- Automotive Components & Materials

- Automotive Wrap Films Market

Automotive Wrap Films Market Size, Share, and Growth Forecast, 2026 – 2033

Automotive Wrap Films Market by Film Finish (Gloss Finish, Matte Finish, Satin Finish, Carbon Fiber Finish, Chrome Finish), Application (Car Wraps, Truck Wraps, Bus Wraps, Motorcycle Wraps, Fleet Wraps), and Regional Analysis for 2026 – 2033

Automotive Wrap Films Market Size and Trends Analysis

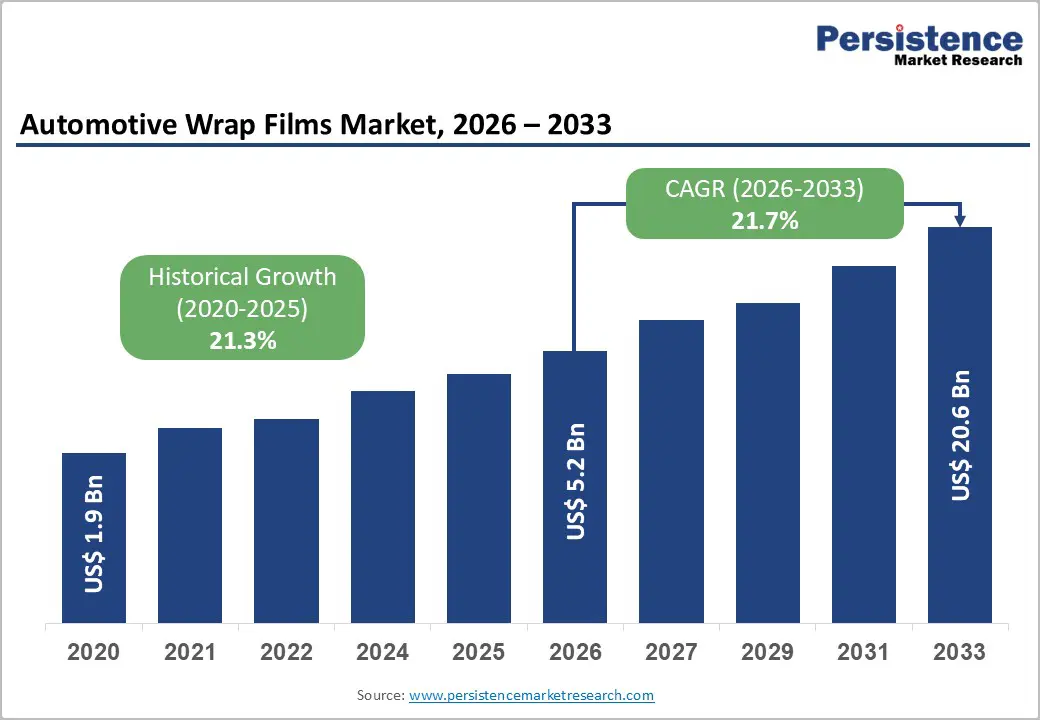

The global automotive wrap films market size is likely to be valued at US$5.2 billion in 2026 and is expected to reach US$20.6 billion by 2033, growing at a CAGR of 21.7% during the forecast period from 2026 to 2033, driven by the rising demand for vehicle aesthetics customization, increasing use of wrap films for commercial fleet branding and mobile advertising, and continuous advancements in high-performance vinyl materials offering enhanced durability, conformability, and surface protection.

The expanding automotive aftermarket ecosystem, coupled with consumer preference for cost-effective, reversible alternatives to repainting, supports demand for such alternatives across passenger and commercial vehicles. Wrap films provide functional benefits such as UV resistance, scratch protection, and paint preservation, strengthening adoption. While raw material price volatility and skilled installation costs remain key challenges, strong aftermarket penetration and growing awareness position the automotive wrap films market for sustained double-digit growth.

