- Smart Packaging

- Track and Trace Packaging Market

Track and Trace Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Track and Trace Packaging Market by Technology (Barcode, RFID, Others), Product Type (Labels & Tags, RFID-Embedded Packaging, Others), Packaging Level, Application, and Regional Analysis for 2026 - 2033

Track and Trace Packaging Market Size and Trends Analysis

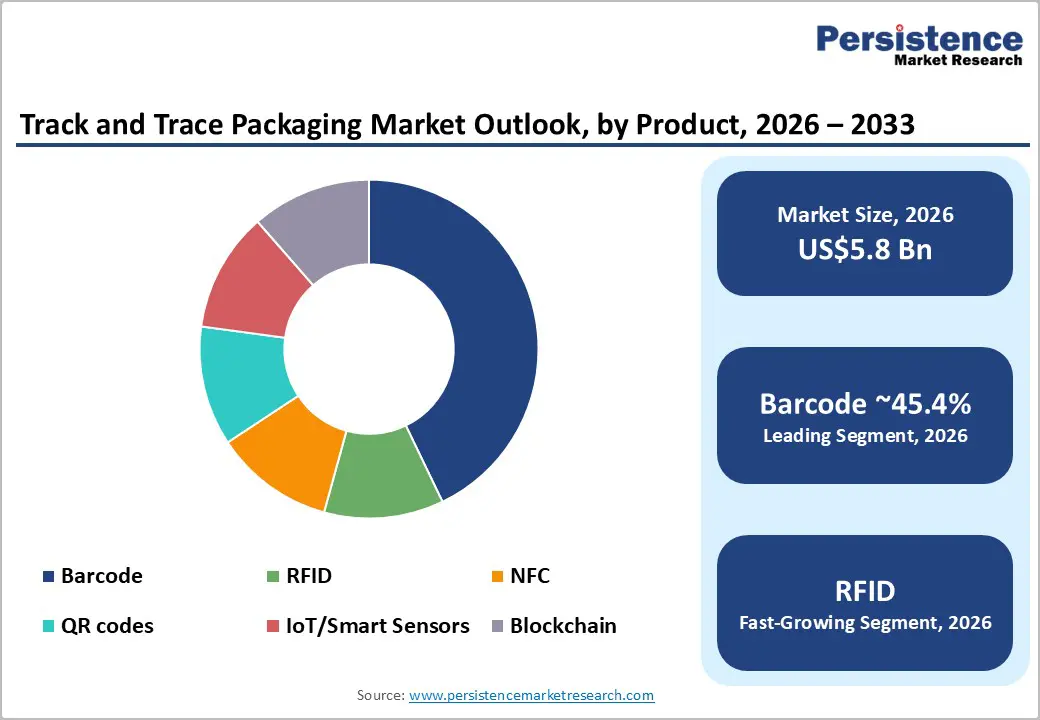

The global track and trace packaging market size is likely to be valued at US$5.8 billion in 2026 and is expected to reach US$11.8 billion by 2033, growing at a CAGR of 10.7% between 2026 and 2033, driven by expanding regulatory mandates for pharmaceutical serialization and electronic traceability, alongside increasing adoption of automated identification technologies such as 2D barcodes, RFID, and NFC across the food, e-commerce, and logistics sectors.

Investment activity remains heavily centered in North America, led by the U.S., while Asia Pacific is rapidly emerging as the fastest-growing region, supported by large-scale manufacturing capacity and improving regulatory harmonization. Market expansion is largely technology-led, evolving from conventional barcode systems toward RFID, IoT-enabled sensing, and blockchain-based solutions, and is increasingly shaped by vendor consolidation through mergers, acquisitions, and strategic platform alliances.

Key Industry Highlights

- Leading Region: North America is projected to account for approximately 37.3% of market share, led by the U.S. due to stringent pharmaceutical serialization enforcement, advanced logistics infrastructure, and early adoption of RFID and automated identification technologies.

- Fastest-Growing Region: Asia Pacific is likely to be the fastest-growing region, driven by large-scale pharmaceutical manufacturing in China and India, rapid e-commerce growth, and increasing convergence toward international traceability regulations.

- Investment Plans: More than 60% of industry investment is directed toward software platforms, cloud-based serialization systems, and RFID infrastructure, with a strong focus on compliance automation, warehouse integration, and multi-enterprise data orchestration across pharmaceutical and retail supply chains.

- Dominant Technology: The barcode technologies (2D DataMatrix and QR codes) segment dominates the market with an estimated 45.4% share, supported by regulatory mandates in pharmaceuticals and widespread adoption across food, retail, and logistics applications.

