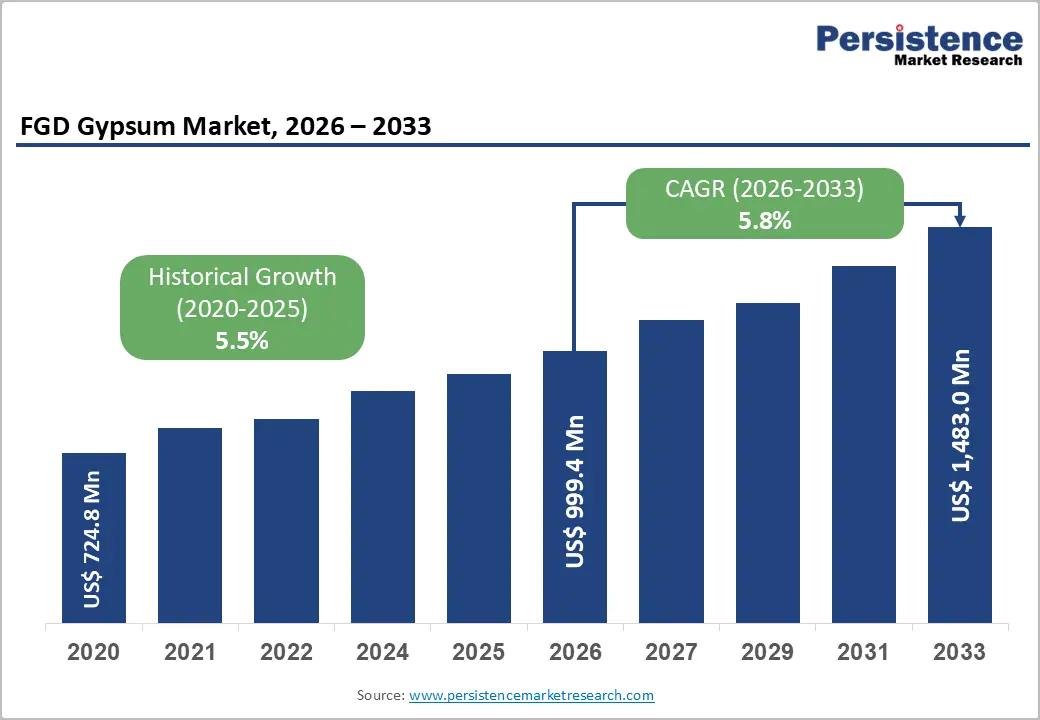

The global FGD Gypsum market size is valued at US$ 999.4 Mn in 2026 and is projected to reach US$ 1,483.0 Mn by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

The FGD gypsum market is on a structurally sound growth trajectory, driven by the material's unique position as a high-purity byproduct of coal-fired power plant flue gas desulfurization, a process mandated globally by air quality regulations, which simultaneously generates a synthetic gypsum supply while aligning with circular economy priorities that are reshaping construction material procurement. The sustained global demand for wallboard and drywall in residential and commercial construction, combined with FGD gypsum's cost and quality advantages over mined natural gypsum, underpins consistent volume absorption.

