- Specialty & Fine Chemicals

- Aviation Chemicals Market

Aviation Chemicals Market Size, Share, and Growth Forecast 2025 - 2032

Aviation Chemicals Market by Product Type (Paints & Coatings, Adhesives & Sealants, Lubricants & Coolants, Deicing & Anti-icing Fluids, Cleaning Chemicals, Others), Channel Type (Original Equipment Manufacturer (OEM), Maintenance, Repair, and Overhaul (MRO)), End-use (Civil Aviation, Commercial Cargo Aviation, Military & Space Exploration), Regional Analysis, 2025 - 2032

Aviation Chemicals Market Size and Trend Analysis

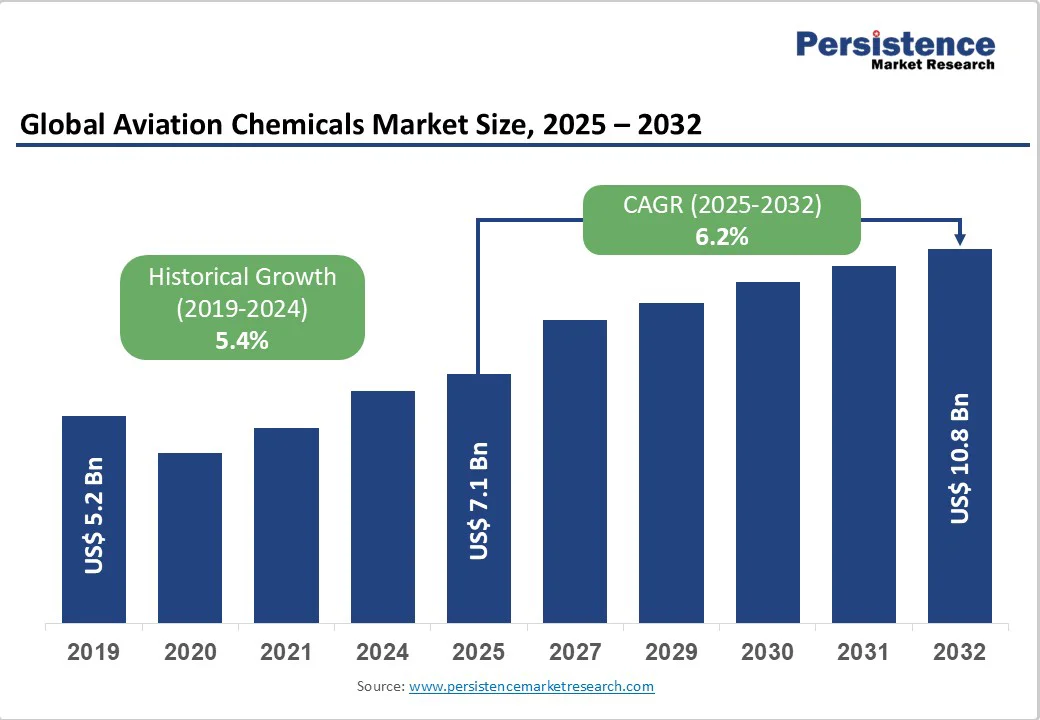

The global Aviation Chemicals Market size was valued at US$ 7.1 Bn in 2025 and is projected to reach US$ 10.8 Bn by 2032, growing at a CAGR of 6.2% between 2025 and 2032. The growth is driven by increasing air travel demand, expanding aircraft fleet modernization programs, and stringent aviation safety regulations requiring specialized chemicals. Rising demand for fuel-efficient aircraft and the need for advanced maintenance solutions are catalyzing market expansion globally.

