- Specialty & Fine Chemicals

- Microcrystalline Wax Market

Microcrystalline Wax Market Size, Share, and Growth Forecast 2026 - 2033

Microcrystalline Wax Market by Product Type (Flexible and Hard), Product Form (Granule, 15 to 30 micron, Pellets, Slabs, and Bulk liquids), Application (Packaging, Adhesives, Pharmaceuticals, Plastics, Cosmetics, Chewing gum, Rubber, Candles, and Others), and Regional Analysis for 2026 - 2033

Microcrystalline Wax Market Size and Share Analysis

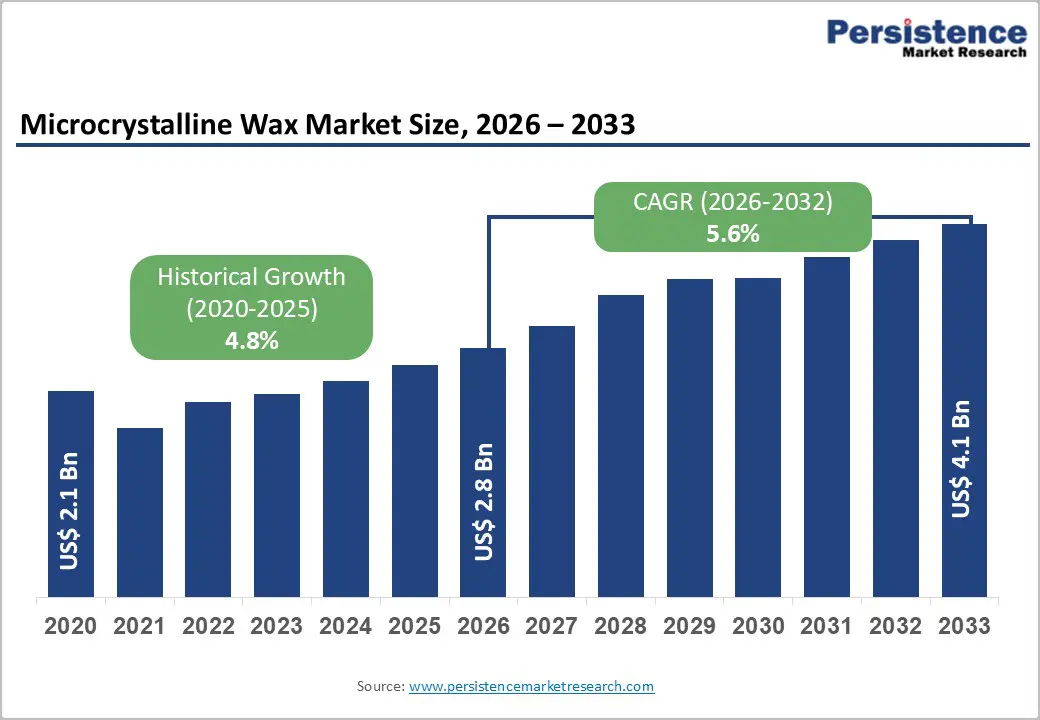

The global microcrystalline wax market size was valued at US$ 2.8 Bn in 2026 and is projected to reach US$ 4.1 Bn by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

This steady expansion is primarily driven by escalating demand from the packaging and cosmetics sectors, where microcrystalline wax serves as a critical moisture barrier and texturizing agent. The pharmaceutical industry's increasing adoption of controlled-release drug formulations further amplifies market growth, supported by regulatory approvals from the FDA and EFSA that validate the material's safety for sensitive applications.

Key Industry Highlights:

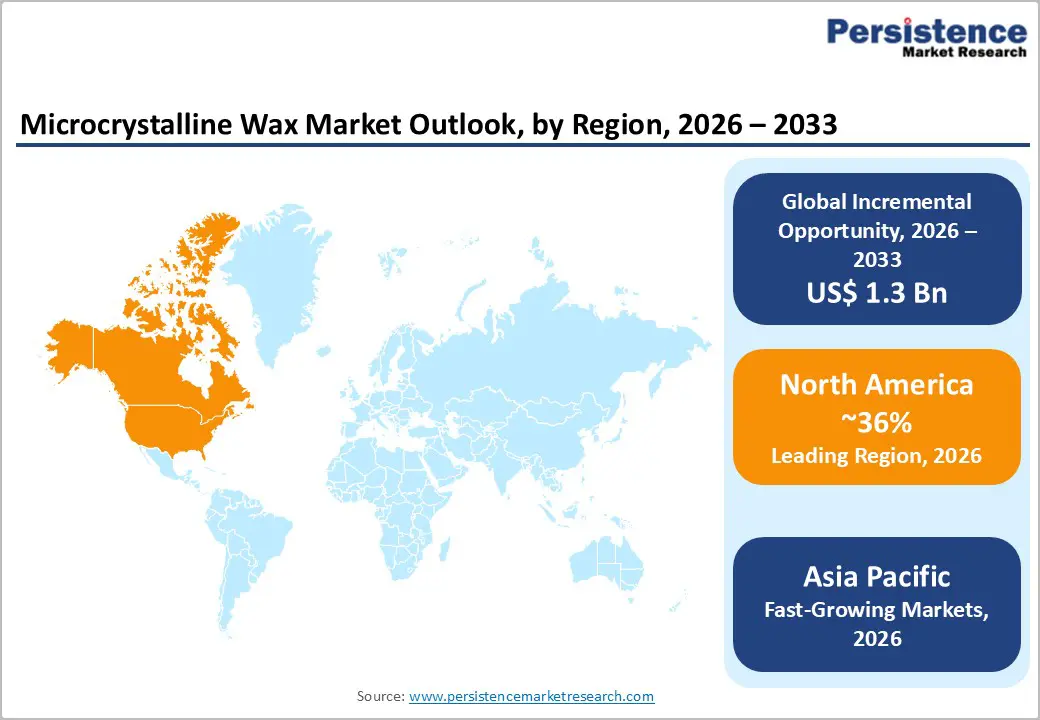

- Leading Region: North America dominates the global microcrystalline wax market with 36% market share, driven by mature cosmetics and pharmaceutical sectors, stringent regulatory compliance standards, and strong demand from hot-melt adhesive manufacturers serving corrugated packaging applications across the region.

- Fastest Growing Region: Asia-Pacific emerges as the fastest-expanding market fueled by India's 800,000 bpd refining capacity expansion, China's dominance in cosmetics manufacturing, and Japan's technological leadership through Nippon Seiro's innovations.

- Dominant Product Type: Flexible microcrystalline wax captures 62% market share within the product type category, driven by superior adhesive and binding properties essential for cosmetics formulations, hot-melt adhesives, and pharmaceutical controlled-release applications serving premium market segments.

- Growing Segment: Adhesives application represents the fastest-growing segment with 5.9% CAGR through 2033, supported by expanding corrugated packaging demand, India's packaging industry growth, and manufacturers' migration from solvent-based to environmentally compliant hot-melt adhesive systems.

- Key Market Opportunity: Bio-based microcrystalline wax development presents substantial growth potential, driven by regulatory mandates and consumer sustainability preferences.

| Key Insights | Details |

|---|---|

| Global Microcrystalline Wax Market Size (2026E) | US$ 2.8 Bn |

| Market Value Forecast (2033F) | US$ 4.1 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.6% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - Growing Demand in Personal Care & Cosmetics Accelerating the Microcrystalline Wax Market

The rising demand for personal care and cosmetics products is a significant driver of the global microcrystalline wax market, as manufacturers increasingly prioritize product performance, texture, and stability. Microcrystalline wax is widely used in formulations such as lip balms, lipsticks, moisturizers, cold creams, ointments, hair pomades, and sunscreens due to its superior binding, thickening, and emollient properties. Unlike paraffin wax, microcrystalline wax has a fine crystalline structure and higher viscosity, enabling it to improve product consistency, enhance spreadability, and deliver a smooth, non-greasy feel that modern consumers prefer.

The global shift toward premiumization in beauty and personal care products has further strengthened demand, as high-end formulations require ingredients that provide enhanced sensory appeal, long-lasting texture, and improved moisture retention. Emerging economies, particularly in Asia-Pacific, Latin America, and the Middle East, are witnessing rapid expansion in personal care consumption driven by urbanization, rising disposable incomes, and exposure to global beauty trends through digital platforms and social media.

