- Pharmaceuticals

- Dysphagia Management Market

Dysphagia Management Market Size, Share and Growth Forecast, 2026 - 2033

Dysphagia Management Market by Product (Drug, Feeding Tubes, Nutritional Solutions), Indication (Oropharyngeal Dysphagia, Esophageal Dysphagia), Distribution Channel (Hospital Pharmacies, Retail Pharmacies), and Regional Analysis for 2026 - 2033

Dysphagia Management Market Share and Trends Analysis

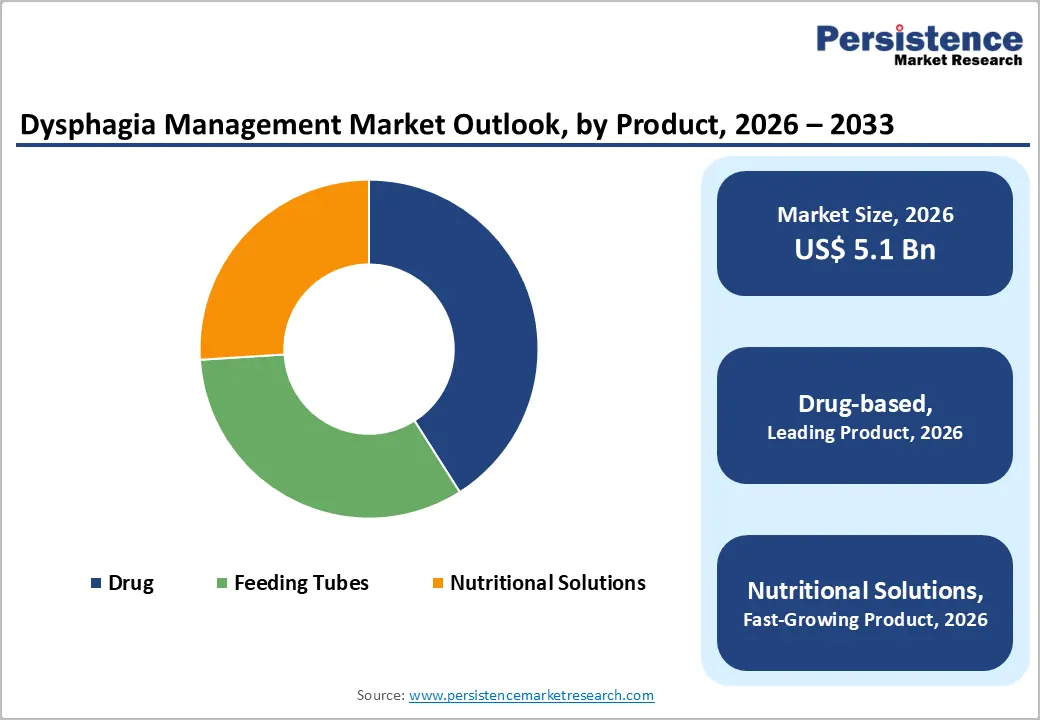

The global dysphagia management market size is likely to be valued at US$5.1 billion in 2026 and is projected to reach US$7.6 billion by 2033, growing at a CAGR of 5.9% during the forecast period 2026 - 2033, driven by the rising prevalence of neurological disorders, the expanding elderly population, and the increasing demand for swallowing disorder treatment across hospitals and long-term care facilities.

Higher cases of stroke, Parkinson’s disease, dementia, and head and neck cancers are driving the demand for dysphagia therapy products, enteral feeding devices, and specialized nutritional support. A stronger focus on patient safety and malnutrition prevention is supporting the adoption of clinical nutrition for swallowing disorders and rehabilitation solutions globally.

Key Industry Highlights:

- Product Segment Leadership: Drug-based therapies are set to lead with around 41% share in 2026, while nutritional solutions are projected to grow the fastest through 2033, due to the rising demand for clinical nutrition for swallowing disorders.

- Indication Segment Leadership: Oropharyngeal dysphagia is anticipated to dominate with nearly 64% share in 2026, while esophageal dysphagia is likely to witness the fastest growth owing to increasing gastrointestinal disease incidence.

- Distribution Channel Leadership: Hospital pharmacies are expected to lead in 2026, while retail pharmacies are projected to register the fastest growth during the forecast period, driven by expanding home healthcare adoption and the use of thickening agents for dysphagia.

