- Food Packaging

- Cassava Bags Market

Cassava Bags Market Size, Share, and Growth Forecast, 2026 - 2033

Cassava Bags Market By Product Type (Grip-Hole, T-Shirt, Others), Category (Organic, Conventional), Application, and Regional Analysis for 2026 - 2033

Cassava Bags Market Size and Trends Analysis

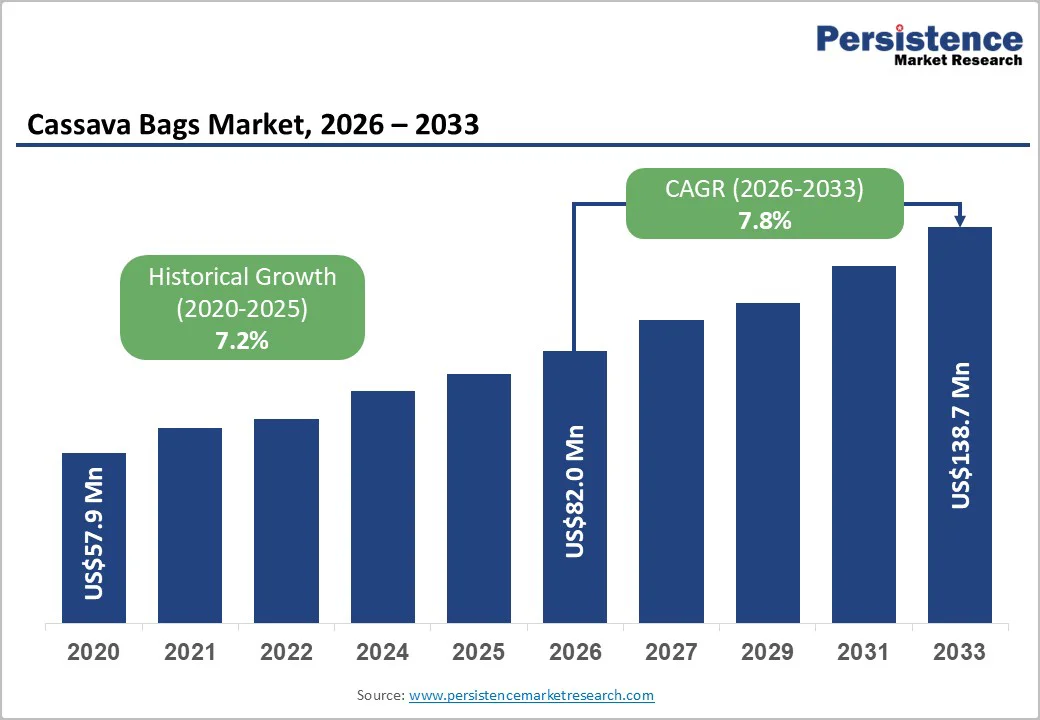

The global cassava bags market size is projected to be valued at US$82.0 million in 2026. It is expected to reach US$138.7 million by 2033, growing at a CAGR of 7.8% between 2026 and 2033, driven by regulatory efforts to curb single-use plastics, rising consumer demand for compostable packaging, and advancements in cassava-starch processing technologies.

Key challenges include performance limitations compared to traditional polymers and fluctuations in agricultural feedstock costs. Promising opportunities lie in retail and e-commerce packaging, development of regionally scaled production hubs in Southeast Asia, and value differentiation through compostability certification and feedstock traceability.

