- Smart Packaging

- Wrap Around Label Films Market

Wrap Around Label Films Market Size, Share, and Growth Forecast, 2026 - 2033

Wrap Around Label Films Market by Material Type (Polyethylene (PE), Polypropylene (PP), Others), Product (Shrink, Roll-fed, Others), End-use Industry, and Regional Analysis for 2026 - 2033

Wrap Around Label Films Market Size and Trends Analysis

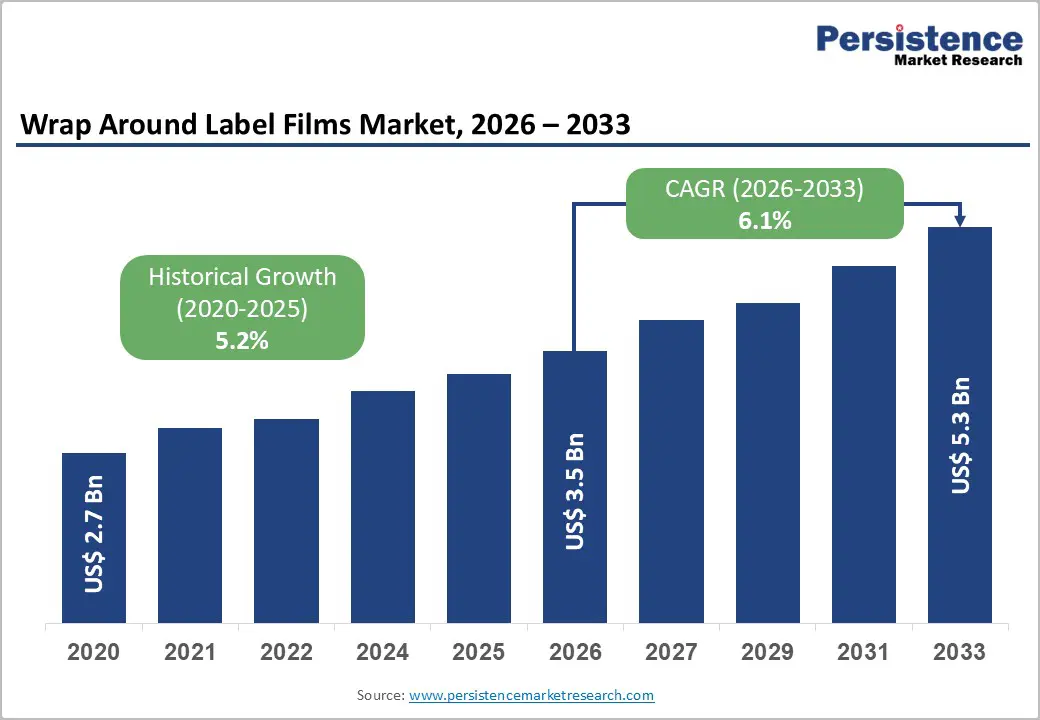

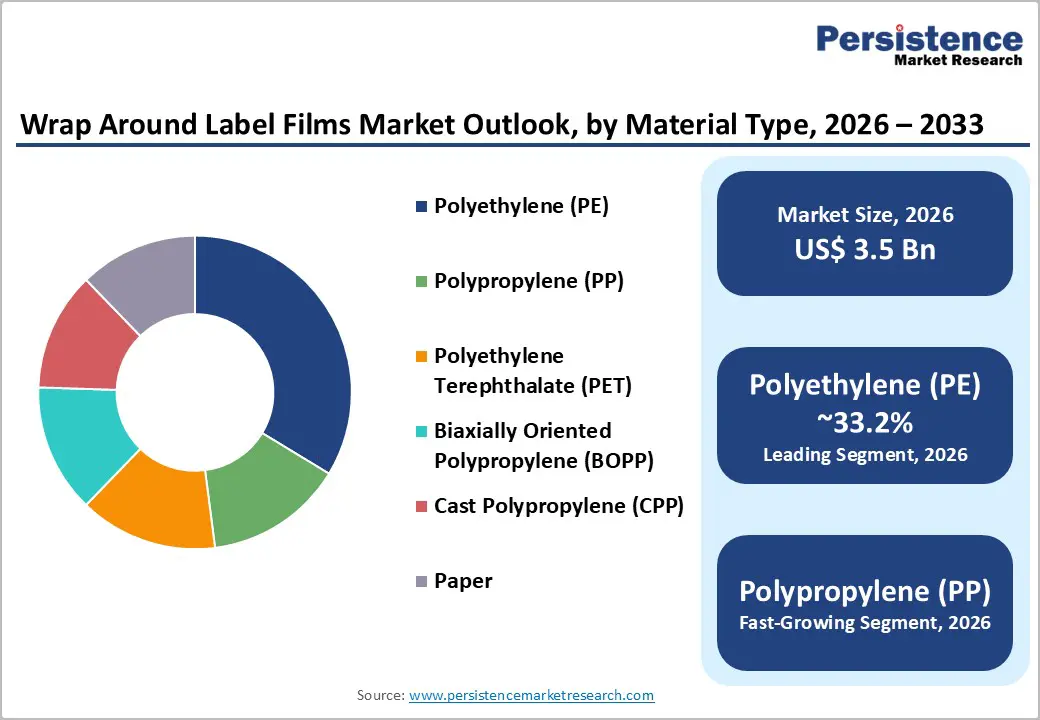

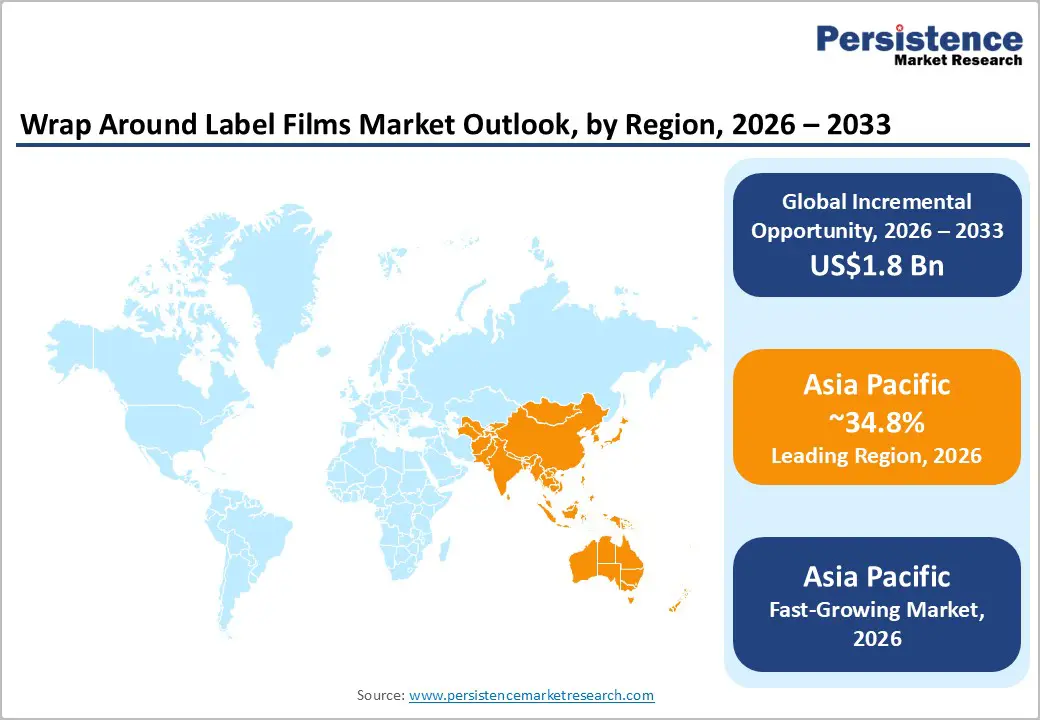

The global wrap around label films market size is likely to be valued at US$3.5 billion in 2026 and is expected to reach US$5.3 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033, driven by structural growth in packaged food and beverage consumption, rising demand for high-impact 360° product branding, and accelerating automation in labeling operations. Material innovation in polyolefin films and increasing regulatory pressure to improve recyclability and post-consumer recycled (PCR) content are reshaping procurement strategies.