Key Market Highlights

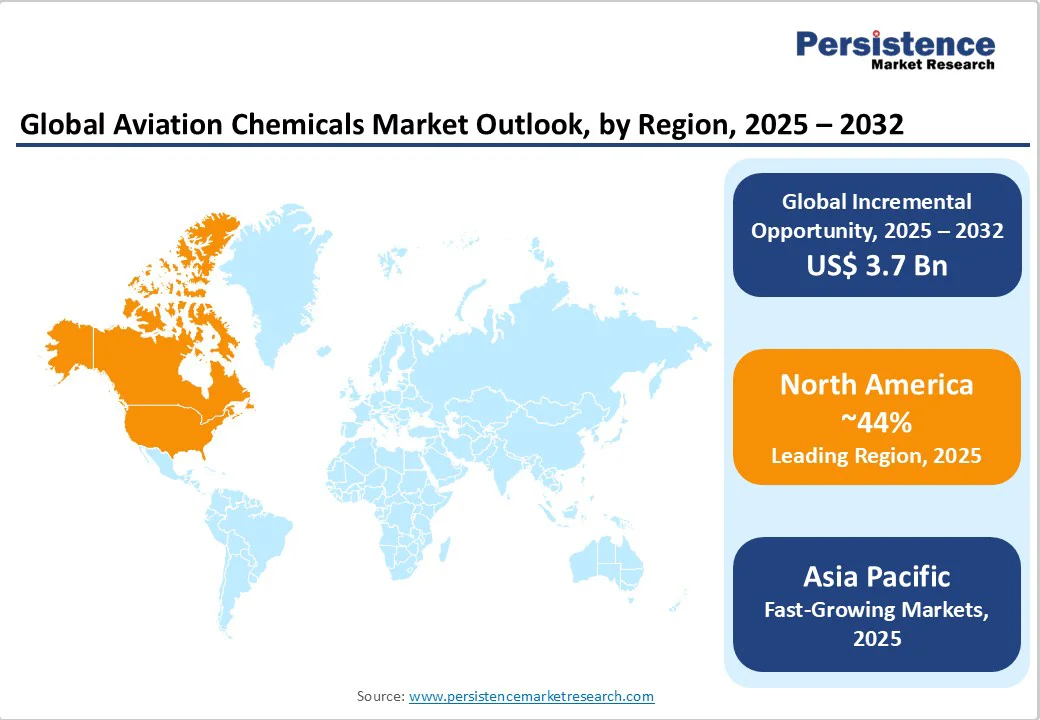

- Leading Region: North America leads the aviation chemicals market with 44% market share, driven by an established aerospace manufacturing base and extensive commercial aviation infrastructure

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region with a 7.3% CAGR through 2032, fueled by rapid economic growth and expanding aviation infrastructure investments

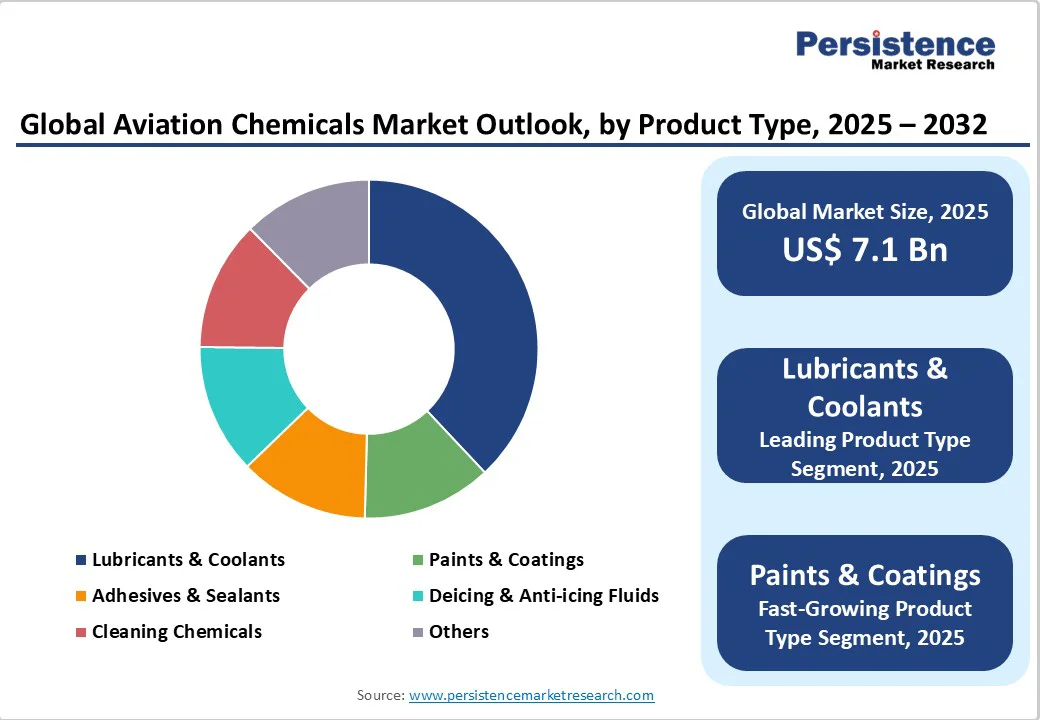

- Leading Product Type: Lubricants & Coolants segment dominates with 38% market share due to its critical role in engine performance and aircraft component protection requirements