Key Industry Highlights:

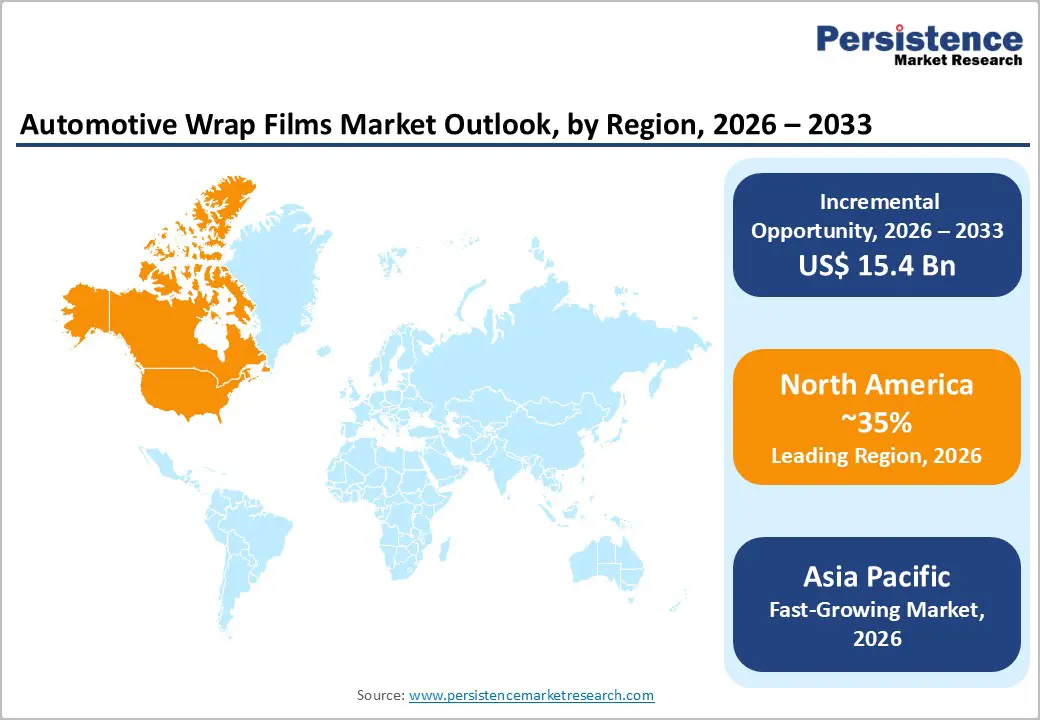

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by strong aftermarket customization demand, widespread fleet advertising adoption, advanced distribution networks, and growing opportunities in EV personalization.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the automotive wrap films in 2026, supported by rapid vehicle production growth, rising customization demand, expanding EV adoption, and a fast-developing automotive aftermarket across China, Japan, India, and ASEAN countries.

