- Media & Entertainment

- Video Conferencing Endpoints and Infrastructure Market

Video Conferencing Endpoints and Infrastructure Market Size, Share, and Growth Forecast 2026 - 2033

Video Conferencing Endpoints and Infrastructure Market by Component (Hardware, Software, Services), Deployment (On-Premises, Cloud-Based), End Points (Desktop Endpoints, Room-Based Systems, Mobile Endpoints, Integrated Solutions), Industry (Corporate Communication, Education, Healthcare, Government, Telecommuting, Others), by Regional Analysis, 2026 - 2033

Video Conferencing Endpoints and Infrastructure Market Size and Trend Analysis

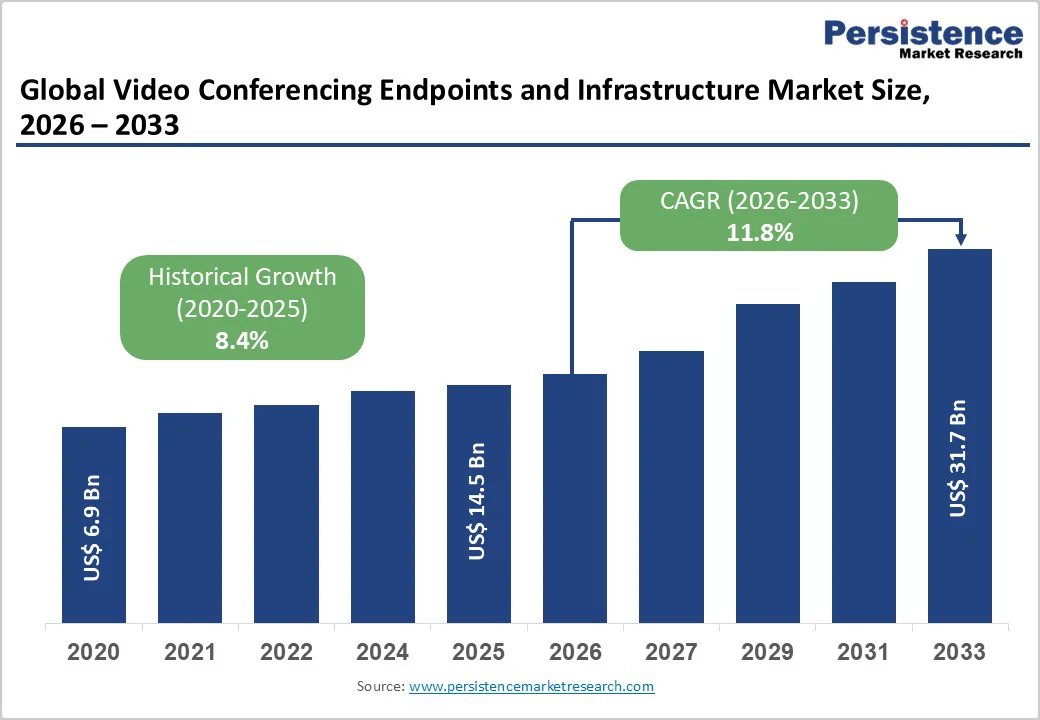

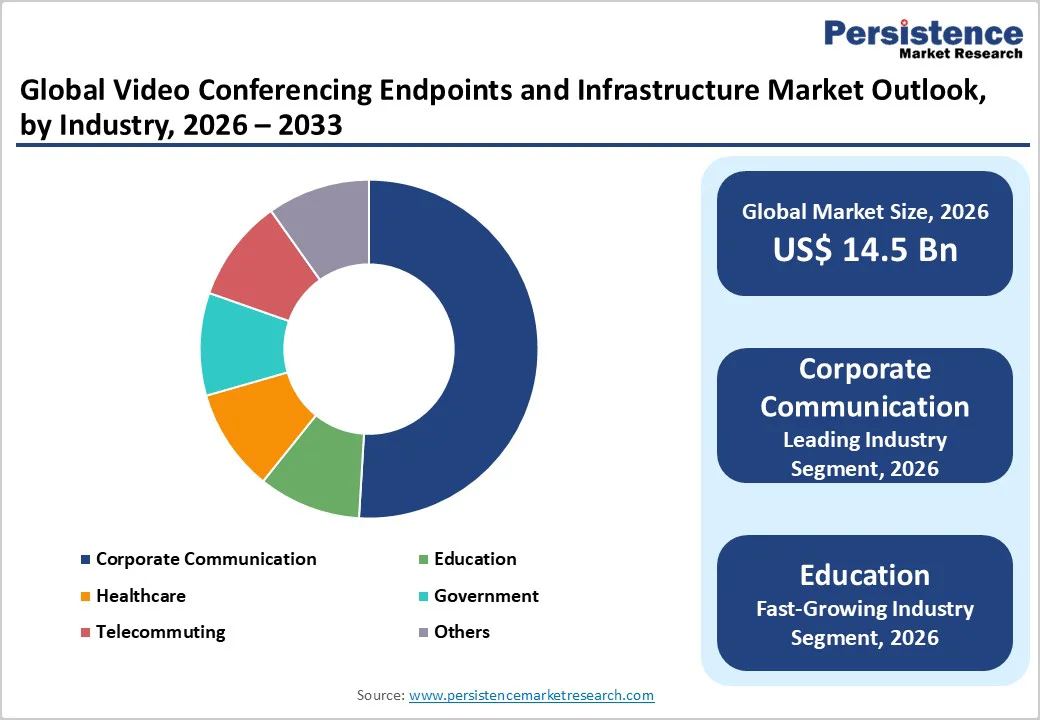

The global video conferencing endpoints and infrastructure market is projected to reach US$31.7 billion by 2033, growing at a CAGR of 11.8% between 2026 and 2033. The market is likely to be valued at US$14.5 billion in 2026.

The market expansion is driven by the permanent shift toward hybrid and remote work models, with approximately 83% of global employees preferring hybrid arrangements that combine office and home-based days, and by rapid digital transformation initiatives across industries.

Advanced technology integration, including AI-powered meeting analytics, 5G-enabled ultra-low latency video, and cloud-based infrastructure deployment, is revolutionizing collaboration infrastructure, enabling organizations to support geographically dispersed teams with seamless real-time communication while reducing travel expenses and improving workforce productivity.

