- Medical Devices

- Examination Tables Market

Examination Tables Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Examination Tables Market by Product Type (General Examination Tables, Special Examination Tables), Source Type (Powered, Manual), End-user, and Regional Analysis from 2026 - 2033

Examination Tables Market Share and Trends Analysis

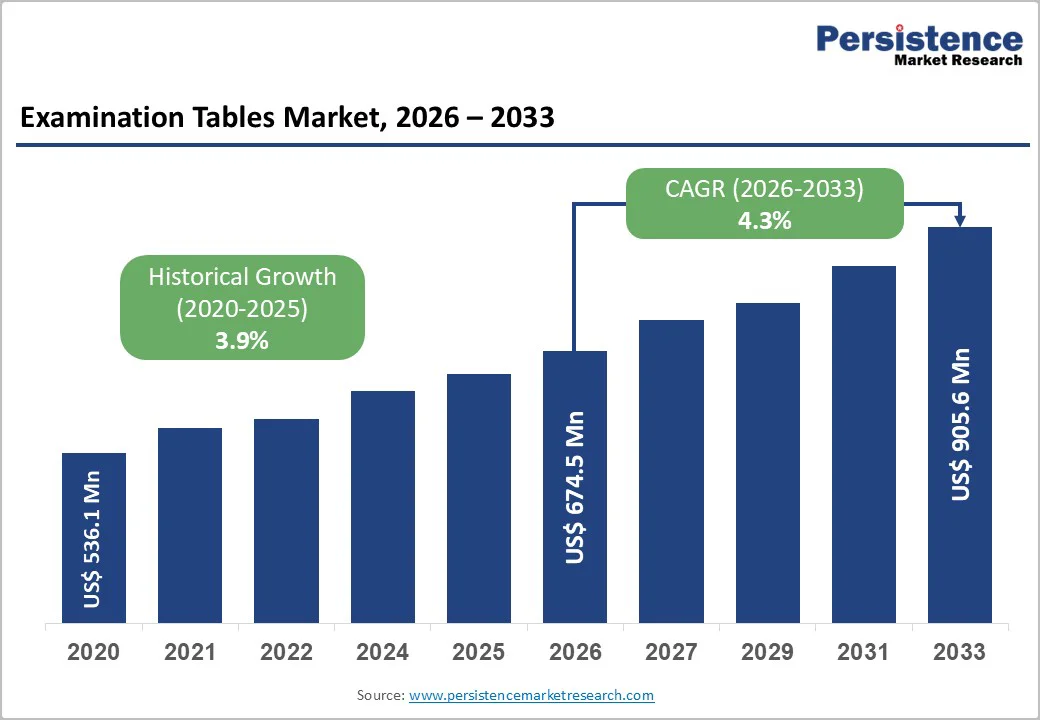

The global examination tables market size is estimated to grow from US$ 674.5 million in 2026 to US$ 905.6 million by 2033. The market is projected to record a CAGR of 4.3% from 2026 to 2033. There are two main types of examination tables, namely treatment tables and procedure or exam tables. The global examination tables market encompasses a range of medical furniture used in patient examination and treatment across hospitals, clinics, diagnostic centers, and specialty care facilities.

Rising healthcare infrastructure investments, increasing patient visits, and a growing focus on improving clinical workflows are key trends driving market growth. Demand is also supported by ergonomic design innovations, adjustable and multi-functional tables that enhance patient comfort and provider efficiency, and rising adoption in emerging markets. Additionally, advancements such as integrated digital features and compatibility with diagnostic equipment are shaping product development, positioning the market for steady expansion in the coming years.