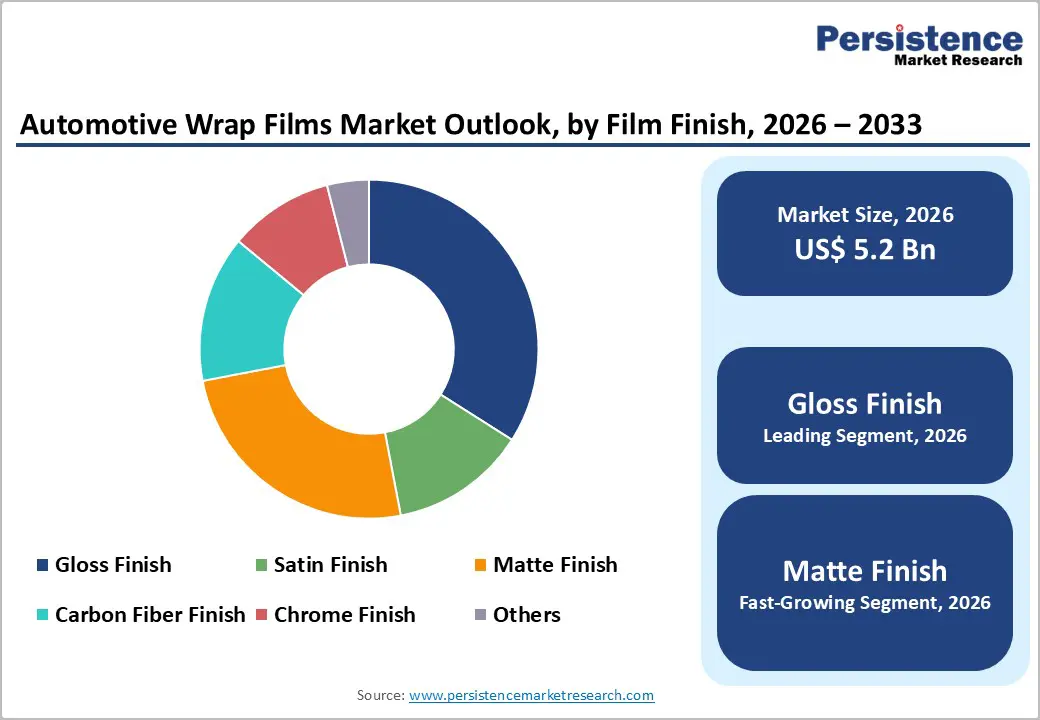

- Leading Film Finish Type: Gloss finish is projected to represent the leading film finish type in 2026, accounting for 40% of the revenue share, driven by its paint-like shine, broad consumer acceptance, and ease of maintenance for vehicle personalization and protection.

- Leading Application: Car wraps are anticipated to be the leading application type, accounting for over 50% of the revenue share in 2026, supported by high passenger vehicle ownership and strong demand for customization and paint protection.

| Report Attribute | Details |

|---|---|

|

Automotive Wrap Films Market Size (2026E) |

US$5.2 Bn |

|

Market Value Forecast (2033F) |

US$20.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

21.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

21.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand for Vehicle Personalization and Customization

Consumers increasingly seek unique visual identities for their vehicles without permanent paint changes. Wrap films offer flexibility in colors, textures, and finishes such as gloss, matte, satin, and carbon fiber, appealing to younger buyers and car enthusiasts. The ability to customize vehicles at a lower cost than repainting, combined with reversibility, strongly supports adoption. Growing social media influence, car culture communities, and lifestyle branding accelerate demand for personalized automotive aesthetics across passenger vehicles.

Rising disposable incomes and urbanization are enabling consumers to spend more on vehicle appearance upgrades. Automotive wrap films also protect the original paint, preserving resale value and enhancing their appeal. OEMs and aftermarket installers increasingly collaborate to offer certified wrap services, improving quality and consumer trust. This driver is particularly strong in North America, Europe, and emerging Asia-Pacific markets, where customization trends are becoming mainstream, driving sustained demand growth for wrap film solutions.

Growth in Commercial Fleet Branding and Advertising

Businesses adopt vehicle wraps for cost-effective, high-visibility advertising. Fleet wraps transform vehicles into mobile billboards, offering continuous brand exposure compared to traditional advertising channels. Logistics companies, food delivery services, ride-hailing platforms, and service providers increasingly rely on wrap films to enhance brand recognition while protecting vehicle surfaces. The durability and removability of wrap films make them ideal for temporary campaigns, fleet rebranding, and leased vehicle applications.

The expansion of e-commerce, last-mile delivery, and shared mobility services is accelerating fleet size growth. Fleet sizes are increasing, and demand for durable, easy-to-install, and visually appealing wrap films is rising. Wrap films enable uniform branding across large fleets with minimal downtime and maintenance. Advances in digital printing allow high-resolution graphics and faster customization, increasing adoption. Businesses prioritize measurable marketing returns and brand consistency, and fleet wraps continue to generate strong demand, supporting long-term market expansion. Wrap films protect fleet vehicles from surface damage, reducing maintenance costs.