Key Industry Highlights

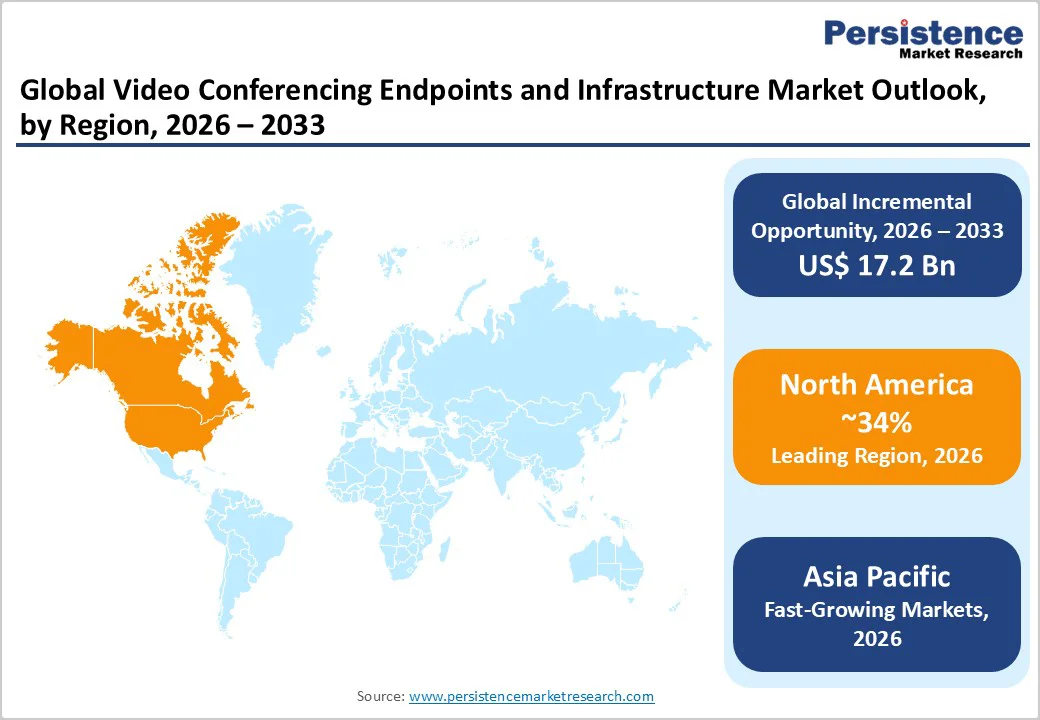

- Leading Region: North America holds around 34% of global 2025 revenues, driven by strong hybrid-work adoption, heavy enterprise IT spending, dense presence of major vendors, and strict security-led demand in regulated industries.

- Fastest Growing Region: Asia Pacific is the fastest-expanding market with a 2026 - 2032 CAGR of 14.8%, supported by rapid digitalization, SME cloud uptake, a growing IT services ecosystem, and government-backed digital infrastructure programs.

- Dominant Segment: Software leads with a 53% share in 2025 as enterprises shift to cloud subscriptions and AI-enhanced capabilities such as live transcription, meeting intelligence, and virtual assistants over hardware-centric systems.

- Fastest Growing Segment: Mobile endpoints grow fastest at a 15.2% CAGR from 2026 - 2032, enabled by BYOD expansion, widespread remote work, and rising smartphone usage that facilitates seamless video participation through mobile apps.

- Key Market Opportunity: Telehealth-driven healthcare investments grow at a 17.1% CAGR, fueled by expanding virtual consultations, compliance-focused infrastructure needs, government support programs, and enduring adoption of video-enabled clinical workflows.

| Key Insights | Details |

|---|---|

| Video Conferencing Endpoints and Infrastructure Market Size (2026E) | US$14.5 Bn |

| Market Value Forecast (2033F) | US$31.7 Bn |

| Projected Growth CAGR (2026 - 2033) | 11.8% |

| Historical Market Growth (2020 - 2025) | 8.4% |

Market Dynamics

Market Growth Drivers

Accelerating Adoption of Hybrid and Remote Work Models

The fundamental shift in workplace norms toward hybrid and remote operations is the primary growth catalyst for the video conferencing endpoints and infrastructure market, with 22% of the United States workforce working remotely as of 2025, up from 6.5% in 2019.

Organizations are investing substantially in enterprise-grade video conferencing solutions to support distributed teams across multiple geographic locations, recognizing that 81% of employees rank remote work flexibility as more important than salary, and that 46% of remote-capable workers are willing to quit if forced to return to full-time office environments.

Corporate enterprises are establishing sophisticated meeting room infrastructure equipped with Cisco Webex Room Kit EQX systems, Microsoft Teams Rooms Display Kits, and Zoom Rooms appliances to enable seamless participation for both in-office and remote attendees, addressing the collaboration gap that traditional video platforms cannot fully resolve.

Cost reduction opportunities further accelerate enterprise adoption, as companies recognize that video conferencing infrastructure eliminates expensive business travel, reduces physical office space requirements, and enables faster decision-making by facilitating real-time cross-border collaboration with minimal delays.

AI-Powered Meeting Intelligence and Advanced Collaboration Features

Artificial intelligence integration has emerged as the overarching technology driving unprecedented innovation in video conferencing endpoints and infrastructure, with AI-powered transcription achieving accuracy levels exceeding 99% for Zoom and 98.71% for Webex, and reducing transcription errors by approximately 27% compared to legacy systems.

Organizations are increasingly deploying AI-driven meeting analytics, real-time transcription services, automated action-item tracking, and contextual meeting summarization capabilities, transforming video conferencing from simple communication tools into strategic business intelligence platforms.

