- Technology

- Digital Workplace Market

Digital Workplace Market Size, Share, and Growth Forecast, 2026 – 2033

Digital Workplace Market by Component Type (Solutions, Services), Enterprise Size (Large Enterprise, SMEs), Industry Vertical (BSFI, Healthcare, Others), and Regional Analysis 2026 – 2033

Digital Workplace Market Size and Trends Analysis

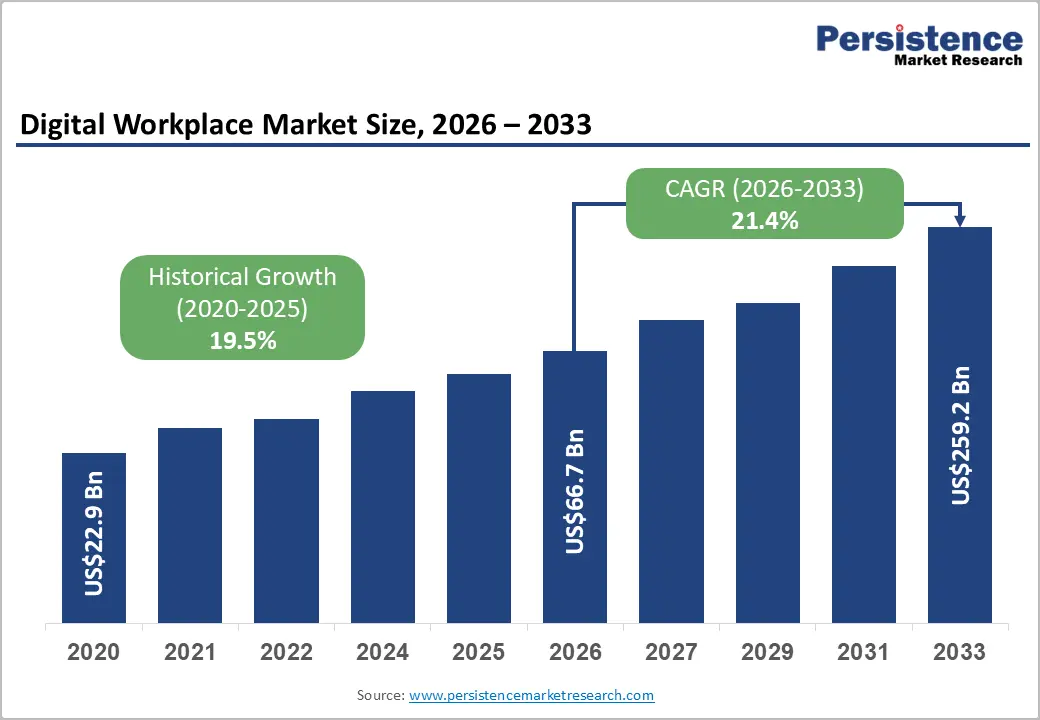

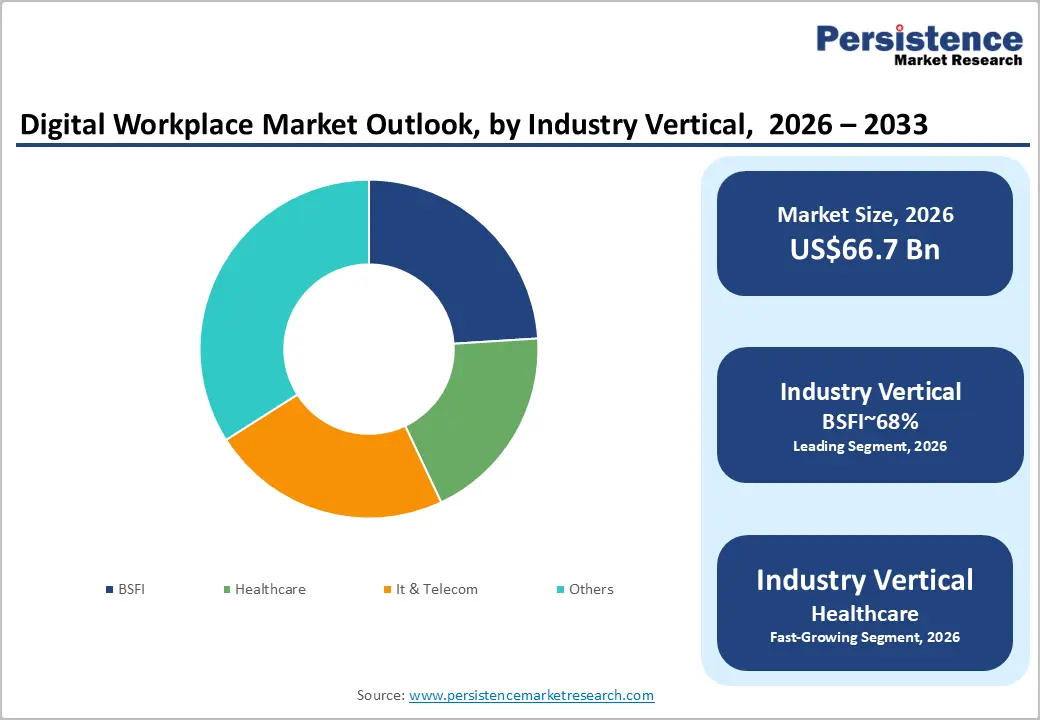

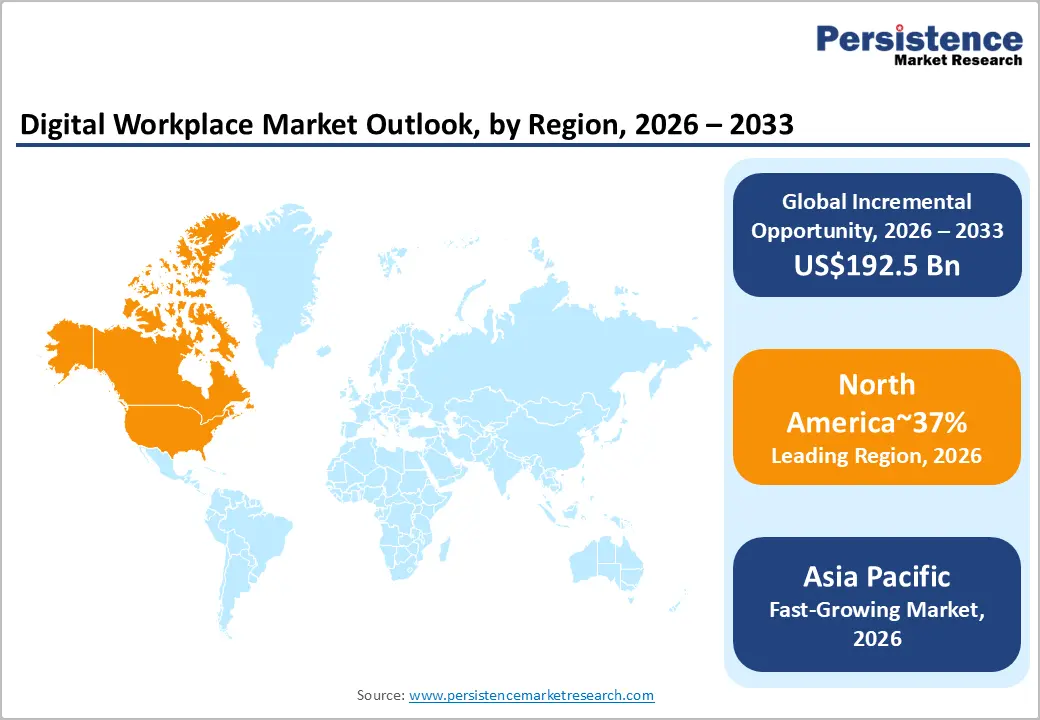

The global digital workplace market size is likely to be valued at US$66.7 billion in 2026 and is expected to reach US$259.2 billion by 2033, growing at a CAGR of 21.4% during the forecast period from 2026 to 2033, driven by the accelerating shift of enterprises toward hybrid work models, which is fueling increased investment in unified communication and collaboration platforms. The integration of generative AI technologies is further enhancing employee engagement while streamlining complex administrative tasks. Organizations are placing greater emphasis on delivering seamless digital experiences to attract and retain talent in an increasingly competitive global workforce. Additionally, cloud-native architectures are enabling efficient scalability for distributed teams, while AI-powered productivity tools are supporting faster, data-driven decision-making. Together, these factors are expected to sustain strong demand for secure, scalable, cloud-based digital workplace solutions.

Key Industry Highlights:

- Leading Region: North America is projected to lead, accounting for approximately 37% share in 2026, supported by early technology adoption, a high concentration of software vendors, and advanced digital infrastructure.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest, driven by rapid industrialization, expanding mobile-first workforces, and significant digital transformation initiatives across emerging economies.