Barrier Analysis - Regulatory and Environmental Concerns

Many wrap films are manufactured from PVC-based materials, raising concerns about recyclability, waste disposal, and environmental impact. Increasingly stringent environmental regulations in regions such as Europe and North America require manufacturers to comply with restrictions on volatile organic compounds (VOCs), chemical additives, and production emissions. Compliance with these regulations increases operational costs and may limit manufacturers' material options.

Regulatory requirements governing vehicle appearance and advertising content can restrict the use of wrap films, especially for commercial fleets. Certain jurisdictions impose limitations on reflective finishes, colors, or advertising graphics on public transport and commercial vehicles. These regulatory variations create complexity for manufacturers and fleet operators. Manufacturers must invest in eco-friendly alternatives and certification processes to mitigate regulatory risks while maintaining performance standards. Adapting products to meet diverse compliance standards requires continuous investment in research, testing, and certification, which can slow market growth in highly regulated regions.

Limited Durability and Performance under Harsh Conditions

Prolonged exposure to extreme heat, ultraviolet radiation, humidity, and pollution can lead to fading, peeling, cracking, or discoloration of wrap films. These issues reduce aesthetic appeal and shorten product lifespan, increasing replacement frequency. In regions with severe climates, such as high-temperature or coastal environments, durability concerns are more pronounced, discouraging adoption among cost-sensitive consumers and commercial fleet operators.

Installation quality also significantly impacts performance, and improper application can accelerate wear and failure. The availability of skilled installers varies by region, creating inconsistencies in product performance. Although premium wrap films offer enhanced durability and protective coatings, their higher costs limit adoption among price-conscious buyers. Addressing durability limitations through material innovation and installer training remains critical to overcoming this restraint.

Opportunity Analysis - Technological Convergence with Digital Printing and Sustainable Materials

Technological convergence presents a significant opportunity for the automotive wrap films market, particularly through advances in digital printing. High-resolution digital printing allows intricate designs, faster turnaround times, and mass customization for both personal and commercial applications. This capability enhances value for fleet branding, promotional campaigns, and limited edition vehicle designs. Improved printing efficiency reduces production lead times and supports scalability, expanding the potential customer base across aftermarket and commercial segments.

The shift toward sustainable materials creates new growth opportunities. Manufacturers are investing in non-PVC films, recyclable substrates, and low-VOC adhesives to address environmental concerns and regulatory requirements. Sustainable wrap films appeal to environmentally conscious consumers and businesses while ensuring compliance. The combination of advanced printing and eco-friendly materials positions wrap films as innovative, future-ready solutions, driving adoption across markets.

Increased Demand from Motorsports, Luxury Vehicles, and Premium Finishes

Motorsports teams widely use wrap films for sponsorship branding, rapid design changes, and lightweight surface solutions. Wrap films enable quick updates between races without repainting, making them highly efficient for competitive environments. This segment demands high-performance films with superior durability and visual impact. Wraps provide enhanced protection against high speeds, heat, and track debris, ensuring consistent branding throughout racing seasons. The growing commercialization of motorsports and sponsorship deals increases demand for advanced wrap film solutions.

Luxury and premium vehicle owners are increasingly adopting wrap films to enhance exclusivity while preserving the original paint. Specialty finishes such as satin, carbon fiber, and chrome are particularly popular in this segment. Electric and high-end vehicles benefit from wraps that deliver both aesthetic appeal and surface protection. Rising demand for personalized luxury mobility and limited-edition vehicle appearances strengthens adoption. Expanding luxury-vehicle sales and premium aftermarket services continue to drive innovation and higher-margin wrap-film product development.

Category-wise Analysis

Film Finish Insights

Gloss finish films are expected to lead the automotive wrap films market, accounting for approximately 40% of revenue in 2026, driven by their strong resemblance to factory paint and broad consumer acceptance across passenger and commercial vehicles. Its high-shine finish enhances vehicle aesthetics while maintaining a clean, premium look, making it a preferred choice for full-body wraps and paint protection. Gloss films are easier to clean and maintain than textured finishes, supporting widespread adoption among daily-use vehicles and commercial fleets. For example, fleet vehicles for food delivery and logistics companies, where gloss wraps are widely used to ensure vibrant branding, color consistency, and long-term durability while protecting the original paint surface.

