- Hardware & Software IT Services

- Workplace Analytics Market

Workplace Analytics Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Workplace Analytics Market by Solution (Workplace Analytics Software and Services), Deployment Mode (Cloud-based and On-premises, Organization Size (Large Enterprises and SMEs), End-user (Healthcare, IT & Telecommunication, BFSI, Manufacturing, Retail, Aerospace & Defense and Others) and Regional Analysis for 2026 - 2033

Workplace Analytics Market Size and Trends Analysis

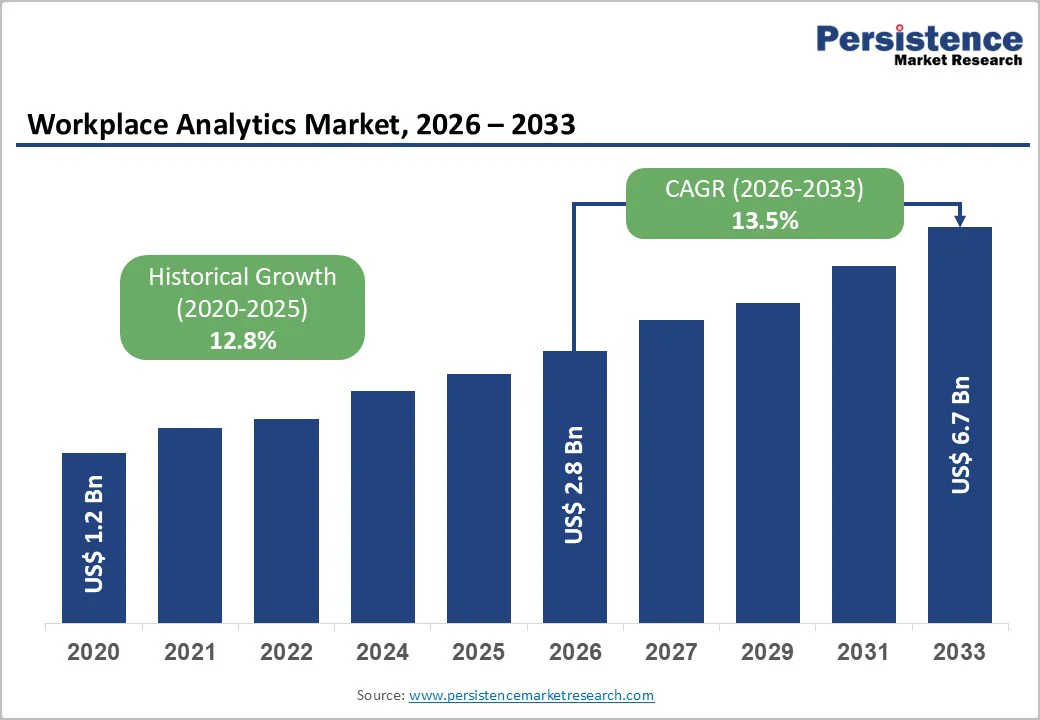

The global workplace analytics market size was valued at US$ 2.8 billion in 2026 and is projected to reach US$ 6.7 billion by 2033, growing at a CAGR of 13.5% between 2026 and 2033.

The market's acceleration is propelled by three primary catalysts: accelerating adoption of cloud-based HR analytics platforms enabling real-time decision-making, enterprise implementation of artificial intelligence and machine learning within human capital management systems, and intensifying focus on employee engagement, retention, and productivity measurement across organizational hierarchies.

Key Industry Highlights:

- Component Leadership: Services dominate the market with 65.3% share, driven by extensive deployment support, managed services, and ongoing optimization needs across enterprises. Analytics software emerges as the fastest-growing component at 17% CAGR, reflecting the rapid shift toward cloud-based SaaS intelligence platforms and decreasing reliance on traditional professional services.

- Deployment Model Dynamics: Cloud-based deployment maintains clear leadership with 60% market share, supported by scalability, lower upfront costs, and seamless integration capabilities. On-premises solutions record the fastest growth at 18% CAGR among highly regulated sectors such as BFSI and defense, where strict compliance, data sovereignty, and security mandates drive local infrastructure adoption.