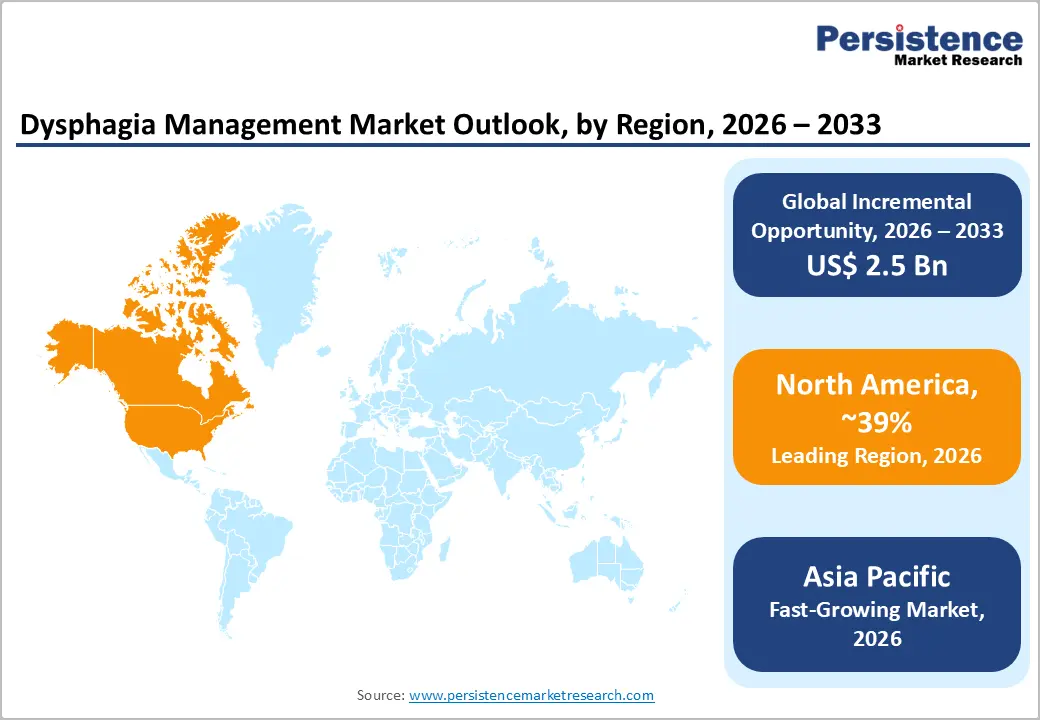

- Regional Leadership: North America is poised to dominate with nearly 39% share in 2026, while Asia Pacific is projected to record the fastest growth through 2033, supported by expanding healthcare infrastructure and aging populations.

- Competitive Environment: Competitive activity is centered on investments in dysphagia rehabilitation solutions, enteral feeding technologies, AI-assisted swallowing assessment tools, and specialized nutritional formulations.

DRO Analysis

Driver - Growing Global Burden of Neurological and Age-related Disorders Driving Dysphagia Care Demand

The rising prevalence of neurological diseases and geriatric conditions is a primary growth driver for the global dysphagia management market trends 2026 - 2033. According to the World Health Organization (WHO), the global population aged 60 years and above is projected to exceed 1.4 billion by 2030, significantly increasing the patient pool susceptible to swallowing dysfunction. Dysphagia affects nearly 50% of stroke survivors and approximately 80% of Parkinson’s disease patients, based on data from the U.S. National Institutes of Health (NIH) and the American Speech-Language-Hearing Association (ASHA).

Hospitals and long-term care facilities are therefore expanding investments in oropharyngeal dysphagia treatment, texture-modified nutrition, and rehabilitation protocols. Increased clinical awareness regarding aspiration pneumonia prevention and malnutrition management is also supporting broader adoption of dysphagia nutrition products market offerings across developed healthcare systems.

Restraint - High Treatment Costs and Limited Specialist Availability Restrict Market Growth

The market faces challenges related to treatment affordability and uneven healthcare infrastructure. Advanced enteral feeding devices, nutritional formulations, and rehabilitation therapies increase overall treatment costs and limit accessibility in low- and middle-income countries. According to the Centers for Medicare & Medicaid Services (CMS), dysphagia-related hospitalization costs in the U.S. exceed several billion dollars annually due to aspiration pneumonia and malnutrition complications. These financial pressures continue to restrict broader market penetration.

The shortage of trained speech-language pathologists and swallowing rehabilitation specialists remains another key barrier, particularly across emerging economies. Limited reimbursement coverage for specialized dysphagia therapy products and home-based nutritional care further affects long-term patient adherence. Rural healthcare systems continue to face gaps in diagnostic and rehabilitation capabilities, slowing early intervention rates. Lower awareness regarding swallowing disorder management also limits the adoption of advanced care solutions in underdeveloped regions.

Opportunity - Expansion of Home Healthcare and Clinical Nutrition, Creating New Growth Opportunities

The expansion of home healthcare services and medical nutrition programs is creating strong opportunities across the dysphagia management market. Healthcare systems are increasingly prioritizing outpatient rehabilitation and home-based nutritional support to reduce hospitalization costs and improve patient outcomes. According to ESPEN, malnutrition management remains a major priority among aging populations, particularly stroke and oncology patients. This trend is accelerating demand for portable feeding systems, thickening agents for dysphagia, and ready-to-consume nutritional formulations.

