- Industrial Machinery

- Vapour Recovery Units Market

Vapour Recovery Units Market Size, Share, and Growth Forecast 2025 - 2032

Vapour Recovery Units Market Analysis by Technology (Adsorption, Condensation, Absorption), Application (Processing, Storage, Transportation), End-user (Oil & Gas), and Regional Analysis 2025 - 2032

Vapour Recovery Units Market Share and Trends Analysis

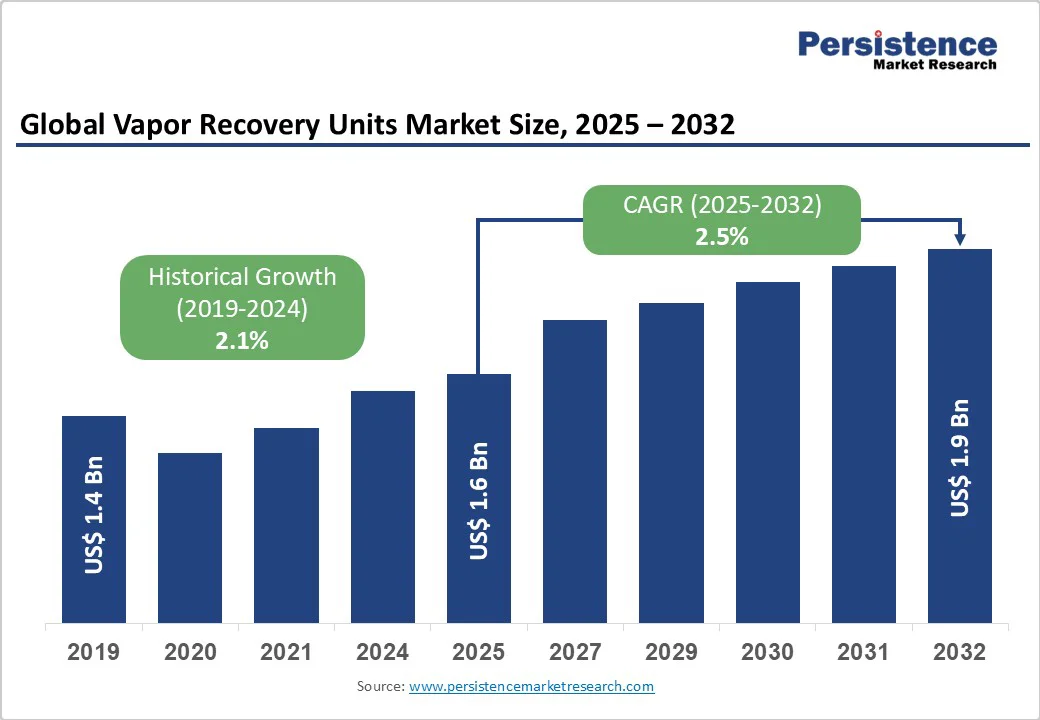

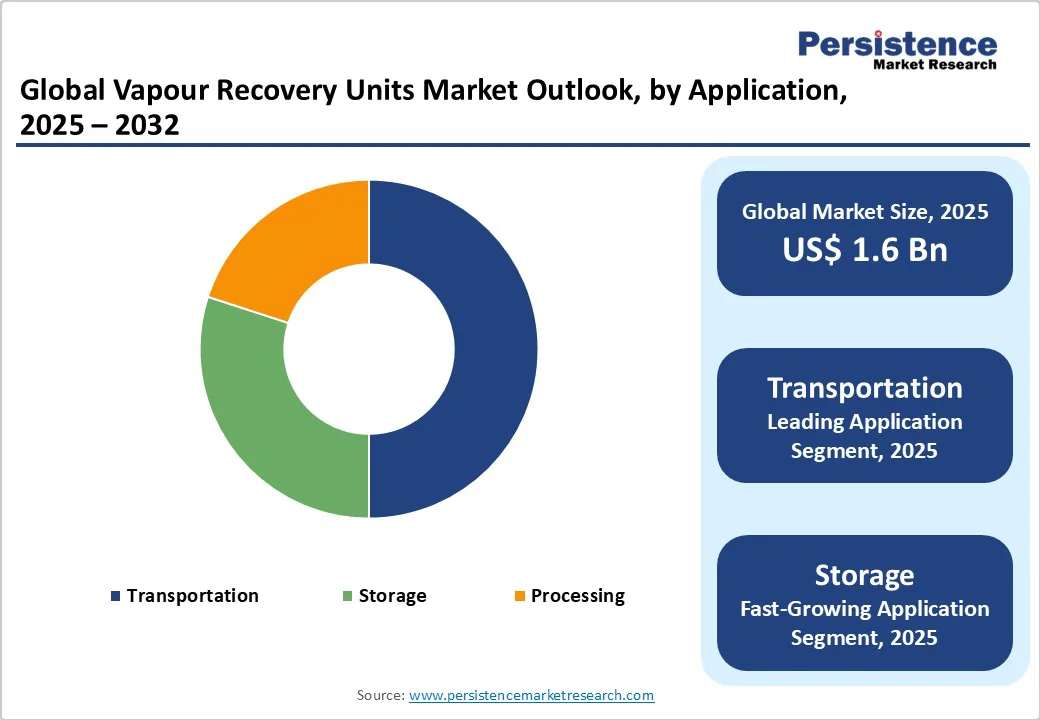

The global vapour recovery units market size is likely to value US$1.6 Bn in 2025 and is projected to reach US$1.9 Bn by 2032, growing at a CAGR of 2.5% between 2025 and 2032.

Stringent environmental regulations worldwide drive market expansion as governments enforce stricter controls on volatile organic compound emissions. The Environmental Protection Agency requires operators to eliminate at least 95% of vapors from hydrocarbon storage units under New Source Performance Standard 40 CFR Part 60 Subpart OOOO.

Key Market highlights:

