- Sensors & Controls

- Area Sensor Market

Area Sensor Market Size, Share, and Growth Forecast 2025 - 2032

Area Sensor Market by Product Type (General Purpose Area Sensors, Cross-beam Area Sensors), Sensing Range (Less than 1 Meter, 1 Meter - 3 Meters, 3 Meters - 5 Meters, More than 5 Meters), Application (Object Detection, Picking Systems, Positioning and Examination, Personnel Safety, Equipment Protection, Others), Industry, Regional Analysis, 2025 - 2032

Area Sensor Market Size and Trend Analysis

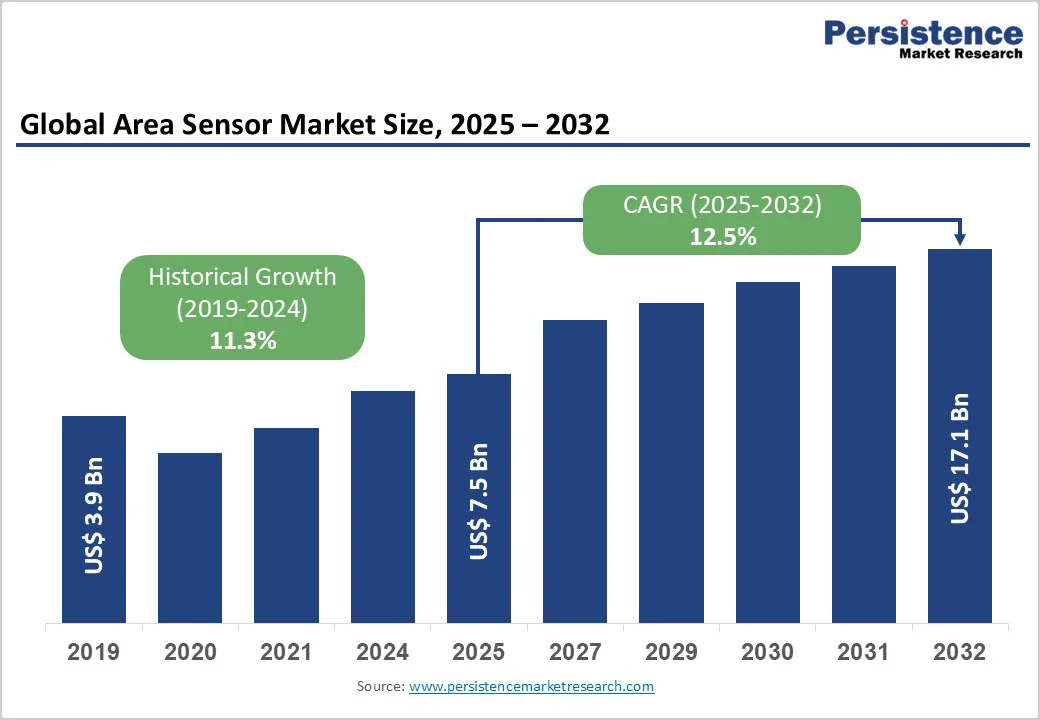

The global area sensor market is projected to be valued at US$7.5 billion in 2025 and reach US$17.1 billion by 2032, growing at a CAGR of 12.5% between 2025 and 2032.

The market is experiencing robust growth driven by rising adoption of industrial automation, stringent workplace safety regulations, and the proliferation of smart manufacturing initiatives across developed and emerging economies.

Rapid digitalization of factories, integration of Industry 4.0 technologies, and growing emphasis on personnel protection systems are creating unprecedented opportunities for area sensor manufacturers to deliver advanced sensing solutions that enhance operational efficiency while ensuring worker safety.

Key Market Highlights:

- Leading Region: North America leads with a 32% share in 2025, supported by high automation adoption, strict OSHA safety mandates, and an innovation ecosystem advancing AI-enabled sensing and Industrial IoT technologies.