Key Market Highlights

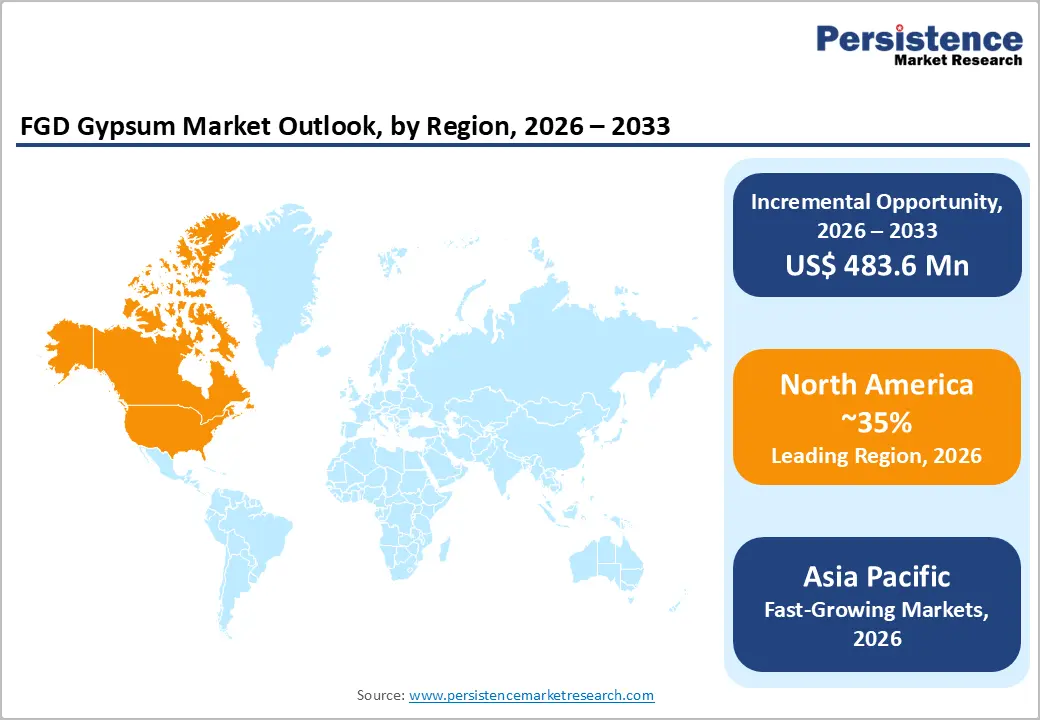

- Leading Region: North America leads the global FGD Gypsum market, holding approximately 35% of global revenue in 2025, with the U.S. ACAA-certified supply chain delivering over 33 million tons for wallboard manufacturing.

- Fastest Growing Region: Asia Pacific is the fastest-growing region through 2033, driven by China's MIIT-mandated 70%+ FGD gypsum utilization targets, India's accelerating FGD scrubber installation program under MoEFCC emission norms, and the rapid expansion of wallboard demand across Southeast Asian construction markets.

- Leading Segment: Wallboard/Drywall dominates the Application category with approximately 58% market share in 2025, reflecting FGD gypsum's technical equivalency to natural gypsum in wallboard production and the structural cost advantage that has made it the preferred input for leading manufacturers, including USG, Saint-Gobain, Knauf, and National Gypsum.

- Fastest Growing Segment: Agriculture is the fastest-growing application segment, underpinned by USDA-certified agronomic benefits including up to 25% root penetration improvement, calcium-sulfur nutrient delivery for deficient Midwestern soils, and expanding extension service programs systematically converting corn and soybean farmers to FGD gypsum soil amendment adoption.

- Key Opportunity: The most significant market opportunity lies in India's emerging FGD gypsum supply chain development, as MoEFCC scrubber mandates generate millions of tonnes of new production, meeting ready-made wallboard absorption demand through Saint-Gobain India and Holcim India operations, with circular economy policy frameworks reinforcing commercial utilization over costly landfill disposal.

DRO Analysis

Market Growth Drivers

Flue Gas Desulfurization Mandates Generating Reliable High-Purity Synthetic Gypsum Supply

Environmental regulations requiring sulfur dioxide (SO?) controls at coal-fired power plants constitute the primary supply catalyst for the FGD gypsum market, generating a consistent, high-volume byproduct stream for wallboard, cement, and agricultural applications. In the United States, the U.S. Environmental Protection Agency’s Clean Air Act provisions, including the Acid Rain Program and the Cross-State Air Pollution Rule (CSAPR), have driven near-universal deployment of FGD scrubbers across the coal fleet.

The American Coal Ash Association (ACAA) reports that recent annual FGD gypsum output in the U.S. has been approximately 33 million tons. In China, the Ministry of Ecology and Environment’s ultra-low emission standards cap SO? concentrations below 35 mg/Nm3, producing substantial volumes that are increasingly redirected from disposal to commercial utilization through government-supported industrial symbiosis initiatives.

Construction Sector Demand for Wallboard Driven by Residential and Commercial Development

The global construction industry's sustained demand for gypsum wallboard, the primary application consuming FGD gypsum, provides a durable and high-volume absorption channel that underpins market revenue growth. USG Corporation, Saint-Gobain, Knauf, and National Gypsum have each invested in FGD gypsum-capable manufacturing infrastructure precisely because the material's consistent purity (CaSO?·2H?O content typically exceeding 94%) enables direct substitution for mined gypsum without reformulation.