Key Industry Highlights:

- Leading Region: Asia Pacific is projected to hold approximately 34.8% market share, driven by expanding beverage production in China and India, rising packaged goods consumption, and large-scale investments in extrusion and high-speed labeling infrastructure.

- Fastest-growing Region: Asia Pacific is expected to register the highest CAGR through 2032, supported by rapid urbanization, automation in beverage bottling, and increasing adoption of recyclable mono-material film structures aligned with global sustainability standards.

- Investment Plans: Strong capital deployment in North America and Europe toward recyclable mono-material shrink and roll-fed films, hybrid flexographic–digital printing lines, downgauged BOPP capacity expansion, and compliance-driven packaging redesign to meet EU and U.S. regulatory requirements.

- Dominant Material Type: Polyethylene (PE) is anticipated to hold approximately 33.2% market share, supported by cost efficiency, recyclability compatibility, and widespread use in high-volume beverage and household care applications.

- Leading Product Type: Shrink labels are estimated to account for nearly 41.3% share, favored for full-body decoration, tamper evidence, and strong adoption across bottled water, carbonated beverages, and alcoholic drink packaging.

| Key Insights | Details |

|---|---|

|

Wrap Around Label Films Market Size (2026E) |

US$3.5 Bn |

|

Market Value Forecast (2033F) |

US$5.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Beverage and Packaged Food Production Driving Volume Demand

Global beverage and packaged food output continues to expand, directly increasing consumption of wrap around label films. Beverage bottling lines operating at speeds exceeding 40,000 bottles per hour require consistent, high-performance labeling materials that minimize downtime and waste. Wrap around formats enable full-body graphics, tamper evidence, and improved shelf visibility, which are critical in competitive retail environments. Premium bottled beverages, functional drinks, and ready-to-drink products further stimulate labeling demand. For suppliers, this volume-driven growth necessitates investments in high-output extrusion, coating, and printing capabilities to meet escalating order sizes and maintain supply reliability.

Material Innovation and Shift toward Polyolefin-Based Films

Advancements in polyethylene (PE) and polypropylene (PP) film chemistries are improving printability, barrier performance, and downgauging capabilities. These improvements reduce per-unit labeling costs while maintaining aesthetic quality and mechanical strength. Polyethylene leads the market with approximately 33.2% share, supported by its cost efficiency and compatibility with mono-material recycling streams. Meanwhile, enhanced surface treatments and co-extrusion technologies enable higher-resolution graphics and improved ink adhesion. Converters that integrate advanced polyolefin grades achieve faster throughput, lower waste rates, and improved production economics, reinforcing demand across food, beverage, and home-care applications.

Sustainability Regulations and Corporate ESG Commitments

Packaging regulations in major economies are tightening recyclability and recycled-content requirements. Governments are implementing extended producer responsibility (EPR) frameworks and setting minimum recycled content targets that directly influence material selection. Brand owners increasingly adopt mono-material label solutions to simplify sorting and mechanical recycling processes. As sustainability disclosures become mandatory in several jurisdictions, procurement teams prioritize films that meet recyclability certifications and PCR integration standards. This regulatory and ESG alignment drives demand for PE- and PP-based wrap films that are compatible with established recycling infrastructures.