- Leading Components: Solutions are expected to lead, accounting for approximately 67% share in 2026, anchored by the massive deployment of collaborative suites and virtual desktop infrastructure.

- Leading Industry Vertical: The BFSI segment is anticipated to lead, holding approximately 24% share in 2026, driven by stringent regulatory compliance needs and the shift toward digital-first banking services.

| Key Insights | Details |

|---|---|

|

Digital Workplace Market Size (2026E) |

US$66.7 Bn |

|

Market Value Forecast (2033F) |

US$259.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

21.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

19.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - AI-Powered Collaboration Enhancing Productivity and Workflow Efficiency

Artificial intelligence capabilities embedded within collaboration platforms analyze behavioral interaction patterns to optimize workflow coordination. These systems interpret communication signals and task dependencies to dynamically guide resource allocation decisions. Enterprises adopt intelligent collaboration environments to reduce administrative overhead across geographically distributed hybrid teams. Predictive analytics engines surface contextual insights that accelerate decision cycles and streamline cross-functional coordination processes. Automated meeting intelligence and content synthesis capabilities improve information retention while minimizing manual documentation burdens. Such productivity improvements strengthen enterprise demand for digitally integrated collaboration ecosystems.

Enterprise software vendors expand artificial intelligence functionality through managed deployment frameworks supporting scalable platform adoption. Natural language processing capabilities automate document generation, conversation summarization, and contextual knowledge retrieval across collaboration channels. These advancements address persistent inefficiencies arising from fragmented communication flows across complex organizational structures. Intelligent automation embedded within collaboration software strengthens workflow continuity and operational transparency across departments. Organizations increasingly evaluate collaboration platforms based on measurable productivity improvements enabled by advanced analytical capabilities. Sustained innovation in artificial intelligence integration, therefore, reinforces structural expansion of enterprise collaboration technology markets.

Generative AI Integration in Collaborative Workflows

The rapid proliferation of generative artificial intelligence is reshaping the functional core of modern digital environments. Automated content generation and intelligent data summarization are significantly reducing the time required for administrative tasks. Organizations are prioritizing tools that offer native AI capabilities to enhance individual and team productivity levels. Unified platforms are expected to incorporate more advanced machine learning models to facilitate real-time decision support. Enhanced conversational interfaces are likely to become the standard method for interacting with complex enterprise datasets. This technological shift is anticipated to drive a substantial increase in long-term enterprise software investments.