Advanced features, including speaker diarization with deep learning models, real-time multilingual translation, automated sentiment analysis, and personalized meeting insights, are enhancing user experience while simultaneously driving adoption across corporate, educational, and healthcare sectors.

The integration of generative AI into conferencing platforms enables context-aware transcription, automated task extraction, predictive insights generation, and intelligent assistant capabilities that help teams stay aligned during meetings while reducing cognitive load through automated follow-up management.

Market Restraints

High Capital Expenditure Requirements and Infrastructure Complexity

High upfront costs remain a major barrier to adoption, especially for small and mid-sized enterprises that struggle to justify the investment required for advanced room-based systems. Deploying high-quality cameras, microphone arrays, control panels, and displays often requires network upgrades, installation services, and integration with existing collaboration platforms, adding significant technical and operational complexity.

Many organizations also face challenges aligning new endpoints with legacy IT environments, which requires network assessments, security reviews, and configuration management across multiple sites. Ongoing maintenance, firmware updates, and user training further add to operating expenses, prompting budget-constrained enterprises to delay adoption or rely on basic, software-only solutions.

Data Security and Regulatory Compliance Concerns

Stringent data security and privacy requirements act as a major restraint, particularly as organizations must comply with frameworks such as GDPR, HIPAA, and region-specific data protection mandates. These regulations require robust encryption, secure data storage, detailed audit logs, access controls, and formal incident response processes, increasing implementation complexity and solution costs.

Procurement cycles lengthen as enterprises review Data Processing Agreements, validate certifications, and conduct risk assessments to ensure compliance. Increasing emphasis on continuous monitoring, DPIA obligations, and stronger authentication requirements creates additional operational burdens, especially for organizations lacking mature security infrastructure or dedicated compliance teams.

Market Opportunities

Healthcare Telehealth Expansion and Clinical Collaboration Infrastructure

The healthcare sector presents one of the strongest growth opportunities as providers accelerate investment in telehealth and virtual care infrastructure. Hospitals and clinics are increasingly adopting secure, compliance-ready video conferencing systems to support remote consultations, virtual rounds, specialist collaboration, and remote diagnostics, with HIPAA-compliant encryption and Business Associate Agreements now standard requirements.

Telehealth usage, which surged dramatically during the pandemic, has stabilized at elevated levels as patients and providers embrace hybrid care models. This sustained demand is driving the deployment of endpoints in exam rooms, counseling spaces, and monitoring centers, supported by reimbursement reforms and government initiatives aimed at expanding rural digital healthcare access.

Advanced capabilities, such as high-resolution medical image sharing, diagnostic device integration, and automated compliance logging, further enhance clinical workflows, supporting a projected double-digit CAGR for healthcare facility endpoint investments.

Education Digital Learning Infrastructure and Virtual Classroom Modernization

The education sector offers significant expansion potential as institutions modernize learning environments to support hybrid and distance education models. Schools and universities are increasingly equipping classrooms and lecture halls with dedicated video conferencing endpoints that enable seamless interaction between in-person and remote learners.

Government digital education programs and funding initiatives are accelerating these deployments, particularly in rural and underserved regions seeking equitable access to quality instruction. Purpose-built classroom solutions now include features such as lecture recording, intelligent student engagement tools, breakout room support, and privacy-focused controls that enhance the learning experience while protecting student data.

As hybrid learning becomes a long-term fixture in global education systems, institutions recognize that technology-enabled classrooms expand enrollment reach, improve accessibility, and support diverse pedagogical approaches. This sustained digital transformation positions education as a major driver of future market growth.

Category-wise Insights

Component Analysis

Software remains the dominant component due to the industry-wide shift toward cloud-first collaboration models, accounting for more than half of total market value in 2025. Organizations increasingly prioritize software-based platforms that offer scalable deployment, rapid feature updates, strong security frameworks, and seamless integration with enterprise applications.