Barrier Analysis - Polymer Feedstock Price Volatility

Wrap around label films depend heavily on polyolefin resins derived from crude oil and natural gas. Volatility in global energy markets creates unpredictable cost structures for film manufacturers. Margin compression of 4–10 percentage points can occur during periods of rapid resin price escalation. While converters may pass through some cost increases, long-term contracts and competitive bidding limit flexibility. Managing procurement risk through hedging, diversified sourcing, and recycled-content blending is essential to maintain profitability.

Inconsistent Recycling Infrastructure

Recyclability claims depend on effective collection, sorting, and reprocessing systems. In regions where material recovery facilities are underdeveloped, recyclable films may still fail to achieve meaningful recovery rates. This fragmentation increases compliance costs for brand owners and slows the adoption of PCR-integrated films. Infrastructure gaps create uncertainty around regulatory enforcement timelines and investment returns for sustainable film development.

Opportunity Analysis - Expansion in Asia Pacific and Emerging Economies

Asia Pacific represents the leading regional market, accounting for approximately 34.8% of global share, and is also the fastest-growing region. Rising disposable incomes, urbanization, and growth in modern retail channels drive increased consumption of packaged goods. Domestic beverage production and contract manufacturing growth further stimulate demand for wrap labeling solutions. Suppliers that localize manufacturing, optimize logistics, and provide technical training to converters can rapidly expand regional market share.

Growth of Roll-Fed Labeling Systems

Roll-fed wrap labeling formats are gaining traction due to compatibility with automated, high-speed production lines. Continuous web systems reduce changeover time, minimize waste, and improve throughput efficiency. Beverage and home-care manufacturers increasingly invest in roll-fed systems to support rapid product launches and seasonal promotions. Film producers that develop dimensionally stable, print-ready roll-fed substrates gain competitive positioning in large-volume applications.

Category-wise Analysis

Material Type Insights

Polyethylene-based films are anticipated to maintain approximately 33.2% share, reinforcing their leadership position across high-volume packaging applications. Their dominance reflects cost competitiveness, moisture resistance, flexibility, and recyclability advantages. PE integrates effectively into mono-material packaging structures, facilitating mechanical recycling and alignment with circular economy objectives set by brand owners and regulators. In beverage and household care packaging, PE wrap films deliver reliable performance in high-speed labeling lines while maintaining graphic clarity and seal integrity. For instance, bottled water brands and liquid detergent manufacturers commonly deploy HDPE and LDPE-based wrap labels to ensure durability during transport and storage. Brand owners focused on mass-market SKUs prefer PE solutions due to favorable total cost of ownership, wide raw material availability, and compatibility with established extrusion, flexographic, and gravure printing processes. Continuous advancements in metallocene PE grades are further enhancing puncture resistance and downgauging potential.

Polypropylene films are projected to witness the fastest growth trajectory during the forecast period. Growth momentum stems from enhanced stiffness, superior print surface characteristics, and downgauging potential compared to conventional PE grades. BOPP (biaxially oriented polypropylene) and cast PP variants provide improved gloss, dimensional stability, and ink adhesion, making them particularly suitable for premium branding. These attributes are highly valued in personal care, cosmetics, and premium beverage applications where aesthetics significantly influence purchasing decisions. For example, carbonated soft drinks and craft beverage brands increasingly use BOPP wrap labels to achieve high-definition graphics and vibrant color reproduction. PP also enables thinner film structures without compromising tensile strength, reducing raw material consumption per unit, and supporting lightweighting initiatives. As converters pursue operational efficiency and higher visual differentiation, PP adoption continues to accelerate across automated, high-speed production environments.

Product Insights

Shrink wrap films are anticipated to account for roughly 41.3% of the market share, maintaining their position as the leading label format, particularly in beverage packaging. Shrink labels offer a tight, tamper-evident fit and enable full-body decoration on irregular or curved containers, enhancing shelf visibility and brand storytelling. Bottled water, carbonated beverages, energy drinks, and alcoholic beverages frequently utilize shrink labels for 360-degree graphics and security assurance. PET bottles with contoured designs especially benefit from shrink technology due to its ability to conform precisely to complex shapes. Operational compatibility with existing shrink tunnels and minimal equipment modifications further supports widespread adoption across high-volume bottling plants. Ongoing development of low-density and recyclable shrink films is also strengthening their sustainability profile.

