Wax Market Size, Share, and Growth Forecast 2026 - 2033

Wax Market by Wax Type (Synthetic Wax, Natural Wax, Mineral Wax (Paraffin Wax, Microcrystalline Wax, Ozokerite, Ceresin, Montan Wax, Others)), by Application (Candles, Packaging, Plastics & Rubber, Pharmaceuticals, Cosmetics & Toiletries, Fire Logs, Adhesives, Coating and Sealing, Lubrication, Others), and Regional Analysis, 2026 - 2033

Wax Market Size and Trend Analysis

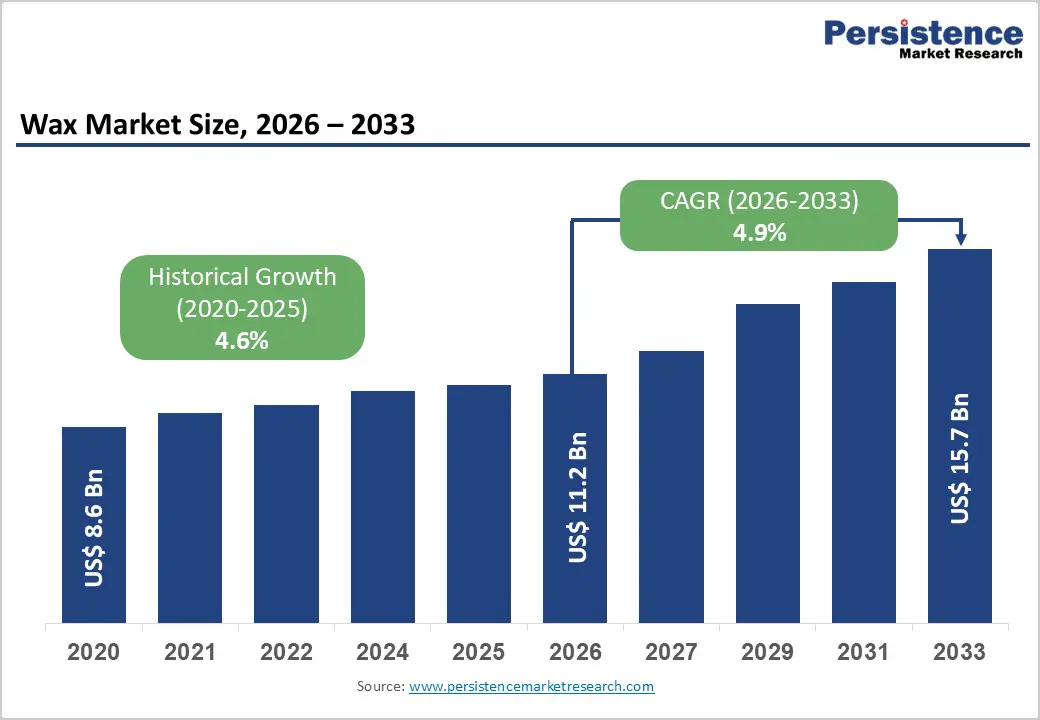

The global Wax Market size is expected to be valued at US$ 11.2 billion in 2026 and projected to reach US$ 15.7 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

This growth is driven by expanding demand across candles, packaging, cosmetics, pharmaceuticals, and plastics processing. Sustainability trends are accelerating the adoption of natural and bio-based waxes, while industrial sectors continue to rely on synthetic and mineral variants for performance applications. The market demonstrated resilience with a 4.6% CAGR during 2020–2025. According to the National Candle Association, over 1 billion pounds of wax are used annually in U.S. candles alone, highlighting strong and diversified end-use demand.