The matte finish is expected to be the fastest-growing segment in 2026, driven by the increasing demand for sleek, subtle, and non-reflective vehicle designs. Matte wraps are especially favored by luxury, premium, and urban car owners looking for exclusivity and distinction. Social media trends and influencer-driven automotive styling are fueling this shift. For instance, luxury sedans and premium SUVs are increasingly opting for matte black and matte gray finishes to achieve a bold, modern look while ensuring surface protection.

Application Insights

Car wraps are expected to dominate the market, accounting for approximately 50% of the revenue share in 2026. This growth is driven by high passenger-vehicle ownership rates and rising demand for vehicle customization and paint protection. More car owners are choosing wrap films to personalize their vehicle’s color, texture, and finish without making permanent changes. Car wraps also offer protection against scratches, UV damage, and minor abrasions, helping to maintain the vehicle’s long-term value. The widespread availability of aftermarket services and the ease of installation further solidify their market leadership. For example, personal passenger vehicles in urban areas often feature full-body gloss or satin wraps to enhance their appearance while preserving the original paint.

Fleet wraps are expected to be the fastest-growing application in 2026, driven by rising demand for mobile advertising and brand visibility on commercial vehicles. Businesses are increasingly opting for fleet wraps as a cost-effective marketing tool that delivers ongoing exposure without recurring advertising costs. The growth of logistics, e-commerce delivery, and service fleets is driving this trend, with durable wrap materials designed to withstand high-mileage usage. For instance, e-commerce delivery vans often use fleet wraps to ensure consistent branding, promotional messaging, and vehicle surface protection across large fleets.

Regional Insights

North America Automotive Wrap Films Market Trends

North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by a strong culture of vehicle customization, aftermarket demand, and commercial branding, securing the region's position as the dominant shareholder. Consumers increasingly view wrap films as a cost-effective way to personalize aesthetic finishes from gloss and matte looks to specialty textures while protecting original paintwork. For example, Avery Dennison Corporation has expanded offerings such as its Supreme Wrapping Film series with new colors and finishes aimed specifically at North American customers, strengthening its market foothold and aligning with consumer expectations for high-quality aesthetics and durability.

The North American market is also shaped by business needs, particularly in fleet branding, digital printing adoption, and installer innovation. Commercial fleets in logistics, delivery, and service sectors are increasingly outfitted with high-resolution vehicle graphics as mobile advertising tools, making wrap films a strategic marketing asset beyond aesthetic personalization. Companies are leveraging enhanced digital printing capabilities to offer intricate, brand-aligned designs that appeal to both regional businesses and national campaigns.

Europe Automotive Wrap Films Market Trends

Europe is likely to be a significant market for automotive wrap films in 2026, due to strong automotive cultures in countries such as Germany, France, and the U.K. European consumers increasingly choose wraps over traditional paint jobs because they offer cost, time, and flexibility advantages while preserving the vehicle's original finish. The region also benefits from a well-developed aftermarket ecosystem, including advanced installation networks and digital printing services that support intricate custom designs and quick turnaround times. For example, ORAFOL Europe GmbH has expanded its ORACAL wrap film portfolio with premium shift-effect and eco-compliant cast films tailored to high-end customization and regulatory expectations, reinforcing European leadership in advanced wrap technologies.

Growth trends in Europe’s automotive wrap films market also reflect rising commercial and corporate adoption alongside evolving consumer tastes. Fleet branding remains a notable driver, with European businesses, logistics providers, and service fleets increasingly deploying wraps for mobile advertising, vehicle identity, and promotional campaigns. Wrap films convert fleets into dynamic marketing platforms that deliver wide visibility across urban and suburban corridors, making them more cost-effective than traditional static advertising.