Google with Google Workspace is leading this transition by embedding intelligent Gemini assistants into core productivity applications. Microsoft, with Microsoft 365 Copilot, further illustrates the massive shift toward AI-powered document creation and communication management. These innovations are expected to create a robust demand cycle for higher-tier premium subscription service models. Enterprises are projected to accelerate their migration to cloud-based systems to leverage these emerging computational capabilities. ServiceNow Now Assist demonstrates how automated workflows are likely to transform internal employee support services. The convergence of AI and collaboration tools is positioned to define the next phase of market expansion.

Barrier Analysis – Complexity of Legacy Infrastructure Integration

The persistence of outdated legacy systems presents a significant technical barrier to modern digital workplace adoption. Many large organizations struggle with the high costs and risks associated with migrating data from on-premise servers. Incompatibility between modern cloud-native applications and older proprietary software often leads to fragmented user experiences. High initial capital expenditures for infrastructure overhauls can deter smaller enterprises from pursuing full digital transformation. Technical debt accumulated over years of piecemeal IT upgrades continues to limit organizational agility and scalability. These integration challenges are likely to slow the pace of digital workplace deployment in conservative industries.

IBM with IBM Watson Orchestrate attempts to bridge these gaps by automating tasks across disparate legacy and modern systems. However, the fundamental structural differences between old and new architectures often require extensive custom coding and consultancy. Broadcom with VMware Anywhere Workspace seeks to simplify management but faces hurdles in environments with extreme hardware diversity. Such complexities are anticipated to increase the demand for specialized professional services and long-term integration support. Organizations are likely to experience extended implementation timelines when attempting to modernize deeply entrenched legacy workflows. This friction is expected to remain a primary restraint for large-scale digital workplace evolution.

Data Sovereignty Regulations Fragmenting Global Platform Strategies

Regional compliance mandates enforce localized data residency requirements stringently. Multinational enterprises navigate divergent GDPR and CCPA interpretations carefully. Cross-border data flows trigger audit-intensive verification processes. Salesforce with Salesforce Platform encrypts data per jurisdictional specifications. This regulatory mosaic elevates operational costs for global rollouts. Platform providers adapt architectures reactively rather than proactively.

Audit trails and consent management add administrative burdens systematically. Service delivery models require geo-fencing for compliance assurance. These constraints limit seamless multinational deployments significantly. Enterprises prioritize regional customization over universal scalability. The restraint shapes conservative expansion strategies across borders.

Opportunity Analysis – Generative Artificial Intelligence Enabling Personalized Workflow Automation across Enterprise Platforms

Generative artificial intelligence integration enables adaptive digital interfaces that dynamically adjust to evolving enterprise user preferences. Natural language interaction models streamline task execution across complex enterprise software environments and collaboration platforms. Custom intelligent agents address specialized departmental workflows requiring contextual understanding and domain-specific automation. These capabilities reduce manual coordination burdens while improving responsiveness within distributed enterprise communication systems. As conversational interfaces mature, organizations expand adoption beyond messaging toward broader operational productivity use cases. The convergence of automation and language intelligence reshapes expectations for intuitive enterprise software engagement.

Strategic alliances between enterprise software providers and artificial intelligence developers accelerate advanced model optimization. Integrated platforms increasingly embed generative capabilities within workflow orchestration systems governing service management and collaboration. These developments address persistent operational bottlenecks through contextual decision support and automated knowledge synthesis. Enterprise buyers recognize productivity gains from intelligent augmentation layers embedded directly within digital infrastructure. Commercial models increasingly reflect premium positioning for platforms offering advanced automation and contextual assistance capabilities. Expansion opportunities deepen as large language model ecosystems mature and enterprise integration architectures stabilize.

Healthcare Digital Transformation and Telehealth

The healthcare sector is undergoing a rapid digital evolution that requires specialized workplace and collaboration frameworks. Medical professionals are increasingly utilizing secure digital platforms for patient coordination and remote consultations. Integrated digital environments are likely to improve the speed and accuracy of clinical decision-making processes. Ensuring HIPAA compliance and data security remains a top priority for healthcare-focused technology deployments. Virtual training and augmented reality (AR) are expected to play a larger role in medical education and surgical planning. This specialized demand is projected to create a lucrative niche for security-focused digital workplace vendors.