Key Industry Highlights

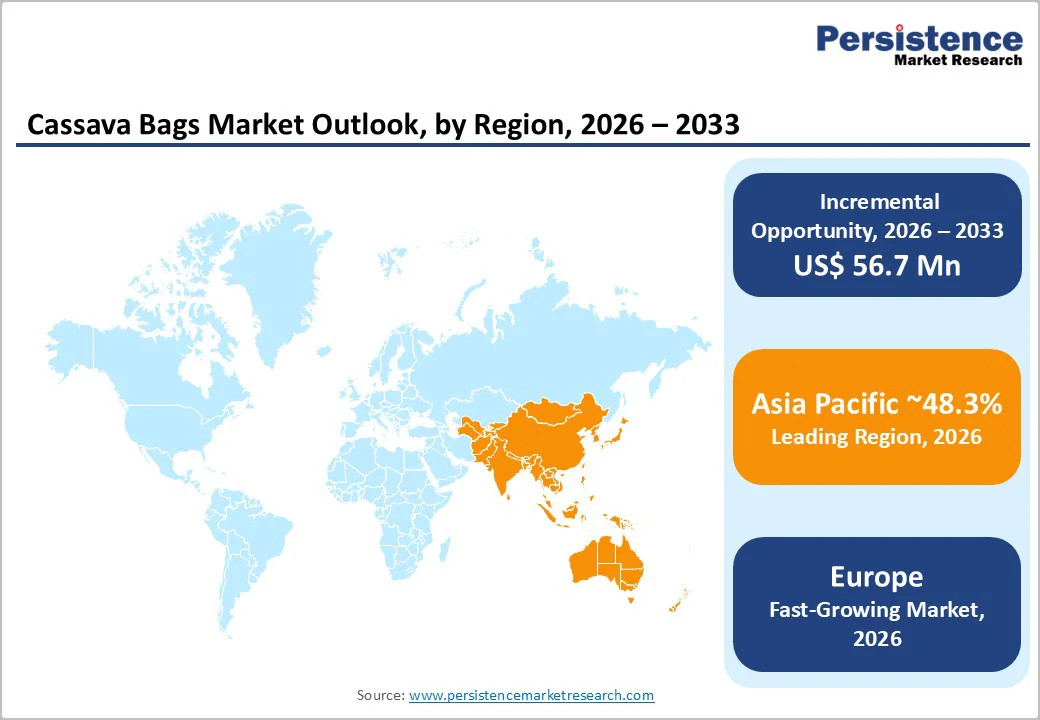

- Leading Region: Asia Pacific is projected to hold 48.3% of market share, driven by proximity to cassava production, established converting clusters in Indonesia, the Philippines, and Vietnam, and cost-competitive manufacturing.

- Fastest-Growing Region: Europe is experiencing the fastest growth due to regulatory tailwinds, strong industrial composting infrastructure, and high consumer willingness to pay for certified compostable products.

- Investment Plans: Investments are focused on new extrusion lines, farm-to-factory integration models, and regional converting capacity expansions, alongside partnerships with waste-management operators to ensure end-of-life processing for compostable bags.