Asia Pacific and Latin America are emerging as high-potential markets due to expanding healthcare infrastructure and growing elderly populations. In 2025, ESPEN further strengthened its focus on early nutritional intervention and geriatric malnutrition management through updated clinical nutrition initiatives. Japan and China are also increasing investments in elderly rehabilitation and long-term care infrastructure, supporting wider adoption of dysphagia care solutions. Companies investing in AI-assisted swallowing assessment and digital rehabilitation technologies are expected to gain long-term advantages.

Category-wise Analysis

Product Insights

Drug-based therapies are expected to lead the product segment with approximately 41% market share in 2026, due to their widespread use in managing neurological and gastrointestinal conditions linked to dysphagia. Hospitals continue to rely on pharmacological treatments for stroke recovery, gastroesophageal reflux disease, and esophageal motility disorders. In January 2025, the U.S. FDA expanded pediatric clearance for enteral nutrition support products targeting safer nutritional management in vulnerable patient groups. This continues to strengthen demand for integrated swallowing disorder treatment solutions across hospital settings.

Nutritional solutions are projected to register the fastest growth during the forecast period, driven by rising awareness regarding malnutrition prevention among dysphagia patients. Demand for texture-modified foods and clinical nutrition for swallowing disorders is increasing across elderly care and rehabilitation facilities. In 2025, Japanese hospitals expanded nutrition support initiatives focused on texture-modified diets and dysphagia care management for aging populations. Manufacturers are also investing in fortified beverages, easy-to-swallow formulations, and personalized nutritional support products.

Indication Insights

Oropharyngeal dysphagia is anticipated to dominate the indication segment with nearly 64% share in 2026, due to its strong association with stroke, Parkinson’s disease, and other neurological disorders. Aging populations continue to increase patient incidence globally, particularly across developed healthcare systems. In 2025, rehabilitation hospitals in Vietnam expanded post-stroke dysphagia nutrition assessment programs to improve dietary suitability and recovery outcomes. Hospitals and rehabilitation centers are also increasing investments in oropharyngeal dysphagia treatment involving speech therapy and swallowing rehabilitation.

Esophageal dysphagia is projected to witness the fastest growth through 2033, due to the increasing prevalence of gastroesophageal reflux disease, obesity-related digestive disorders, and esophageal cancer. Advancements in endoscopic diagnostics and minimally invasive procedures are improving patient access to specialized treatment. In 2025, healthcare institutions expanded gastrointestinal rehabilitation and nutrition-focused recovery programs to address the rising digestive disease burden among elderly populations. Pharmaceutical innovation targeting esophageal motility disorders is further supporting segment expansion globally.

Distribution Channel Insights

Hospital pharmacies are projected to account for approximately 58% of total market revenue in 2026, due to the high concentration of dysphagia treatment within inpatient healthcare settings. Acute stroke care, oncology treatment, and post-surgical recovery programs continue to generate strong demand for feeding systems and dysphagia therapy products. In January 2025, the FDA granted expanded clearance to Gravitas Medical’s smart enteral feeding system, designed to improve feeding tube monitoring and placement accuracy. Strong reimbursement frameworks and physician-supervised treatment pathways continue to support channel dominance.

Retail pharmacies are expected to record the fastest growth during the forecast period, supported by expanding home healthcare and outpatient rehabilitation services. Patients are increasingly seeking convenient access to nutritional supplements and thickening agents for dysphagia through retail and online channels. In 2026, ENvue Medical expanded distribution of its FDA-cleared enteral feeding navigation platform across trauma centers and home-care-linked clinical settings in the U.S. Growing e-commerce integration and pharmacist-led counseling services are further accelerating segment growth.

Regional Analysis

North America Dysphagia Management Market Trends

North America is expected to account for nearly 39% of the global dysphagia management market in 2026, due to advanced healthcare infrastructure, high neurological disorder prevalence, and strong reimbursement systems. The region is witnessing rising adoption of dysphagia rehabilitation solutions, AI-assisted swallowing assessment technologies, and home-based nutritional care. Regulatory support from the U.S. FDA and growing elderly populations continue to strengthen long-term market demand.

U.S. Dysphagia Management Market Trends

The U.S. is projected to contribute approximately 38% of the North American market in 2026, due to its advanced rehabilitation ecosystem and large aging population. According to the CDC, stroke remains a major cause of long-term disability, increasing demand for swallowing disorder treatment solutions. In 2025, the FDA granted expanded clearance to advanced smart enteral feeding technologies aimed at improving patient monitoring and feeding accuracy.