- Fastest Growing Region: Asia Pacific is the fastest-growing market at a 14.7% CAGR from 2025 - 2032, driven by rapid manufacturing automation, strong Industry 4.0 investments, and expanding e-commerce logistics requiring advanced detection and positioning sensors.

- Leading Segment: General-purpose aaea ensors hold a dominant 63% share in 2025 due to their versatile applications, cost-effectiveness, and broad availability from major global automation manufacturers.

- Fastest Growing Segment: Cross-beam Area Sensors grow fastest at a 14.2% CAGR from 2025 - 2032, enabled by superior accuracy from 3-point cross-beam designs that reliably detect small and irregular objects in demanding manufacturing conditions.

- Key Opportunity: E-commerce logistics and warehouse automation offer major opportunities driving sensor demand for AGV/AMR navigation, precise picking, and high-speed sorting.

| Key Insights | Details |

|---|---|

| Area Sensor Market Size (2025E) | US$7.5 Bn |

| Market Value Forecast (2032F) | US$17.1 Bn |

| Projected Growth CAGR (2025 - 2032) | 12.5% |

| Historical Market Growth (2019 - 2024) | 11.3% |

Market Dynamics

Drivers - Accelerating Industrial Automation and Smart Manufacturing Adoption

The global shift toward automated production systems is fundamentally transforming manufacturing landscapes, with area sensors playing a pivotal role in enabling intelligent factory operations. According to projections for the industrial automation market, the Asia Pacific region is expected to hold 39% of the market share.

Government initiatives such as China’s Made in China 2025 and India’s Make in India programs are driving large-scale adoption of Industrial IoT, AI, and robotics across manufacturing sectors.

Similarly, smart manufacturing is projected to grow at a CAGR of 14.2% through 2032, with manufacturers deploying area sensors for precise object detection, positioning accuracy, and process monitoring.

SICK AG, a global leader in sensor technology, reported sales of EUR 2.307 billion in 2023, with factory automation representing the strongest growth segment at 6.9% year-over-year. The company’s investment of 11.7% of sales in research and development underscores the industry’s commitment to advancing sensor intelligence for automated applications, including robotic assembly, material handling, and quality inspection systems.

Stringent Workplace Safety Regulations and Personnel Protection Requirements

Escalating regulatory emphasis on occupational safety is compelling industries to implement advanced safety systems, with area sensors serving as critical components in personnel protection frameworks.

The European Union Machinery Regulation 2023/1230, effective from January 2027, mandates enhanced safety standards for industrial equipment, explicitly incorporating requirements for autonomous mobile machinery and connected equipment safety functions. Manufacturing facilities worldwide are adopting Type 4/SIL 3/PL e-compliant safety solutions to meet the standards outlined in ISO 13849-1 and the Machinery Directive 2006/42/EC.

In automotive production lines, light sensors and area detection systems have become indispensable for monitoring hazardous zones around spot welding robots, painting systems, and assembly stations where human-machine collaboration occurs.

Taiwan-based Delta Electronics showcased advanced automation solutions at SEMICON Taiwan 2024 and Automation Taipei 2024, highlighting how integrated sensor systems enable safe, efficient operations in semiconductor manufacturing and precision engineering applications where worker safety and process reliability are paramount.

Restraints - High Initial Investment and Integration Complexity

The deployment of sophisticated area sensor systems requires substantial capital expenditure and technical expertise, creating barriers to adoption, particularly for small and medium-sized enterprises. Industrial-grade area sensors can range from thousands to tens of thousands of dollars per installation, with costs escalating further when integrated into comprehensive safety and automation architectures.

The industrial robotics market analysis indicates that high initial investment requirements present significant challenges for SMEs in developing economies, including India and Southeast Asian nations, where capital expenditure constraints limit technology adoption.

Beyond hardware costs, successful implementation demands specialized training for operators and maintenance personnel, integration with existing Programmable Logic Controllers (PLCs), Human-Machine Interfaces (HMIs), and Supervisory Control and Data Acquisition (SCADA) systems, as well as potential facility modifications to accommodate new sensing infrastructure.