Microcrystalline wax also plays a critical role in improving product shelf life and stability under varying climatic conditions, making it particularly valuable for markets with high temperature and humidity fluctuations. The growing demand for multifunctional cosmetic products, such as tinted balms, medicated skincare, and protective formulations, supports the continued use of microcrystalline wax as a reliable formulation aid.

Rising Demand from Industrial Applications & Coatings Driving Steady Demand for Microcrystalline Wax

Microcrystalline wax is widely used in industrial coatings, metal protection, corrosion prevention, adhesives, sealants, polishes, and surface treatment formulations, where durability, flexibility, and adhesion are essential. Its fine crystalline structure and higher molecular weight enable excellent binding properties, making it more effective than conventional paraffin wax in industrial-grade applications. In coatings and surface protection, microcrystalline wax acts as a moisture barrier and protective layer, safeguarding metals, machinery, tools, and components from oxidation, rust, and environmental degradation during storage and transportation.

This is particularly important in industries such as manufacturing, automotive, heavy engineering, and logistics, where equipment longevity and material integrity directly impact operational efficiency and costs. Microcrystalline wax enhances flexibility and toughness in industrial coatings, preventing brittleness and improving resistance to abrasion and mechanical stress. These properties make it ideal for use in protective coatings for pipes, cables, fasteners, and industrial packaging materials.

In adhesives and sealants, it improves viscosity control, tackiness, and cohesion, contributing to better bonding strength and application stability. The expansion of global manufacturing activities, infrastructure development, and industrial automation, particularly in emerging economies, has increased demand for advanced protective materials. Ongoing formulation innovations in industrial coatings are increasing reliance on microcrystalline wax for specialized and high-value applications, reinforcing its role as a critical input material in the industrial sector.

Restraints - Crude Oil Price Volatility and Raw Material Constraints Are Creating Supply Uncertainty

Crude oil price volatility remains a critical restraint for the global microcrystalline wax market, as the material is derived directly from petroleum refining processes. Fluctuations in global crude oil prices, driven by geopolitical tensions, supply-demand imbalances, production cuts by oil-exporting nations, and changes in energy policies, directly influence the availability and cost of microcrystalline wax. When crude oil prices rise sharply, refiners often prioritize fuel production over specialty byproducts, leading to constrained wax output and reduced supply consistency.

In addition to pricing instability, raw material constraints arise from the declining number of refineries equipped to produce high-quality microcrystalline wax. Many refineries are upgrading or reconfiguring units to meet stricter environmental standards or shifting toward lighter crude processing, which limits the yield of heavy residual fractions required for wax extraction. This structural shift reduces global supply flexibility and increases dependence on the limited number of producers. As a result, end-use industries face unpredictable lead times, fluctuating procurement costs, and supply disruptions.

Regulatory Complexity for Bio-based Alternatives Slowing Market Transition and Investment Clarity

Regulatory complexity surrounding bio-based alternatives presents a nuanced restraint for the global microcrystalline wax market, particularly as sustainability pressures intensify. While demand for renewable and eco-friendly wax substitutes is growing, the regulatory landscape governing bio-based materials is often fragmented, inconsistent, and evolving across regions.

Different countries impose varying standards for certification, biodegradability, sourcing transparency, and carbon footprint assessment, making compliance complex and costly for manufacturers seeking to transition away from petroleum-derived waxes. This lack of harmonization slows the commercial scalability of bio-based alternatives and creates uncertainty for end users.

For microcrystalline wax producers and downstream formulators, this regulatory ambiguity complicates strategic decision-making. Companies face challenges in reformulating products or investing in alternative wax technologies without clear, long-term regulatory guidance. In personal care and packaging applications, for instance, regulatory approvals for bio-based inputs can be time-consuming, involving extensive testing for safety, stability, and performance equivalence. Smaller manufacturers may lack the resources to navigate multi-regional compliance frameworks, discouraging rapid adoption of substitutes.

Opportunities - Development of Specialty and High-Purity Wax Grades Unlocks Value-Added Market Potential

The development of specialty and high-purity microcrystalline wax grades represents a significant opportunity for market participants to move beyond commodity-driven competition and capture higher margins. End-use industries such as cosmetics, pharmaceuticals, food packaging, and specialty adhesives increasingly require waxes with precise melting points, controlled viscosity, low oil content, minimal odor, and high chemical stability. By investing in advanced refining, filtration, and de-oiling technologies, manufacturers can deliver consistent, application-specific wax grades that meet stringent quality and safety standards.