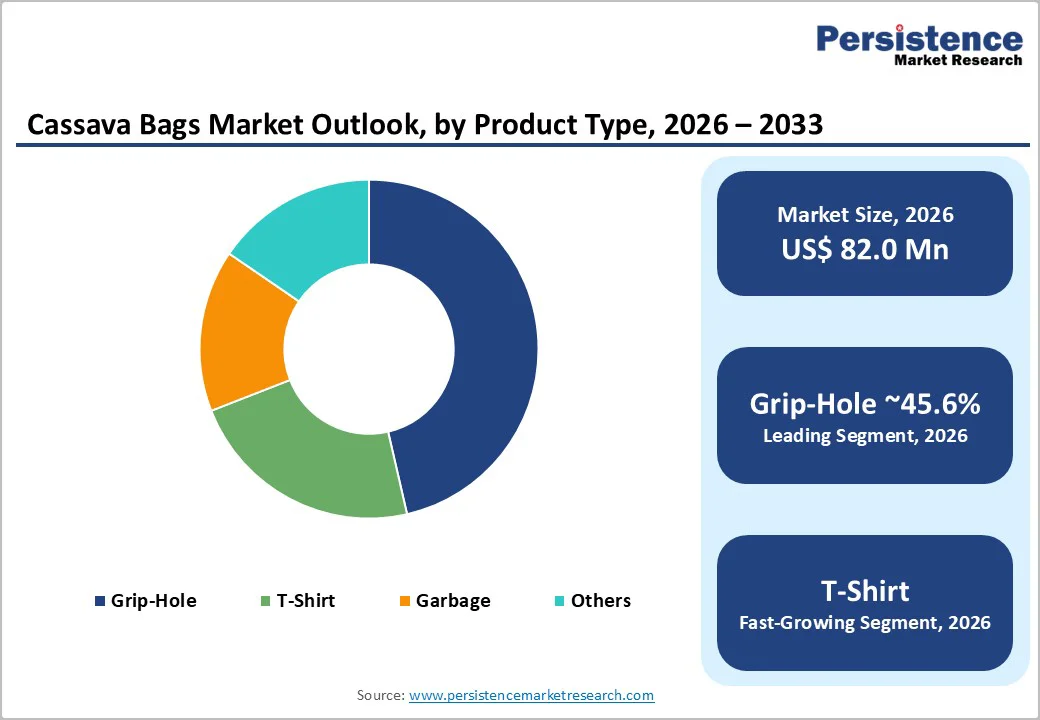

- Dominant Product Type: Grip-hole carry bags, estimated to hold 45.6% market share, are the most widely used product type, favored across supermarkets, convenience stores, and foodservice operations for their versatility, low per-unit cost, and compatibility with existing retail practices.

- Leading Application: Food & beverages, anticipated to hold 41.6% market share, is the largest application segment, including disposable bags for fresh produce, bakery items, prepared meals, and takeaway food, with cassava-based films meeting food-contact regulations.

| Key Insights | Details |

|---|---|

| Cassava Bags Market Size (2026E) | US$82.0 Mn |

| Market Value Forecast (2033F) | US$138.7 Mn |

| Projected Growth (CAGR 2026 to 2033) | 7.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Pressure and Single-use Plastic Bans

Regulation remains the strongest catalyst for cassava bag adoption. Governments across major regions are phasing out conventional single-use plastics and introducing mandatory labeling, compostability criteria, and extended producer-responsibility frameworks. These measures create a direct procurement pull for certified compostable alternatives.

National rules such as plastic-waste legislation in large Asian markets and municipal restrictions in Western economies accelerate transitions in retail, grocery, foodservice, and hospitality.

As enforcement strengthens, retailers and consumer-goods companies face compliance obligations tied to sustainability reporting, prompting rapid substitution toward cassava-based carry bags and produce bags. Jurisdictions with existing industrial composting infrastructure experience the fastest adoption.

Consumer Preferences and Retail Adoption

Consumers increasingly favor packaging that is verifiably compostable and free from toxic additives. Retailers, brand owners, and e-commerce companies reflect this shift in their sustainability scorecards, prioritizing cassava-based bags in product categories where consumers expect environmentally responsible packaging.

Market observations indicate strong traction for cassava bags in organic food stores, supermarkets, quick-commerce delivery services, and direct-to-consumer channels. Private-label programs and retail procurement contracts reduce commercial risk for converters scaling cassava-starch processing lines.

Technological Improvements in Starch Formulations

Advances in cassava-starch modification, fiber reinforcement, and processing have significantly improved film properties. New formulations enhance tensile strength, tear resistance, moisture tolerance, and thermal stability while maintaining compostability. Research into compatibilizers and optimized plasticizers has resulted in films suitable for high-speed converting lines and thicker-gauge bags for garbage, courier, and heavy-duty applications.

These enhancements reduce performance gaps relative to polyethylene and lower rejection rates in mass production. Improved processability also narrows cost differences between cassava-based and petroleum-based bags, helping converters achieve competitive price points in large retail tenders while meeting sustainability criteria.

Barrier Analysis - Feedstock Price and Supply Volatility

Cassava, as an agricultural commodity, is exposed to seasonal variability and competing end-uses. Weather changes, fertilizer price fluctuations, and regional yield differences can cause raw material costs to swing by 15-25% during periods of stress.

As a food-chain input, cassava also faces stricter traceability and compliance requirements, adding procurement complexity. These uncertainties can pressure processor margins, especially for spot buyers, prompting greater use of long-term farmer contracts and partial upstream integration.

Performance Perceptions and Fragmented Standards

Confusion over terms such as “biodegradable,” “compostable,” and “home compostable,” along with country-specific certification requirements, slows large-scale procurement. Not all cassava-based bags meet industrial compostability criteria, and buyers often mandate third-party verification before approving full rollouts.