These financial and operational complexities can extend payback periods and delay return on investment, particularly in price-sensitive markets where manufacturers must balance automation benefits against immediate cost pressures.

Technical Limitations in Challenging Environmental Conditions

Area sensors face performance degradation in harsh industrial environments characterized by extreme temperatures, dust contamination, electromagnetic interference, and chemical exposure. Applications in steel production, foundries, chemical processing, and outdoor logistics operations present unique challenges where conventional photoelectric sensing principles may be compromised.

While manufacturers have developed ruggedized solutions with protection ratings up to IP67, IP68, and IP69K, certain environmental factors, including heavy steam, fog, airborne particulates, and direct exposure to cleaning chemicals, can affect optical transmission and reception reliability.

The electronic sensors market highlights that supply chain disruptions affecting component availability can delay sensor production and increase costs, impacting market growth momentum.

Market Opportunities

Expansion in E-Commerce Logistics and Warehouse Automation

The exponential growth of e-commerce and the demand for rapid order fulfillment are driving unprecedented investment in automated warehouse systems, creating substantial opportunities for area sensor integration in picking, sorting, and material-handling applications.

Global logistics automation is experiencing a transformative change with Automated Guided Vehicles (AGVs) and Autonomous Mobile Robots (AMRs) becoming essential infrastructure components in modern distribution centers.

AMRs leverage multi-sensor fusion techniques that combine cameras, LiDAR, and photoelectric sensors to navigate dynamic warehouse environments, with area sensors providing critical object-detection capabilities for collision avoidance, pallet positioning, and parcel sorting operations.

Leading e-commerce fulfillment providers are implementing pick-to-light systems, voice-directed picking, and robotic picking stations that rely on area sensors for real-time item detection and quality control, presenting manufacturers with opportunities to develop application-specific solutions optimized for high-speed, high-accuracy logistics environments.

Integration with Industry 4.0 and IoT Ecosystems

The convergence of area sensors with Industrial Internet of Things (IIoT) platforms and Industry 4.0 architectures is unlocking new value propositions, including predictive maintenance, real-time process optimization, and data-driven decision making.

Modern area sensors increasingly feature IO-Link connectivity, Ethernet-based protocols, and cloud integration capabilities that enable seamless data exchange with enterprise manufacturing execution systems and analytics platforms.

Manufacturers including Delta Electronics are showcasing digital twin platforms and AI-based automation solutions that integrate sensor data for virtual equipment testing, optimal recipe parameter generation, and production lifecycle management.

Pepperl+Fuchs offers wireless WILSEN IoT sensors with LoRaWAN connectivity for remote monitoring applications. At the same time, Panasonic Industry provides IO-Link-enabled sensors that support predictive maintenance and condition monitoring, allowing manufacturers to minimize downtime, optimize asset utilization, and improve operational efficiency through sensor-driven insights and automated feedback loops.

Category-wise Analysis

Product Type Insights

The General Purpose Area Sensors segment is set to dominate the market with around 63% share in 2025, supported by its versatility and suitability for a broad spectrum of industrial automation tasks. These sensors provide dependable multi-beam detection for presence verification, object counting, and positioning in sectors such as automotive assembly, packaging, material handling, and pharmaceuticals.

Their wide availability in multiple sensing distances and adjustable detection fields enables seamless integration into both compact workcells and large conveyor systems. With competitive pricing and robust performance across varying environmental conditions, general-purpose variants remain the preferred option for manufacturers seeking cost-efficient, adaptable, and easy-to-deploy sensing solutions for foundational automation requirements.

Sensing Range Insights

The 1-3 meters sensing range segment is projected to hold the largest share at roughly 41% in 2025, reflecting its alignment with the spatial requirements of typical production cells, assembly machines, and packaging equipment. This range supports essential tasks such as robot perimeter monitoring, machine safeguarding, and object detection in close-proximity industrial setups.