In the United States, housing construction activity, with 1.6 million new starts recorded in 2024 (per U.S. Census Bureau), creates persistent wallboard demand that is predominantly met by FGD gypsum-incorporating products. In India, the Pradhan Mantri Awas Yojana-Urban (PMAY-U) housing program's sanction of 1.18 crore houses and Europe's social housing investment programs are similarly generating long-horizon construction demand that directly benefits FGD gypsum wallboard manufacturers.

Market Restraints

Structural Decline of Coal Power Generation Threatening FGD Gypsum Supply

The accelerating global transition away from coal-fired power generation, driven by climate policy, renewable energy cost deflation, and national decarbonization commitments, poses the most significant structural risk to FGD gypsum supply over the forecast horizon and beyond. The International Energy Agency (IEA)'s World Energy Outlook projects coal's share of global electricity generation declining from 36% in 2022 to below 20% by 2035 under stated policy scenarios, with steeper declines under net-zero pathways.

As coal plants are retired, particularly in the European Union, where Germany, the Netherlands, and Belgium have committed to a full coal phase-out by 2030–2038, FGD gypsum production volumes in those markets will structurally decline, creating supply gaps that natural gypsum mining or alternative synthetic sources must fill.

Logistics and Quality Variability Challenges in FGD Gypsum Handling and Transport

FGD gypsum presents handling, storage, and transport challenges that add cost and complexity relative to natural gypsum, particularly for wallboard manufacturers sourcing material from multiple power plants with variable production quality. FGD gypsum is typically generated as a high-moisture slurry (free moisture 8–15%) requiring dewatering and drying before use, adding processing steps and energy costs.

Unlike quarried gypsum with consistent mineralogy, FGD gypsum quality varies by coal composition, scrubber technology, and operating parameters, requiring incoming quality testing at receiving plants. Transportation logistics, moving large volumes from geographically fixed power plant locations to geographically concentrated wallboard manufacturing facilities, create supply chain concentration risks and freight cost exposure that can undermine the material cost advantage over locally quarried natural gypsum.

Market Opportunities

Agricultural FGD Gypsum as a High-Value Soil Amendment in Intensive Farming Markets

The agricultural use of FGD gypsum as a calcium-sulfur soil amendment represents one of the fastest-growing and highest-margin demand channels, enabling producers to diversify revenues beyond construction cycles. Research from the U.S. Department of Agriculture (USDA) and Ohio State University documents measurable agronomic benefits, including improved soil structure through reduced compaction and crusting, enhanced water infiltration, and root penetration increases of up to 25%.

The American Coal Ash Association (ACAA) has certified FGD gypsum as suitable for agricultural use under defined purity protocols, thereby reducing regulatory constraints on adoption. As sulfur deficiency becomes more prevalent, particularly as atmospheric sulfur deposition declines following SO2 emission controls, the agronomic value proposition for FGD gypsum continues to strengthen alongside expanding byproduct availability.

Circular Economy Policy Frameworks Mandating Industrial Byproduct Utilization in Construction

Strengthening circular economy legislation across the European Union, China, and South Korea is institutionalizing FGD gypsum utilization by discouraging landfilling and encouraging construction manufacturers to adopt certified secondary raw materials. In the EU, the Packaging and Packaging Waste Regulation (PPWR), alongside Circular Economy Action Plan objectives, is increasing pressure on supply chains to demonstrate circular sourcing and material traceability, for which FGD gypsum offers a clear, auditable pathway from power plant to finished wallboard.

China's Ministry of Industry and Information Technology (MIIT) has issued specific industrial solid waste utilization targets requiring power companies to achieve FGD gypsum utilization rates above 70%, directly stimulating commercial off-take agreements between power producers and gypsum product manufacturers. These policy drivers are creating a government-backed structural demand incentive that complements market-led consumption growth.