Roll-fed labels represent the fastest-growing product category, driven by efficiency gains and cost optimization priorities. Their compatibility with ultra-high-speed filling lines, reduced adhesive usage, and continuous web processing make them economically attractive for large-scale beverage and FMCG manufacturers. Roll-fed systems enable rapid SKU changeovers, improved line uptime, and consistent dimensional accuracy. Major soft drink and dairy producers increasingly deploy roll-fed labeling systems to support automation and production scalability. These films also offer material savings compared to pressure-sensitive alternatives, improving overall packaging economics. As global consumer goods manufacturers invest in smart manufacturing and high-throughput bottling infrastructure, demand for dimensionally stable, high-clarity roll-fed films is projected to expand steadily over the coming years.

Regional Insights

North America Wrap Around Label Films Market Trends - Automation-Driven Premium Beverage Expansion and Regulatory-Led Performance Upgrades

North America represents a mature yet stable market characterized by high per-capita consumption of packaged beverages, personal care products, and household goods. The U.S. leads regional demand, supported by its extensive beverage bottling infrastructure and large-scale operations of global players such as The Coca-Cola Company and PepsiCo. These companies continue to invest in packaging redesigns that improve recyclability and labeling efficiency, directly influencing demand for advanced wrap around label films. Pharmaceutical labeling standards enforced by the U.S. Food and Drug Administration elevate technical requirements related to ink adhesion, chemical resistance, and traceability, raising the performance threshold for film converters.

Growth in the region is supported by premium beverage launches, compliance-driven packaging updates, and automation investments. For example, Constellation Brands has expanded production capacity across North America to support premium alcoholic beverages, increasing demand for high-clarity decorative labeling solutions. Converters are modernizing production lines with hybrid flexographic–digital printing technologies to handle shorter runs and SKU proliferation efficiently. Sustainability remains central, as resin suppliers such as Dow Inc. and ExxonMobil continue developing recyclable polyethylene and polypropylene film grades compatible with store drop-off and mechanical recycling streams.

Private equity participation has accelerated consolidation across packaging and labeling converters, improving operational efficiency and expanding integrated service offerings. Companies such as CCL Industries have expanded their North American footprint through acquisitions, strengthening their shrink sleeve and roll-fed labeling capabilities. Regional suppliers emphasize technical support, rapid prototyping, and collaborative design services to help brand owners meet sustainability pledges while maintaining high-speed production efficiency.

Europe Wrap Around Label Films Market Trends - EU Circular Economy Compliance and Recyclable Mono-Material Film Innovation

Europe maintains strategic importance due to stringent environmental regulations and advanced recycling infrastructure. Countries including Germany, the U.K., France, and Spain serve as major production and consumption centers. Regulatory alignment under the European Union’s packaging and waste directives has accelerated the transition toward recyclable and PCR-compatible film structures. The European Commission continues advancing circular economy action plans, directly influencing material selection and labeling system design. Sustainability mandates are compelling packaging redesigns to comply with recyclability and recycled content targets. For instance, Nestlé has implemented recyclable packaging initiatives across several European beverage brands, encouraging the adoption of mono-material label films compatible with PET bottle recycling streams. Film producers such as Berry Global and Taghleef Industries have expanded sustainable BOPP film portfolios in Europe, supporting downgauging and improved recyclability. Digital watermarking initiatives backed by organizations such as HolyGrail 2.0 are being piloted to enhance automated sorting accuracy, which increases the value proposition of advanced decorative films that remain recyclable.

Investment across Europe focuses on upgrading extrusion capacity, incorporating advanced coating systems, and strengthening recycling partnerships. Companies capable of certifying compliance with EU recyclability standards and offering life-cycle assessment data gain a measurable competitive advantage in this regulation-driven market environment.