- Organization Size Trends: Large enterprises hold 62.3% share, underpinned by robust analytics investments and enterprise-wide digital transformation initiatives. SMEs represent the fastest-growing segment at 17.8% CAGR, enabled by affordable SaaS models and simplified deployment that democratize access to advanced analytics tools.

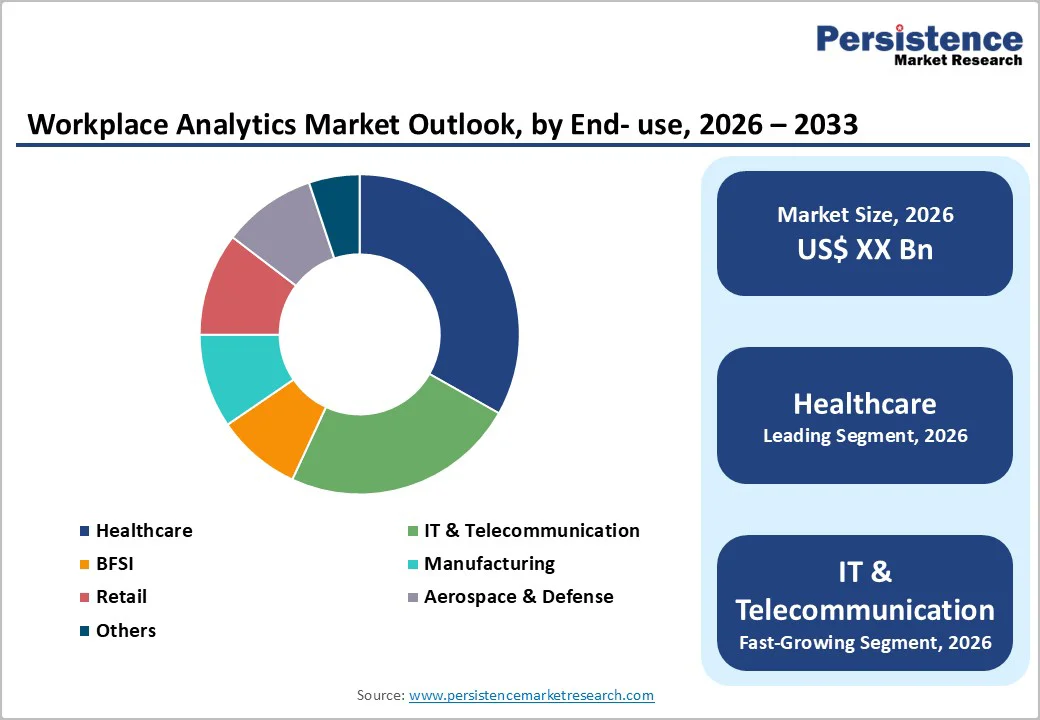

- End-user Vertical Patterns: Healthcare leads with 32.3% market share, driven by workforce optimization needs, patient flow management, and increasing digital health adoption. Manufacturing is the fastest-growing vertical at 19% CAGR, fueled by Industry 4.0 initiatives, predictive analytics adoption, and operational efficiency imperatives.