Key Industry Highlights:

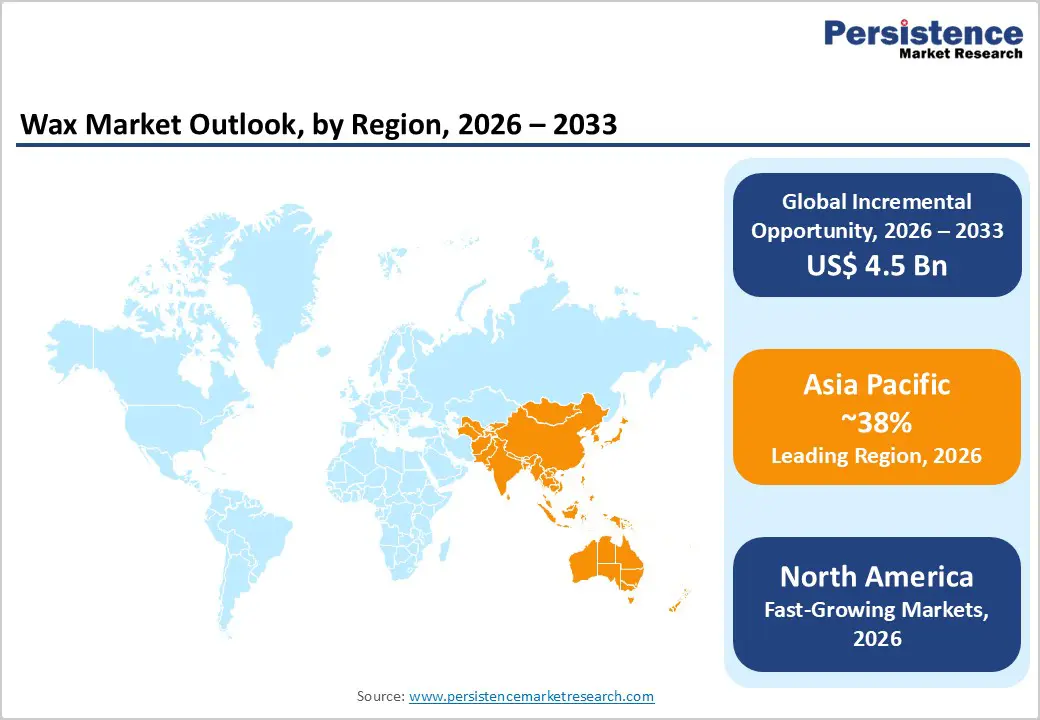

- Leading Region: Asia Pacific leads the global wax market with a 38% share in 2025, driven by China’s production capacity.

- Fastest-Growing Region: North America is the fastest-growing region, supported by sustainable wax adoption, industrial innovation, and expanding candle exports.

- Leading Wax Type: Mineral wax dominates the market with a 52% share in 2025, due to cost-effectiveness and wide availability.

- Fastest-Growing Wax Type: Natural wax is the fastest-growing category, propelled by sustainability trends and rising demand for plant-based alternatives.

- Key Opportunity: Bio-based waxes, especially in EV lubricants and premium candles, present high-growth opportunities globally.

| Key Insights | Details |

|---|---|

|

Wax Market Size (2026E) |

US$ 11.2 billion |

|

Market Value Forecast (2033F) |

US$ 15.7 billion |

|

Projected Growth CAGR(2026-2033) |

4.9% |

|

Historical Market Growth (2020-2025) |

4.6% |

Market Dynamics

Drivers - Rising Consumer Preference for Candles and Home Fragrance Products Driving Large-Scale Wax Consumption

The candle segment remains a primary volume driver for the wax market, supported by rising consumer spending on home décor, aromatherapy, and wellness-oriented products. According to the National Candle Association, U.S. candle production consumes over 1 billion pounds of wax annually, reflecting sustained end-user demand across paraffin, soy, and blended wax formats.

Premiumization trends and product innovation in scented, decorative, and seasonal candles are further stimulating wax utilization. Expanding online retail and cross-border trade, as reflected in trade flows tracked by UN Comtrade, continue to strengthen supply chains and encourage manufacturers to invest in specialty wax formulations for high-margin consumer segments globally.