Asia Pacific Wrap Around Label Films Market Trends - High-Volume Beverage Capacity Expansion and Cost-Competitive Sustainable Film Growth

Asia Pacific is projected to account for approximately 34.8% of market share and remains the fastest-growing regional market. Major economies such as China, India, Japan, and members of the Association of Southeast Asian Nations drive substantial demand through expanding beverage production and consumer goods manufacturing. Rapid urbanization and rising disposable incomes continue to elevate packaged product consumption across urban centers. In China, large beverage producers, including Nongfu Spring, have expanded bottling capacity to meet domestic demand, stimulating the need for high-speed roll-fed and shrink labeling films. India’s packaged beverage and dairy sectors, led by brands such as Amul, are investing in automated filling and labeling lines, increasing the adoption of dimensionally stable polypropylene films. Meanwhile, Japan emphasizes high-performance specialty films, with companies such as Toray Industries advancing high-clarity BOPP and PET film technologies.

Cost advantages, proximity to petrochemical feedstocks, and government-backed manufacturing initiatives enhance regional competitiveness. Regulatory frameworks vary across countries; however, multinational companies often apply global sustainability standards across their Asian operations. As a result, demand for recyclable mono-material film solutions is expanding, particularly among exporters aligning with European and North American environmental requirements. Suppliers combining cost efficiency with strong technical service networks are positioned for sustained double-digit growth in this dynamic regional market.

Competitive Landscape

The global wrap around label films market demonstrates moderate concentration. Large global packaging and label solution providers maintain strong positions in high-value technical segments, while regional converters compete in commodity volumes. Tier-1 players differentiate through R&D capability, sustainability credentials, and integrated service offerings. Competitive intensity centers on innovation, cost optimization, and geographic expansion. Market leaders prioritize recyclable mono-material innovation, supply chain integration for PCR sourcing, and expansion into high-growth Asia Pacific markets. Technical service excellence, rapid product customization, and sustainability validation form key competitive differentiators.

Key Industry Developments

- In 2025, Innovia Films opened a new multi-layer co-extrusion line in P?ock, Poland, producing sustainable low-density polyolefin shrink film (RayoFloat™) that floats during recycling and facilitates separation from PET containers in beverage and home-care packaging.

- In June 2025, Innovia Films showcased a next-generation sustainable label portfolio at Labelexpo 2025, including floatable shrink sleeves, recycled-content films (Encore™ with 35% mechanically recycled content), and PVC-free graphic films, reinforcing the industry trend toward recyclable wrap-around materials.

Companies Covered in Wrap Around Label Films Market

- Berry Global

- CCL Industries

- Taghleef Industries

- Toray Industries

- Dow Inc.

- ExxonMobil

- Avery Dennison

- Amcor

- Mondi

- Huhtamaki

- Jindal Poly Films

- UFlex Limited

- Cosmo Films

- Polinas

- Treofan Group

- Innovia Films

- Sealed Air

- Constantia Flexibles

Frequently Asked Questions

The global wrap around label films market is estimated to be valued at US$3.5 billion in 2026.

The wrap around label films market is projected to reach approximately US$5.3 billion by 2033.

Key trends include increasing adoption of recyclable mono-material PE and PP films, downgauging of BOPP structures to reduce material usage, integration of hybrid flexographic–digital printing for shorter SKU cycles, and regulatory-driven packaging redesign in North America and Europe.

By material type, polyethylene (PE) leads with an anticipated share of 33.2%, while by product type, shrink Labels dominate with approximately 41.3% market share, widely used in beverage packaging for full-body decoration and tamper evidence.

The wrap around label films market is expected to expand at a CAGR of 6.1% during the forecast period.

Major players include Berry Global, CCL Industries, Taghleef Industries, Toray Industries, and Dow Inc.