Key Industry Highlights

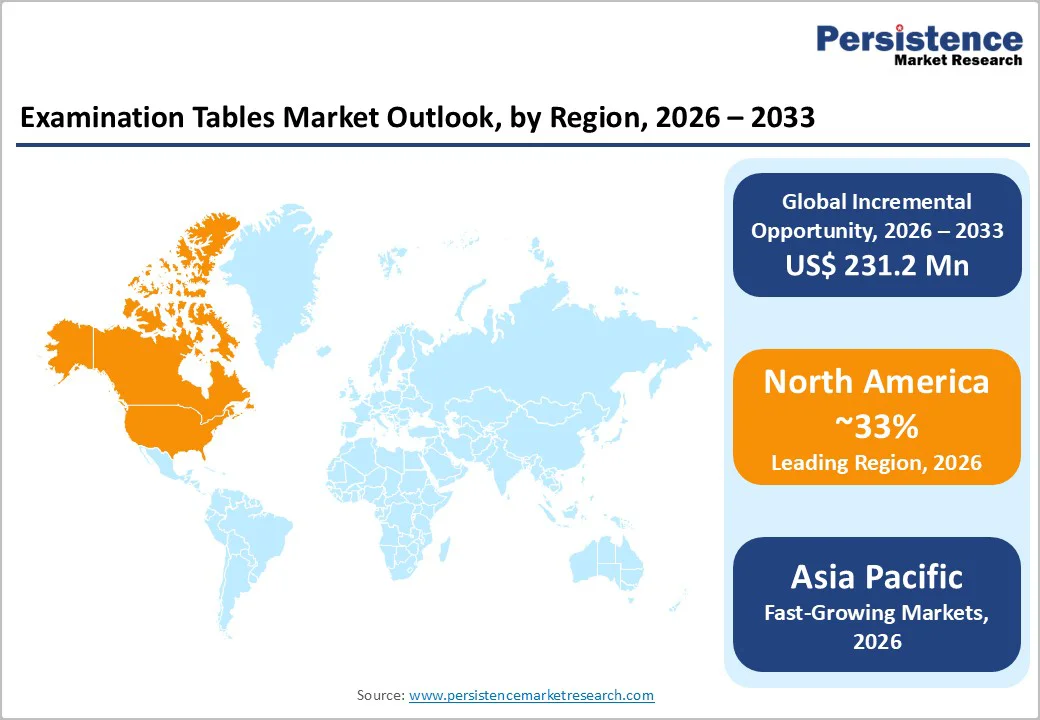

- Leading Region: North America, driven by advanced agricultural infrastructure, supported by high healthcare spending, dense hospital and ASC networks, and a strong focus on safety, accessibility, and infection control compliance.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market for examination tables, driven by rapid hospital construction, the expansion of private clinics and ASCs, and manufacturing cost advantages in China, India, and the ASEAN economies.

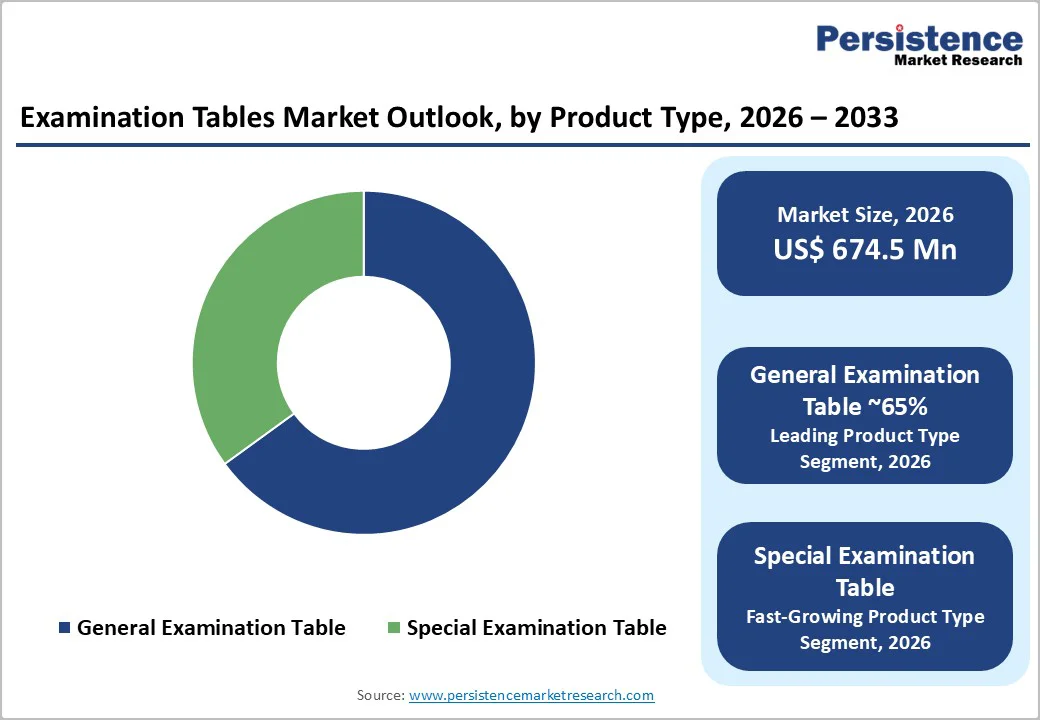

- Dominant Segment: General examination tables lead the examination tables market, due to their broad use across primary care and outpatient settings and favorable economics for large-scale deployment in growing health systems.