Expanding Packaging Applications Strengthening Wax Demand for Moisture Barrier and Food Safety Solutions

Growth in global packaging production is significantly increasing demand for wax coatings, particularly in corrugated boxes and food-grade paper applications. Paraffin wax remains widely used for moisture resistance and durability in transit packaging. Data referenced by the Food and Agriculture Organization indicates steady expansion in food and agricultural exports, reinforcing the need for protective packaging materials.

The rise of e-commerce and processed food distribution in Asia Pacific further supports scalable wax consumption. Wax coatings enhance shelf life, prevent contamination, and improve structural strength during shipping. As sustainability standards evolve, manufacturers are also developing recyclable and biodegradable wax-based coatings to align with regulatory and environmental requirements.

Restraints - Volatility in Crude Oil Prices Creating Cost Pressures Across Mineral Wax Supply Chains

Fluctuations in crude oil prices directly impact mineral wax production, particularly paraffin and microcrystalline wax derived from petroleum refining. The International Energy Agency reported significant oil price swings in 2024, creating instability in feedstock costs and compressing margins for refiners and downstream wax manufacturers globally.

Supply adjustments by the OPEC have further contributed to raw material uncertainty, disrupting availability and pricing structures. These shifts increase procurement risks for candle makers, packaging producers, and industrial users, forcing manufacturers to adopt hedging strategies, optimize sourcing, and explore alternative wax blends to maintain profitability.

Tightening Environmental Regulations Increasing Compliance Costs and Limiting Synthetic Wax Usage

Stricter environmental frameworks are placing pressure on certain synthetic wax formulations, particularly those associated with microplastic concerns. The European Chemicals Agency has introduced regulatory measures targeting specific polymer-based additives, compelling producers to reassess formulation strategies and accelerate research into compliant alternatives.

In emerging economies, regulatory oversight is also intensifying. India’s Ministry of Environment, Forest and Climate Change implemented tighter emission and manufacturing controls in 2024, raising compliance costs for domestic processors. These evolving policies increase operational complexity and slow the transition toward scalable bio-based wax alternatives across industrial applications.

Opportunity - Rising Adoption of Bio-Based Waxes Creating Sustainable Growth Pathways Across Consumer and Industrial Applications

Growing environmental awareness and regulatory backing are accelerating the shift toward bio-based waxes, particularly soy wax and other plant-derived alternatives. Expanding soybean cultivation supported by the United States Department of Agriculture ensures scalable raw material availability, strengthening supply stability for candle, packaging, and cosmetic manufacturers worldwide.

Sustainability frameworks such as the European Commission Green Deal are encouraging adoption of renewable and biodegradable materials in consumer goods. Asia-Pacific is witnessing rapid uptake of natural waxes due to rising disposable incomes and eco-conscious purchasing trends, positioning bio-based formulations as a high-growth opportunity through 2033.

Expanding Electric Vehicle and Industrial Lubricant Applications Boosting Demand for High-Performance Synthetic Waxes

The rapid electrification of mobility is creating new opportunities for specialty synthetic waxes in advanced lubricants and thermal management systems. The International Energy Agency projects strong electric vehicle adoption momentum, reinforcing demand for performance-enhancing additives that reduce wear and improve component efficiency.

Technical studies from the SAE International highlight the role of advanced lubricant additives in enhancing durability under high-load conditions. Additionally, supportive new energy vehicle policies in China are stimulating industrial-scale production, further expanding the addressable market for synthetic wax applications in automotive and heavy machinery sectors.

Category-wise Analysis

Wax Type Insights

Mineral wax dominates the global wax market, accounting for an estimated 52% share in 2025, supported by its cost efficiency, large-scale availability, and established refining infrastructure. Paraffin wax remains the most widely produced mineral variant, with production volumes linked closely to petroleum refining output tracked by the U.S. Geological Survey and the American Petroleum Institute. Its functional versatility makes it highly suitable for candles, packaging coatings, and industrial applications, reinforcing its leading position across bulk consumption segments.

