- Technology

- Aviation Cyber Security Market

Aviation Cyber Security Market Size, Share, and Growth Forecast, 2026 - 2033

Aviation Cyber Security Market by Component Type (Hardware, Software, Services), Deployment Mode (On-Premises, Cloud-Based), Solution Type (Endpoint Security, Cloud Security, Network Security, Application Security, Infrastructure Protection, Data Security, Others), Application (Airlines, Airports, Aircraft Manufacturers, MRO Providers, Air Traffic Management) and Regional Analysis for 2026 - 2033

Aviation Cyber Security Market Size and Trends Analysis

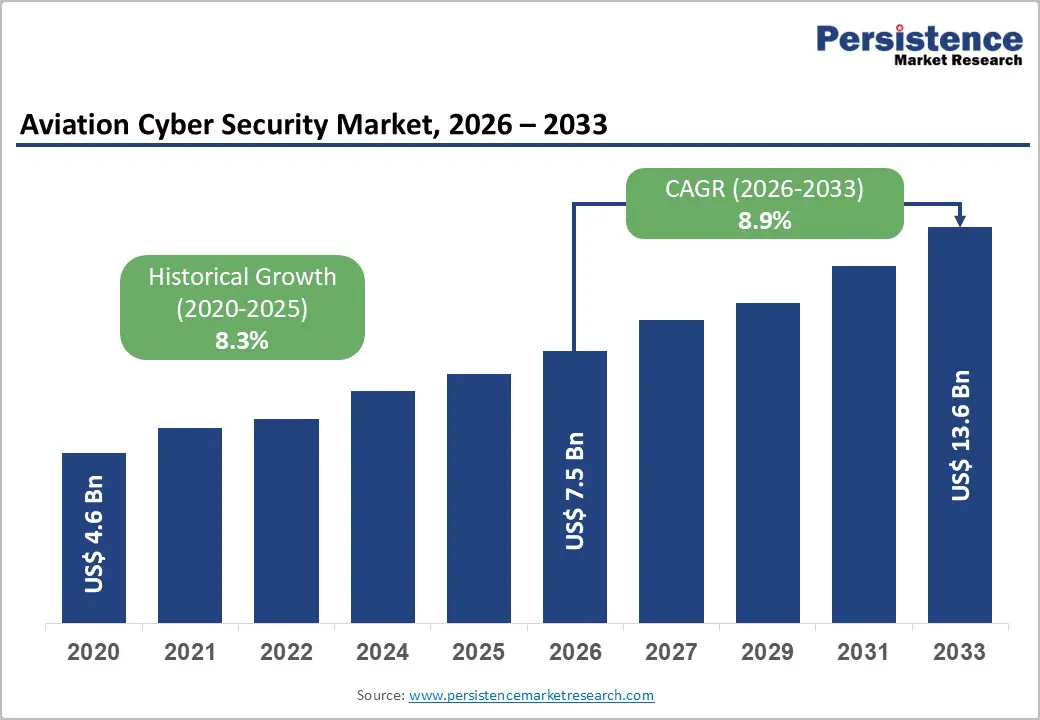

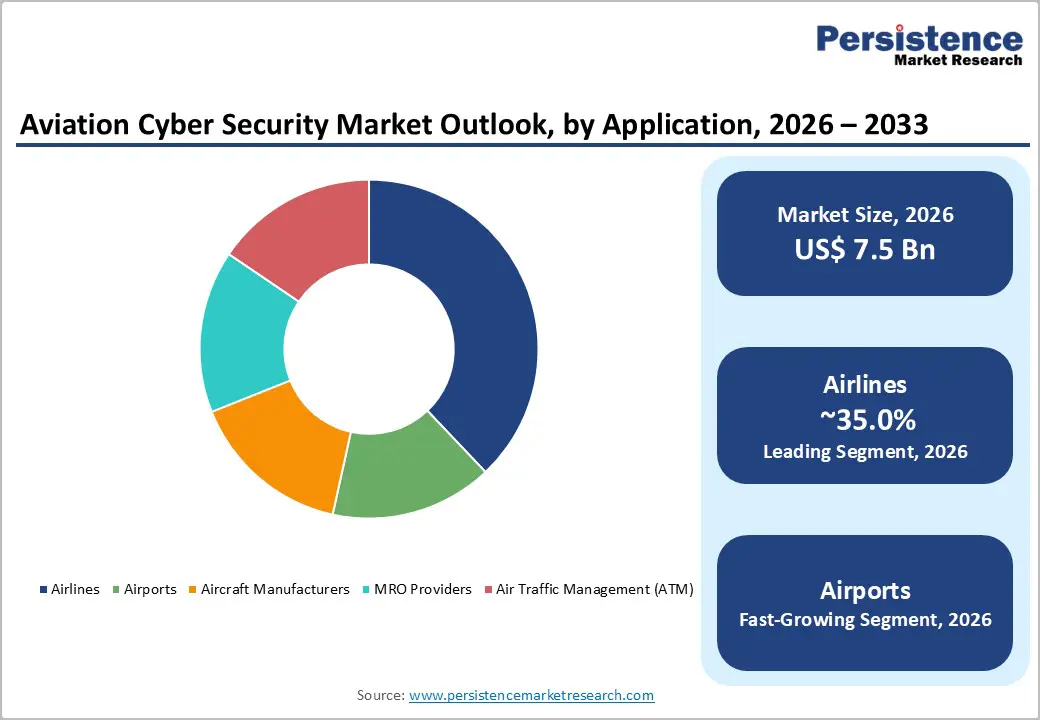

The Global Aviation Cyber Security Market size was valued at US$7.5 billion in 2026 and is projected to reach US$13.6 billion by 2033, growing at a CAGR of 8.9% between 2026 and 2033. Market expansion reflects a dramatic