Sensors designed for this distance offer compact footprints, fast response times, and high environmental resilience, making them suitable for high-speed operations and frequent washdowns. Their ability to deliver precise detection within limited workspace geometries ensures dependable performance in automated manufacturing environments, reinforcing their role as a standard choice for mid-range industrial sensing applications.

Applications Insights

Object Detection is expected to remain the leading application, representing about 35% of market share in 2025 due to its central role in nearly all automated manufacturing and logistics workflows. Area sensors are essential for verifying part presence, identifying materials, and detecting items of varying shapes, colors, and reflectivity as they move along production lines.

Technologies such as ToF measurement, laser-based detection, and advanced CMOS sensing enhance accuracy and stability, even in demanding environments involving heat, vibration, or high-speed motion. Their use in applications like assembly verification, counting, and position control supports Just-In-Time manufacturing models and zero-defect strategies, making object detection an indispensable component of modern automation systems.

Industry Insights

The automotive industry is poised to capture roughly 29% of market share in 2025, driven by its extensive reliance on automation, stringent quality requirements, and complex multistage manufacturing processes. Area sensors are widely utilized for precision component positioning, surface inspection, conveyor monitoring, and real-time verification of assembled parts across powertrain, body-in-white, and final assembly operations.

Their fast response and high reliability directly influence production throughput, accuracy, and safety performance in facilities where human-robot collaboration and heavy machinery coexist. As automotive plants advance toward fully digitalized and autonomous production systems, area sensors continue to serve as critical enablers of process stability, defect prevention, and compliance with rigorous global manufacturing standards.

Regional Insights

North America Area Sensor Market Trends

North America is positioned to account for roughly one-third of global area sensor demand in 2025, supported by its highly advanced manufacturing base, strong automation culture, and stringent occupational safety regulations governing industrial environments.

The United States drives most regional uptake as automotive, pharmaceutical, electronics, and food processing industries deploy area sensors for quality assurance, machine safeguarding, and real-time production monitoring.

Momentum from the rapidly expanding North America Warehouse Automation Market further strengthens sensor adoption, as fulfillment centers and logistics hubs increasingly rely on AGVs, AMRs, and high-speed sorting systems requiring precise detection capabilities. The region’s smart manufacturing sector is also growing rapidly, with Industrial IoT integration improving OEE, energy efficiency, and process stability across large-scale facilities.

Strict regulatory frameworks, including OSHA safety mandates and compliance requirements tied to pharmaceutical GMP and food safety protocols, reinforce demand for certified and high-reliability sensing systems.

North America’s innovation ecosystem-driven by collaboration among automation suppliers, system integrators, and research institutions-continues to accelerate advancements in AI-enabled sensing, machine vision fusion, predictive analytics, and wireless sensor networks, positioning the region as a proving ground for next-generation automation technologies.

Europe Area Sensor Market Trends

Europe is expected to capture about 28% of global area sensor revenue in 2025, underpinned by mature industrial automation deployment, robust safety legislation, and strong commitment to sustainable manufacturing across major economies. Germany remains the region’s core growth engine, leveraging extensive automation in automotive production, mechanical engineering, and process industries aligned with long-standing Industry 4.0 digitalization initiatives.

The European Union Machinery Regulation 2023/1230 strengthens safety obligations by mandating conformity assessment, CE marking, and integration of advanced protective technologies, encouraging broader use of area sensors in machinery and collaborative robot systems.

Adoption is also strong in the United Kingdom, France, and Spain, where pharmaceuticals, food processing, and packaging sectors rely on high-precision optoelectronic sensing to meet hygiene, traceability, and quality assurance standards.

The market shows clear preference for high-specification sensors with diagnostic features, IO-Link connectivity, and compatibility with MES and BAS platforms, supporting Europe’s broader goals around energy efficiency, equipment longevity, and circular economy practices.

Asia Pacific Area Sensor Market Trends

Asia Pacific is set to emerge as the fastest-growing region with a projected CAGR of 14.7% from 2025 to 2032, driven by large-scale industrial expansion, aggressive automation rollout, and substantial government investment in manufacturing modernization.

