ID: PMRREP3279| 237 Pages | 8 Jan 2026 | Format: PDF, Excel, PPT* | Consumer Goods

The global Residential Robotic Vacuum Cleaner Market size is projected to reach US$4.2 Billion in 2026 and is anticipated to expand to US$10.7 Billion by 2033, growing at a CAGR of 14.4% between 2026 and 2033. This robust expansion reflects accelerating consumer demand driven by smart home integration, technological advancement in AI-powered navigation systems, and rising disposable income in emerging markets. The market's trajectory demonstrates strong momentum as urbanization intensifies globally, particularly in Asia Pacific where manufacturing advantages and population density create substantial growth opportunities. Rising awareness of cleanliness and hygiene combined with increasing female workforce participation are fundamental socioeconomic drivers reshaping residential cleaning preferences toward automation.

| Key Insights | Details |

|---|---|

| Residential Robotic Vacuum Cleaner Market Size (2026E) | US$ 4.2 billion |

| Market Value Forecast (2033F) | US$ 10.7 billion |

| Projected Growth CAGR (2026-2033) | 14.4% |

| Historical Market Growth (2020-2025) | 13.1% |

Smart Home Integration and IoT Ecosystem Expansion

The integration of robotic vacuums into smart home ecosystems represents a primary growth catalyst. As of 2024, approximately 69.9 million U.S. households actively utilize smart home technology, representing over 50% of all households with 10% annual growth. Modern robotic vacuums seamlessly connect with voice assistants including Amazon Alexa and Google Assistant, enabling remote scheduling, real-time monitoring, and voice-activated control through smartphone applications. This technological convergence significantly enhances user convenience and appeal. The proliferation of IoT platforms—including Apple HomeKit and Amazon—creates substantial value-add for consumers seeking integrated home automation. Market research indicates over 70% of consumers prefer appliances with seamless smart home connectivity. This driver directly contributes to elevated market adoption rates and represents significant revenue expansion potential across residential segments. Enhanced accessibility through mobile app interfaces and voice commands transforms robotic vacuums from niche products into mainstream household solutions, driving sustained market penetration.

Advancing AI-Powered Navigation and Obstacle Avoidance Technology

Artificial intelligence integration fundamentally transforms robotic vacuum capabilities and market positioning. Contemporary models employ LiDAR mapping, camera-based vision systems, and AI-driven object recognition algorithms enabling systematic navigation and real-time obstacle avoidance. Advanced models now identify specific objects including shoes, toys, and pet waste, preventing collision and optimizing cleaning efficiency. SLAM (Simultaneous Localization and Mapping) algorithms enable comprehensive home coverage while maintaining consistent performance across varied floor types. Manufacturers investing in AI-powered navigation report enhanced customer satisfaction and reduced warranty claims. Premium segments featuring autonomous obstacle avoidance command pricing premiums of 30-50% above conventional models. These technological advancements justify premium pricing while expanding addressable markets toward tech-savvy demographics. Continuous machine learning capabilities enable models to improve performance over time, creating sustained customer value and reducing purchase replacement cycles.

High Initial Purchase Cost and Maintenance Requirements

Premium robotic vacuum models command retail prices ranging from $600-$1,400 USD, creating accessibility barriers for middle and lower-income households. Initial cost sensitivity remains pronounced in emerging markets despite rising disposable incomes. Maintenance requirements including filter replacements, brush maintenance, and dock cleaning necessitate ongoing operational expenses, potentially discouraging adoption among cost-conscious consumers. Product failure rates and warranty claim frequencies impact long-term total cost of ownership perception. Supply chain constraints periodically elevate component costs including specialized sensors and motors, influencing retail pricing strategies. Consumer education regarding value proposition remains inconsistent across geographic regions, potentially suppressing demand among price-sensitive segments.

Competitive Intensity and Market Consolidation Pressures

The residential robotic vacuum market exhibits intensifying competition from established electronics manufacturers including Samsung, LG, and Dyson alongside specialized robotics firms. Market fragmentation presents consolidation pressures, with acquisitions including Amazon's attempted acquisition of iRobot (valued at $1.7 billion) exemplifying strategic buyer intent. New entrants including Dreame and emerging Chinese manufacturers aggressively expand market share through competitive pricing and feature-rich offerings. Distribution channel conflicts arise as manufacturers balance direct-to-consumer e-commerce strategies with traditional retail partnerships. Brand loyalty remains moderate, with consumers frequently switching between competitors based on price and feature evaluations. Competitive pressure constrains profit margins, particularly within mid-range market segments where value-oriented consumers demonstrate high price elasticity.

Outdoor and Perimeter Robotic Cleaning Applications

Outdoor robotic vacuum technology represents an emerging market segment currently commanding approximately 16% of total market share with projected CAGR of 16.5% through 2033. Mid-range and high-end outdoor robots collectively represent 75-80% of outdoor segment revenue, indicating premium product positioning. Applications including patio cleaning, driveway maintenance, and pool area management address substantial unmet customer needs. Technological adaptations for outdoor environments including weather-resistant components and advanced terrain navigation create product differentiation opportunities. Market expansion into outdoor applications extends addressable market boundaries and creates cross-selling opportunities for residential customers. Potential market sizing estimates indicate outdoor robotic segment could reach US$1.2-1.5 billion by 2033 from base allocations of US$400-600 million in 2026.