escalation in cyberattack frequency with a documented 600% year-on-year increase in attacks between January 2024 and April 2025 coupled with stringent regulatory frameworks from the FAA, ICAO, IATA, and EASA mandating comprehensive cybersecurity implementation across aviation infrastructure.

Digital transformation initiatives, cloud migration programs, and integration of AI and IoT technologies within aircraft and airport operations are simultaneously expanding attack surfaces while creating urgent requirements for advanced security solutions protecting mission-critical aviation systems.

Key Industry?Highlights:

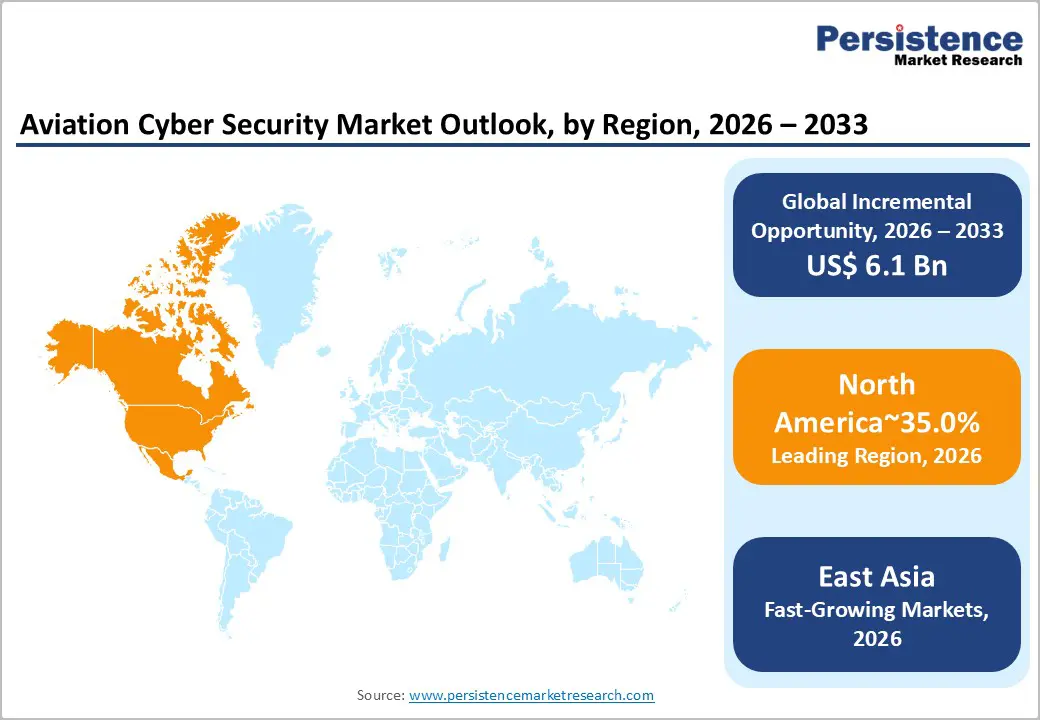

- Regional Leadership: North America leads the global Aviation Cyber Security market with 35% share, driven by stringent FAA and TSA regulations, high cyber incident exposure, and strong aerospace and defense sector investment.