- Fastest Growing Segment: Special examination tables are the fastest-growing segment, driven by rising demand for bariatric, pediatric, and procedure-specific designs across expanding outpatient settings.

| Key Insights | Details |

|---|---|

|

Examination Tables Market Size (2026E) |

US$ 674.5 Mn |

|

Market Value Forecast (2033F) |

US$ 905.6 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

4.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.9% |

Market Dynamics

Driver - Rising Outpatient and Ambulatory Surgical Volumes

The global examination tables market is strongly driven by the increasing number of outpatient visits and the growth of ambulatory surgical centers (ASCs). A growing proportion of procedures is shifting from traditional inpatient hospital settings to outpatient facilities to reduce costs and enhance patient convenience. ASCs are performing more elective and minimally invasive surgeries, which rely on reliable, adjustable examination and procedure tables for preoperative and postoperative care.

Hospitals and clinics are investing in multi-purpose tables that allow quick adjustments, optimize room turnover, support bariatric and special-needs patients, and accommodate various diagnostic or procedural requirements. In high-volume markets such as the U.S., ASCs account for a significant share of same-day surgeries, prompting facilities to purchase ergonomic, durable, and multifunctional tables. This trend not only drives replacement demand for older tables but also stimulates incremental purchases as outpatient care expands. Facilities prioritize tables that enhance workflow efficiency, improve patient comfort, and integrate with specialty accessories, reinforcing sustained market growth. The demand for trajectory is particularly strong in regions where outpatient services are rapidly expanding, and healthcare providers seek operational efficiencies.

Restraints - High Capital Costs for Advanced Powered Tables

Adoption of advanced-powered examination tables is constrained by their high upfront capital costs, which limit accessibility for smaller clinics, rural facilities, and providers in low- and middle-income countries. These tables often feature electric actuators, integrated weighing scales, electronic controls, and automated adjustment mechanisms, significantly increasing purchase prices compared with standard manual tables. Budget-conscious healthcare providers frequently prioritize essential diagnostic and therapeutic equipment over premium furniture, particularly where operating budgets are tight.

Furthermore, reimbursement policies rarely differentiate based on the use of high-end tables, reducing financial incentives to invest in costly products. In facilities with modest patient volumes, the return on investment for advanced tables is harder to justify, making basic manual tables the preferred choice. Limited availability of financing options or leasing programs further restrains adoption in emerging markets. High maintenance and service requirements associated with powered tables also contribute to operational hesitancy. These factors collectively slow market penetration for premium tables despite technological advantages, creating a barrier to widespread deployment, especially in small-scale outpatient clinics or resource-constrained healthcare settings.

Opportunity - Infection-Control Features and Smart Integration

The global examination tables market presents significant opportunities through infection control innovations and smart technology integration. The COVID-19 pandemic intensified awareness of infection prevention, prompting healthcare facilities to adopt tables with antimicrobial surfaces, seamless upholstery, and designs that facilitate thorough disinfection. Easy-to-clean materials and construction that minimize contamination points help hospitals, clinics, and ASCs comply with strict hygiene protocols while protecting staff and patients. Beyond infection control, integrating smart technologies offers new value propositions.

Features such as memory positioning, occupancy sensors, and connectivity with electronic health record (EHR) systems streamline workflow, automate documentation, and improve operational efficiency. Electrically powered tables used in therapy, examination, and minor procedures have already demonstrated the benefits of advanced controls, setting expectations for the migration of technology into general and specialty examination tables. These advancements enable better patient experience, reduce staff workload, and support multi-functionality across outpatient, inpatient, and surgical care areas.

Manufacturers can develop hybrid solutions combining infection-resistant materials with digital automation, appealing to hospitals prioritizing safety, efficiency, and compliance. This dual focus on hygiene and smart integration is expected to drive incremental demand and differentiation in a competitive market.

Category-wise Analysis

By Product Type Insights

The general examination table segment is projected to dominate, accounting for approximately 65% of the global market in 2025. These tables are extensively utilized in primary care, internal medicine, pediatrics, and routine outpatient settings, where cost efficiency, durability, and versatility are prioritized. Multi-purpose designs with simple mechanical adjustments, standardized accessories, and robust construction meet the needs of high-patient-throughput environments. Budget-conscious healthcare facilities favor these tables over expensive specialty models.

Additionally, the special examination table segment is the fastest-growing category, driven by rising demand for procedure-specific, bariatric, pediatric, and diagnostic-focused tables. Specialty tables incorporate advanced features such as powered height adjustment, modular accessories, infection control surfaces, and ergonomic design, addressing the requirements of ambulatory surgical centers, specialty clinics, and high-end hospital units. Expansion of outpatient facilities, day care centers, and specialty treatment units is further stimulating adoption of these tables. The combination of volume-driven demand for general tables and rapid growth in specialty solutions ensures a balanced market trajectory, supporting both replacement cycles in established facilities and incremental demand in expanding healthcare infrastructure worldwide.