Category-wise Insights

Application Analysis

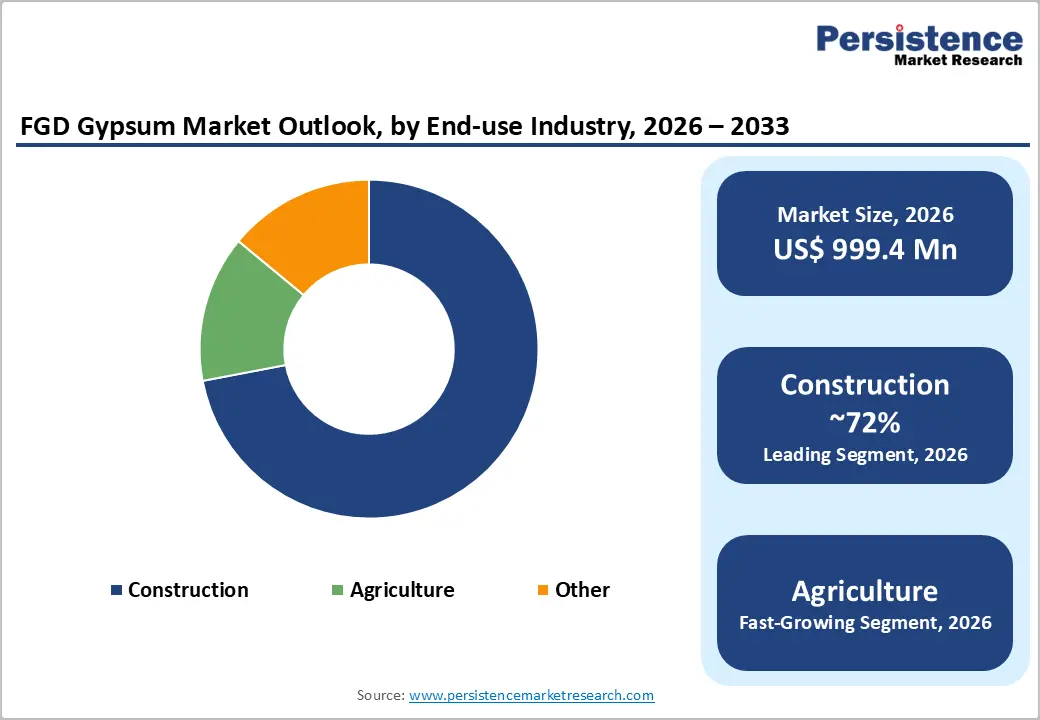

The Wallboard/Drywall application segment dominates the global FGD Gypsum market, commanding approximately 58% of total market share in 2025. This leadership reflects gypsum wallboard's position as the universal interior partition and ceiling material across residential, commercial, and industrial construction globally, combined with FGD gypsum's technical equivalency to, and cost advantages over, mined natural gypsum in wallboard manufacturing. Saint-Gobain's Gyproc product lines, USG Corporation's SHEETROCK brand, and Knauf's global wallboard portfolio all incorporate FGD gypsum as a primary input, reflecting the industrial scale of this application.

End-Use Industry Analysis

The Construction sector is the dominant end-use industry for FGD gypsum, representing approximately 72% of the total market share in 2025. Construction's commanding position reflects the combined volume of wallboard and cement applications, both construction-serving, and the sector's structural reliance on consistent, high-purity gypsum supply at the scale and cost point that FGD gypsum uniquely provides.

Eagle Materials, American Gypsum, and PABCO Gypsum have specifically structured their manufacturing networks around FGD gypsum supply agreements with power utilities to ensure cost-competitive and geographically reliable input sourcing. The Agriculture end-use segment is the fastest-growing category, driven by documented soil amendment efficacy and expanding USDA and extension service outreach programs educating farmers on FGD gypsum's agronomic benefits.

Regional Analysis

North America FGD Gypsum Market Trends & Analysis

North America is the largest and most mature regional market for FGD gypsum, holding approximately 35% of global revenue in 2025, underpinned by the U.S.'s comprehensive Clean Air Act-driven FGD scrubber adoption. The region is simultaneously experiencing the early stages of supply constraint as coal plant retirements, accelerated by the EPA's power plant greenhouse gas rules, begin to reduce FGD gypsum production volumes in specific states, incentivizing manufacturers to strengthen long-term supply agreements and quality monitoring protocols.