- Fastest Growing End Use Segment: Civil Aviation represents the fastest-growing end-use segment with over 50% market share, driven by post-pandemic air travel recovery and fleet expansion programs

- Key Market Opportunity: Sustainable aviation chemicals present a key market opportunity as the industry pursues net-zero carbon emissions by 2050 through bio-based and eco-friendly formulations.

| Key Insights | Details |

|---|---|

|

Aviation Chemicals Market Size (2025E) |

US$ 7.1 Billion |

|

Market Value Forecast (2032F) |

US$ 10.8 Billion |

|

Projected Growth CAGR(2025-2032) |

6.2% |

|

Historical Market Growth (2019-2024) |

5.4% |

Market Dynamics

Market Growth Drivers

Rising Global Air Traffic and Fleet Expansion

The substantial increase in global air passenger traffic is driving unprecedented demand for aviation chemicals across all segments. According to industry data, the global aircraft fleet is anticipated to grow from approximately 7,200 aircraft in 2021 to over 8,300 by 2041 [15]. Airlines are significantly ramping up their aircraft procurement to meet rising air travel demand, with Airbus delivering 735 aircraft and Boeing delivering around 528 aircraft by the close of 2023 [28]. This expansion necessitates extensive use of aviation chemicals including lubricants, paints, coatings, and cleaning chemicals for both manufacturing and maintenance operations. The expanding fleet size directly correlates with increased consumption of aviation chemicals, particularly in the Aerospace Coatings Market which is experiencing robust growth driven by new aircraft deliveries and refurbishment requirements [25].

Stringent Aviation Safety and Environmental Regulations

Regulatory frameworks such as FAA, EASA, and ICAO standards are mandating the use of high-performance, certified aviation chemicals to ensure operational safety and environmental compliance [42]. The REACH (Registration, Evaluation, Authorisation, and Restriction of Chemicals) regulation is driving manufacturers to develop safer alternatives, particularly for substances like chromium-based coatings and PFASs (per- and polyfluoroalkyl substances) [10]. These regulations are compelling airlines and MRO providers to invest in advanced chemical formulations that meet strict performance criteria while reducing environmental impact. The growing emphasis on sustainable aviation practices is accelerating research and development in bio-based and low-toxicity aviation chemicals, creating new market opportunities for compliant products [43].

Market Restraints

Volatile Raw Material Costs and Supply Chain Disruptions

The aviation chemicals market faces significant challenges from fluctuating crude oil prices and raw material shortages, which directly impact manufacturing costs and pricing strategies [109]. Base oils derived from petroleum products are particularly susceptible to price volatility, affecting the production of lubricants and hydraulic fluids. Supply chain disruptions, including geopolitical tensions and natural disasters, can severely impact the availability of critical raw materials such as propylene glycol and ethylene glycol used in deicing fluids [23]. These challenges are compounded by the limited number of qualified suppliers who can meet aviation industry specifications, creating bottlenecks in the supply chain.

Complex Certification and Approval Processes

The aviation industry's stringent certification requirements create significant barriers for new chemical products entering the market. Each aviation chemical must undergo extensive testing and approval processes by multiple regulatory bodies including engine manufacturers, aircraft OEMs, and aviation authorities [70]. This process can take several years and requires substantial investment in testing and documentation. The lengthy approval timelines limit the introduction of innovative products and create market entry barriers for smaller manufacturers, potentially stifling innovation and competition in the aviation chemicals sector.

Market Opportunities

Advanced Air Mobility and Electric Aircraft Development

The emergence of electric vertical take-off and landing (eVTOL) aircraft and Advanced Air Mobility (AAM) platforms presents significant opportunities for specialized chemical formulations [12]. These next-generation aircraft require unique lubricants, thermal management fluids, and lightweight coatings designed for electric propulsion systems. Companies are investing in developing chemicals compatible with electric and hybrid aircraft technologies, including specialized battery cooling fluids and electromagnetic interference shielding materials [98]. The AAM industry is expected to advance design, testing, and certification in 2024 while preparing for commercialization in 2025, creating demand for innovative chemical solutions tailored to these emerging platforms.