By End-User Insights

Hospitals represent the leading end-user segment in the global examination tables market, accounting for around 46% share in 2025. Large installed bases across emergency departments, outpatient clinics, and inpatient units drive high procurement volumes. Hospitals manage diverse patient populations requiring both general and specialized examinations, necessitating frequent replacement and upgrading of tables to comply with evolving safety, infection control, and accessibility standards. Steady procurement cycles are supported by institutional budgets and regulatory compliance mandates.

Ambulatory surgical centers (ASCs) and specialty clinics, however, are the fastest-growing end-user segments. Rising outpatient procedures, elective surgeries, diagnostic services, and chronic disease management are shifting care away from inpatient settings. This trend increases demand for versatile and procedure-ready tables that integrate adjustable heights, specialty accessories, and advanced infection control features. ASCs and specialty clinics prioritize tables that streamline workflow, support high patient turnover, and enable multi-functionality across consultation, preoperative, and postoperative areas. The combined effect of hospitals’ stable demand and rapid growth in outpatient and specialty facilities is shaping competitive dynamics and driving innovation in both general and speciality examination tables.

Region-wise Insights

North America Examination Tables Market Trends

North America, led by the U.S., is the dominant regional market, estimated to hold about 33% share in 2025, supported by high per-capita healthcare expenditure, extensive hospital and ASC networks, and strong adoption of technologically advanced equipment. The region’s robust innovation ecosystem, including medical-device clusters in states such as Minnesota, Indiana, and California, supports continuous product upgrades in ergonomics, powered actuation, and integration with digital health systems.

Stringent regulatory and accreditation frameworks, including U.S. FDA medical device requirements and Joint Commission standards for environment of care, encourage facilities to invest in tables that meet enhanced safety, infection-control, and accessibility benchmarks. Rapid expansion of ASCs, with estimates of nearly 9,600 operational centers in the U.S., further boosts demand for high-quality general and specialty examination tables used across pre-op, post-op, and consultation rooms.

Asia Pacific Examination Tables Market Trends

Asia Pacific is expected to be the fastest-growing market for examination tables, driven by the rapid expansion of healthcare infrastructure in China, India, Japan, and the ASEAN countries. Rising middle-class populations, government investments in public hospitals, and the growth of private multi-specialty chains are leading to the construction and upgrading of thousands of facilities that require basic and specialty examination furniture.

Cost-competitive manufacturing bases in China and parts of Southeast Asia provide advantages in producing manual and entry-level powered examination tables, enabling regional players to serve domestic demand and export to other emerging markets. In India and ASEAN, the proliferation of-day-care centers and ASCs– supported by policy measures encouraging affordable surgery outside tertiary hospitals – is expected to create strong incremental demand for versatile, durable tables that support high patient turnover at accessible price points.

Market Competitive Landscape

The global examination tables market is moderately fragmented, with a mix of multinational medical-device companies and specialized regional manufacturers. Leading players compete on ergonomics, build quality, customization options, aftersales service, and integration of powered mechanisms and infection-control features, while many smaller firms focus on cost-effective manual tables tailored to local standards and purchasing power. Strategic priorities include geographic expansion into high-growth Asia Pacific markets, development of bariatric-friendly and specialty tables, and partnerships with hospital groups and groups purchasing organizations (GPOs) to secure long-term supply contracts.

Key Industry Developments:

- In March 2024, AGA Sanitätsartikel GmbH expanded its range of height-adjustable examination tables with enhanced load capacity and modular accessories targeting outpatient clinics and day-surgery centers in Europe.

Companies Covered in Examination Tables Market

- Cardinal Health, Inc.

- Allengers Medical Systems Limited

- Narang Medical Limited

- Skytron Corporation

- United Metal Fabricators, Inc

- ADDvise Group AB

- Hamilton Medical AG

- Aero Healthcare AU Pty Ltd

- AGA Sanitätsartikel GmbH

- ArjoHuntleigh AB by Getinge Group

- Brewer Company

- Clinton Industries

- Favero Health Projects Spa

- Others

Frequently Asked Questions

The global examination tables market is projected to be valued at US$ 674.5 Mn in 2026.

Rising outpatient visits, growing chronic diseases, hospital expansions, ergonomic product demand, and increasing focus on patient comfort and safety drive market growth.

The global market is poised to witness a CAGR of 4.3% between 2026 and 2033.

Major opportunities include smart adjustable tables, bariatric models, specialized pediatric designs, and expanding sales in emerging markets, upgrading primary and secondary healthcare facilities.

Companies such as Cardinal Health, Inc., AGA Sanitätsartikel GmbH, ArjoHuntleigh AB by Getinge Group, Skytron Corporation, United Metal Fabricators, Inc., are some major players operating in the global esxamination tables market.