This opportunity is further strengthened by the trend toward premiumization across consumer and industrial products, where formulation performance and aesthetic quality are critical differentiators. High-purity wax grades improve texture, binding efficiency, shelf stability, and resistance to temperature fluctuations, making them ideal for high-end formulations. Specialty waxes enable manufacturers to customize solutions for niche applications such as pressure-sensitive adhesives, protective coatings, and high-performance rubber compounds.

Growth of Pharmaceutical and Medical Applications Is Creating Long-Term Demand Stability

The expansion of pharmaceutical and medical applications presents a robust and relatively stable growth opportunity for the microcrystalline wax market. Microcrystalline wax is widely used in ointment bases, topical creams, tablet coatings, and controlled-release drug formulations due to its chemical inertness, non-toxicity, and excellent binding properties. As global healthcare spending continues to rise, driven by aging populations, increasing prevalence of chronic diseases, and improved access to medical care in emerging economies, demand for pharmaceutical-grade excipients is growing steadily.

In medical packaging and device protection, microcrystalline wax is used for moisture barriers, surface protection, and corrosion resistance, ensuring product integrity during storage and transportation. The opportunity is amplified by stricter regulatory requirements for drug stability, safety, and shelf life, which favor reliable and well-characterized excipients.

Manufacturers capable of producing pharmacopeia-compliant, high-purity wax grades can benefit from long-term supply contracts and lower demand cyclicality compared to industrial applications. As pharmaceutical innovation advances and topical and transdermal drug delivery systems gain traction, microcrystalline wax is expected to play an increasingly important role, reinforcing its growth potential within the medical and healthcare sector.

Category-wise Analysis

Product Type Insights

The hard microcrystalline wax segment dominates the market, commanding approximately 62% market share due to its superior performance in high-temperature applications and structural stability requirements. Hard grades exhibit needle penetration values of 25-30 dmm at 25°C and solidification points ranging from 70°C to 90°C, making them ideal for precision applications in pharmaceutical tablet coatings and premium candle manufacturing. The U.S. Pharmacopeia (USP) specifies hard microcrystalline wax for oral dosage forms, where controlled hardness ensures consistent drug release profiles.

In the packaging sector, hard grades provide exceptional dimensional stability for laminated structures, reducing deformation during storage and transportation. Production data from major refiners indicates that Sasol and Calumet Specialty Products allocate 65-70% of their microcrystalline wax capacity to hard grades, reflecting strong downstream demand.

The segment's growth is further bolstered by its use in chewing gum base formulations, where FDA 21 CFR 172.886 approval enables food-grade applications. Hard microcrystalline wax's ability to enhance oil binding capacity by 40-60% compared to flexible grades makes it indispensable in cosmetic stick formulations, contributing to segment leadership.

Product Form Analysis

Granule form represents the leading segment, capturing approximately 45% of the market share due to its superior handling characteristics and processing efficiency in automated manufacturing systems. Granules offer uniform melting behavior and precise metering capabilities, critical for hot-melt adhesive formulations used in high-speed packaging lines.

The Packaging Machinery Manufacturers Institute (PMMI) reports that 78% of modern adhesive applicators are optimized for granule feed systems, driving standardization across the industry. Granules also exhibit reduced dust generation compared to powdered alternatives, improving workplace safety and reducing explosion hazards in compliance with OSHA combustible dust regulations.

Major producers, including Indian Oil Corporation Ltd and Nippon Seiro Co., Ltd, have expanded granule production capacity by 15% since 2023 to meet growing demand from the Asia Pacific region. The form's popularity extends to pharmaceutical processing, where granule uniformity ensures consistent batch-to-batch quality in tablet coating applications. Bulk density optimization in granule form reduces transportation costs by 12-15% compared to slab forms, providing economic advantages for large-scale industrial users while maintaining the material's intrinsic performance characteristics.

Application Analysis

The packaging application segment leads the microcrystalline wax market, accounting for approximately 38% of total consumption, driven by the material's exceptional moisture barrier properties and regulatory approvals for food contact. FDA 21 CFR 178.3710 explicitly permits microcrystalline wax as a component of food-contact coatings, enabling its use in direct food packaging applications.