- b: The labels and tags segment represents approximately 42.3% of the total market demand, owing to their cost efficiency, ease of retrofit on existing packaging lines, and recurring consumable usage across regulated and high-volume industries.

| Key Insights | Details |

|---|---|

| Track and Trace Packaging Market Size (2026E) | US$5.8 Bn |

| Market Value Forecast (2033F) | US$11.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Mandates in Pharmaceuticals and Life Sciences

Mandatory serialization and package-level traceability requirements across regulated pharmaceutical supply chains are a primary structural driver of the track and trace packaging market. Regulations requiring unique identification, verification, and data exchange across manufacturers, distributors, and dispensers compel companies to embed serialization at scale. These mandates generate sustained demand for line-level hardware such as printers and vision readers, serialization and aggregation software platforms, and specialized integration and compliance services. As enforcement timelines tighten and regulatory scopes expand to include additional product categories and trading partners, pharmaceutical manufacturers, contract packagers, and logistics providers continue to represent the largest and most consistent source of market demand.

Cost Declines and ROI Improvements in RFID and Smart Sensors

The declining cost of passive RFID tags, combined with advances in reader performance and cloud-based software architectures, has materially improved the economic viability of RFID-enabled track and trace systems. Lower total cost of ownership has expanded adoption across high-volume retail, logistics, and returnable asset management environments. RFID deployments increasingly demonstrate measurable gains in inventory accuracy, labor efficiency, and shrinkage reduction, with typical return-on-investment timelines ranging from 12 to 36 months in warehouse and retail operations. These improvements position RFID as a practical complement to barcodes, particularly for environments requiring bulk, non-line-of-sight scanning and automation at scale.

E-Commerce Growth, Anti-Counterfeiting, and Consumer Engagement

Rapid expansion of e-commerce and omnichannel fulfillment models has increased demand for parcel-level tracking, provenance verification, and tamper evidence throughout distribution networks. Track and trace technologies such as QR codes, serialization, and digital authentication enable improved delivery transparency and post-sale traceability. At the brand level, companies are deploying consumer-facing QR and NFC features to authenticate products, support loyalty programs, and enable lifecycle engagement. Rising financial and reputational risks associated with counterfeiting further accelerate investments in digital verification, expanding the market beyond compliance into marketing, brand protection, and after-sales service applications.

Barrier Analysis - Upfront Capital and Integration Complexity

End-to-end track and trace implementations require significant upfront investment in line-level hardware, systems integration with manufacturing and enterprise software, and connectivity with external data repositories. For mid-sized manufacturers, this translates into elevated capital expenditure and heightened project execution risk. Process re-engineering requirements, including aggregation, rework handling, and exception management, can delay operational stabilization and extend payback periods. In complex packaging environments involving metals or flexible materials, read-rate challenges further increase implementation risk. Typical line retrofit projects may increase overall capital equipment budgets by approximately 5-12%.

Data Governance, Interoperability, and Standards Fragmentation

The coexistence of multiple data standards, regional repository protocols, and proprietary system interfaces creates operational complexity across global supply chains. Inconsistent data quality and limited interoperability among trading partners increase onboarding costs and complicate multi-market expansion strategies. Compliance with data privacy, security, and retention requirements adds additional administrative and technical burden, particularly in regulated industries such as pharmaceuticals and food. These factors contribute to higher professional services expenditure and longer system stabilization cycles, constraining rapid and cost-efficient deployment in fragmented supply networks.

Opportunity Analysis - Transition from Secondary to Primary Packaging with Smart Sensors

Integrating smart sensors and serialization directly into primary packaging enables high-value use cases such as temperature monitoring, spoilage detection, and condition assurance throughout the product lifecycle. Advances in sensor miniaturization, printed electronics, and disposable NFC technologies are reducing integration complexity and cost barriers. These capabilities allow brands to monetize provenance services, including authentication, dynamic content delivery, and warranty activation. If primary-level smart packaging adoption captures even 5-7% of the broader smart packaging opportunity, it would represent a multi-hundred-million-dollar incremental revenue pool within the forecast period.

Multi-Enterprise Data Orchestration and Service Platforms

There is growing demand for network-based platforms that aggregate serialization data, automate reconciliation, and deliver analytics across multiple supply chain participants. Such platforms are particularly attractive in regulated industries, where compliance infrastructure exhibits high renewal rates and predictable recurring revenue characteristics. Providers can expand value through advanced analytics, predictive alerts, and supplier compliance services. As more trading partners connect to shared networks, platform providers benefit from defensible network effects that enhance customer retention and long-term revenue scalability.