Growing Focus on Sustainable and Bio-Based Chemical Solutions

The aviation industry's commitment to achieving net-zero carbon emissions by 2050 is driving demand for sustainable aviation chemicals including bio-based lubricants, eco-friendly cleaning agents, and environmentally acceptable deicing fluids [54]. Airlines and MRO providers are increasingly prioritizing procurement agreements with suppliers offering eco-certified products, particularly in North America and Europe where environmental compliance is strictly enforced [47]. The development of biodegradable and non-toxic formulations presents significant market opportunities, especially in the Expired Aviation Chemicals Market segment where proper disposal and recycling become critical considerations. This trend toward sustainable chemistry is fostering innovation in green alternatives that maintain performance while reducing environmental impact.

Category-wise Insights

Product Type Analysis

Lubricants & Coolants dominate the aviation chemicals market with approximately 38% market share in 2025, driven by their critical role in engine performance and aircraft component protection. These products are essential for reducing friction between metal parts and maintaining optimal operating temperatures in aircraft engines and hydraulic systems [48]. The segment benefits from continuous technological advancement in synthetic lubricant formulations, with products like Mobil Jet Oil 387 and Shell Aviation lubricants delivering superior performance across wide temperature ranges [67][70]. The growing demand for high-performance lubricants is fueled by increasing flight hours, extended aircraft service lives, and the need for enhanced fuel efficiency, making this segment particularly attractive for market participants.

Channel Type Analysis

Original Equipment Manufacturer (OEM) channels command approximately 63% market share in 2025, reflecting the higher volume of chemicals consumed during aircraft manufacturing compared to maintenance operations. OEM applications require specialized formulations for structural bonding, surface treatment, and protective coatings during the manufacturing process [45]. Major aircraft manufacturers like Boeing, Airbus, and defense contractors rely heavily on qualified aviation chemicals to meet stringent production specifications and certification requirements. The OEM segment benefits from long-term supply agreements and partnerships with chemical manufacturers, ensuring stable demand and predictable revenue streams for suppliers in this growing market segment.

End Use Analysis

Civil Aviation represents more than 50% market share in 2025, driven by the recovery and expansion of commercial air travel post-pandemic [48]. This segment includes passenger airlines, cargo carriers, and regional aviation operators who collectively consume the largest volumes of aviation chemicals for fleet maintenance and operations. The Civil Aviation segment benefits from increasing air passenger traffic, with the number predicted to exceed 8 billion by 2040 according to IATA projections [48]. Growing emphasis on aircraft safety, reliability, and operational efficiency continues to drive demand for high-quality aviation chemicals across all commercial aviation applications, making this the most substantial end-use segment for market participants.

Regional Insights

North America Aviation Chemicals Market Trends

North America dominates the global aviation chemicals market with 44% market share in 2025, primarily driven by the region's established aerospace manufacturing base and extensive commercial aviation infrastructure [55]. The United States leads this dominance with major aircraft manufacturers like Boeing, Lockheed Martin, and defense contractors creating substantial demand for specialized aviation chemicals. The region benefits from advanced MRO facilities and a large fleet of commercial and military aircraft requiring regular maintenance and chemical applications [64].

The region's regulatory framework, including EPA and FAA standards, drives demand for high-performance, environmentally compliant chemical formulations. U.S. aviation industry regulations mandate the use of Environmentally Acceptable Lubricants (EALs) in marine applications and promote sustainable aviation practices [75]. Major chemical manufacturers like ExxonMobil, PPG Industries, and Eastman Chemical Company maintain significant operations in North America, supporting both domestic and global aviation markets with advanced product development and technical support capabilities.

Europe Aviation Chemicals Market Trends

Europe represents a significant market for aviation chemicals, driven by major aerospace manufacturers including Airbus, Rolls-Royce, and Safran who require extensive chemical solutions for aircraft production and maintenance. The region's stringent environmental regulations, particularly REACH compliance requirements, are accelerating the development of safer, more sustainable aviation chemical alternatives [10]. European aviation authorities including EASA maintain rigorous certification standards that drive demand for high-quality, compliant chemical products.