- Fastest-Growing Region: East Asia holds 20% share and represents the fastest growth, supported by rapid aviation expansion, airport modernization, and rising cyber threat activity across India, China, and Southeast Asia.

- Strong European Presence: Europe accounts for 25% market share, underpinned by EASA Part-IS regulatory mandates, large aerospace manufacturing base, and coordinated EU-level cybersecurity governance.

- Leading Application Segment: Airlines dominate with 35% share, reflecting their extensive digital attack surface, high-value data exposure, and board-level prioritization of cybersecurity investment.

- Leading Component Segment: Hardware solutions lead with 40% share, driven by mission-critical requirements for secure gateways, encrypted communications, and high-reliability aviation-grade security infrastructure.

| Key Insights | Details |

|---|---|

|

Aviation Cyber Security Market Size (2026E) |

US$ 7.5 Bn |

|

Market Value Forecast (2033F) |

US$ 13.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.3% |

Market Dynamics

Growth Drivers

Escalating Cyberattack Sophistication and Threat Actor Diversification

The aviation industry has experienced an unprecedented surge in targeted cyberattacks driven by financial incentives, ideological agendas, and state-sponsored cyber operations. Thales's comprehensive threat analysis documented a staggering 600% year-on-year increase in cyberattacks between January 2024 and April 2025, with 27 major incidents perpetrated by 22 distinct ransomware groups targeting airlines, airports, navigation systems, and critical suppliers. Notably, 71% of recorded attacks involved credential theft or unauthorized access to critical systems, demonstrating attacker focus on account compromise enabling lateral movement and persistence within target networks.

The Market has emerged as the target focus as attackers recognize aviation sector concentration of high-value data including passenger information, diplomatic travel itineraries, confidential cargo shipments, and sensitive technological knowledge regarding avionics and communication systems.

Cyber adversaries are increasingly employing sophisticated techniques extending beyond traditional financial extortion. Advanced persistent threats from state-sponsored actors blend technical capabilities with geopolitical objectives, targeting industrial espionage and supply chain disruption alongside operational disruption.

The Delta Air Lines incident in July 2024, where a faulty CrowdStrike software update cascaded across 8.5 million Windows systems causing 7,000 flight cancellations and 35,500 delays affecting 1.3 million passengers, exemplified how interconnected systems amplify the impact of security incidents across the entire aviation ecosystem. The incident prompted a $500 million lawsuit against CrowdStrike and crystallized stakeholder recognition that the Aviation Cyber Security Market addresses existential operational threats rather than optional compliance requirements.

Regulatory Mandate Codification and Compliance Enforcement

Government authorities worldwide have shifted from issuing guidance recommendations to establish enforceable regulatory requirements mandating comprehensive cybersecurity implementation across aviation infrastructure. The Federal Aviation Administration announced proposed regulations in August 2024 addressing cybersecurity for aircraft and equipment, explicitly recognizing that aviation equipment increasingly connects to internal and external data networks including satellite communications and internet-enabled devices. The FAA initiative reflects systematic regulatory pressure converting voluntary cybersecurity frameworks into mandatory design and operational standards binding aircraft manufacturers, airlines, airports, and air navigation service providers.

EASA Part-IS Regulation establishes compliance deadlines of October 2025 for production organizations and February 2026 for air operators and maintenance organizations, mandating implementation of Information Security Management Systems (ISMS) and comprehensive risk assessments.

The International Civil Aviation Organization's seven-pillar Aviation Cybersecurity Strategy, operational since 2019, has matured into enforceable standards through Annex 17 recommendations, establishing baseline expectations for network security, supply chain risk management, and incident response capabilities. These regulatory frameworks create predictable, sustained demand for aviation cybersecurity solutions as organizations systematically invest in compliance infrastructure. SITA's 2024 Air Transport IT Insights report revealed that 66% of airlines and 73% of airports ranked cybersecurity among their top three strategic priorities, directly translating regulatory mandates into budget commitments for security infrastructure upgrades, cloud migration, and enhanced data protection systems across the aviation sector.

Market Restraining Factors

Legacy System Integration Complexity and Modernization Cost Burdens

The aviation industry's operational foundation rests partially on legacy systems designed decades ago that prioritized reliability and functional performance over cybersecurity considerations. These systems frequently lack modern security capabilities including encryption, multi-factor authentication, and activity logging necessary for contemporary threat detection and response.