Microsoft, with Microsoft Cloud for Healthcare, integrates collaborative tools with specific clinical workflows and data standards. Google with Google Workspace for Healthcare enables secure communication between doctors, nurses, and administrative staff across different locations. These innovations are likely to reduce administrative burdens and allow practitioners to focus more on direct patient care. Zoom with Zoom for Healthcare provides a reliable platform for high-definition telehealth visits and medical team meetings. The integration of AI-driven diagnostic tools into the digital workplace is anticipated to further revolutionize medical services. This sector is likely to see sustained investment as global healthcare systems modernize their digital cores.

Category–wise Analysis

Component Insights

Solutions as a component is anticipated to lead, accounting for approximately 67% share in 2026, underpinned by the high demand for integrated software platforms. Organizations are prioritizing unified suites that combine messaging, video conferencing, and document management into a single user interface. The transition toward cloud-native architectures is likely to accelerate the replacement of fragmented on-premise legacy tools. Scalable software-as-a-service (SaaS) models are projected to remain the preferred procurement method for modern global enterprises. Microsoft, with Microsoft 365, continues to define the standard for enterprise productivity through its deeply integrated application ecosystem. Google with Google Workspace offers a competitive cloud-first alternative that emphasizes real-time collaboration and cross-platform accessibility. These solution providers are likely to focus on embedding advanced artificial intelligence to maintain their dominant market positions. The shift toward "composable" digital workplaces is anticipated to allow firms to customize their software stacks more effectively.

Services are expected to be the fastest-growing segment, driven by the increasing complexity of cloud migration and system integration. Many organizations lack the internal expertise required to manage the transition from legacy systems to modern digital environments. Specialized consulting and managed services are likely to play a critical role in ensuring successful long-term technology adoption. Professional service providers are projected to offer tailored strategies for cybersecurity, data privacy, and employee experience optimization. Accenture, with its Cloud First services, helps global clients navigate the nuances of large-scale digital workplace transformations. Microsoft, with Microsoft Cloud for Sustainability, provides emissions tracking. These offerings address regulatory reporting requirements proactively. IBM, with IBM Consulting, provides the strategic technical guidance needed to integrate AI-driven workflows into existing corporate structures. This demand for expert-led implementation is anticipated to grow as technologies such as generative AI become more sophisticated. Strategic partnerships between software vendors and service providers are likely to define the competitive landscape for complex enterprise contracts.

Industry Vertical Insights

BFSI is anticipated to lead, holding approximately 24% share in 2026, driven by stringent regulatory compliance needs and the shift toward digital-first banking services. Financial institutions require highly secure digital environments to protect sensitive customer data and ensure operational resilience. Digital workplace tools are projected to enable more efficient remote collaboration between decentralized financial advisory and support teams. Citrix with Citrix DaaS provides the secure application access required by banks to maintain strict data sovereignty standards. Broadcom with VMware Anywhere Workspace helps financial firms manage and secure mobile devices used by employees in the field. This vertical is anticipated to see continued investment in "Zero Trust" security architectures and AI-driven fraud detection. Salesforce with Salesforce Financial Services Cloud embeds industry workflows natively. ServiceNow with ServiceNow for Financial Services automates compliance processes. The digital transformation of banking is likely to remain a primary driver of high-value software demand.

Healthcare is expected to be the fastest-growing segment in the Digital Workplace Market, driven by the technology inflection point in telehealth and remote clinical coordination. Medical providers are increasingly adopting secure digital platforms to manage patient care and facilitate real-time communication between specialists. The integration of electronic health records (EHR) into collaborative digital environments is likely to improve patient outcomes. Epic with Epic MyChart integrates patient-provider communication channels. Cerner with Cerner Millennium supports care team orchestration. Microsoft, with Microsoft Cloud for Healthcare, provides the necessary infrastructure for secure and compliant medical team collaboration. Zoom with Zoom for Healthcare offers a reliable and easy-to-use platform for virtual patient visits and medical education. This sector is anticipated to experience a surge in demand for AI-assisted diagnostics and virtual reality training tools. The move toward more patient-centric and digitally enabled healthcare systems is likely to accelerate software investment.

