- Automotive Components & Materials

- Forestry Equipment Tires Market

Forestry Equipment Tires Market Size, Share, and Growth Forecast 2025 - 2032

Forestry Equipment Tires Market By Tire Type (Pneumatic Tires, Solid Tires, Polymer-based Tires), Equipment (Forestry Tractors, Forestry Harvesters, Trailers, Forwarders, Forestry Skidders, Others), Sales Channel, Regional Analysis 2025 - 2032

Forestry Equipment Tires Market Share and Trends Analysis

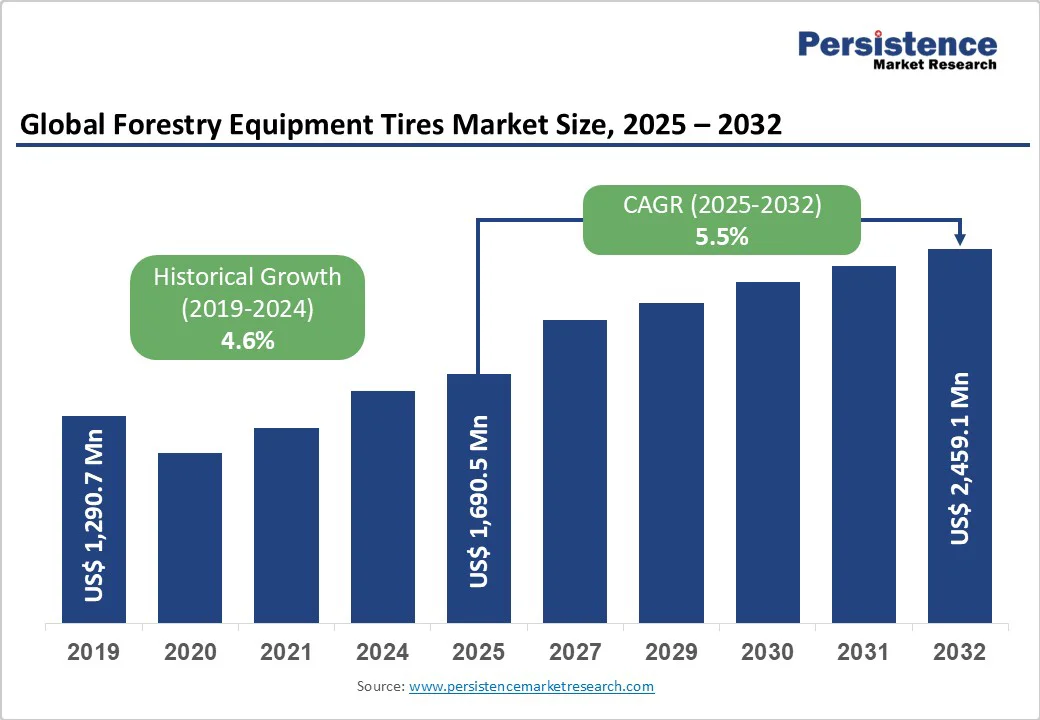

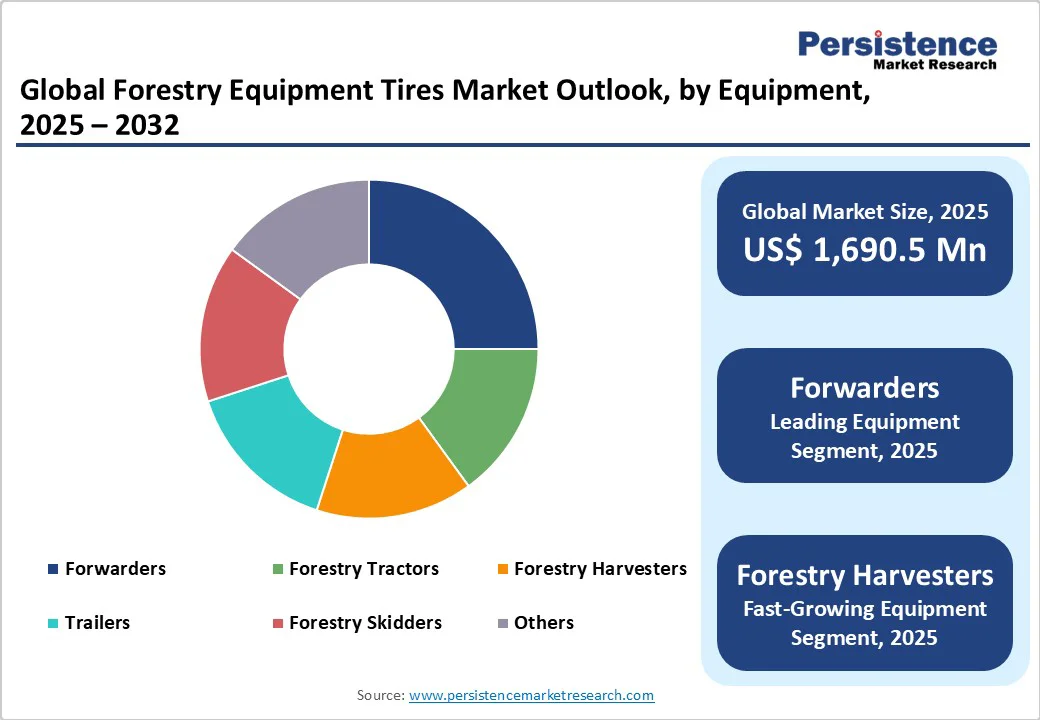

The global forestry equipment tires market size was valued at US$ 1,690.5 Mn in 2025 and is projected to reach US$ 2,459.1 Mn by 2032, growing at a CAGR of 5.5% between 2025 and 2032.

The market growth is propelled due to rising global demand for timber and sustainable forestry practices, which necessitate durable tires for heavy machinery operating in rugged terrains.

The FAO Global Forest Resources Assessment 2025 reports that industrial roundwood consumption grew by 1.5% annually till 2023, reflecting heightened demand in Asia and Africa.

Key Market Highlights

- Regional Leader: North America dominates as the leading region, driven by vast U.S. and Canadian timberlands supporting advanced mechanization and sustainable logging practices for efficient tire demand.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, fueled by China's afforestation and India's infrastructure boom, enhancing mechanized forestry and tire adoption rates.

- Leading Segment: Pneumatic Tires represent the dominant segment with a share of 60%, offering versatile traction essential for diverse equipment in global logging operations.

- Fastest Growing Segment: Solid Tires are the fastest-growing segment, gaining traction for puncture resistance in rugged terrains amid rising sustainable equipment use.