Natural wax is emerging as the fastest-growing category, driven by rising demand for biodegradable and plant-based alternatives. Soy, carnauba, and beeswax are increasingly adopted in cosmetics, premium candles, and eco-friendly packaging solutions. Clean-label preferences and sustainability regulations are encouraging manufacturers to diversify portfolios toward renewable wax sources, strengthening long-term growth potential.

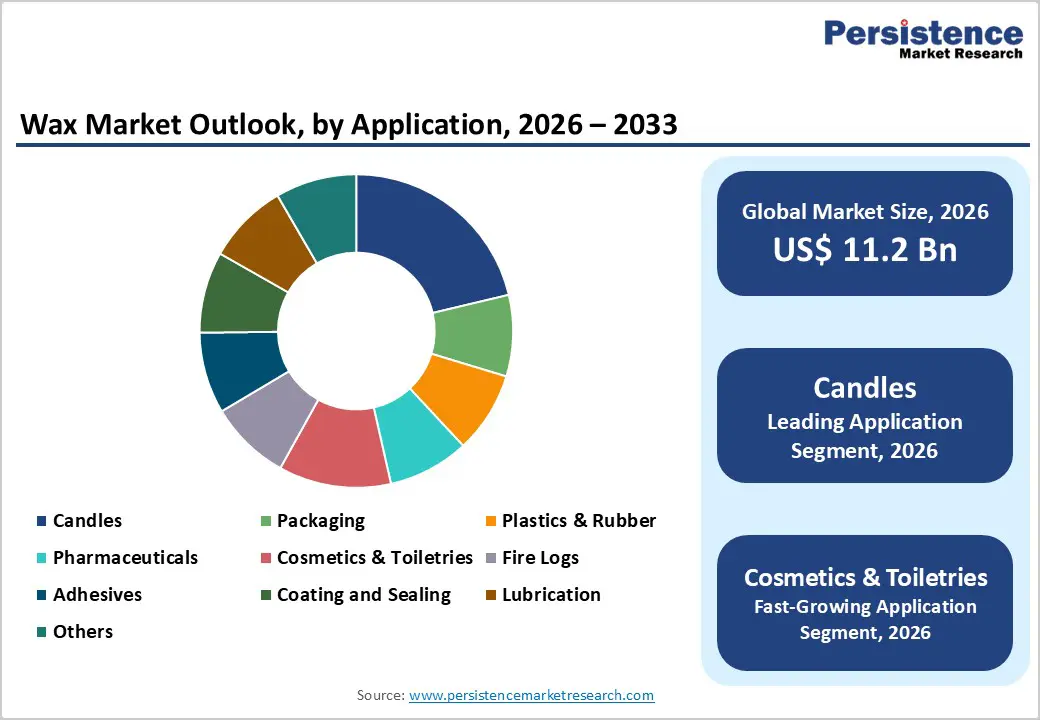

Application Insights

Candles represent the leading application segment, holding approximately 35% share of the wax market in 2025. Strong consumer spending on home décor and wellness products supports sustained demand, particularly in the United States where industry data from the National Candle Association indicates over 1 billion pounds of wax are used annually. Paraffin and soy wax remain preferred due to consistent burn quality, scent retention, and cost-performance balance across mass and premium product lines.

Cosmetics and toiletries are among the fastest-growing application areas, fueled by demand for natural emollients and texture enhancers in personal care formulations. Growth in skincare, lip care, and organic beauty products is accelerating wax usage, particularly plant-derived and specialty synthetic waxes designed for enhanced stability and performance.

Regional Insights

North America Wax Market Trends

North America holds a significant share of the global wax market, with the U.S. leading industrial demand and accounting for approximately 30% of regional wax consumption in 2025. Innovation in product development, along with FDA approvals for food and pharmaceutical packaging, has strengthened the region’s market position. The Environmental Protection Agency is promoting sustainable wax adoption, encouraging soy and bio-based wax usage, while candle exports have grown by roughly 8%, reflecting strong cross-border trade and consumer demand for premium home fragrance products.