Certification processes can extend procurement timelines and add testing expenses for smaller manufacturers. In markets with strict enforcement, uncertified suppliers risk exclusion from retail and institutional tenders, reducing addressable demand and increasing compliance burdens across the supply chain.

Opportunity Analysis - Rapid Replacement in Retail and E-Commerce

Retail and e-commerce represent the fastest-growing addressable segment, supported by government bans and retailer commitments. Lightweight carry bags, courier sleeves, and t-shirt variants designed for automated packing are rapidly replacing conventional plastic versions.

Companies that deliver certified compostable, moisture-resistant, and mechanically robust cassava bags can secure multi-year supply agreements with major retail chains and last-mile delivery firms.

Vertical Integration and Feedstock Valorization

Integrating upstream cassava-starch processing enables manufacturers to stabilize raw-material costs, reduce logistics overhead, and offer verified traceability. Vertical models, from farm aggregation to starch milling to film extrusion, can yield mid-single-digit percentage improvements in EBITDA while ensuring consistent quality and supply security.

This approach is especially attractive to investors with agri-value chain experience. By controlling feedstock sourcing, manufacturers can enhance brand credibility, meet procurement requirements for traceable inputs, and negotiate more favorable export contracts with buyers in markets where sustainability documentation is mandatory.

Category-wise Analysis

Product Type Insights

Grip-hole carry bags are expected to remain the dominant product type, accounting for 45.6% of market share in 2026, driven by their widespread use across supermarkets, convenience stores, and foodservice outlets. Their versatility, low unit cost, and direct substitution for conventional thin-film polyethylene bags make them the preferred option in high-turnover retail environments.

Frequent consumer use ensures consistent demand, positioning grip-hole bags as the backbone of overall market revenue. In developed markets such as the U.S., Germany, and Japan, retailers frequently issue bulk tenders for certified compostable grip-hole bags, particularly in regions that enforce single-use plastic bag bans or mandatory labeling requirements.

These bags are also widely used in hospitality settings, including cafés, bakeries, and takeaway outlets, where compact, branded formats enhance customer experience while supporting sustainability goals. Large retail chains increasingly require compostable variants that meet food-contact safety standards. In emerging economies, rapid adoption by small grocery stores and local markets supports steady demand and gradual market expansion.

T-shirt (loop-handle) bags are likely to be the fastest-growing product sub-segment, fueled by the rapid expansion of e-commerce, grocery home delivery, and quick-commerce platforms. Their superior durability and load-bearing capacity make them well-suited for stacked goods and automated packing lines. Growth in this segment consistently outpaces the overall market CAGR, as t-shirt bags better address last-mile logistics needs.

Advances in cassava-starch formulations, such as fiber-reinforced blends and thicker-gauge films, enable higher weight capacity without tearing. As a result, online grocers, meal-kit providers, and subscription box retailers increasingly favor compostable t-shirt bags. To capture this demand, manufacturers are investing in dedicated extrusion lines, positioning this segment as a key growth driver within the evolving omnichannel retail landscape.

Application Insights

Food and beverage applications account for the largest share, estimated to hold 41.6% of the market, due to the frequent use of disposable bags for fresh produce, bakery items, prepared meals, and takeaway food.

Cassava-based films that comply with food-contact regulations, demonstrate odor neutrality, and retain mechanical strength are particularly suitable for these applications. Many supermarkets, restaurants, and quick-service operators require compostable bags to meet corporate sustainability goals or to comply with regional single-use plastic restrictions.

Examples include large retail chains that provide certified compostable produce bags in-store, bakeries that use printed cassava bags for pastries, and meal-prep providers that package lunch kits or snack assortments in compostable options. The high transaction frequency in these settings ensures a consistent baseline demand. The sector’s sensitivity to food safety standards favors organic cassava bags with verified compostability certification.

Retail and e-commerce applications are expanding most rapidly, reflecting the combined effect of plastic bans and the surge in home-delivery services. This segment represents a significant growth opportunity. Cassava bags tailored for online order fulfillment offer improved tear resistance, sealing integrity, and stacking performance, enabling reliable delivery of multiple items or heavier parcels.