- Growth Opportunities: Advancements in eco-friendly tire tech offer key opportunities, targeting low-impact designs for expanding agroforestry and compliant markets.

| Key Insights | Details |

|---|---|

| Forestry Equipment Tires Market Size (2025E) | US$ 1,690.5 Mn |

| Market Value Forecast (2032F) | US$ 2,459.1 Mn |

| Projected Growth CAGR (2025-2032) | 5.5% |

| Historical Market Growth (2019-2024) | 4.6% |

Market Dynamics

Driver - Rising Mechanization in Forestry Operations

The increasing adoption of mechanized equipment in forestry significantly propels the demand for specialized tires designed for harsh environments. With global timber production reaching over 2 billion cubic meters annually, as reported by the Food and Agriculture Organization (FAO), operations require tires that offer superior traction on uneven terrain to boost productivity and safety.

This driver is evident in the shift towards automated harvesters and forwarders, reducing manual labor while minimizing downtime through durable tire designs that withstand punctures and heavy loads. Consequently, tire manufacturers are investing in reinforced compounds, leading to enhanced operational efficiency.

Emphasis on Sustainable Forestry Practices

Sustainable logging practices are accelerating tire innovation to reduce environmental impact, driving market expansion. The FAO highlights that over 1.5 billion hectares of forests are managed sustainably worldwide, necessitating low-compaction tires that preserve soil health during extraction.

These practices, including reduced-impact logging, benefit from polymer-enhanced tires that distribute weight evenly, cutting soil disturbance by up to 30% compared to traditional options. It not only complies with global standards but also appeals to eco-conscious operators, fostering long-term market resilience through tires that align with certification programs like those from the Forest Stewardship Council (FSC).