Organizations attempting to retrofit cybersecurity controls onto legacy infrastructure face substantial technical complexity as security interventions risk disrupting systems providing essential operational functions where downtime poses unacceptable safety risks. The substantial capital investments required for comprehensive system modernization spanning IT infrastructure upgrades, cloud migration, and security tool deployment create procurement barriers particularly for smaller regional operators, budget-constrained airports, and maintenance providers lacking enterprise-scale financial resources.

Key Market Opportunities

Air Navigation Service Provider Modernization and ATM System Cybersecurity

Air Navigation Service Providers (ANSPs) managing air traffic management (ATM) systems represent a critical growth opportunity for the Aviation Cyber Security Market, as global air traffic continues expanding while ATM systems rely increasingly on digital communication links and cloud-based infrastructure.

Modern air traffic systems depend on ACARS (Aircraft Communications Addressing and Reporting System), ATN (Aeronautical Telecommunication Network), and CNS/ATM (Communications, Navigation, Surveillance/Air Traffic Management) systems that require continuous operation without interruption conditions making ATM infrastructure particularly valuable targets for state-sponsored actors seeking operational disruption. The ICAO and aviation authorities worldwide are systematically enhancing ATM security through network segmentation, secure gateway architecture, and behavioral analytics tuned to aviation operational baselines.

The Aviation Cyber Security Market expansion in ATM reflects dual imperatives: capacity expansion to accommodate projected traffic growth and security enhancement to protect against sophisticated adversaries. Global air traffic is projected to double over the next 20 years, with Asia-Pacific leading incremental growth, requiring corresponding expansion of ATM system capacity while simultaneously implementing modern security architectures.

ANSPs in Europe, North America, and Asia-Pacific are systematically modernizing ATM infrastructure, creating sustained procurement opportunities for security solutions protecting air traffic control facilities, communication networks, and data repositories from compromise that could disrupt flight operations across entire regions. The critical infrastructure designation of ATM systems means government funding support for modernization initiatives complements commercial procurement budgets.

Airport Transformation and Smart Terminal Operations Security Implementation

Airports represent the fastest-growing application segment for aviation cybersecurity solutions, driven by systematic transformation from conventional facilities toward digitally integrated "smart airports" incorporating advanced technologies including biometric passenger processing, automated baggage systems, real-time operations planning, IoT sensor networks monitoring facility conditions, and cloud-connected systems enabling remote facility management.

This digital transformation creates unprecedented operational efficiency but simultaneously introduces substantial cybersecurity risks as operational technology systems controlling critical airport functions become networked and potentially remotely accessible. Malfunction or compromise of baggage handling systems, gate assignment systems, or power management infrastructure could rapidly cascade into massive passenger service disruptions and flight delays.

The Market opportunities in airport modernization are substantial as facilities systematically deploy integrated security solutions protecting smart baggage handling systems, visitor management, access control, surveillance integration, and operational data repositories. TXOne's November 2025 focus on airport operational technology security highlighted critical requirements for protecting SCADA and building automation systems, legacy control systems requiring virtual patching, and zone-based security architectures enabling IT/OT segregation

Airports worldwide are allocating material capital budgets to cybersecurity infrastructure modernization aligned with broader facility digital transformation initiatives, creating sustained demand for specialized aviation-grade security solutions addressing airport-specific operational requirements and regulatory compliance expectations.

Category-wise Analysis

Component Type Insights

Hardware components maintained 40% of the Aviation Cyber Security Market share in 2026, encompassing security appliances, network devices, encrypted communication systems, endpoint protection devices, and specialized aviation-grade infrastructure protecting critical systems.

Hardware solutions include firewalls optimized for aviation network architectures, secure gateways protecting ACARS and satellite communication links, intrusion detection systems monitoring aviation-specific protocols, and hardware security modules providing cryptographic key management for sensitive data protection. Leading vendors including Thales, Honeywell, Collins Aerospace, and specialized security providers integrate hardware components with advanced analytics software creating comprehensive security platforms optimized for aviation operational characteristics.

The hardware segment's substantial market share reflects the mission-critical nature of aviation operations where hardware redundancy, fail-safe design, and proven reliability are non-negotiable requirements. Aviation organizations systematically invest in high-reliability hardware solutions capable of operating continuously without interruption, tolerating no single point of failure that could compromise flight safety or operational continuity.