Hybrid Vacuum-Mopping Integration and Multi-Functional Robotics

Multi-functional robotic systems combining vacuuming and mopping capabilities represent rapidly-expanding product category with demonstrated consumer appeal. Recent product innovations showcased at CES 2025 including Ecovacs Deebot X8 Pro Omni and hybrid vacuum-mop combinations indicate consumer receptivity to consolidated cleaning solutions. Multi-functional devices command 15-20% price premiums compared to single-function models while addressing comprehensive household cleaning requirements. Product market expansion potential extends beyond floor cleaning into air purification, security monitoring, and item delivery functionality. Emerging modular robot designs enable removable components transforming single devices into multiple specialized tools, expanding addressable use cases and customer lifetime value. Market analysis indicates hybrid segment growth rates of 18-22% annually, substantially exceeding single-function categories.

In-house robotic vacuum cleaners dominate the residential market, commanding an estimated 89% market share in 2026. These models are engineered for interior residential and commercial spaces, offering autonomous navigation, scheduled cleaning, and intelligent obstacle avoidance. Adoption is driven by smart home integration, silent operation, customizable routines, and self-docking. Advanced sensors, real-time mapping, and app-based controls enhance reliability. Strong demand reflects urban lifestyles and time constraints, while continuous feature upgrades, voice assistants, selective room cleaning, competitive pricing, and reliability sustain leadership.

Outdoor robotic vacuum technology represents a high-growth opportunity, with high-end outdoor robots as the fastest-growing segment at a projected 18.8% CAGR through 2033. These models feature weather resistance, rugged navigation, and durability for patios, driveways, and gardens. Mid-range and high-end units hold 75–80% share, supporting premium positioning and margins globally.

Auto-Battery Charging Leading Segment

Automatic battery charging technology commands approximately 74% market share within the residential robotic vacuum market, reflecting strong consumer preference for hands-free operation. Auto-charging models autonomously return to docking stations when batteries deplete, enabling uninterrupted schedules without manual intervention. This dominance is driven by convenience, smart home integration, and cleaning during user absence. Widespread manufacturer standardization reinforces adoption, shifting competition toward navigation intelligence, mapping accuracy, cleaning efficiency, pricing optimization, feature enhancement, and broad retail availability across global residential usage scenarios worldwide.

Manual charging models show steady growth near 7.4% CAGR through 2033, appealing to budget-conscious consumers and emerging markets. Relevance persists through lower prices, simple interfaces, and manufacturing efficiency. Adoption reflects affordability sensitivity, supporting entry-level competition, geographic expansion, and sustained demand across diverse demographic segments globally over the forecast period ahead.

North America exhibits substantial market maturity with strong consumer awareness and intense manufacturer competition. The region is projected to record 13.2% CAGR through 2033, supported by high disposable income, widespread smart home adoption, and advanced e-commerce infrastructure. The United States accounts for nearly 60% of regional value, driven by urban density, rapid technology uptake, and premium product preference. Regulatory frameworks emphasize safety, labeling, and electromagnetic compliance, shaping entry requirements. Innovation leadership includes iRobot, Neato Robotics, and global electronics brands. Competitive dynamics show iRobot holding 35–40% U.S. share, challenged by SharkNinja, Ecovacs, and new entrants. Online retail channels represent around 61% of sales, reshaping distribution strategies. Product differentiation increasingly centers on premium features, reliability, software intelligence, and customer experience optimization. Sustained investment activity, logistics efficiency, and service networks further reinforce long-term regional growth visibility and competitive resilience across residential robotics ecosystems nationwide.

Europe maintains significant market importance with nearly 25% global share and steady 12% CAGR through 2033. Germany, United Kingdom, France, and Spain serve as primary growth hubs with distinct regulatory and consumer preference patterns. European Union sustainability directives, including ecodesign rules and extended producer responsibility, shape product development and competitive positioning. Germany shows advanced electronics adoption and premium demand, while Southern Europe favors value-oriented offerings. Regulatory harmonization enables standardized compliance and efficient cross-border distribution. Key players such as Dyson, Miele, and Vorwerk benefit from strong regional presence and manufacturing bases. Consumers prioritize reliability, durability, and sustainability, supporting quality differentiation. Investment trends highlight consolidation and acquisitions. Growth potential persists in Poland and Czech Republic, where urbanization, income growth, and smart-home adoption support accelerating residential robotic vacuum penetration across evolving European households and multifamily dwellings with increasing digital lifestyles and automation awareness.