Canada Dysphagia Management Market Trends

Canada is expected to account for nearly 14% of the regional market, supported by rising elderly care expenditure and increasing awareness regarding malnutrition management. Hospitals and long-term care centers are expanding the adoption of texture-modified nutritional therapies and rehabilitation programs. In 2025, Canadian healthcare institutions increased investments in chronic disease nutrition support initiatives targeting elderly and post-stroke patients.

Europe Dysphagia Management Market Trends

Europe accounts for a significant share of the global market, supported by strong public healthcare systems and an aging population. Demand for dysphagia therapy products, texture-modified foods, and specialized nutritional supplements continues to increase across elderly care programs. Harmonized regulatory standards under the EMA and expanding rehabilitation investments are further strengthening regional market adoption.

Germany Dysphagia Management Market Trends

Germany is anticipated to contribute approximately 24% of the Europe market in 2026, due to advanced rehabilitation infrastructure and high healthcare spending on neurological care. Hospitals are increasingly integrating swallowing rehabilitation and dietary management into post-stroke recovery programs. In 2025, German healthcare providers expanded elderly nutrition support initiatives focused on reducing malnutrition risks in long-term care settings.

U.K. Dysphagia Management Market Trends

The U.K. is projected to account for nearly 18% of the regional market in 2026, supported by growing investments in elderly care and outpatient rehabilitation services. National healthcare programs are strengthening their focus on early dysphagia diagnosis and nutritional intervention. In 2025, NHS-supported rehabilitation programs expanded multidisciplinary swallowing management services across elderly care centers.

Asia Pacific Dysphagia Management Market Trends

Asia Pacific is projected to record the fastest regional growth during the forecast period, due to expanding healthcare infrastructure, rising elderly populations, and increasing awareness regarding swallowing disorder treatment. Governments across the region are increasing healthcare spending on rehabilitation services and elderly nutrition programs. The growing demand for localized dysphagia nutrition products market solutions is further supporting regional expansion.

China Dysphagia Management Market Trends

China is expected to contribute approximately 36% of the Asia Pacific market in 2026, due to rapid healthcare modernization and expanding rehabilitation infrastructure. Demand for hospital-based nutrition management and post-stroke swallowing rehabilitation services continues to rise significantly. In 2025, China expanded elderly healthcare initiatives under national chronic disease management programs, supporting broader adoption of dysphagia care solutions.

Japan Dysphagia Management Market Trends

Japan is projected to account for nearly 17% of the regional market in 2026, owing to its rapidly aging population and high prevalence of swallowing disorders. Healthcare providers are increasingly adopting texture-modified diets, nutritional supplementation, and rehabilitation-focused elderly care programs. In 2025, Japanese hospitals expanded dysphagia-focused nutrition support initiatives aimed at improving geriatric recovery outcomes.

Competitive Landscape

The global dysphagia management market is moderately consolidated, with leading companies including Nestlé Health Science, Abbott Laboratories, Danone, and Fresenius Kabi accounting for a significant share of global revenue. These players benefit from strong hospital procurement networks, broad clinical nutrition portfolios, and established reimbursement access. Companies are increasingly investing in specialized nutritional formulations, enteral feeding technologies, and AI-assisted swallowing assessment systems to strengthen long-term market positioning.

Regional players such as SimplyThick LLC and Kent Precision Foods Group are expanding through texture-modified nutrition products and dysphagia-focused dietary solutions. Regulatory compliance and specialized rehabilitation requirements continue to create barriers for new entrants. However, growing demand for home healthcare and digital rehabilitation platforms is enabling smaller healthcare technology firms to enter the market through telehealth-based swallowing management solutions.

Key Industry Developments:

- In September 2025, Abbott Laboratories expanded its enteral nutrition portfolio through advanced protein-rich formulations targeting oncology and geriatric patients. The strategy strengthened its long-term positioning in hospital-based nutrition therapy programs.

- In January 2025, Nestlé Health Science expanded its medical nutrition manufacturing capabilities in Europe to strengthen the supply of specialized nutritional formulations for elderly and neurological patients. The investment supported regional demand growth for clinical nutrition for swallowing disorders.

Companies Covered in Dysphagia Management Market

- Nestlé Health Science

- Abbott Laboratories

- Danone

- Becton Dickinson and Company

- Cardinal Health

- Fresenius Kabi

- Hormel Foods Corporation

- Kent Precision Foods Group

- Medtronic

- Cook Medical

- Baxter International

- Nutricia

- Ajinomoto Co., Inc.

- SimplyThick LLC

Frequently Asked Questions

The global dysphagia management market is projected to reach US$5.1 billion in 2026.

Rising neurological disorders, aging populations, and demand for swallowing disorder treatment drive market growth.

The dysphagia management market is expected to grow at a CAGR of 5.9% from 2026 to 2033.

Growth is driven by home healthcare expansion, clinical nutrition adoption, and digital dysphagia care solutions.

Key players include Nestlé Health Science, Abbott Laboratories, Danone, and Fresenius Kabi.