Services represent the fastest-growing component category within the Aviation Cyber Security Market, driven by escalating operational complexity and widespread organizational recognition that technology deployment alone is insufficient without specialized expertise in implementation, configuration, optimization, and ongoing management.

Application Insights

Airlines maintained approximately 35% of the Aviation Cyber Security Market share in 2026, reflecting their role as primary target organizations for cyberattacks and substantial security investment commitments.

Airlines operate interconnected systems spanning flight operations, crew management, revenue optimization, passenger services, maintenance planning, supply chain coordination, and financial systems creating vast attack surfaces vulnerable to compromise threatening both operational integrity and passenger safety. Cyberattacks targeting airlines can disrupt flight planning, corrupt passenger reservations, compromise crew scheduling, or corrupt aircraft maintenance records with cascading operational consequences affecting multiple flights and disrupting broad geographic regions.

The Airlines segment benefits from SITA's 2024 finding that 66% of airlines rank cybersecurity among their top three strategic priorities, directly translating executive commitment into substantial capital investments across network security, endpoint protection, cloud security, identity management, and managed services.

Major international carriers including Delta, Qantas, and others have experienced high-profile cyber incidents crystallizing board-level recognition of cybersecurity as strategic operational risk requiring sustained investment. Airlines systematically deploying zero-trust security architectures, AI-driven threat detection, behavioral analytics monitoring crew and operations systems, and comprehensive incident response capabilities protecting mission-critical operational systems from compromise.

Airports represent the fastest-growing application segment for aviation cybersecurity solutions, driven by systematic digital transformation projects and escalating cyberattack activity targeting airport infrastructure.

Regional Insights and Trends

North America Market Trend

North America maintained approximately 35% of the Global Aviation Cyber Security Market share, establishing the region as the dominant market driven by regulatory intensity, technology leadership, and substantial defense/aerospace sector participation. The United States alone accounts for approximately 90 to 92 percent of North American aviation cybersecurity spending, benefiting from the FAA's regulatory authority over civil aviation, the TSA's aviation security mandates, and the DHS/CISA coordination on critical infrastructure protection. The U.S. aerospace and defense sector generated over $995 billion in total business activity during 2024, with military and intelligence agencies providing substantial investment in aviation cybersecurity supporting both civilian aviation safety and defense operations.

North American regulatory frameworks have systematically advanced toward mandatory cybersecurity standards. The FAA's August 2024 proposed regulations addressing aircraft cybersecurity represent formal acknowledgment that aviation equipment cybersecurity must be integrated into airworthiness certification. The TSA's requirements for airport and airline vulnerability assessments create systematic demand for comprehensive risk assessment services and security infrastructure modernization.

Major U.S. carriers including Delta, United, American, and Southwest have undertaken substantial security infrastructure investments following high-profile incidents, establishing technology adoption patterns that regional and low-cost carriers are progressively emulating. The region's concentration of aerospace prime contractors, security technology vendors, and aviation systems integrators provides robust competition accelerating innovation and expanding availability.

East Asia Market Trend

East Asia accounted for approximately 20% of the Global Aviation Cyber Security Market share while demonstrating the fastest regional growth trajectory, driven by rapid commercial aviation expansion, defense modernization priorities, and increasing cyber threat activity. The Indian aviation sector has emerged as the region's fastest-growing segment, with passenger traffic reaching 96.54 million passengers during April-July 2025 and government initiatives targeting the sector's expansion through airport development (Navi Mumbai, Noida), regional connectivity expansion under the UDAN scheme, and airline fleet modernization by carriers including IndiGo, Air India, and Air India Express.

China's commercial aviation sector continues expansion with substantial domestic and international airline networks requiring security infrastructure protection. Southeast Asian nations including Thailand, Vietnam, and Malaysia are investing in airport modernization and new aviation hubs supporting tourism and regional trade connectivity.

The Asia-Pacific region faces distinctive cybersecurity challenges from sophisticated cyber threat actors based within the region and foreign state-sponsored groups targeting strategic aviation assets. Aviation authorities across Asia-Pacific are progressively harmonizing cybersecurity standards with international frameworks while establishing regional capability centers exemplified by the UAE Cyber Security Council's November 2025 partnership with Thales establishing a Cyber Centre of Excellence focusing on aviation and critical infrastructure security.