Advanced capabilities-such as AI-driven transcription, automated summaries, multilingual translation, analytics dashboards, and workflow integrations-have positioned software as the central enabler of hybrid work productivity. Cloud delivery further enhances value by minimizing infrastructure costs and supporting global accessibility. As a result, the software segment is expected to record the fastest growth through 2033.

Deployment Analysis

Cloud-based deployment is the fastest-expanding segment as enterprises transition away from on-premises systems in favor of scalable, subscription-driven collaboration environments. Cloud models eliminate hardware overhead, streamline IT management, and allow rapid rollout of AI updates and security enhancements.

The ability to support remote access, deliver consistent performance across geographies, and integrate with widely used digital ecosystems significantly strengthens adoption. Cloud platforms also provide built-in resilience, disaster recovery, and advanced compliance controls that often surpass on-premises capabilities. As organizations prioritize agility, cost efficiency, and user accessibility, cloud deployment continues to gain traction across enterprises of all sizes.

End Points Analysis

Room-based systems hold the largest endpoint share as organizations prioritize reliable, high-quality collaboration environments for boardrooms, project rooms, and executive spaces. These systems integrate advanced cameras, multi-microphone arrays, intelligent framing, and touch controls to deliver consistent, high-impact meeting experiences.

Demand is also strengthened by the rapid conversion of small meeting spaces into video-enabled huddle rooms that support agile teamwork and hybrid collaboration. Room systems increasingly incorporate AI-assisted features such as automated recording, analytics, participant framing, and acoustic optimization, positioning them as strategic infrastructure in enterprise productivity planning.

Their reliability and immersive experience continue to outpace desktop and mobile endpoints.

Industry Analysis

Corporate communication remains the largest application segment with 52% market share in 2025 as enterprises rely heavily on video conferencing to manage distributed teams, streamline internal communication, and connect with clients across global markets. Organizations in knowledge-driven sectors such as IT, consulting, and financial services depend on high-quality video collaboration to support complex workflows and accelerate decision-making.

Investments in sophisticated room systems, centralized management platforms, and integrated communication ecosystems are driven by the need for productivity, workflow continuity, and reduced travel. While corporate usage dominates, healthcare represents the fastest-growing segment, with telehealth expansion accelerating demand for secure, compliant video solutions that support remote patient engagement and clinical collaboration.

Regional Insights

North America Video Conferencing Endpoints and Infrastructure Trends

North America retains its position as the global leader, generating roughly 34% of market revenue in 2025 due to early adoption of collaboration technologies, mature hybrid-work systems, and consistently high enterprise IT spending.

The United States dominates regional demand, supported by a large concentration of major enterprises and regulated industries that prioritize secure, high-performance communication infrastructure. Regulatory frameworks across healthcare, finance, and government strongly influence procurement decisions, encouraging deployment of platforms with stringent encryption, auditing, and compliance features.

Rapid 5G expansion across major metropolitan areas is further elevating meeting quality by enabling ultra-low-latency, high-bandwidth video experiences. The region is also at the forefront of AI-enabled collaboration, with organizations aggressively upgrading endpoints to leverage advanced transcription, analytics, and automated meeting assistance.

This focus on innovation, combined with strong cloud ecosystem maturity, continues to position North America as the most technologically advanced and commercially significant market for video conferencing infrastructure.

Europe Video Conferencing Endpoints and Infrastructure Trends

Europe represents the second-largest regional market, accounting for about 28% of global revenue in 2025, supported by a robust digital infrastructure, high hybrid-work penetration, and strict data governance requirements.

GDPR plays a central role in shaping vendor strategies, driving demand for platforms that deliver strong encryption, transparent data processing controls, resilient audit capabilities, and verified compliance certifications. Major economies such as Germany, the United Kingdom, and France are leading deployment activity as enterprises modernize meeting spaces and integrate secure, cloud-based collaboration environments.

Germany’s manufacturing-led digital transformation agenda is fueling adoption of advanced room systems that support cross-border engineering and operational collaboration.

The UK continues to expand rapidly, supported by strong enterprise digital strategies and government-backed modernization programs. Across Western Europe, organizations are prioritizing fully compliant, enterprise-grade solutions that protect sensitive corporate and personal data, strengthening long-term demand for premium endpoints and infrastructure.