E-commerce grocers and quick-commerce platforms increasingly adopt compostable t-shirts or polybag formats to comply with sustainability policies, reduce plastic waste, and meet consumer expectations.

Examples include online grocery subscriptions that use thicker compostable bags for perishables, or eco-conscious retailers shipping personal care products in certified cassava packaging. The combination of regulatory compliance and operational performance makes cassava bags an attractive solution for digital retail channels, ensuring rapid adoption and higher per-unit value in this growing application.

Regional Insights

North America Cassava Bags Market Trends - Corporate Partnerships & Compliance-Driven Adoption

North America is anticipated to exhibit steady growth, with the U.S. as the core market where corporate sustainability initiatives drive adoption. Major retailers and foodservice companies, including regional grocery chains and sustainable suppliers such as Ecoenclose and Novolex, have announced collaborations to co-develop compostable bag solutions tailored to retail and foodservice packaging.

In 2025, Ecoenclose formed a strategic partnership with GreenDot to expand plant-based bag solutions across North American channels, replacing conventional plastics in consumer goods and retail packaging. State and municipal regulations are shaping procurement behavior.

For example, California’s statewide plastic-bag restrictions have compelled many grocery stores to switch to certified compostable alternatives for produce and checkout bags to comply with local law, even if enforcement and composting infrastructure vary. Federally, collaborations between U.S. biodegradable-packaging innovators and retail brands signal an expanding set of commercial trials.

In 2025, Novolex’s collaboration with TIPA Corp. aimed to commercialize additional compostable bag films suitable for U.S. retail environments, supporting retailers’ commitments to reduce plastic. Procurement teams are increasingly emphasizing third-party certification and consistent performance in moisture and load conditions as conditions for supply agreements.

Retail pilots are progressing into larger rollouts as supply consistency improves. Companies capable of supplying certified, large-volume compostable bags, backed by testing and performance validation, are positioned to win multi-year contracts with major grocery and foodservice networks that are formalizing sustainability targets across store networks.

Europe Cassava Bags Market Trends - Regulatory Acceleration & Certification-Led Demand

Europe is likely to be the fastest-growing regional market for cassava bags, driven by one of the strongest regulatory frameworks globally and high consumer environmental awareness.

Strict single-use plastic rules across the European Union and national bans in countries such as France, Germany, the U.K., and Spain have accelerated the shift toward certified compostable alternatives. Under EU directives, grocers and retail brands increasingly specify industrially compostable bags in tender documents, incentivizing suppliers to meet harmonized standards for biodegradability and traceability.

European waste-management systems support the acceptance of compostable bags, particularly for food waste collection and retail shopping bags. Industry players such as Walki Plastiroll Oy and RKW Group have expanded production capacity in response to these regulatory signals, deploying advanced multilayer biobased films that comply with stringent EU compostability and performance requirements.

At the brand level, European retailers are incorporating compostable bags into broader sustainability strategies. Supermarket chains across the region, from discount grocers to high-end organic markets, are piloting cassava-based alternatives for produce and checkout bags, linking procurement choices to corporate ESG reporting.

Consumer willingness to pay a small premium for certified compostable packaging reinforces demand for organic cassava bags and supports stable pricing dynamics.

Investment trends in Europe emphasize regional converting capacity, partnerships with waste processors, and feedstock sourcing strategies, including traceability commitments from Asia Pacific starch supplies. As compliant compostability testing is a common baseline for procurement, European buyers increasingly favor suppliers with demonstrated certifications and documented environmental performance.

Asia Pacific Cassava Bags Market Trends - Supply-Base Expansion & Export-Oriented Growth

The Asia Pacific region is expected to hold the largest share of the global cassava bags market at 48.3%, driven by abundant feedstock and cost-competitive manufacturing. Countries such as Indonesia, the Philippines, and Vietnam have developed local conversion hubs, enabling lower logistics costs and a rapid response to demand.