Regional Insights

North America Digital Workplace Market Trends

North America is expected to remain the leading regional market, accounting for approximately 37% share in 2026, supported by structural dominance and early technology adoption. The region benefits from a high concentration of major software vendors and a robust ecosystem of cloud infrastructure providers. Large-scale enterprise penetration of hybrid work models is projected to sustain consistent demand for unified communication platforms. Advanced cybersecurity mandates and a focus on employee experience are likely to drive high-value premium service subscriptions. Microsoft, with Microsoft 365, and Google, with Google Workspace, maintain a strong presence across corporate and public sectors in this region. This innovation leadership is anticipated to keep North America at the forefront of the global digital workplace evolution.

The U.S. acts as the primary regional anchor, shaping market momentum through significant venture capital flows and enterprise R&D investments. Most leading global vendors are headquartered in the U.S., allowing for rapid feedback loops and local technology pilot programs. The domestic regulatory environment is likely to favor the adoption of AI-driven productivity tools that enhance economic competitiveness. Salesforce with Slack AI is widely utilized by American tech firms to streamline internal communications and project management. Strong investment in 5G and fiber infrastructure is projected to support the seamless delivery of high-bandwidth digital workplace services. The U.S. market is anticipated to focus heavily on the integration of generative AI into standard enterprise workflows.

Asia Pacific Digital Workplace Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as rapid industrialization and manufacturing scaling drive the need for digital connectivity. The region is experiencing a massive shift toward mobile-first workforces, particularly in emerging economies with high smartphone penetration. Infrastructure buildout for high-speed internet is projected to accelerate the adoption of cloud-based collaborative tools among localized vendors. Cost-driven adoption of software-as-a-service models is likely to help regional businesses compete on a global scale. Zoom with Zoom Workplace has seen significant uptake in the region due to its ease of use in diverse network conditions. Asia Pacific is anticipated to become a major hub for digital workplace innovation as local tech ecosystems mature.

India serves as a critical growth anchor for the region, driven by its massive IT services sector and burgeoning startup ecosystem. The country's "Digital India" initiative is likely to further catalyze the adoption of enterprise software across both public and private sectors. Indian firms are projected to increasingly utilize digital workplace tools to manage large-scale remote business process outsourcing operations. ServiceNow with ServiceNow Now Assist is being integrated by major Indian IT firms to automate internal service desk functions. The expansion of domestic data centers is likely to address local data sovereignty concerns and reduce latency for end-users. India is anticipated to see a rapid increase in the number of SMEs adopting standardized digital productivity suites.

Europe Digital Workplace Market Trends

Europe is expected to remain a mature and structurally stable regional market, approximating balanced growth, with demand primarily anchored in compliance-driven platform upgrades. GDPR enforcement elevates privacy-by-design as table stakes. Cross-border operations demand multilingual interface standardization. SAP with SAP SuccessFactors integrates HR workflows seamlessly. Sustainability regulations favor energy-efficient cloud providers. Enterprise replacement cycles sustain steady demand patterns.

Germany serves as the regional anchor through its manufacturing digitalization leadership. Industry 4.0 mandates the integration of collaboration into smart factory ecosystems. Mittelstand firms upgrade legacy systems methodically. Siemens with Siemens MindSphere bridges OT-IT collaboration gaps. Precision engineering cultures emphasize reliability over experimentation. These characteristics define measured expansion dynamics.