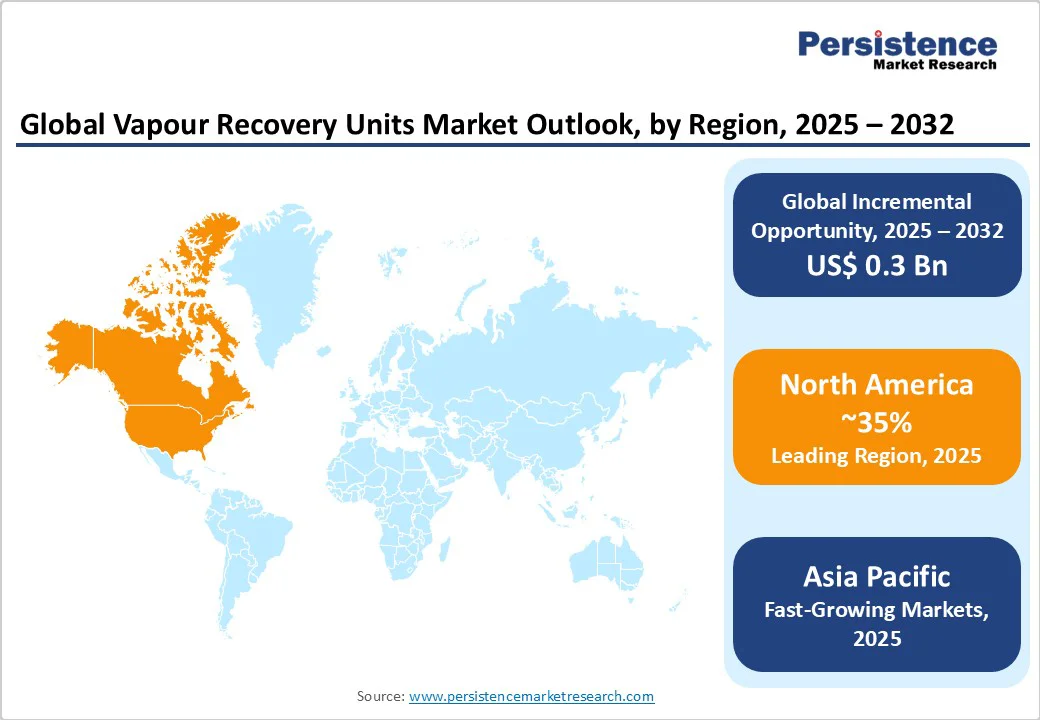

- Leading Region: North America leads globally through EPA regulatory frameworks requiring 95% vapor recovery efficiency, supported by over 18 million barrels per day refining capacity and comprehensive emission control infrastructure, driving sustained market dominance.

- Fastest-Growing Region: The Asia Pacific emerges as the fastest-growing region, propelled by China's Air Pollution Prevention and Control Action Plan and India's refining expansions, which target an additional 2 million barrels per day, creating policy-driven acceleration of adoption.

- Leading End-User Segment: The oil and gas end-user segment dominates with a 60% market share, driven by essential emission management in upstream and downstream operations, as supported by IEA reports indicating that 15% of energy-related emissions require comprehensive vapor recovery solutions.

- Leading Technology: Adsorption technology represents the fastest-growing segment, achieving 95% recovery efficiency through activated carbon systems, driven by EPA regulations and technological innovations that enable superior volatile organic compound capture performance.

- Key opportunity: The Asia Pacific’s policy-driven expansion, where regulatory mandates and infrastructure investments create demand for scalable vapor recovery solutions targeting the transportation and storage segments, with substantial long-term revenue potential.

| Key Insights | Details |

|---|---|

| Vapour Recovery Units Market Size (2025E) | US$1.6 Bn |

| Market Value Forecast (2032F) | US$1.9 Bn |

| Projected Growth CAGR (2025-2032) | 2.5% |

| Historical Market Growth (2019-2024) | 2.1% |

Market Dynamics

Market Growth Driver - Rise in Regulatory Enforcement on Emission Controls

Government mandates worldwide are increasingly driving the adoption of vapor recovery technologies. In the United States, the Environmental Protection Agency’s (EPA) updated regulations NESHAP Subpart R and NSPS Subpart XXa require new bulk gasoline terminals and storage facilities to maintain total organic compound (TOC) emissions below 550 ppm in vent streams.

These rules enforce strict monitoring, often through Continuous Emissions Monitoring Systems (CEMS), and compel operators to install and maintain advanced vapor recovery units (VRUs) to ensure compliance. Failure to meet these standards can result in significant penalties, incentivizing investments in emission control infrastructure.

The European Union’s Industrial Emissions Directive mandates Stage I and Stage II petrol vapor recovery systems at service stations with annual throughput exceeding 500,000 liters, requiring a minimum 85% vapor capture efficiency.

This regulatory landscape forces oil and gas operators to upgrade existing facilities and integrate emission control technologies. Combined with U.S. compliance requirements, these mandates create sustained demand for VRU systems, fueling market growth as refiners and distributors implement mandatory emission reduction measures to meet global environmental standards.

Rising Global Energy Production and Processing Activities

The expansion of oil and gas production, particularly in emerging markets, is driving strong demand for vapor recovery units (VRUs). Operators are increasingly focused on capturing valuable hydrocarbons while adhering to stringent environmental regulations.

The International Energy Agency (IEA) forecasts continued global oil demand growth, with Asia-Pacific countries such as Indonesia planning to expand their refining capacity by up to 2 million barrels per day. This expansion increases the need for advanced vapor recovery solutions across storage, transportation, and processing facilities to prevent emissions and optimize hydrocarbon recovery.

