What’s Happening?

Many license applications are facing delays of up to two or three months, with a significant number being denied altogether. This move is widely seen as a strategic response to rising geopolitical tensions with the U.S. and European Union. The resulting uncertainty has triggered widespread disruptions, particularly in the automotive industry. While China has issued temporary six-month export licenses to suppliers for U.S. automakers like Ford, General Motors (GM), and Stellantis, the broader impact continues to reverberate across global supply chains, underscoring the industry's vulnerability to such policy shifts.

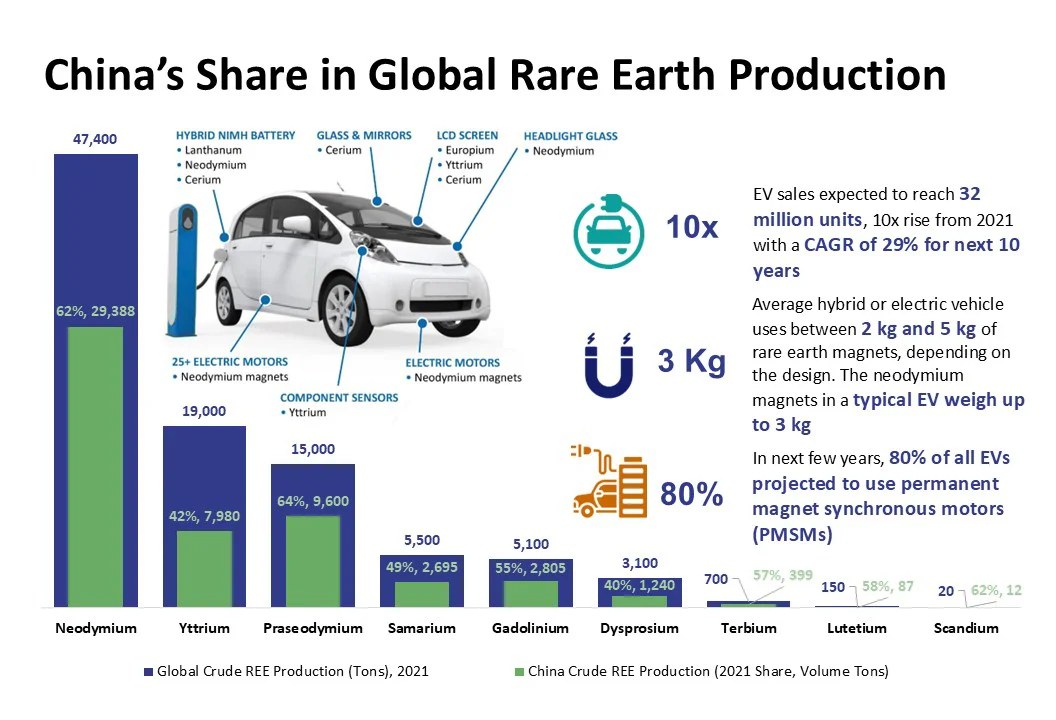

Why are Rare Earth Elements important in the Automotive Industry?

Rare earth elements are critical to the automotive industry, particularly for the production of electric and hybrid vehicles. They are used to manufacture neodymium-iron-boron (NdFeB) magnets, which are essential for electric motors due to their strong magnetic properties and efficiency. These magnets are found in EV powertrains, vehicle lighting, capacitors, and AI-driven chips, as noted by Automotive Manufacturing Solutions.

Rare earths power not just electric motors but also catalytic converters in ICE vehicles, high-precision sensors used in ADAS and autonomous features, and various electronic components such as speakers, capacitors, and display systems. Lanthanum plays a key role in nickel-metal hydride batteries, while neodymium-based magnets are critical for compact, high-torque electric motors.

The global shift toward sustainable mobility has sharply increased demand for EVs, which rely more heavily on rare earth elements than traditional internal combustion engine (ICE) vehicles.

Impact of Rare Earth Export Restrictions on the U.S. Automotive Industry

The U.S. auto industry has faced serious setbacks following China's restrictions on rare earth exports. In May 2025, Ford Motor Company was forced to suspend production of its Explorer SUV for an entire week at its Chicago assembly plant due to a shortage of rare earth magnets, a direct consequence of the disrupted supply chain. While a temporary reprieve came in June 2025 when General Motors, Ford, and Stellantis obtained six-month export licenses from Chinese authorities. The fundamental issue of heavy reliance on Chinese rare earth supplies remains unresolved, leaving the industry vulnerable to future shocks.

In response, companies like MP Materials are working to establish domestic production capabilities. MP Materials plans to start magnet production in Texas by the end of 2025 to supply GM and other automakers, according to Automotive Manufacturing Solutions.

Impact of Rare Earth Export Restrictions on the European Automotive Industry

In Europe, the situation has escalated into full-blown production halts. Component plants in Germany and Austria were forced to shut down in June 2025 as rare earth magnet inventories ran dry. The European Association of Automotive Suppliers (CLEPA) reported a mere 25% success rate in securing export licenses, triggering a supply chain crunch. Mercedes-Benz and BMW have responded by building temporary stockpiles, but industry experts warn these will last only weeks without renewed supply.

In parallel, the European Commission has accelerated its critical minerals strategy, announcing 13 new projects focused on diversifying rare earth sourcing from mines in Africa and Australia to expanded recycling infrastructure within the EU. However, most of these projects remain years from scaling, leaving Europe exposed in the near term.

Impact of Rare Earth Export Restrictions on the Indian Automotive Industry

India, among the fastest-growing automotive markets and a rising EV production hub is especially vulnerable to the rare earth bottleneck. Though the country holds around 6% of global rare earth reserves, it lacks the processing capacity needed to turn these resources into usable components. As a result, Indian automakers remain heavily reliant on Chinese imports.

By late May 2025, magnet supplies had already begun to dry up. Bajaj Auto warned of severe disruptions to EV production unless the situation improves by July. Maruti Suzuki and Tata Motors are also operating with limited inventories and have urged the Indian government to engage in diplomatic intervention.

Industry groups like SIAM and ACMA have called for the creation of a “green channel” to fast-track critical imports and emphasized the urgency of building domestic processing infrastructure. Until then, India’s electrification goals could stall under the weight of global geopolitics.

Building Resilience: The Path Forward for the Global Auto Industry

The rare earth crisis is more than a supply chain problem; it’s a wake-up call for the global automotive industry to build resilience through multiple strategies. Diversifying supply is essential, with countries like the U.S., Canada, and Australia investing in new mining and processing projects, though these will take time to become operational.

Technology innovation is also crucial; companies such as BMW and ZF are developing rare-earth-free electric motors, but these alternatives currently face challenges in performance and cost. Recycling rare earth elements from end-of-life vehicles and electronics offers promise but needs stronger infrastructure. Diplomacy plays a key role too, with nations like India pushing China for clearer trade rules to avoid disruptions. Together, these approaches are vital for a stable, resilient automotive future.