Producers such as Avani Eco in Indonesia offer fully bio-based cassava packaging for export markets, providing customizable, sustainable bag solutions and reinforcing the region’s role as both a supply base and innovation hub.

In the Philippines, Ako Packaging launched 100% compostable cassava bags for local retailers and SMEs, which biodegrade in about 180 days, offering a practical alternative to conventional plastics. The company is pursuing partnerships to scale production for high-volume commercial segments, reflecting strong local demand for sustainable materials.

China contributes substantial capacity and export-oriented manufacturing for organic and blended cassava films. At the same time, India’s updated plastic-waste regulations drive domestic demand for labeled and traceable compostable products, though adoption varies with local composting infrastructure. Vietnam and Malaysia have set timelines for plastic bag bans, emphasizing the need for certified plant-based alternatives.

Despite regulatory support, industrial composting systems remain limited in many parts of the region, prompting manufacturers to collaborate with waste handlers and pilot end-of-life programs to ensure proper processing. Investments are increasing in new extrusion lines, farm-to-factory integration, and export-oriented facilities.

Exporters emphasizing feedstock traceability and consistent quality are preferred by international distributors, reinforcing Asia Pacific’s strategic role as a leading supplier of certified compostable cassava bags.

Competitive Landscape

The global cassava bags market structure is moderately concentrated among experienced cassava-film producers and highly fragmented across regional SMEs. Several specialized manufacturers lead in technology, certification, and export presence, while smaller converters cater to local retail and foodservice markets with cost-sensitive blends.

Global market share remains distributed, as the industry is still emerging and dominated by regional supply clusters. Consolidation trends are visible as larger packaging companies seek to acquire or partner with cassava-film innovators to expand compostable product portfolios.

Companies focus on compostability certification, vertical integration to stabilize feedstock supply, and retail channel partnerships to secure long-term contracts. Geographic expansion into markets with strong regulatory support and investment in product innovation, such as moisture-resistant or reinforced formulations, serve as differentiators in an increasingly competitive environment.

Key Industry Developments

- In February 2025, Ako Packaging announced the commercial rollout of 100% compostable cassava-based “green” plastic bags in the Philippines, offering local businesses an alternative to conventional plastics and expanding biobased bag adoption in Southeast Asian retail and foodservice channels.

- In November 2025, CONICET (Argentina’s National Scientific and Technical Research Council) partnered with Plastimi SRL to advance the development of biodegradable bags made from cassava starch, aiming to scale local production of sustainable alternatives to conventional plastics in regional markets.

Companies Covered in Cassava Bags Market

- Avani Eco

- Envigreen Biotech India Pvt. Ltd.

- Biogreen Bags Co. Ltd.

- Evoware

- SainBag No Plastic International

- Oikos PH

- Biopak

- EcoBags Products Inc.

- BioBag International AS

- Green Dot Bioplastics

- Plantic Technologies

- Natur-Tec® (Northern Technologies International Corp.)

- EarthPack

- CornWare International

- Polymer Environmental Technology Co., Ltd.

- Shenzhen Ecomann Biotechnology Co., Ltd.

- Xiamen Changsu Industrial Co., Ltd.

- OK Compost-Certified Cassava Bag Manufacturers

- Asia Pulp & Paper - Biopackaging Division

- BioPak Vietnam Co., Ltd.

Frequently Asked Questions

The global cassava bags market size is expected to be US$82.0 million in 2026.

By 2033, the market is projected to reach US$138.7 million, reflecting sustained growth driven by regulatory support and increasing adoption of sustainable packaging.

Key trends include rising adoption of compostable packaging due to single-use plastic bans, growth in retail and e-commerce applications, technological improvements in cassava-starch film formulations, and increasing demand for certified organic and traceable products.

The grip-hole carry bags segment leads the market with approximately 45.6% share, widely used across supermarkets, convenience stores, and foodservice operations for their versatility and low cost per unit.

The cassava bags market is expected to grow at a CAGR of 7.8% between 2026 and 2033.

Major players include Avani Eco, Evoware, Oikos Sustainable Solutions, Affinity Supply Co., and Biogreen Bags/Biopac India.