U.S. FGD Gypsum Market Size

The U.S. FGD Gypsum market is valued at approximately US$ 315 Mn in 2025, anchored by the country's 33 million tons of annual FGD gypsum production, the world's largest national output, and a wallboard manufacturing industry that is the primary consumer.

Europe FGD Gypsum Market Trends, Drivers & Insights

Europe holds approximately 22% of the global FGD Gypsum market revenue in 2025, with demand anchored in Germany, the U.K., Poland, and the Netherlands, nations with large coal fleet FGD installations, and supply increasingly concentrated among a declining number of operating plants as the region's coal phase-out accelerates. The region's circular economy policy framework, particularly the EU Circular Economy Action Plan, is providing institutional support for FGD gypsum utilization over landfilling, sustaining demand even as supply volumes gradually contract.

Germany FGD Gypsum Market Size

Germany's FGD Gypsum market is valued at approximately US$ 68 Mn in 2025, historically anchored in the country's large lignite and hard coal power fleet that generates substantial FGD gypsum volumes. Germany's Knauf Gips KG, headquartered in Iphofen, Bavaria, has built a European gypsum products empire substantially supported by FGD gypsum from domestic and Eastern European power plants.

U.K. FGD Gypsum Market Size

The U.K. FGD Gypsum market is valued at approximately US$ 42 Mn in 2025, with British Gypsum (Saint-Gobain) representing the primary commercial utilizer of FGD gypsum from Drax Power Station, the UK's largest power plant and FGD gypsum producer, in its Robertsbridge and East Leake wallboard manufacturing facilities.

France FGD Gypsum Market Size

France's FGD Gypsum market, with US$ 29 Mn in 2025, is modest but structurally supported by Saint-Gobain's domestic wallboard manufacturing operations and the country's low coal power dependency, which limits domestic FGD gypsum production but creates import-dependent demand.

Asia Pacific FGD Gypsum Market Drivers & Analysis

Asia Pacific is the fastest-growing regional market for FGD gypsum, representing approximately 34% of global revenue in 2025 and projected to grow at the fastest regional CAGR through 2033. China dominates the regional landscape as both the world's largest FGD gypsum producer, generating an estimated 80-100 million tons annually from its massive coal fleet, and a rapidly developing commercial utilization market.

China FGD Gypsum Market Size

China's FGD Gypsum market is valued at approximately US$ 168 Mn in 2025, reflecting both the country's unparalleled production volume and its government-mandated utilization push that has elevated commercial consumption from disposal to commodity status. China's 14th Five-Year Plan explicitly targets industrial solid waste reduction, with FGD gypsum identified as a priority secondary resource.

India FGD Gypsum Market Size

India's FGD Gypsum market is valued at approximately US$ 48 Mn in 2025 and represents one of the highest-growth opportunities globally, as the country is in the early stages of mandating FGD scrubber installation across its large coal power fleet. The Ministry of Environment, Forest and Climate Change (MoEFCC) has issued emission norms requiring SO? controls at coal plants, with compliance deadlines repeatedly extended but ultimately directing substantial FGD scrubber capital investment.

Japan FGD Gypsum Market Size

Japan's FGD Gypsum market is a mature and highly efficient ecosystem, estimated at approximately US$ 38 Mn in 2025, with near-100% FGD gypsum utilization rates achieved through decades of industrial coordination between power utilities and Yoshino Gypsum, Japan's dominant wallboard manufacturer with plants strategically co-located near major FGD gypsum-producing power stations.

Competitive Landscape

Market Structure Analysis

The global FGD Gypsum market exhibits a moderately consolidated structure, with a small number of integrated gypsum product manufacturers, including USG Corporation (Knauf), Saint-Gobain, Knauf Gips KG, National Gypsum, and Eagle Materials, commanding dominant positions in wallboard end-markets while simultaneously acting as the primary commercial buyers of FGD gypsum from power utilities. Key competitive differentiators include long-term supply agreements with coal power operators, geographic co-location of manufacturing with FGD gypsum production, quality certification capabilities, and product diversification into agricultural markets.

