- Bulk Chemicals

- Soda Ash Market

Soda Ash Market Size, Share, and Growth Forecast, 2025 - 2032

Soda Ash Market By Production Type (Natural, Synthetic), Product Form (Dense, Light, Others), End-user, and Regional Analysis for 2025 - 2032

Soda Ash Market Size and Trends Analysis

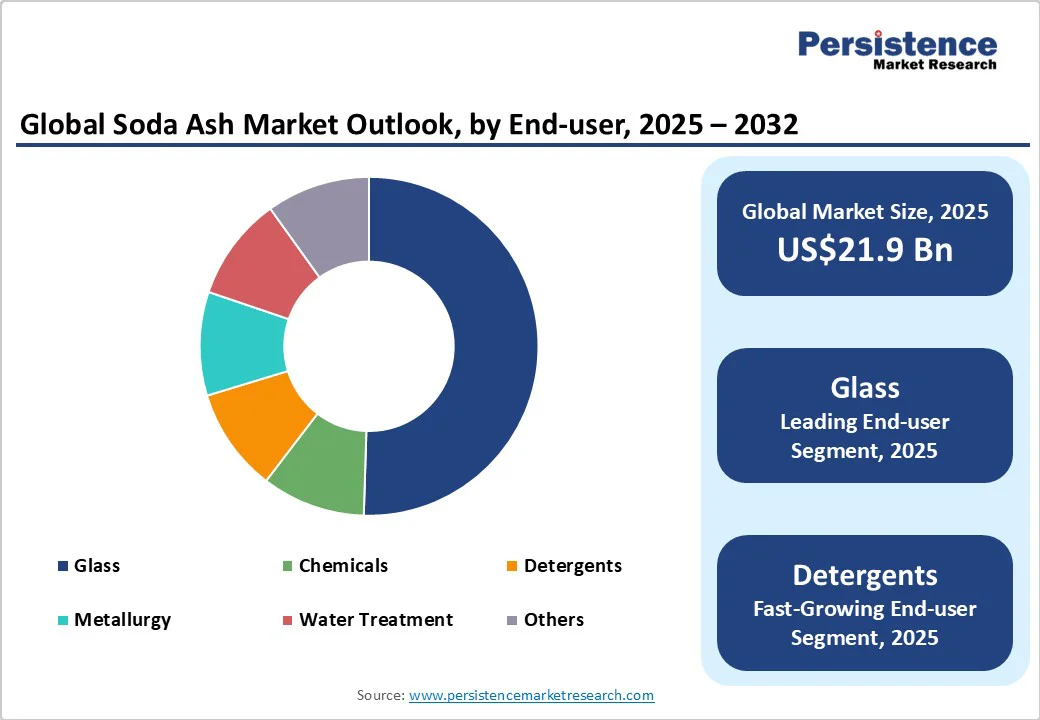

The global soda ash market size is likely to be valued at US$21.9 Billion in 2025 and is expected to reach US$29.4 Billion by 2032, growing at a CAGR of 4.3% during the forecast period from 2025 to 2032, driven by strong demand from the glass industry, consistent industrial chemicals consumption, and recovery in the construction and automotive sectors.

Both trona-based (natural) and synthetic production methods shape supply dynamics, while rising focus on low-carbon production is influencing capacity expansion and investment decisions. Price fluctuations and Chinese production patterns create short-term market volatility, whereas long-term demand from glass and water-treatment applications provides structural stability.