China dominates regional activity, supported by policies such as Made in China 2025 and its global leadership in industrial robot installations, fostering strong demand for advanced sensing in electronics, automotive, and semiconductor production.

Japan continues to lead in precision engineering and robotics innovation, developing highly sensitive and miniaturized area sensors suitable for complex, high-accuracy applications. India is accelerating automation adoption through Make in India and PLI initiatives that attract global manufacturers to modern, sensor-rich facilities.

Taiwan’s semiconductor ecosystem further boosts demand as factories integrate high-speed sensing into digital twin environments and ultra-precise electronic assembly. Expanding e-commerce logistics across China, India, and ASEAN economies additionally fuels sensor deployment in automated warehouses, sorting hubs, and last-mile fulfillment centers.

Competitive Landscape

The global area sensor market is moderately consolidated, with a few large automation and sensing technology providers dominating through broad product portfolios, strong distribution networks, and sustained investment in innovation.

These players reinforce their positions by expanding application coverage, enhancing device intelligence, and integrating advanced communication capabilities that support seamless deployment across diverse industrial environments.

Substantial R&D spending, increasing patent activity, and continuous product upgrades strengthen their technological edge while enabling differentiation through performance, reliability, and compatibility with modern automation architectures.

Alongside these multinationals, a growing base of regional manufacturers competes through localized engineering support, faster customization cycles, and cost-efficient offerings tailored to small and medium enterprises and niche applications.

The market is steadily shifting toward sensor systems integrated with edge processing, wireless connectivity, and cloud analytics, encouraging strategic partnerships across the Industrial IoT ecosystem to deliver data-driven services such as predictive maintenance and operational optimization that deepen customer engagement and long-term value.

Key Market Developments:

- August 2024: Delta Electronics introduced DIATwin digital-twin platform cutting development time 20%, smart warehouse solutions boosting logistics efficiency 30%, and high-speed die pick-and-place technology improving semiconductor production yield 20% at Automation Taipei.

- June 2024: SICK AG launched the Inspector83x AI vision sensor featuring quad-core processing, integrated illumination, and on-device AI inference, enabling high-speed, sub-millimeter defect detection across electronics, pharmaceutical, and precision engineering applications.

- September 2024: Pepperl+Fuchs released new LoRaWAN-enabled WILSEN sensors for remote valve and fill-level monitoring, and advanced development of wide-field retroreflective sensors for detecting small, irregular objects in logistics and packaging automation.

Companies Covered in Area Sensor Market

- SICK AG

- OMRON Corporation

- Panasonic Corporation

- Autonics Corporation

- Datalogic S.p.A.

- Keyence Corporation

- Delta Electronics, Inc.

- Pepperl+Fuchs

- XECRO GmbH

- Riko Opto-electronics Co., Ltd.

- Orbital Mekatronik Systems Pvt. Ltd.

- Hamamatsu Photonics

- MISUMI Corporation

- IMO Precision Controls

- VergeSense

- Banner Engineering

- Balluff

- IFM Electronic

- Micro-Epsilon

- TE Connectivity

Frequently Asked Questions

The global area sensor market is expected to reach US$ 17.1 billion by 2032, up from US$ 7.5 billion in 2025 at a 12.5% CAGR.

Market growth is driven by rising industrial automation, stricter global safety regulations, and rapid Industry 4.0 adoption.

General Purpose Area Sensors lead the market with 63% share in 2025, attributed to their versatility and cost-effectiveness.

North America leads with a 32% share due to advanced automation adoption and stringent safety standards.

Major opportunities arise from warehouse automation, AMR/AGV navigation, predictive maintenance, and expanding semiconductor and pharmaceutical automation.

Key players include SICK AG, OMRON Corporation, Keyence Corporation, Panasonic Corporation, Autonics Corporation, etc. offering broad portfolios and strong R&D investments.