Key Market Developments

March 2025: Knauf announced expanded FGD gypsum procurement agreements with Central European power utilities, securing long-term supply for its wallboard manufacturing facilities in Germany, Poland, and the Czech Republic ahead of anticipated coal phase-out supply contraction through 2030.

October 2025: Saint-Gobain completed a US$240+ million expansion of its CertainTeed Gypsum facility in Palatka, Florida, doubling production capacity and making it the largest gypsum wallboard plant globally, targeting growing demand in the southeastern U.S.

May 2025: Eagle Materials announced a US$330 million investment to modernize and expand its gypsum wallboard plant in Oklahoma, targeting a 25% capacity increase and approximately 20% reduction in operating costs to strengthen its competitive position.

Top Companies in the FGD Gypsum Market

Saint-Gobain (Courbevoie, France) is the global leader in light and sustainable construction materials, with FGD gypsum-based wallboard manufactured under its CertainTeed brand across North America, Europe, and Asia. The company operates across more than 80 countries, with ongoing significant capital allocation to gypsum capacity expansion and sustainability-led product innovation.

USG Corporation / Knauf Gips KG (Iphofen, Germany), the combined entity is among the world's largest gypsum wallboard producers. Knauf leverages a global manufacturing network and deep FGD gypsum procurement relationships to supply diverse markets. The company commenced production at a new gypsum quarry in Michigan in 2024 to address supply diversification needs.

Eagle Materials Inc. (Dallas, Texas, USA) is a leading North American wallboard producer with a focused strategy centered on cost efficiency and production modernization. Its US$330 million Oklahoma plant expansion, announced in May 2025, signals strong confidence in long-term FGD gypsum wallboard market fundamentals and positions it for significant share gains in the U.S. interior construction market.

Companies Covered in FGD Gypsum Market

- USG Corporation (Knauf)

- Saint-Gobain

- Georgia-Pacific Gypsum

- National Gypsum Company

- Knauf Gips KG

- Lafarge Holcim (Holcim Group)

- Etex Group

- Eagle Materials Inc.

- Boral Ltd.

- Yoshino Gypsum Co. Ltd.

- PABCO Gypsum

- American Gypsum

- British Gypsum

- Beijing New Building Materials (BNBM)

- Jason Industries

Frequently Asked Questions

The global FGD Gypsum market is valued at US$ 999.4 Mn in 2026 and is projected to reach US$ 1,483.0 Mn by 2033, expanding at a CAGR of 5.8% during the forecast period.

The two primary drivers are EPA and international SO₂ emission mandates compelling FGD scrubber installation across coal power plants, which generate high-purity synthetic gypsum as a byproduct, and construction sector demand for gypsum wallboard, where FGD gypsum's consistent chemical purity exceeding 94% CaSO₄·2H₂O and competitive cost relative to mined natural gypsum have made it the preferred input material for leading manufacturers including USG, Saint-Gobain, and Knauf.

Wallboard/Drywall is the leading application segment with approximately 58% market share in 2025, reflecting gypsum wallboard's universal adoption as the standard interior construction material globally. FGD gypsum's technical equivalency to mined natural gypsum in wallboard manufacturing, validated through ACAA quality standards and decades of commercial use by major manufacturers, has enabled seamless substitution at an industrial scale, making wallboard the single largest FGD gypsum consumption channel.

North America leads with approximately 35% revenue share in 2025. The U.S. dominates North America through its 33 million tons of annual FGD gypsum production and the ACAA-certified supply chain connecting coal utilities to wallboard manufacturers.

India's emerging FGD gypsum supply chain represents the most compelling near-term opportunity. As MoEFCC emission norms compel FGD scrubber installations across India's large coal fleet, millions of tons of new high-purity synthetic gypsum supply will require commercial absorption channels.

The market is led by USG Corporation (now part of Knauf), Saint-Gobain, Knauf Gips KG, National Gypsum Company, and Eagle Materials, which collectively dominate North American and European FGD gypsum wallboard manufacturing through vertically integrated supply agreements with coal utilities. Yoshino Gypsum leads Japan's near-100% FGD gypsum utilization ecosystem, while Beijing New Building Materials (BNBM) and domestic Chinese producers are the primary consumers of China's massive FGD gypsum production volumes.