Key Industry Highlights

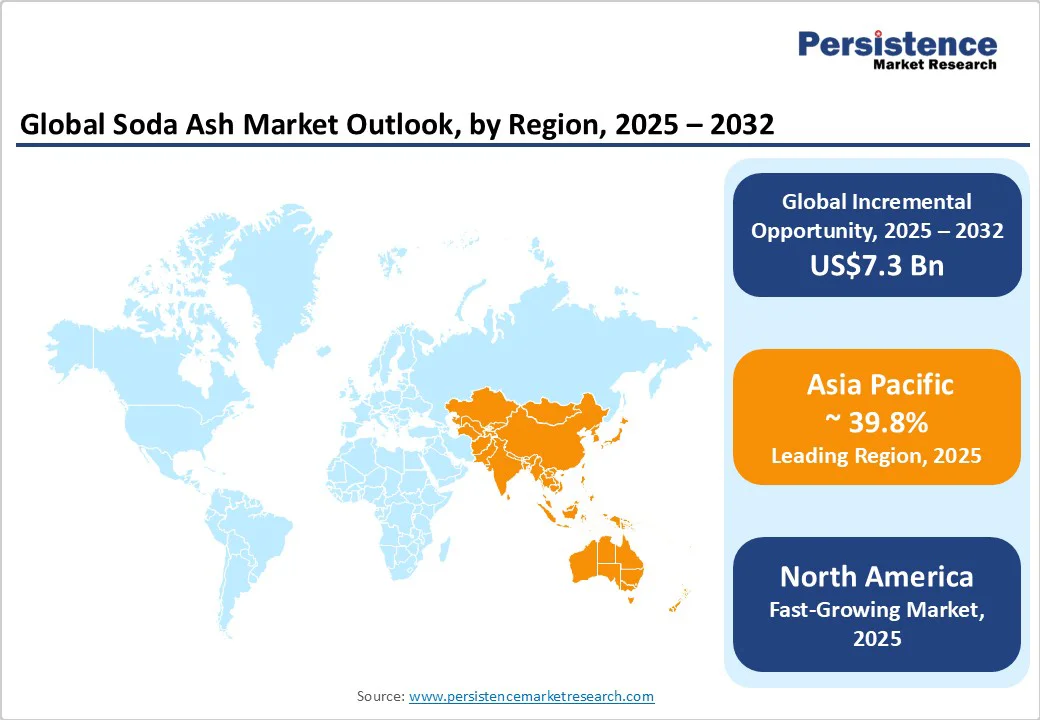

- Leading Region: Asia Pacific leads the soda ash market, driven primarily by China, accounting for over 39.8% of the market share.

- Fastest-growing Region: North America is the fastest-growing region, supported by trona-based natural soda ash production, expanding exports, and infrastructure-driven domestic demand.

- Investment Plans: Key players are investing in low-carbon production technologies, capacity expansion in emerging markets, and greenfield projects in India and ASEAN to meet growing demand.

- Dominant End-user: Glass remains the dominant end-use segment, accounting for 51% of global soda ash consumption, with flat and container glass applications driving steady demand.

- Leading Production Type: Synthetic soda ash is the leading production type, holding 57.6% of market share, supporting specialty glass, chemical intermediates, and industrial applications in Europe and Asia.

| Key Insights | Details |

|---|---|

|

Soda Ash Market Size (2025E) |

US$21.9 Bn |

|

Market Value Forecast (2032F) |

US$29.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.2%= |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Glass Industry Expansion

Glass manufacturing, including flat, container, and solar glass, accounts for nearly 45–53% of global soda ash consumption. Growth in solar-grade glass and energy-efficient building materials in Asia and other emerging regions is driving incremental demand. This structural demand ensures a predictable offtake for producers and supports investment in natural trona and synthetic capacity.

Industrial Chemicals and Detergents

Chemicals and detergents represent a significant portion of soda ash consumption, supporting a stable baseline demand. Soda ash is a key raw material for sodium bicarbonate, sodium silicates, and detergents. Growth in industrial processing and detergent use in emerging markets ensures steady demand and balances cyclical swings in the glass segment.

Sustainability and Low-carbon Production Investment

Producers are increasingly adopting low-emission processes and renewable energy sources to reduce CO? intensity. These investments not only comply with regulatory requirements but also create a premium for low-carbon soda ash. Over time, this trend reshapes capacity allocation and enhances long-term competitiveness.

Barrier Analysis - Price Volatility and Chinese Supply Cycles

China, a dominant soda ash producer, exerts a strong influence on global pricing. Production fluctuations and export policy changes have historically led to price swings of 20–35%, pressuring margins for other producers. This volatility can affect working capital management and investment planning, particularly for export-oriented operations.