Asia Pacific Video Conferencing Endpoints and Infrastructure Trends

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of 14.8% from 2026 to 2032, driven by rapid economic development, large-scale digital transformation, and expansion of manufacturing and IT-enabled services. China leads regional demand, with significant enterprise investment, widespread adoption of digital communication systems, and rapid growth in cloud infrastructure, supporting both domestic and international collaboration needs.

India is experiencing accelerated uptake due to the expansion of its IT services sector, government digital initiatives, SME cloud migration, and rising demand from BPO operations requiring stable, high-quality video connectivity. Japan continues to contribute strong value through advanced manufacturing modernization, a preference for high-reliability endpoints, and ongoing innovation in enterprise collaboration technologies.

Southeast Asian markets such as Singapore, Thailand, and Vietnam are scaling rapidly as business hubs grow, government investments in digital infrastructure increase, and organizations adopt modern collaboration systems to support regional and global operations.

Competitive Landscape

Market Structure Analysis

The video conferencing endpoints and infrastructure market is moderately consolidated, with a small group of global vendors accounting for a significant share through vertically integrated ecosystems that combine hardware, software, and cloud services.

These leading players strengthen their positions by expanding partner networks, investing heavily in AI-driven capabilities, and offering tightly unified platforms that encourage long-term customer retention. Mid-tier and regional vendors compete by focusing on differentiated feature sets, value-driven pricing, and localized channel strategies, enabling them to serve mid-market enterprises and cost-sensitive buyers effectively.

Across the market, competitive strategies increasingly revolve around AI-enhanced meeting intelligence, including advanced transcription, analytics, translation, and automated assistance, which has become a primary area of product differentiation.

Business models continue shifting toward subscription-based offerings, reflecting enterprise preferences for scalable, OPEX-oriented deployment. M&A activity remains active as companies acquire specialized AI, security, and vertical-focused collaboration technologies to expand capabilities and accelerate innovation.

Key Market Developments

- October 2024: Zoom launched its Zoom Phone cloud Private Branch Exchange (PBX) service in India, offering global native coverage across 50 countries with local presence enabling enterprises to establish cloud-based phone systems supporting hybrid work environments and reducing dependency on traditional PSTN (Public Switched Telephone Network) infrastructure.

- September 2025: Cisco unveiled “agentic collaboration” via RoomOS 26 and updated devices at WebexOne 2025 integrating Webex Suite with tools like Microsoft 365 Copilot, Amazon Q index and Salesforce.

Companies Covered in Video Conferencing Endpoints and Infrastructure Market

- Avaya, Inc.

- Cisco Systems, Inc.

- Microsoft Corporation

- Plantronics, Inc.

- Zoom Video Communications, Inc.

- Huawei Technologies Co., Ltd.

- Polycom Inc.

- Amazon Web Services (AWS)

- Google, LLC

- HP Inc.

- Qumu Corporation

- Sonic Foundry Inc.

- Lifesize, Inc.

- Kaltura Inc.

- BlueJeans Network

- Logitech International

- Yealink Technology

- Poly (formerly Plantronics/Polycom)

- ClearOne Communications

- Crestron Electronics

Frequently Asked Questions

The market is projected to reach US$ 31.7 billion by 2033, growing at an 11.8% CAGR from 2026.

Demand is driven by hybrid work adoption, AI-enabled meeting features, cloud migration, 5G expansion, and compliance requirements in regulated industries.

The software segment leads with about 53% share due to its scalability, AI capabilities, and widespread adoption of cloud-based platforms.

North America leads with 38-40% share, supported by strong hybrid work usage, high IT spending, and stringent security regulations.

Major opportunities include telehealth expansion requiring secure video platforms and digital learning infrastructure growth in education.

Key players include global providers of room systems, cloud platforms, and peripherals such as Cisco, Microsoft, Zoom, Google, Poly, Huawei, Avaya, and Logitech.