Europe Market Trend

Europe represented approximately 25% of the Global Aviation Cyber Security Market share, characterized by stringent regulatory frameworks, substantial aerospace manufacturing, and coordinated supranational governance. The European aerospace and defense sector generated €325.7 billion in turnover during 2024 with €23.4 billion in R&D investment, and European aviation directly employed 2.9 million people while supporting 15 million jobs across the broader economy, contributing $1.2 trillion to GDP.

EASA's Part-IS Regulation, with compliance deadlines in October 2025 and February 2026, establishes mandatory cybersecurity governance across production organizations, air operators, and maintenance providers, creating systematic demand for security infrastructure modernization and governance transformation.

European airports and airlines face particular cybersecurity pressure as targets for state-sponsored cyber operations given the region's geopolitical significance and the strategic value of compromised European aviation systems. The European Commission has supported aviation modernization through substantial R&D investment and regulatory harmonization efforts, with emphasis on cybersecurity as integral to next-generation air traffic management systems.

The region's aviation cybersecurity market benefits from strong indigenous security technology vendors including Thales (France), advanced expertise across aerospace-focused organizations, and government support for critical infrastructure protection. EASA's regulatory leadership is driving harmonized European cybersecurity standards that are progressively influencing global aviation security frameworks.

Competitive Landscape

The Global Aviation Cybersecurity Market is moderately consolidated, with a few leading players dominating the sector due to their technological expertise and strategic presence. Key companies such as Thales Group, Raytheon Technologies Corporation, BAE Systems, Airbus SE, Lockheed Martin Corporation, and Northrop Grumman Corporation provide comprehensive solutions including threat detection, secure communications, and risk management for airlines, airports, and aerospace systems. These firms leverage strong R&D capabilities and government partnerships to maintain their competitive edge.

Mid-tier players contribute niche solutions, ensuring the market remains innovative and dynamic. High entry barriers and stringent regulatory requirements limit new entrants, making the market competitive yet controlled by these top players.

Key Industry Developments

- 13 June 2025, Thales: The aviation sector experienced a 600% year-on-year increase in cyberattacks, with 27 major incidents by 22 ransomware groups between January 2024 and April 2025. Approximately 71% of attacks involved credential theft or unauthorized access to critical systems, affecting airlines, airports, navigation systems, and suppliers. This surge in cyber threats has highlighted the strategic vulnerabilities of the sector, driving the global aviation cybersecurity market to an estimated USD 5.32 billion in 2025 and emphasizing the urgent need for advanced security measures to protect flight operations, sensitive data, and supply chains.

- 26 November 2025, TXOne: The aviation sector is facing critical operational technology (OT) challenges due to legacy, interconnected systems that were never designed for modern cyber threats. TXOne introduced solutions such as Portable Inspector for agentless malware scanning, EdgeIPS/EdgeFire for virtual patching of unpatchable legacy systems, and Stellar for access control and application lockdown. These innovations help airports and airlines protect OT environments, enforce zone-based security, and comply with international regulations from ICAO, IATA, EASA, and CIRCIA, addressing vulnerabilities that can disrupt flight operations, passenger processing, and national-level aviation security.

Companies Covered in Aviation Cyber Security Market

- Thales Group

- Raytheon Technologies Corporation

- BAE Systems

- Airbus SE

- IBM Corporation

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Honeywell International Inc.

- Booz Allen Hamilton Inc.

- Cisco Systems, Inc.

Frequently Asked Questions

The global Aviation Cyber Security Market is projected to be valued at US$ 7.5 Bn in 2026.

Airlines Segment is expected to account for approximately 35% of the global Aviation Cyber Security Market by Application in 2026.

The market is expected to witness a CAGR of 20.3% from 2026 to 2033.

The Aviation Cyber Security Market growth is driven by rapidly escalating and increasingly sophisticated cyberattacks on aviation systems, combined with stringent regulatory mandates enforcing mandatory cybersecurity compliance across airlines, airports, aircraft manufacturers, and air navigation infrastructure.

Key opportunities in the Aviation Cyber Security Market stem from air navigation service provider (ANSP) and ATM system modernization to secure critical air traffic infrastructure, along with rapid airport digital transformation and smart terminal deployments requiring advanced IT/OT and operational technology cybersecurity solutions.

The key players in the Aviation Cyber Security Market include Thales Group, Raytheon Technologies Corporation, BAE Systems, Airbus SE, IBM Corporation, and Lockheed Martin Corporation.