Energy, Water, and Regulatory Compliance Costs

Soda ash production, especially via the synthetic Solvay process, is energy- and water-intensive, with high CO? emissions. Tightening environmental regulations and carbon pricing can increase operating expenses and necessitate significant capital investment in emission-control technologies. Synthetic plants, in particular, face higher breakeven costs without process improvements.

Opportunity Analysis - Low-carbon Soda Ash and Premium Contracts

Demand for low-carbon soda ash is rising among industrial buyers seeking to reduce Scope-3 emissions. Suppliers offering low-emission products can capture premium pricing, potentially generating an incremental revenue pool of US$200–400 million annually by 2030.

Emerging-market Glass Demand and Solar Glass Growth

Rapid urbanization in Asia and increased solar PV deployment are creating above-average growth for flat and solar glass applications. This trend is expected to add millions of tonnes of soda ash demand by 2030, offering significant revenue potential for suppliers who secure long-term offtake agreements.

Category-wise Analysis

Production Type Insights

Synthetic soda ash continues to dominate the market with a market share of 57.6% in 2025, due to the widespread adoption of the Solvay process in Europe and Asia. Large-scale producers such as Solvay in Belgium and GHCL in India supply synthetic soda ash to industrial clusters where natural trona deposits are unavailable. This type of soda ash is especially important for specialty glass applications, including high-performance flat glass, optical glass, and laboratory-grade glass, which require stringent purity levels. Synthetic soda ash also enables manufacturers to produce uniform particle sizes, which is critical for chemical intermediates such as sodium silicate and sodium bicarbonate.

Natural soda ash is experiencing the fastest growth globally due to its lower carbon footprint, reduced energy requirements, and cost advantage per tonne. Key trona-producing regions include Wyoming (USA), Turkey, and parts of Africa, where investments in extraction and processing are increasing. Companies such as Ciner Group in Turkey and We Soda in the U.S. are expanding trona production to meet rising export demand. Natural soda ash is particularly attractive for bulk glass production in emerging markets, including China and India, where cost efficiency and sustainability considerations drive procurement decisions.

End-user Insights

Glass manufacturing remains the largest end-use segment for soda ash, accounting for approximately 51% of market share in 2025. This includes flat glass for construction and automotive industries, container glass for beverages and food packaging, and specialty glass such as borosilicate and solar glass. The growth of energy-efficient buildings in Europe and the increasing penetration of automotive glass in North America have contributed to a steady demand. Major producers often secure long-term supply contracts with glass manufacturers, ensuring predictable demand. For example, Solvay supplies soda ash for flat glass production used in solar panels in Germany and India, aligning with renewable energy infrastructure growth.

The detergents segment is the fastest-growing end-use category, supported by rising household and industrial cleaning product demand, particularly in Asia Pacific and Latin America. Soda ash serves as a key ingredient in laundry detergents, dishwashing powders, and cleaning agents, enhancing alkalinity and improving surfactant performance. Rapid urbanization, population growth, and higher hygiene awareness are boosting detergent consumption in countries such as India, China, and Indonesia. Producers such as Nirma Ltd. and GHCL Limited are expanding production capacity for light soda ash to cater to this growing market, while investing in packaged and specialty-grade soda ash formulations to enhance product value and profitability.

Regional Insights

Asia Pacific Soda Ash Market Trends

Asia Pacific is the largest global consumption region, with China alone accounting for more than 39.8% of total soda ash volumes. The region’s demand is driven by rapid urbanization, container and flat glass production, solar panel installations, and detergent manufacturing. China’s production decisions heavily influence global pricing, while India and Southeast Asian markets are experiencing rapid growth in infrastructure, construction, and renewable energy deployment.

Recent developments include Ciner Group’s exports of natural soda ash from Turkey to Asia, expansions of domestic Indian production by Tata Chemicals, and greenfield projects in ASEAN countries to meet rising industrial and solar glass demand. Producers are also increasingly focusing on low-carbon capacity and process optimization to reduce emissions and energy costs while remaining competitive on price and logistics. India’s growing middle class and industrialization are driving higher soda ash consumption for glass, chemicals, and detergents. Tata Chemicals has expanded its synthetic and natural soda ash facilities to meet both domestic and export demand, while government initiatives to support solar and energy-efficient construction are boosting the consumption of high-purity soda ash.