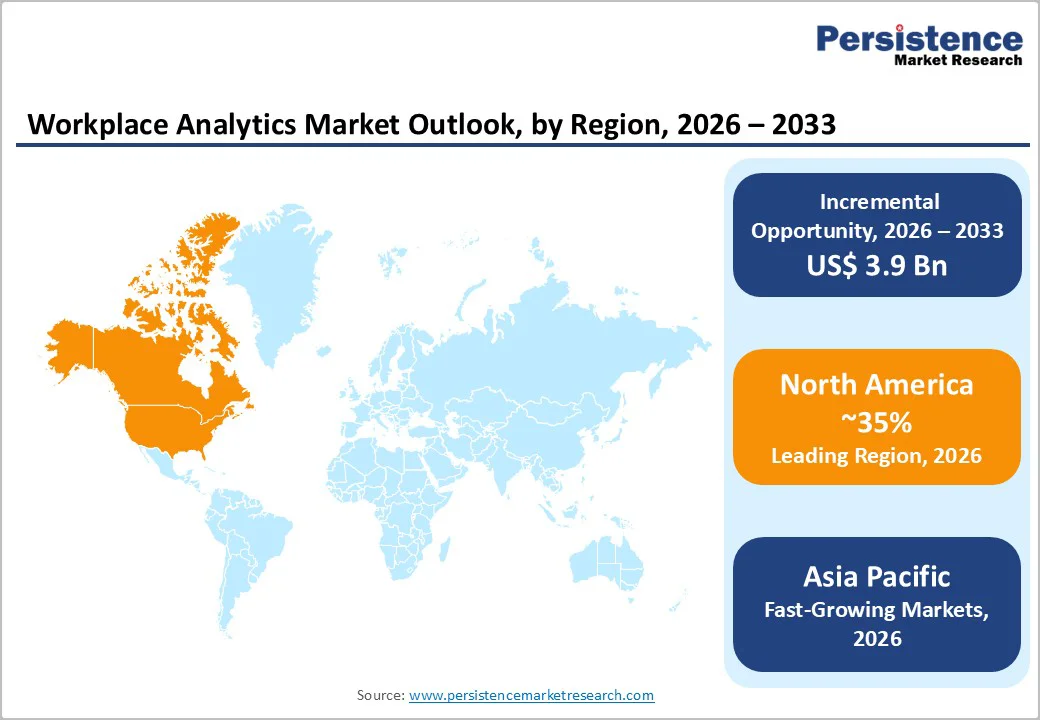

- Regional Growth Patterns: North America maintains leadership with 35% share, supported by advanced analytics adoption and mature enterprise IT ecosystems. Asia Pacific is the fastest-growing region at 16.3% CAGR, with India expanding at 19% CAGR, driven by rapid digitalization, manufacturing expansion, and growing cloud adoption across emerging economies.

| Key Insights | Details |

|---|---|

| Workplace Analytics Market Size (2026E) | US$ 2.8 Bn |

| Market Value Forecast (2033F) | US$ 6.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13.5% |

| Historical Market Growth (CAGR 2020 to 2024) | 12.8% |

Market Dynamics

Drivers - Remote and Hybrid Work Model Expansion and Workplace Management Complexity

The structural shift toward remote and hybrid work arrangements fundamentally transformed organizational requirements for workforce visibility, engagement monitoring, and distributed team management.

Post-COVID pandemic normalization stabilized hybrid work adoption, with approximately 70% of enterprise organizations maintaining hybrid or flexible work policies through 2025 - 2026, creating a persistent need for workplace analytics infrastructure enabling distributed workforce oversight.

Traditional office-based performance metrics became obsolete; organizations require sophisticated analytics platforms capturing productivity indicators, collaboration patterns, engagement signals, and performance data across geographically dispersed teams.

Workplace analytics solutions address this organizational imperative by providing centralized dashboards aggregating performance indicators from multiple data sources-email communications, calendar utilization, project management systems, employee surveys-into actionable intelligence.

Artificial Intelligence and Machine Learning Integration in Workforce Analytics

Generative AI and advanced machine learning integration fundamentally enhanced workplace analytics capabilities, transitioning platforms from descriptive reporting to predictive and prescriptive analytics, enabling proactive workforce management.

Contemporary workplace analytics platforms leverage machine learning algorithms to identify talent gaps through skill-gap analysis, predict employee attrition with 70-85% accuracy, and recommend targeted retention interventions. IBM's workforce analytics research demonstrates that AI-powered talent prediction systems improve hiring accuracy by 25-30%, reducing costly recruitment failures and onboarding costs.

SAP SuccessFactors analytics and Oracle Fusion HCM Analytics integrate generative AI, enabling conversational interfaces, natural language processing for sentiment analysis from employee surveys, and autonomous anomaly detection, identifying organizational dysfunction indicators.