Specialty applications in coatings, adhesives, and industrial lubricants are driving incremental growth. Increased awareness of environmental sustainability and regulatory compliance is prompting North American manufacturers to invest in renewable waxes, reformulated blends, and high-performance synthetics, ensuring long-term market resilience across both consumer and industrial sectors.

Europe Wax Market Trends

Europe maintains a well-regulated wax market, harmonized through Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) compliance. Germany and the UK are key importers of specialty waxes such as carnauba, with imports increasing roughly 14%. The European Commission Green Deal is also encouraging the use of sustainable waxes, including montan, across industrial and consumer applications. The region is expected to achieve a CAGR of 5.8% between 2025 and 2032, supported by rising demand for eco-friendly packaging, cosmetics, and premium candles. Regulatory alignment, sustainability incentives, and consumer preference for renewable wax sources continue to drive investment in natural and bio-based wax formulations across Europe.

Asia Pacific Wax Market Trends

Asia Pacific leads the global wax market with a 38% share in 2025, reflecting its dominance in manufacturing and industrial applications. China accounts for 53–60% of regional production capacity, while India and ASEAN countries are growing at approximately 12% annually, supported by increasing packaging, automotive, and candle production. Trade data from UN Comtrade highlights strong export flows and cross-border supply chain integration across the region.

Rapid industrialization and urbanization are driving wax consumption for packaging, plastics, and consumer goods applications. The fastest growth is seen in eco-friendly and natural wax adoption, as manufacturers respond to sustainability trends, renewable raw material availability, and rising middle-class demand for premium and functional wax products.

Competitive Landscape

The global wax market is moderately consolidated, with leading players focusing on vertical integration to secure raw materials and enhance supply chain efficiency. Investment in research and development, particularly in functional and Fischer-Tropsch wax technologies, enables companies to create high-performance and sustainable wax products for industrial and consumer applications. Market participants actively pursue strategic expansions, partnerships, and facility upgrades to strengthen regional presence and meet growing demand. Certifications and compliance with environmental and safety standards are prioritized to maintain market credibility. Innovation in bio-based waxes and specialty formulations remains a key differentiator, driving competitive advantage across product portfolios.

Key Developments:

- In April 2025, Clariant launched Ceridust 1310, a rice-bran-based wax designed for ink applications, offering improved print quality, enhanced dispersibility, and sustainable sourcing to meet growing eco-friendly packaging and printing industry demands.

- In February 2025, Sasol introduced low-carbon Fischer-Tropsch (FT) waxes, achieving a 32% reduction in carbon footprint, targeting environmentally conscious industrial applications while maintaining performance in coatings, adhesives, and specialty manufacturing processes.

- In May 2025, Sasol expanded its HDPE wax production sustainably, focusing on renewable feedstocks and energy-efficient processes to support packaging, plastics, and industrial applications while aligning with global decarbonization and circular economy initiatives.

Companies Covered in Wax Market

- Sinopec Corp

- China National Petroleum Corporation

- HollyFrontier Corporation

- BP P.L.C

- Nippon Seiro Co., Ltd

- Baker Hughes Company

- Exxon Mobil Corporation

- Sasol Limited

- The International Group, Inc.

- Evonik Industries AG

- BASF SE

- Dow

- Honeywell International Inc.

- Royal Dutch Shell P.L.C

- Mitsui Chemicals, Inc.

Frequently Asked Questions

The global wax market is projected to reach US$ 11.2 billion in 2026, supported by steady industrial applications and rising consumer demand across candles, packaging, and cosmetics.

Market demand is primarily driven by the candle segment, with over 1 billion pounds of wax used annually in the U.S., alongside growing applications in packaging and cosmetics.

Asia Pacific leads the market with a 38% share in 2025, driven by China’s large-scale production capacity and increasing industrial and consumer wax consumption.

Natural and bio-based waxes, including soy wax, offer high-growth opportunities, especially in Asia Pacific, supported by sustainability trends and rising demand for eco-friendly products.

The major players in the Wax Market are Sinopec Corp. China National Petroleum Corporation, HollyFrontier Corporation, BP P.L.C, and Nippon Seiro Co., Ltd.