The segment's dominance is reinforced by e-commerce growth, which has increased demand for protective packaging by 23% annually since 2021. Microcrystalline wax coatings represent 10-25% of the weight of coated paperboard, providing critical water resistance while maintaining recyclability.

European Committee for Standardization (CEN) guidelines for sustainable packaging recognize microcrystalline wax as compatible with paper recycling streams when used at concentrations below 5% by weight. Major fast-moving consumer goods companies have adopted microcrystalline wax laminates for 90% of their moisture-sensitive product lines, including dry foods and pharmaceuticals. The segment's growth trajectory is further supported by innovations in active packaging, where microcrystalline wax serves as a carrier for antimicrobial agents, extending product shelf life by 25-40% in challenging supply chain conditions.

Regional Insights

North America Microcrystalline Wax Market Trends

North America commands the largest microcrystalline wax market share, representing approximately 36% of global consumption, anchored by the United States' advanced manufacturing infrastructure and stringent quality standards. The U.S. Energy Information Administration reports that domestic wax production reached 2,159 thousand barrels in 2024, ensuring a stable supply for downstream industries.

The region's packaging sector, valued at $200 Bn, extensively utilizes microcrystalline wax in moisture-barrier coatings for food and pharmaceutical applications. FDA regulatory clarity under 21 CFR 178.3710 and 21 CFR 172.886 provides manufacturers with compliance confidence, accelerating product development cycles.

Recent capacity expansions by Calumet Specialty Products Partners and HollyFrontier Refining have increased regional production by 8% since 2023. The cosmetics industry's shift toward premium, long-wearing formulations has boosted microcrystalline wax demand by 7.5% annually, particularly in color cosmetics and skincare segments. Canada's robust regulatory framework, aligned with U.S. EPA and FDA standards, facilitates cross-border trade, while Mexico's growing manufacturing base presents emerging opportunities for wax suppliers serving the North American supply chain.

Europe Microcrystalline Wax Market Trends

Europe represents approximately 28% of the global microcrystalline wax market, characterized by stringent regulatory harmonization and sustainability-driven innovation. The European Chemicals Agency (ECHA) enforces REACH compliance across the supply chain, with registration costs for new wax formulations exceeding €50,000 per substance. Germany, France, and the U.K. collectively account for 65% of regional demand, driven by advanced pharmaceutical and cosmetics manufacturing. The EU's Packaging and Packaging Waste Regulation (PPWR) mandates recyclable packaging by 2030, prompting reformulation with microcrystalline wax to enhance material separability.

European Food Safety Authority (EFSA) approval of microcrystalline wax as food additive E905 supports its use in direct food contact applications, with certified volumes growing 6.8% annually. The region's commitment to circular economy principles has spurred development of bio-based microcrystalline wax alternatives, with Sasol and Paramelt investing €20 million in sustainable wax research since 2023. Regulatory convergence through CEN standards ensures consistent quality specifications across member states, while the German Federal Institute for Risk Assessment (BfR) provides additional safety guidance for food-contact applications.

Asia Pacific Microcrystalline Wax Trends

Asia Pacific emerges as the fastest-growing microcrystalline wax market, expanding at a 6.2% CAGR and capturing 25% of global consumption, powered by rapid industrialization and expanding manufacturing capabilities. China leads regional production and consumption, with its packaging industry growing 22% annually and driving microcrystalline wax demand in moisture-barrier applications.

India's packaging sector, expanding at 25% per year according to the Packaging Industry Association of India, presents significant growth opportunities, particularly in food-grade applications compliant with FSSAI regulations. Japan's advanced cosmetics industry, valued at $35 Bn, utilizes high-purity microcrystalline wax for premium skincare formulations, with Nippon Seiro Co., Ltd commanding 40% domestic market share.

Competitive Landscape

The global microcrystalline wax market exhibits a moderately consolidated structure, characterized by the presence of major integrated petroleum producers controlling approximately 60% - 65% of global supply, alongside a fragmented tier of regional blenders and specialty producers capturing niche segments. Sasol, Sonneborn (subsidiary of HollyFrontier), CEPSA, and Sinopec dominate through captive refining capacity and established distribution networks spanning cosmetics, pharmaceuticals, and industrial adhesive manufacturers.