These technological advancements enable HR teams to transition from reactive problem-solving to proactive workforce strategy optimization. Johnson & Johnson's AI skills-inference framework, integrating passive assessments and taxonomies, improved learning alignment and hiring accuracy measurably.

Restraints - Data Privacy Regulations, Employee Monitoring Concerns, and Compliance Complexity

Employee privacy apprehension regarding data collection, algorithmic decision-making transparency, and fragmented regulatory frameworks create structural adoption headwinds limiting market expansion velocity.

Workplace analytics inherently involves collecting sensitive employee data-performance metrics, email communications, calendar utilization, location tracking-generating legitimate privacy concerns among workforce populations and employee advocacy organizations. Recent surveys indicate that 25% of potential enterprise adopters cite privacy concerns as primary adoption barriers, representing substantial addressable market loss.

Regulatory fragmentation amplifies compliance burden: GDPR requirements in Europe mandate explicit consent protocols, purpose limitation restrictions, and data minimization standards fundamentally constraining analytics data collection scope.

Emerging frameworks including Europe's Digital Services Act, California's CCPA, and sector-specific regulations (healthcare HIPAA, financial services regulations) impose fragmented compliance requirements requiring vendors to maintain bifurcated product architectures and support structures.

High Implementation Costs, Change Management Complexity, and SME Budget Constraints

Enterprise workplace analytics platform implementation requires substantial technology investment, organizational change management, and skills development creating adoption barriers particularly acute for SME segments operating under capital expenditure constraints. Typical enterprise analytics platform deployment costs range USD 200,000 to USD 1.5 million for implementation, integration, training, and change management across organizations.

Change management complexity represents underestimated adoption barrier: approximately 89% of manufacturing organizations express intention to implement AI systems, but only 16% achieve enterprise scale, reflecting process and cultural challenges outweighing technology obstacles.

Opportunities - Generative AI-Powered Predictive Analytics and Autonomous HR Decision-Making

Next-generation workplace analytics platforms integrating generative AI enable autonomous workflow automation, conversational analytics interfaces, and predictive talent ecosystem management, representing nascent but high-growth opportunity segment.

Emerging applications include AI-powered succession planning identifying high-potential candidates using competency modeling and performance prediction; autonomous compensation optimization calculating equitable pay structures while managing market competitiveness; predictive attrition modeling identifying flight-risk employees with personalized retention interventions; and skills orchestration algorithms matching internal talent to emerging organizational capabilities.

These advanced capabilities transition analytics from insight generation to autonomous decision support, expanding addressable use cases and deployment value. Fortune 100 insurer case study illustrates opportunity: Workday Prism Analytics reduced dashboard build time from three weeks to one day, enabling manager-level access to self-service insights and accelerating decision velocity.

Cloud-Based SME Analytics Solutions and Vertical-Specific Implementations

Cloud-based software-as-a-service (SaaS) workplace analytics solutions targeting SME organizations represent highest-growth opportunity segment, enabling analytics democratization across mid-market enterprise populations historically excluded from enterprise suite deployments.

SME organizations leverage SaaS subscriptions, pre-configured dashboards, and low-code interface implementations to capture data-driven insights without heavy IT infrastructure investments or specialized analytics skills. SME segment demonstrates 17.8% CAGR, substantially exceeding large enterprise growth rates (12% CAGR), reflecting technology accessibility expansion and cost reduction enabling mass-market adoption.

Vertical-specific SaaS implementations addressing healthcare staffing optimization, retail labor scheduling, or IT services resource allocation create tailored solutions generating superior ROI relative to enterprise suite generic approaches. Market research indicates that approximately 70% of SME organizations intend workplace analytics implementation within 24 months, representing transformation from early-adopter technology to mainstream business requirement.

Category-wise Analysis

Solution Type Insights

Professional services account for 65.3% of the workplace analytics market, driven by essential implementation, integration, change management, and ongoing support needs in enterprise deployments.