Asia Pacific Automotive Wrap Films Market Trends

The Asia-Pacific region is expected to be the fastest-growing in the automotive wrap films market in 2026, driven by rising vehicle ownership, expanding middle-class incomes, and growing consumer interest in customization and protection. The region’s rising disposable incomes and urbanization are fueling strong demand for vehicle personalization, protective finishes, and commercial branding applications. Increasing aftermarket awareness, coupled with expanding installer networks, has broadened the adoption of vinyl wraps for both personal and commercial use.

Asia Pacific's diverse consumer base favors a range of finishes from gloss and matte to specialty textures, driving manufacturers to offer broader portfolios tailored to regional tastes and climate conditions. For example, Guangzhou Carbins Film Co., Ltd. is recognized in industry reports as a significant regional provider of automotive wrap vinyl, leveraging local manufacturing and distribution to serve growing markets in China and Southeast Asia. The company's expanding product range supports aesthetic customization and functional surface protection, helping meet the needs of both consumer and commercial vehicle segments.

Competitive Landscape

The global automotive wrap films market exhibits a moderately fragmented structure, driven by competition among established multinational manufacturers and a long tail of regional specialists focusing on price, customization, and niche segments. Leading film producers invest heavily in material technology development, adhesive innovations, and expanded finish portfolios to meet rising demand for customization, paint protection, and commercial branding applications. Large players benefit from strong brand recognition, extensive distribution networks, and certified installer programs that help maintain product quality and market reach.

With key leaders including 3M Company, Avery Dennison Corporation, and ORAFOL Europe GmbH, the market’s competitive landscape reflects both dominance and localized strategies. These players compete through broad product portfolios that span gloss, matte, and specialty finishes, advanced digital printing solutions, and installer support services that improve application quality and end-user experience. Competitive dynamics are influenced by strategic partnerships, product launches, and sustainability initiatives aimed at capturing varied consumer and commercial segments worldwide.

Key Industry Developments:

- In September 2025, XPEL, Inc. launched its COLOR Paint Protection Film (PPF), combining vehicle personalization with top-tier paint protection. Offering 16 premium color options, it allows full-vehicle or accent wraps while maintaining the durability and self-healing qualities of XPEL’s traditional clear PPF. Thicker than vinyl wraps, COLOR PPF resists fading and peeling, and offers long-term protection against scratches, rock chips, and environmental damage.

- In September 2025, Avery Dennison® debuted an exclusive Supreme Wrapping Film™ collection in collaboration with automotive influencer Supercar Blondie (Alex Hirschi). The limited-edition range features four striking finishes, Matte Dreamline Blue, Gloss Metallic Cosmic Rose, Gloss Smooth Sage, and Satin Sunset Ride, targeting luxury car owners and customization enthusiasts. Developed with Easy Apply™ RS technology, the films ensure quick, high-quality installation and long-lasting performance.

Companies Covered in Automotive Wrap Films Market

- 3M Company

- Avery Dennison Corporation

- Hexis S.A.

- Orafol Group

- Arlon Graphics, LLC

- VViViD Vinyl

- KPMF USA Ltd

- Ritrama S.p.A.

- FELLERS

- TeckWrap

- Wrap Films Systems

- Incision Vinyl

- MetroWrapz

- GrafiWrap

Frequently Asked Questions

The global automotive wrap films market is projected to reach US$5.2 billion in 2026.

The automotive wrap films market is driven by rising vehicle personalization demand, expanding commercial fleet branding, cost-effective alternatives to repainting, and growing adoption of protective and premium aesthetic solutions.

The automotive wrap films market is expected to grow at a CAGR of 21.3% from 2026 to 2033.

Key market opportunities lie in premium and colored paint protection films, sustainable and digitally printed wrap technologies, growing EV and luxury vehicle customization, and expanding commercial fleet branding applications.

3M Company, Avery Dennison Corporation, Hexis S.A., Orafol Group, and Arlon Graphics, LLC are the leading players.