Market concentration is reinforced by significant capital barriers to entry, including refinery infrastructure, de-oiling technology, and regulatory certifications that limit new-entrant competition. Consolidation trends are evident through strategic acquisitions, such as HollyFrontier's integration of Sonneborn's specialty wax portfolio, aimed at expanding geographic reach and application breadth.

Smaller independent blenders such as Kerax Limited (UK) and Paramelt (Netherlands) pursue differentiation through product customization, regional proximity to customers, and sustainability initiatives rather than competing on commodity pricing. Emerging producers in India and Southeast Asia are progressively upgrading manufacturing capabilities, leveraging lower labor costs and proximity to rapidly expanding cosmetics and pharmaceutical markets. Research and development investments are concentrated among market leaders, with emphasis on bio-based wax alternatives, improved thermal stability grades, and regulatory compliance formulations driving competitive positioning.

Key Developments:

- In January 2025, Nippon Seiro Co., Ltd. announced commercialization of rice-based microcrystalline wax derived from rice bran waste, targeting 30% cost reduction by 2027 compared to petroleum-derived variants, and expanding production capacity by 15,000 metric tons annually to serve Asian cosmetics manufacturers seeking sustainable alternatives.

- In October 2024, CEPSA expanded its CERASURâ„¢ microcrystalline wax production line in Spain with US$ 45 Mn investment, increasing capacity by 12% and targeting pharmaceutical-grade formulations to meet accelerating demand from European drug delivery companies under ICH Q12 harmonization frameworks.

- In August 2024, Indian Oil Corporation Ltd. initiated research partnerships with Indian Institute of Technology to develop algae-derived microcrystalline wax prototypes, aiming to commence pilot-scale production by 2026 for export to Southeast Asian cosmetics manufacturers.

Companies Covered in Microcrystalline Wax Market

- Indian Oil Corporation Ltd

- Calumet Specialty Products Partners, L.P.

- Sonneborn LLC

- Koster Keunen

- Kerax Limited

- The International Group, Inc

- Asian Oil Company

- CEPSA

- Nippon Seiro Co., Ltd.

- Sasol

- MOL Group

- HollyFrontier Refining & Marketing LLC

- Paramelt

- Alfa Chemical Ltd

- Alpha Wax

Frequently Asked Questions

The global microcrystalline wax market was valued at US$ 2.8 Bn in 2026 and is projected to reach US$ 4.1 Bn by 2033, representing a compound annual growth rate of 5.6%, driven by escalating demand from cosmetics, pharmaceuticals, and hot-melt adhesive applications across developed and emerging markets worldwide.

The market is primarily driven by increasing demand from the cosmetics and personal care industry, where skincare products account for 42% of total cosmetics consumption, the surge in hot-melt adhesive applications for corrugated packaging driven by e-commerce growth, and pharmaceutical sector adoption for controlled-release tablet formulations and biocompatible binders meeting FDA and EMA regulatory standards.

Flexible microcrystalline wax dominates with 62% market share due to its superior adhesive properties, fine crystal structure, and branched hydrocarbon composition enabling superior flexibility and emulsion stability essential for premium cosmetics formulations, hot-melt adhesive systems, and pharmaceutical controlled-release applications serving high-margin market segments.

North America commands the largest market share at 36%, supported by mature cosmetics manufacturing infrastructure, stringent FDA regulatory compliance standards driving product quality premiums, robust adhesive and packaging industries, and advanced research and development ecosystems fostering innovation in sustainable formulations and specialty applications.

Bio-based microcrystalline wax development presents the most substantial opportunity, with rice-based, soy-derived, and algae-based alternatives commanding price premiums of 15% to 25% and projected to capture 8% to 12% of market volume by 2033, driven by regulatory mandates for sustainability and rising consumer demand for eco-friendly cosmetics and packaging solutions.

Major market leaders include Sasol (South Africa), Sonneborn LLC (USA, subsidiary of HollyFrontier), Indian Oil Corporation Ltd. (India), CEPSA (Spain), Nippon Seiro Co., Ltd. (Japan with 70% domestic market share), Sinopec (China), Calumet Specialty Products (North America), and regional specialists including Kerax Limited (UK) and Paramelt (Netherlands).