Services include consulting, system integration with ERP/HCM platforms, user training, and managed services supporting continuous optimization. Enterprises allocate 40-60% of analytics project budgets to services, making it a core success factor for adoption. Major consulting firms such as Deloitte, Accenture, PwC, and KPMG capture nearly 45-50% of this revenue through strategic vendor partnerships.

Although services grow at a steady 12.5% CAGR, software solutions are expanding faster due to cloud-based SaaS models, pre-built data frameworks, and reduced implementation complexity. SaaS platforms enable faster deployments, lower upfront costs, and broader SME adoption. As a result, the software segment is expected to rise from 34.7% to 40% of market share by 2033, reflecting a structural shift toward scalable, AI-enabled, vendor-driven analytics solutions.

Deployment Mode Insights

Cloud-based workplace analytics account for 60% of market revenue, driven by demand for scalable, flexible solutions that eliminate on-premises infrastructure costs and support distributed workforces.

Benefits include automatic updates, reduced IT burden, faster deployments, and lower long-term ownership costs. Vendors such as Workday, SAP SuccessFactors, and Oracle Cloud report that 78% of new deployments now occur in the cloud, supported by improved security certifications and compliance frameworks.

While cloud solutions grow at 15% CAGR, on-premises deployments are the fastest-growing segment (18% CAGR) in highly regulated sectors like BFSI, government, and defense due to strict data sovereignty mandates. Hybrid models are increasingly adopted, balancing local data control with cloud scalability through enhanced access controls and encryption.

Organization Size Insights

Large enterprises account for 62.3% of workplace analytics market value due to large budgets, complex multi-unit operations, and the need for centralized workforce insights. These organizations invest USD 500,000-2.5 million annually in advanced analytics for engagement, productivity, retention, and compensation equity. With 75% of Fortune 500 already deployed, the segment shows 11% CAGR but faces saturation in mature regions.

SMEs are the fastest-growing segment, expanding at 17.8% CAGR as cloud-based SaaS platforms reduce cost and complexity barriers. Solutions from BambooHR, Dayforce, and UKG offer pre-built, configurable analytics for USD 5,000-25,000 per month, driving strong adoption in emerging markets.

End-user Insights

Healthcare organizations hold 32.3% of the workplace analytics market, driven by acute workforce shortages, high turnover, and burnout. Analytics supports scheduling optimization, predictive retention, burnout monitoring, and succession planning.

Case studies such as INTEGRIS Health’s USD 30 million savings highlight strong ROI, contributing to an 18.1% CAGR well above the market average. With 87% of U.S. hospitals planning higher analytics spending, the healthcare segment shows >95% renewal rates due to high operational dependence.

Manufacturing is the fastest-growing vertical (19% CAGR) as companies address aging workforces, skills gaps, and Industry 4.0 demands. Analytics improves skills planning, training effectiveness, scheduling, and succession development. Successes like Tata Steel’s USD 4 million annual savings fuel sector investment, driving significant market expansion through 2033.

Regional Insights and Trends

North America Workplace Analytics Market Share Insights

North America represents dominant regional market with 35% of global workplace analytics market share, commanding estimated market value of USD 1.0-1.1 billion in 2026 with projected expansion to USD 1.8-2.0 billion by 2033 at approximately 12.5-14.2% CAGR.

The United States dominates regional market with 69.3% market share of North American analytics deployments, reflecting advanced IT infrastructure maturity, sophisticated HR technology adoption, and established vendor ecosystem concentration. Canada and Mexico represent secondary markets demonstrating comparable adoption trajectories to U.S. patterns, though with delayed penetration cycles and lower overall solution sophistication.

North American market demonstrates a concentrated competitive structure dominated by Workday (9.8% market share), Microsoft (strong cloud presence), UKG, SAP, and ADP, collectively commanding 45% of regional market revenue. Workday's market leadership derives from sophisticated cloud platform, agentic AI integration, and a strategic acquisition strategy (HiredScore, VNDLY acquisitions expanding recruiting and contingent workforce capabilities).