Germany, United Kingdom, France, and Spain represent key markets within the region, each hosting significant aerospace manufacturing and MRO capabilities. European airlines and MRO providers are increasingly prioritizing eco-certified products and sustainable chemical solutions to meet regional environmental compliance requirements. The region's focus on reducing carbon emissions and promoting sustainable aviation practices creates opportunities for bio-based and environmentally friendly aviation chemical formulations.

Asia Pacific Aviation Chemicals Market Trends

Asia Pacific is the fastest-growing region in the aviation chemicals market with approximately 7.3% CAGR through 2032, driven by rapid economic growth and expanding aviation infrastructure across key markets [55]. China, Japan, India, and ASEAN countries are experiencing significant growth in air travel demand, leading to fleet expansion and increased chemical consumption. China's civil aviation market shows strong recovery with government support, and the sector has demonstrated a V-shaped recovery according to the Civil Aviation Administration of China (CAAC) [48].

The region benefits from substantial investments in airport infrastructure, MRO facilities, and domestic aircraft manufacturing capabilities. Asian countries are increasingly investing in defense aviation and space exploration programs, creating additional demand for specialized military-grade aviation chemicals. Singapore and Malaysia serve as regional MRO service hubs for both regional and international airlines, further driving chemical consumption. The region's growing middle class and increasing disposable income continue to fuel air travel demand, supporting sustained growth in aviation chemical requirements.

Competitive Landscape

The aviation chemicals market exhibits a moderately concentrated structure dominated by multinational corporations with extensive product portfolios and global distribution networks. Major players including ExxonMobil, BASF, Shell, PPG Industries, and Akzo Nobel maintain significant market share through comprehensive product offerings and established OEM relationships [103][107]. These companies leverage substantial investments in research and development to maintain technological leadership and meet evolving aviation industry requirements. Market competition is intensifying as emerging players focus on specialized eco-friendly chemicals and niche applications, while strategic collaborations between chemical innovators and aerospace OEMs as well as MRO providers are creating new competitive dynamics in the marketplace.

Key Market Developments

- October, 2024: PPG launched its AEROCRON® electrocoat primer technology that revolutionizes aerospace manufacturing by replacing manual spray-applied coating methods, delivering superior uniform corrosion protection while reducing material waste and VOC emissions.

- February, 2025: Henkel opened a new 35 million euro production facility for aerospace applications at its Montornès del Vallès, Spain site, designed to meet increasing demand for high-performance solutions aligned with lightweight construction and fuel efficiency trends.

- March, 2024: Shell introduced its new "Shell Flight" synthetic lubricant designed to enhance engine efficiency and reduce environmental impact, reflecting the industry's shift toward eco-friendly solutions and sustainability initiatives.

Competitive Landscape

By Product Type

- Paints & Coatings

- Adhesives & Sealants

- Lubricants & Coolants

- Deicing & Anti-icing Fluids

- Cleaning Chemicals

- Others

By Channel Type

- Original Equipment Manufacturer (OEM)

- Maintenance, Repair, and Overhaul (MRO)

By End Use

- Civil Aviation

- Commercial Cargo Aviation

- Military & Space Exploration

By Regions

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

Companies Covered in Aviation Chemicals Market

- Exxon Mobil Corporation

- Axalta Coating Systems Ltd.

- Calumet Specialty Products Partners, L.P.

- Akzo Nobel N.V.

- Henkel AG & Co. KGaA

- BASF SE

- Royal Dutch Shell plc

- Fuchs Petrolub SE

- Compagnie de Saint-Gobain S.A.

- Zircotec

- Master Bond Inc.

- APV Engineered Coatings

- PPG Industries Inc.

- Eastman Chemical Company

- The Sherwin-Williams Company

Frequently Asked Questions

The global Aviation Chemicals Market was valued at US$ 7.1 billion in 2025 and is projected to reach US$ 10.8 billion by 2032, growing at a CAGR of 6.2% during the forecast period.

The market is primarily driven by increasing global air traffic, expanding aircraft fleet modernization programs, stringent aviation safety regulations, and growing demand for fuel-efficient aircraft requiring advanced chemical solutions.

Lubricants & Coolants dominate the market with approximately 38% market share in 2025, driven by their critical role in engine performance and aircraft component protection across commercial and military aviation segments.

North America leads the global aviation chemicals market with 44% market share in 2025, driven by established aerospace manufacturing base, extensive commercial aviation infrastructure, and major aircraft manufacturers.