In China, the Air Pollution Prevention and Control Action Plan mandates the implementation of vapor recovery systems at petrol stations, storage tanks, and transport vehicles within specific deadlines. These regulations, coupled with growing production, present significant opportunities for VRU adoption across upstream, midstream, and downstream operations.

Additionally, the evolution of the automotive fuel system market toward cleaner fuel handling standards further reinforces the demand for advanced emission control technologies during processing, storage, and distribution phases, driving sustained market growth.

Restraints - High Capital Investment Requirements

Vapor recovery unit (VRU) installations require significant upfront investments, often running into millions of dollars for large-scale facilities. According to U.S. EPA cost assessments, the expenditure includes not only the purchase of the equipment but also site preparation, integration with existing systems, and compliance with environmental standards. These costs can be prohibitively high for small and mid-sized operators, especially in developing regions where financing options are limited.

The challenge is further compounded by the need for specialized components such as activated carbon systems, vacuum pumps, and condensers, which increase both procurement and maintenance expenses. Beyond initial capital, operators face recurring costs related to skilled labor, inspections, and periodic component replacement. For cost-sensitive players, particularly those with low-throughput operations, the long payback period reduces the incentive for adoption, making capital intensity one of the most significant restraints for the vapor recovery unit market.

Technical Integration Challenges

Integrating vapor recovery systems with legacy infrastructure presents significant technical challenges, necessitating specialized engineering and potentially requiring facility modifications that increase project complexity. Many storage and distribution facilities operate on legacy designs that were not initially intended to accommodate advanced emission control technologies. Retrofitting such sites requires substantial engineering modifications, careful calibration, and the use of specialized equipment to ensure compatibility.

System performance relies heavily on accurate monitoring and adjustment, and regulatory frameworks, such as EPA mandates for Continuous Emissions Monitoring Systems (CEMS) in bulk gasoline terminals, further raise technical requirements. This adds to both the installation time and the need for highly skilled personnel to operate and maintain the systems.

Frequent calibration, troubleshooting, and adherence to strict performance standards make these systems technically demanding. As a result, operators lacking engineering expertise or sufficient technical resources may hesitate to invest, slowing down the adoption rate of vapor recovery units in certain markets.

Opportunities - Advancements in Smart Vapor Recovery Technologies

The vapor recovery market is undergoing a rapid transformation driven by digitalization and the integration of smart technology. Companies are increasingly adopting IoT-enabled monitoring systems and automated control solutions to enhance operational efficiency.

For example, integrated automated control systems can monitor flow rates, pressure, and emissions in real-time, ensuring consistent performance while minimizing the need for human intervention. Regulatory mandates, such as the EPA’s requirement for continuous emissions monitoring systems (CEMS) at bulk gasoline terminals, further accelerate demand for these smart solutions, as operators seek real-time emission data and predictive maintenance capabilities.

Hybrid vapor recovery systems that combine different technologies, such as vacuum-assisted condensers with carbon adsorption, enable optimized performance, reduced emissions, and lower operational costs. These advancements align with circular economy principles, allowing captured vapors to be reused as valuable by-products rather than being released as waste, thereby creating both environmental and economic benefits for operators.

Expansion in Asia Pacific Through Policy-Driven Demand

The Asia Pacific region presents immense growth potential for vapor recovery systems, driven by stringent environmental regulations and rapid industrial expansion. In China, the Air Pollution Prevention and Control Action Plan mandates the full implementation of vapor recovery systems across petrol stations, storage tanks, and transport infrastructure, establishing a clear compliance timeline. The European Union’s Stage II Petrol Vapor Recovery Directive serves as a benchmark for emerging markets adopting similar standards, requiring a minimum of 85% vapor capture efficiency.

India’s expanding refining capacity, coupled with infrastructure projects across ASEAN nations such as Singapore’s 37 million TEU container handling capability, further boosts market demand. Government incentives supporting emission reduction technologies, along with cost advantages in local manufacturing, provide companies with opportunities to deploy scalable solutions. Collectively, these factors drive adoption in transportation, storage, and distribution sectors, creating long-term revenue streams and solidifying the region as a key growth market for vapor recovery technologies.