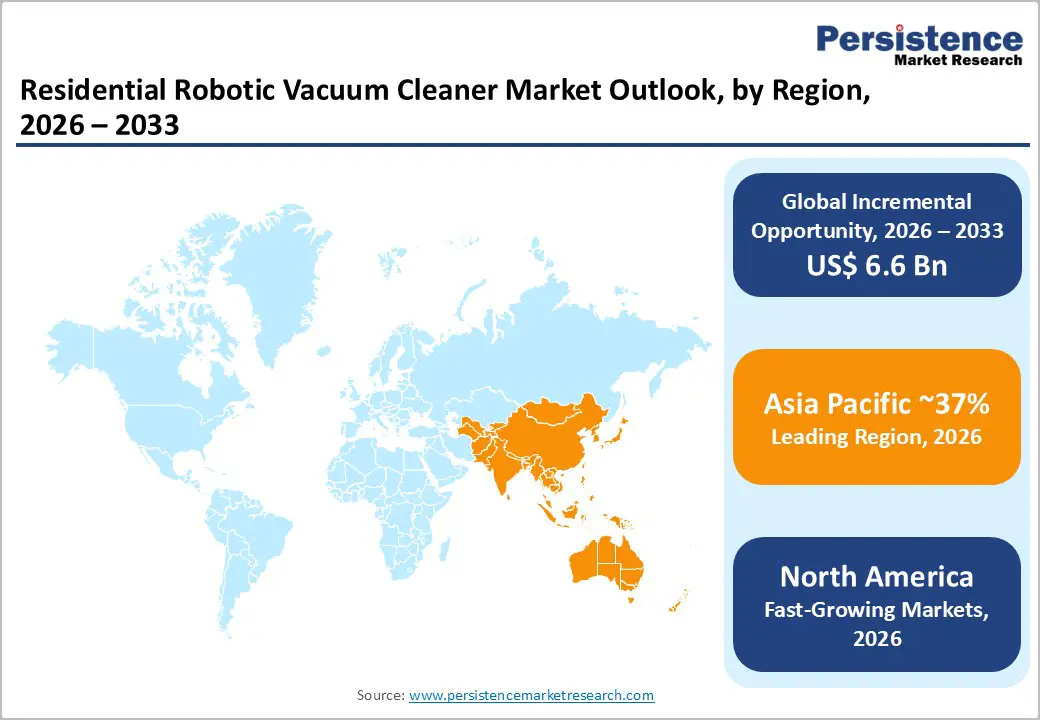

Asia Pacific represents the dominant global region commanding approximately 37% market share with accelerated growth dynamics outpacing other geographic segments. China, Japan, and India drive substantial market expansion reflecting urbanization intensity, disposable income growth, and manufacturing ecosystem advantages. Regional market valuation reaches approximately US$1.55 billion in 2026, expanding to US$4.0 billion by 2033 representing significant expansion opportunity. China's dominant position reflects manufacturing leadership, innovative product development, and large addressable consumer base. Japan demonstrates premium market positioning driven by aging population demographics and government elder-care automation initiatives. India exhibits rapid growth trajectory with expanding middle-class demographics and e-commerce infrastructure development. Regional competitive advantages include low-cost manufacturing, supply chain efficiency, and rapid product iteration cycles. Leading manufacturers including Roborock, Ecovacs, and Xiaomi leverage regional ecosystem advantages to drive global expansion. Technology transfer and innovation dissemination patterns accelerate competitive evolution and feature democratization across price segments.

Strategic Developments

Market leaders deploy sharply differentiated strategies aligned to target segments. iRobot reinforces premium appeal through deep smart home integration and relentless innovation. Ecovacs accelerates scale via geographic expansion, portfolio breadth, and cost efficiency. Roborock pairs cutting-edge technology with aggressive pricing, while emerging Chinese brands champion AI-driven, feature-rich value propositions globally.

The global market reached US$4.2 Billion in 2026 and is projected to expand to US$10.8 Billion by 2033, representing substantial growth potential across residential cleaning solutions.

Primary growth drivers include smart home ecosystem integration connecting to Alexa and Google Assistant, AI-powered navigation technology enabling autonomous operation, and rising disposable incomes in emerging Asia-Pacific markets coupled with accelerating urbanization patterns.

The market projects 14.4% CAGR between 2026-2033, demonstrating strong expansion momentum globally.

Primary opportunities include outdoor robotic applications growing at 16.5% CAGR addressing unmet patio and driveway cleaning needs, hybrid vacuum-mopping solutions commanding premium pricing, and sustainable product development capturing environmentally-conscious consumer segments.

Market leadership includes iRobot Corporation, Roborock Technology, Ecovacs Robotics, Xiaomi Corporation, and Samsung Electronics alongside emerging competitors including Dreame, Dyson, and regional manufacturers capturing diverse market segments through differentiated product positioning

| Report Attributes | Details |

|---|---|

| Historical Data/Actuals | 2020 – 2025 |

| Forecast Period | 2026 – 2033 |

| Market Analysis Units | Value: US$ Bn/Mn, Volume: As applicable |

| Geographical Coverage |

|

| Segmental Coverage |

|

| Competitive Analysis |

|

| Report Highlights |

|

By Robot Type

By Charging Mode

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author