North America Soda Ash Market Trends

North America is the fastest-growing region and a major producer and exporter of natural soda ash, driven primarily by the Green River trona deposits in Wyoming, which provide one of the lowest-cost feedstocks globally. U.S. domestic production reached approximately 11.7 million tonnes in 2019, and it continues to meet both domestic industrial demand and export requirements. Soda ash consumption in the region is largely supported by the construction sector, automotive glass manufacturing, and chemical industries, including detergents and sodium silicate production.

Recent developments include We Soda’s expansion of trona processing facilities in Wyoming to increase export capacity to Latin America and Asia, as well as investments in low-carbon process upgrades by Solvay and Ciner Group to reduce CO? intensity and align with sustainability commitments. Regulatory compliance with EPA emission standards and water usage rules influences plant modernization and operational costs, particularly for synthetic production. The U.S. maintains a competitive advantage due to its abundant natural trona deposits, low production costs, and established logistics for export. Wyoming producers have long-term supply contracts with glass manufacturers in North America and abroad, ensuring stable demand and supporting new investment in decarbonization projects.

Europe Soda Ash Market Trends

Europe predominantly relies on synthetic soda ash production, with Germany, France, and the U.K. representing the largest demand centers. The main end-use applications include flat glass for construction and automotive sectors, container glass, and specialty chemical manufacturing. Regulatory pressures under the EU Green Deal, including carbon pricing and stricter emission limits, are prompting legacy plants to modernize and adopt lower-carbon production technologies.

Recent developments include Solvay’s modernization of European facilities to improve energy efficiency and reduce CO? emissions, and CIECH S.A.’s investment in advanced synthetic soda ash production to meet rising quality standards for automotive and specialty glass. Long-term strategic partnerships between soda ash producers and glass OEMs in Germany are emerging to secure supply for high-performance flat glass and solar glass production. Germany is a key market for high-quality soda ash due to its strong automotive and renewable energy sectors. German producers are increasingly adopting decarbonization measures and forming direct supply agreements with glass manufacturers, ensuring long-term market stability and compliance with EU environmental standards.

Competitive Landscape

The global soda ash market is moderately concentrated, with leading players controlling significant low-cost and exportable capacity. Competition is based on feedstock type, production cost, logistics footprint, and environmental performance. Top companies collectively influence pricing, innovation, and market trends.

Key strategies include cost leadership through trona access, technological differentiation with low-carbon production, and market expansion via long-term contracts with glass OEMs. Vertical integration into specialty chemicals and sustainability-linked supply agreements are emerging trends.

Key Industry Highlights

- In May 2025, CIECH S.A. modernized its synthetic soda ash plant in Poland with energy recovery systems and emission control technology to comply with EU Green Deal regulations and reduce operational carbon footprint.

- In February 2025, We Soda commenced a strategic partnership with a major U.S. glass manufacturer to supply trona-based natural soda ash, securing long-term contracts and strengthening its footprint in North America.

Companies Covered in Soda Ash Market

- Solvay S.A.

- Tata Chemicals Ltd.

- Ciner Group

- Nirma Ltd.

- Shandong Haihua

- GHCL Limited

- CIECH S.A.

- We Soda

- OCI N.V.

- FMC Corporation

- Tronox Holdings PLC

- Occidental Petroleum Corporation

- Tata Chemicals Europe

- Soda Sanayii A.S.

- Gujarat Narmada Valley Fertilizers & Chemicals (GNFC)

- China National Chemical Corporation (ChemChina)

- Searles Valley Minerals

- Anhui Tianda Chemical Co., Ltd.

- Sichuan Tianqi Soda Ash Co., Ltd.

- Novacarb Group

Frequently Asked Questions

The market size in 2025 is estimated at US$21.9 Billion.

By 2032, the market is projected to reach US$29.4 Billion.

Key trends include rising demand from the glass industry, expansion of solar and flat glass applications, growth in low-carbon and sustainable production, increasing consumption in detergents and chemicals, and capacity expansions in emerging markets such as India and Southeast Asia.

The leading segment by end-use is glass, which accounts for 45-53% of total consumption globally.