Europe Workplace Analytics Market Share and Trends Insights

Europe represents approximately 22% of the global workplace analytics market, estimated at USD 600 million in 2026 with projected expansion to USD 1.2 billion by 2033 at approximately 11.5% CAGR.

Germany, United Kingdom, France, and Spain collectively represent 70% of European market value, with Germany maintaining the largest market share (approximately USD 220-280 million) driven by manufacturing sector dominance and advanced industrial infrastructure.

European market demonstrates slower adoption velocity relative to North America (reflecting GDPR compliance complexity), partially offset by the Nordic region's technology adoption leadership and emerging Central European market expansion.

European Union GDPR framework creates structural constraints on analytics data collection and processing methodologies: stringent consent requirements, purpose limitation restrictions, data minimization mandates, and individual access rights fundamentally constrain analytics scope compared to North American regulatory environment.

Asia Pacific Workplace Analytics Market Share and Trends Insights

Asia Pacific commands approximately 25% of the global workplace analytics market, estimated at USD 750 million in 2026 with projected expansion to USD 2.2 billion by 2033, reflecting 16.3% CAGR substantially exceeding the global average (13.5%).

The region demonstrates the highest absolute growth velocity, reflecting convergence of rapid digital infrastructure expansion, emerging market manufacturing transformation, and aggressive vendor investment prioritizing Asian market positioning.

China commands approximately 40% of the Asia Pacific market value, while India represents the fastest-growing Asia Pacific market with 19% CAGR driven by Infosys, Tata Consultancy Services (TCS), and emerging market adoption acceleration.

Asia Pacific regulatory environment demonstrates substantial heterogeneity: China maintains state-controlled ecosystem with centralized data governance requirements; India implements emerging privacy frameworks (Digital Personal Data Protection Act) balancing innovation with consumer protection; Japan maintains technology-forward regulatory approach emphasizing interoperability; ASEAN markets represent a largely unregulated landscape creating market opportunity.

Workplace Analytics Market Competitive Landscape

Market concentration demonstrates oligopolistic characteristics with six major vendors (Workday, Microsoft, SAP, Oracle, UKG, ADP) controlling 50% of global market value.

Workday maintains market leadership with an estimated 9.8% global market share through sophisticated cloud platform, agentic AI integration, and strategic acquisition strategy consolidating talent acquisition, contingent workforce management, and analytics capabilities.

Microsoft follows with a substantial cloud presence and Power BI analytics adoption among Office 365 organizations. SAP SuccessFactors and Oracle Fusion Analytics command enterprise market segments through comprehensive HCM suite integration.

Key Industry Developments

- In January 2024, Accenture acquired Work & Co, expanding digital product and experience transformation capabilities within analytics consulting services.

- In June 2023, Sapience Analytics, a workforce analytics and insights provider, and QuantumWork Advisory (QWA), partnered to revolutionize companies' management of external labor spending through data analytics and strategic workforce design.

- In April 2023, Workday, Inc. and Alight, Inc., providers of enterprise cloud applications for finance and human resources, entered a strategic partnership to provide a simplified, unified payroll experience for human resources and payroll professionals across the globe.

Companies Covered in Workplace Analytics Market

- IBM Corporation

- Oracle Corporation

- SAP SE

- Tableau Software

- ADP, LLC.

- Workday, Inc.

- Workforce Software

- Microsoft

- Slack

- Asana

- Qualtrics

- Others Key Players

Frequently Asked Questions

The Workplace Analytics market is estimated to be valued at US$ 2.8 Bn in 2026.

The primary demand driver for the Workplace Analytics market is the rising need for data-driven workforce optimization and productivity enhancement across enterprises.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Workplace Analytics market.

Among the End- use, Healthcare holds the highest preference, capturing beyond 32.3% of the market revenue share in 2026.

The key players in Workplace Analytics are IBM Corporation, Oracle Corporation, SAP SE, Tableau Software, and ADP, LLC.