Competitive Landscape

The global digital workplace market is moderately consolidated, with leadership concentrated among hyperscale cloud providers and enterprise software incumbents that anchor collaboration and productivity ecosystems. These firms shape procurement standards through expansive application suites, integrated security frameworks, and deeply embedded enterprise workflow platforms. Microsoft, with Microsoft Viva and Microsoft 365, establishes collaboration benchmarks through unified productivity environments reinforced by Copilot-enabled automation layers. Google with Google Workspace strengthens competitive positioning through search-driven productivity tools and scalable cloud-native collaboration infrastructure. Cisco with Webex maintains strategic relevance through telephony interoperability and enterprise-grade communications architecture supporting distributed workforce environments.

Competitive positioning increasingly reflects vertical differentiation driven by artificial intelligence extensibility, workflow orchestration capabilities, and ecosystem integration depth. ServiceNow with the Now Platform strengthens market positioning through workflow orchestration, connecting collaboration, service management, and enterprise automation layers. Salesforce with Einstein GPT extends collaboration capabilities into CRM-adjacent productivity environments, supporting contextual communication across revenue operations. Atlassian with Rovo and Asana with AI Studio illustrate specialization within project-centric collaboration ecosystems targeting high-value productivity workflows.

Key Industry Developments:

- In February 2026, ServiceNow launched "Autonomous Workforce," introducing AI agents capable of resolving IT service desk requests without human intervention. It transitions digital workplaces from "assistive AI" (chatbots) to "agentic AI" that executes end-to-end technical tasks.

- In January 2026, Zscaler completed the acquisition of SquareX, a browser security startup, to bolster secure digital workplace access. This acquisition enhances "zero-trust" security at the browser level, protecting remote employees from web-based threats without requiring traditional VPNs.

- In September 2025, Cisco unveiled "Connected Intelligence" at WebexOne, including plans for a Task Agent and AI Canvas to be generally available by Q1 and Q3 2026. The partnership with NVIDIA to power these agents on RoomOS 26 hardware brings high-performance AI processing directly into physical meeting rooms.

Companies Covered in Digital Workplace Market

- Microsoft Corporation

- Google LLC (Alphabet Inc.)

- Salesforce, Inc. (Slack)

- Cisco Systems, Inc.

- ServiceNow, Inc.

- IBM Corporation

- Broadcom Inc. (VMware)

- SAP SE

- Oracle Corporation

- Zoom Video Communications, Inc.

- Atlassian Corporation

- Workday, Inc.

- Zoho Corporation

- Citrix Systems, Inc. (Cloud Software Group)

- Asana, Inc.

- Monday.com Ltd.

Frequently Asked Questions

The global digital workplace market is projected to be valued at US$66.7 billion in 2026 and is expected to reach US$259.2 billion by 2033, driven by the expansion of hybrid work models, enterprise cloud adoption, and the integration of artificial intelligence into collaboration platforms.

Artificial intelligence embedded within collaboration and productivity platforms enhances workflow automation, meeting intelligence, and knowledge discovery across distributed teams. These capabilities reduce administrative workloads, improve decision-making speed, and enable organizations to manage complex hybrid work environments more efficiently, thereby accelerating enterprise demand for integrated digital workplace ecosystems.

The digital workplace market is forecast to grow at a CAGR of 21.4% from 2026 to 2033, reflecting strong enterprise investment in unified communication platforms, cloud-based collaboration tools, and AI-driven productivity solutions.

North America is the leading regional market, accounting for approximately 37% share, supported by early adoption of enterprise software, strong cloud infrastructure, and the presence of major technology vendors that shape global collaboration and productivity standards.

The digital workplace market is moderately consolidated, with major participants including Microsoft Corporation, Google LLC (Alphabet Inc.), Salesforce, Inc., Cisco Systems, Inc., and ServiceNow, Inc. These companies compete through integrated productivity ecosystems, cloud infrastructure capabilities, and expanding artificial intelligence features embedded within enterprise collaboration platforms.