Market Restraints

Fluctuating Raw Material Prices

Volatility in natural rubber and synthetic compounds poses a major challenge, increasing production costs and affecting affordability. Rubber prices surged by 25% in 2024 due to supply chain disruptions, as noted in reports from the International Rubber Study Group, squeezing margins for tire producers.

This restraint hampers scalability, particularly for small operators in developing regions, potentially delaying equipment upgrades and slowing overall market penetration. Moreover, reliance on imported materials exposes the sector to geopolitical risks, further complicating cost management.

Stringent Environmental Regulations

Regulatory hurdles, such as the EU Deforestation Regulation effective from December 2024, impose strict compliance on tire materials derived from rubber, raising operational complexities.

These rules require traceability to deforestation-free sources, increasing certification costs by an estimated 15-20% for suppliers, as per European Commission guidelines. This negatively impacts smaller manufacturers, unable to adapt quickly, potentially reducing innovation pace and market entry for compliant products.

Opportunity - Advancements in Low-Impact Tire Technologies

The push for eco-friendly tires presents significant potential, especially in sustainable forestry segments where low-compaction designs can capture growing demand. With the FSC certifying over 200 million hectares globally, tires using biodegradable polymers could reduce environmental footprint by 40%, according to FAO studies on soil preservation.

Recent developments, such as reinforced sidewalls for better flotation, align with precision forestry tools, enabling operators to access sensitive areas without damage. This opportunity is amplified in the Agroforestry Market, where integrated land management boosts tire needs for versatile equipment, promising revenue growth for innovators targeting certification-compliant products.

Expansion in Emerging Forestry Markets

Rapid growth in Asia-Pacific and Latin America offers lucrative prospects for tire suppliers focusing on affordable, high-durability options for expanding plantations. Brazil's afforestation programs, covering 10 million hectares by 2030 as per government initiatives, drive demand for rugged tires suited to tropical terrains.

Technological integrations like sensor-embedded tires for real-time monitoring can enhance efficiency in these regions, where mechanization rates are rising at 7% annually, per World Bank data. This taps into the Forestry Trailers Market dynamics, where trailer-compatible tires support export-oriented timber transport, yielding substantial market share for adaptable manufacturers.

Category-wise Insights

Tire Type Analysis

Pneumatic Tires dominate the Tire Type category with a 60% market share, owing to their superior traction and shock absorption in variable forestry conditions. These air-filled tires excel in providing flexibility on soft soils, reducing operator fatigue during long shifts, as supported by USDA Forest Service reports on equipment performance in logged areas.

Their widespread use in standard harvesters and skidders, handling loads up to 20 tons, justifies leadership, with radial variants offering 20% better fuel efficiency as per Tire Technology International analyses. This segment's adaptability integrates seamlessly with the Forestry Machinery Market, ensuring minimal downtime in demanding operations.

Equipment Analysis

Forwarders lead the Equipment category at 25% share, driven by their role in low-impact log transport across global forests. These machines, equipped with cranes for suspended loads, minimize ground disturbance, aligning with sustainable standards from the FSC that cover 18% of managed forests.

Data from the FAO indicates forwarders process over 50% of timber in mechanized operations, favoring tires with high flotation to navigate muddy terrains without compaction. Their prevalence in selective logging enhances efficiency, making them indispensable in regions like Scandinavia.

Sales Channel Analysis

Aftermarket holds the top position in the Sales Channel category with 55% share, fueled by the need for frequent replacements in rugged forestry use. Operators prefer aftermarket for customized fits, extending equipment life by up to 30% through retreading, as per International Tire & Rubber Association guidelines.

This channel benefits from established dealer networks, supporting diverse needs like puncture-resistant upgrades, and reflects the sector's focus on maintenance amid rising operational costs. It also allows integration with evolving Forestry Trailers Market requirements for trailer-specific tires.