Category-wise Insights

Technology Analysis

The adsorption segment dominates the vapor recovery market, capturing approximately 40% share due to its high efficiency in volatile organic compound (VOC) removal. Activated carbon-based systems can achieve recovery rates exceeding 95%, in line with Environmental Protection Agency (EPA) standards. These systems are particularly effective across diverse operational conditions, making them a preferred choice for large-scale storage and distribution facilities.

John Zink Hamworthy has advanced this technology by integrating proprietary sizing methods with activated carbon adsorption, optimizing both capital and operational expenditure. The technology’s widespread adoption is driven by cost-effectiveness, adaptability to varying gas compositions, and proven reliability in high-volume operations where consistent emission control is critical for regulatory compliance and maintaining operational efficiency.

Application Analysis

The transportation segment accounts for roughly 50% of the market, underscoring the critical need for emission management during fuel loading and unloading at terminals and distribution centers. Regulatory frameworks, including EPA mandates, require vapor recovery systems to achieve up to 95% reduction in emissions during these activities.

High-volume fuel transfers across global logistics networks reinforce the segment’s importance. Compliance with International Maritime Organization (IMO) standards, along with safety and operational protocols, ensures that transportation-related vapor recovery systems reduce both emissions and product loss, making them indispensable for modern fuel handling infrastructure.

End User Analysis

The oil and gas sector accounts for approximately 60% of the vapor recovery market, due to its extensive upstream and downstream operations that necessitate comprehensive emission control solutions. Programs such as the EPA’s Natural Gas STAR initiative further encourage the adoption of vapor recovery units to capture methane emissions from storage tanks and low-pressure vents.

The scale of operations and stringent regulatory requirements also drives the sector’s dominance. According to the International Energy Agency, oil and gas activities contribute about 15% of total energy-related greenhouse gas emissions, creating sustained demand for VRUs that not only ensure environmental compliance but also enhance operational efficiency and resource recovery across production and distribution networks.

Regional Insights

North America Vapour Recovery Units Trends

North America maintains market leadership through robust regulatory frameworks, particularly in the United States, where the Environmental Protection Agency enforces comprehensive emission standards under NESHAP and NSPS regulations, which require 95% vapor recovery efficiency.

The region's innovation ecosystem supports advanced technologies, with companies like John Zink Hamworthy developing integrated automated control systems and proprietary sizing methods that optimize system performance for diverse applications.

The EPA's updated regulations require new bulk gasoline terminals to install Continuous Emissions Monitoring Systems (CEMS) while maintaining total organic compound levels below 550 ppm, driving technology upgrades across existing facilities.

Integration with the U.S. Downstream Oil and Gas Market creates synergies as refiners modernize emission control infrastructure to meet federal standards, fostering regional leadership in vapor recovery technology development and deployment.

Europe Vapour Recovery Units Trends

Europe demonstrates steady market performance through regulatory harmonization under the European Union's Industrial Emissions Directive, which mandates the installation of Stage I and Stage II petrol vapor recovery systems across member states. Germany, the U.K., France, and Spain lead regional adoption through coordinated emission standards, with the EU requiring 85% vapor capture efficiency at service stations handling over 500,000 litres annually.

The European Environment Agency's statistics show a 20% reduction in emissions in the petrochemical sector through harmonized vapor recovery policies, while Germany focuses on advanced membrane technologies for refinery applications.

France and Spain emphasize transportation sector applications, with the U.K. investing in storage innovations to support net-zero commitments, creating regional market resilience through diversified technological approaches and cross-border regulatory consistency.