Regional Insights

North America Forestry Equipment Tires Trends

North America spearheads the global market, with the U.S. leading due to extensive commercial logging spanning 300 million acres of forestland, per USDA data. Advanced mechanization, including GPS-enabled forwarders, demands high-performance tires for efficiency, supported by innovations from domestic manufacturers. Regulatory frameworks like the U.S. Forest Service guidelines emphasize low-emission operations, promoting tires that reduce soil impact by 25%.

The region's innovative ecosystem thrives on R&D investments, with over $500 million allocated annually to forestry tech by the National Institute of Food and Agriculture, fostering tire designs for extreme weather. This sustains leadership in sustainable practices, integrating with the Agroforestry Market for dual-use equipment.

Europe Forestry Equipment Tires Trends

Europe's market emphasizes regulatory harmonization, with Germany, the U.K., France, and Spain driving 40% of regional activity through strict EU Timber Regulation compliance. In Germany, precision forestry in 11 million hectares of forests requires low-compaction tires, reducing erosion as per European Forest Institute studies. France and Spain focus on Mediterranean terrains, where tires with enhanced grip support 20% annual timber growth.

The U.K. advances with post-Brexit policies promoting recycled materials, aligning with the EU Deforestation Regulation to ensure deforestation-free rubber since 2020. This harmonization boosts the adoption of eco-tires, evident in Sweden and Finland's certified operations covering 23 million hectares.

Asia Pacific Forestry Equipment Tires Trends

Asia Pacific exhibits robust growth, led by China, Japan, and India, where manufacturing advantages fuel 30% global tire production. China's afforestation of 78 million hectares drives demand for durable tires in large-scale logging, with exports rising 15% yearly according to the State Forestry Administration. India and ASEAN nations benefit from cost-effective production, supporting mechanization in 250 million hectares of forests.

Japan integrates precision tech in its 25 million hectares, using sensor tires for optimal traction, as highlighted by the Ministry of Agriculture, Forestry, and Fisheries. This dynamism, coupled with Agroforestry Market expansion, positions the region for 6% CAGR through infrastructure investments.

Competitive Landscape

The global forestry equipment tires market exhibits a consolidated structure, with top players controlling a 60% share through global supply chains and R&D focus. Companies pursue expansion via partnerships, like joint ventures for sustainable materials, while investing $1 billion annually in innovations such as radial designs for better durability.

Key differentiators include eco-compliant tires, with leaders emphasizing low-compaction tech to meet FSC standards. Emerging models trend towards subscription-based tire management, enhancing uptime in fragmented regional markets.

Key Market Developments:

- December 2024: CEAT Specialty launched the LOGGER XL (LS2) tire for skidders, featuring reinforced sidewalls for puncture resistance in harsh terrains.

- January 2025: Hankook Tire introduced Optimo sub-brand tires adaptable for forestry applications, focusing on value-driven durability and traction enhancements.

- May 2025: PRINX entered the OTR segment with ELD12 tires for loaders, emphasizing environmental compliance for European forestry equipment. Companies Covered in Forestry Equipment Tires Market.

Companies Covered in Forestry Equipment Tires Market

- Michelin

- Nokian Tyres Plc

- Bridgestone Corporation

- Titan International, Inc.

- Balkrishna Industries Limited

- The Yokohama Rubber Co. Ltd.

- Qingdao Qizhou Rubber Co. Ltd.

- Maxam Tire International Ltd

- Tianjin United Tire & Rubber International Company Ltd

- Aichi

- Camso

- Continental AG

- Trelleborg Group

Frequently Asked Questions

The forestry equipment tires market is expected to reach US$ 2,459.1 Mn by 2032, growing from US$ 1,690.5 Mn in 2025 at a 5.5% CAGR.

Rising mechanization in sustainable forestry operations drives demand, with global timber needs exceeding 2 billion cubic meters annually, per FAO.

Pneumatic Tires lead with a 60% share, valued for traction and adaptability in rugged terrains.

North America leads, powered by U.S. commercial logging across 300 million acres and advanced regulations.

Low-impact tire technologies offer growth, reducing soil compaction by 40% in certified sustainable forests.

Top players include MICHELIN, Bridgestone Corporation, and Nokian Tyres plc, dominating through innovative and durable offerings.