Asia Pacific Vapour Recovery Units Trends

The Asia Pacific region exhibits dynamic growth, driven by stringent air quality campaigns and rapid industrial expansion. China's Air Pollution Prevention and Control Action Plan mandates comprehensive oil and gas vapor recovery across petrol stations, storage tanks, and transport vehicles. Japan's Air Pollution Control Act and India's emission standards support the adoption of technology, as refining expansions target an additional 2 million barrels per day in countries like Indonesia.

Manufacturing advantages enable the cost-effective production of vapor recovery units, while ASEAN infrastructure investments, including Singapore's 37 million TEU container handling capacity, drive demand in the transportation segment. China leads technological adoption alongside Japan's precision engineering expertise. At the same time, India's rising energy demand and regional infrastructure development create substantial market potential for emission control solutions across the petrochemical and logistics sectors.

Competitive Landscape

The vapor recovery units’ market is moderately consolidated, with leading players holding substantial shares through strategic mergers, technology collaborations, and focused R&D investments. Market participants differentiate themselves by offering energy-efficient designs, IoT-enabled monitoring, and automated control systems that enhance operational performance and regulatory compliance. Continuous innovation in system sizing and integrated automation ensures consistent emission control while reducing operational costs.

Emerging trends include subscription-based maintenance services and modular, scalable system designs that improve flexibility and deployment speed. Geographic expansion is primarily focused on the Asia Pacific, driven by stringent environmental regulations and growing industrial infrastructure. Companies are capitalizing on these opportunities to drive long-term market growth while expanding their presence in high-demand regions.

Key Market Developments

- In September 2025, S&R Vapor Recovery inaugurated a 15,000-square-foot North American Field Service headquarters in Midland County, Texas. The facility, designed to support regional expansion, includes office, warehouse, and wash bay space, accommodating technical support, sales teams, and approximately 50 service trucks.

- In August 2025, Flowco Holdings Inc. expanded its high-pressure gas lift and vapor recovery fleet through the acquisition of VRU systems from Archrock. This strategic move enhances Flowco's capabilities in production optimization and methane abatement solutions for the oil and natural gas industry.

- In March 2025, JessCo Solutions secured strategic investments from Argentum Capital Partners IV LP and Climate Investment to expand its vapor recovery and emissions control services in the Permian Basin. The funding supports geographic expansion, fleet diversification, and enhanced sales and marketing efforts.

In February 2025, Zeeco launched an advanced research complex at its Global Technology Center in Oklahoma. The facility supports the development and testing of new combustion and pollution-control technologies, including innovations in vapor recovery systems, to meet evolving environmental standards.

Companies Covered in Vapour Recovery Units Market

- Aereon Inc.

- Cimarron Energy, Inc.

- Dover Corporation

- Flogistix LP

- John Zink Hamworthy

- Kappa GI

- Kilburn Engineering Ltd.

- PETROGAS Systems

- VOCZero Ltd.

- Zeeco, Inc.

- Cool Sorption A/S

- BORSIG Membrane Technology GmbH

- ALMA CARBOVAC

- Symex GmbH & Co. KG

- Accel Compression Inc.

Frequently Asked Questions

The global vapour recovery units market is projected to reach US$ 1.9 billion by 2032, growing from US$ 1.6 billion in 2025 at a CAGR of 2.5%.

Primary drivers include stringent environmental regulations requiring 95% vapor recovery efficiency, expanding oil and gas production activities, and government mandates for emission control compliance.

The adsorption segment leads with 40% market share, driven by superior efficiency in volatile organic compound capture and proven performance in high-volume operations.

North America dominates the market through robust EPA regulatory frameworks and comprehensive emission control infrastructure supporting over 18 million barrels per day refining capacity.

Key opportunity lies in Asia Pacific expansion through policy-driven demand, where regulatory mandates and infrastructure investments create substantial market potential for scalable vapor recovery solutions.

Major players include John Zink Hamworthy, Dover Corporation, Zeeco Inc., Aereon Inc., and Cimarron Energy Inc., recognized for advanced emission control technologies and global market presence.