Category-wise Analysis

Technology Insights

Barcodes are anticipated to account for approximately 45.4% of the market share in 2026, during the forecast period, maintaining their leadership due to cost efficiency, global standardization, and broad regulatory acceptance. Two-dimensional DataMatrix codes are extensively mandated in pharmaceutical serialization programs for unit-level identification, while QR codes are widely deployed across food, retail, and logistics applications for traceability, recall management, and consumer engagement. Barcode-based systems integrate smoothly with existing packaging lines, vision inspection systems, and validation workflows, making them the preferred solution for compliance-driven industries operating under strict cost and throughput constraints. Their dominance is particularly pronounced in secondary and tertiary packaging, where point-of-sale verification, aggregation, and human-readable inspection remain critical across global supply chains.

The RFID segment is expected to register the fastest growth rate among track and trace technologies, driven by declining tag costs, improved read accuracy, and demonstrable operational ROI in high-volume environments. Passive UHF RFID enables non-line-of-sight, bulk scanning, making it highly effective for pallet-level tracking, automated warehouse operations, and returns management. Retailers and third-party logistics providers are increasingly mandating RFID tagging for selected product assortments to enhance inventory accuracy and fulfillment speed. Deeper integration with warehouse management systems, transportation platforms, and IoT-based analytics further supports RFID scalability beyond pilot projects, accelerating enterprise-wide deployments across retail, logistics, and industrial applications.

Product Type Insights

Labels and printable tags are anticipated to hold approximately 42.3% of the market share in 2026, reflecting their versatility, low unit cost, and compatibility with established serialization standards. These products are widely used across pharmaceuticals, food and beverages, and logistics for unit-level identification, batch traceability, and recall execution. Labels can be easily retrofitted onto existing packaging lines without major capital investment, making them especially attractive to contract packagers and mid-sized manufacturers. Continuous demand for consumables, combined with their compatibility with barcode and QR coding systems, reinforces their long-term dominance in compliance-driven and high-volume packaging environments.

The RFID-embedded packaging segment is projected to be the fastest-growing product category as supply chains increasingly prioritize automation, real-time visibility, and data accuracy. Embedding RFID directly into cartons, trays, or flexible packaging materials enables automated aggregation, reduces manual scanning requirements, and improves throughput in distribution centers. As packaging converters develop validated, scalable manufacturing processes, unit economics continue to improve, supporting broader adoption across premium consumer goods, pharmaceuticals, and logistics applications. The emergence of managed service and subscription-based deployment models further accelerates uptake by lowering upfront investment barriers for brand owners and distributors.

Regional Insights

North America Track and Trace Packaging Market Trends - Regulatory-Driven Serialization and Retail-Led RFID Expansion

North America is projected to remain the largest regional market, accounting for approximately 37.3% in 2026, driven primarily by regulatory rigor, advanced manufacturing infrastructure, and early adoption of automation technologies. The U.S. leads the region due to long-standing enforcement of pharmaceutical serialization and traceability requirements, which have compelled manufacturers, contract packagers, and distributors to invest consistently in compliant packaging systems, software platforms, and data exchange services.

Major pharmaceutical producers and CMOs have continued upgrading from basic serialization to integrated aggregation and verification architectures to improve audit readiness and operational efficiency. Retail and logistics developments further reinforce regional leadership. Large U.S. retailers and omnichannel operators have expanded RFID-based inventory and fulfillment programs to improve stock accuracy and reduce shrinkage, indirectly accelerating the adoption of RFID-enabled packaging formats across upstream suppliers.

Logistics providers and cold-chain specialists are also integrating serialized packaging data with warehouse management and transportation systems, improving traceability for temperature-sensitive pharmaceuticals and biologics. These investments are closely tied to the modernization of U.S. distribution networks, where automation, robotics, and real-time visibility are becoming standard operating requirements rather than differentiators.

Canada contributes steadily to regional growth through strong adoption in healthcare logistics and food traceability, supported by government-backed transparency initiatives and cross-border trade alignment with U.S. standards. Across the region, technology providers such as global automation firms, coding and marking specialists, and software vendors continue to expand their North American footprints through system upgrades, cloud-based compliance platforms, and managed services. Collectively, these developments position North America as a mature yet innovation-driven market where compliance obligations increasingly converge with efficiency and data monetization objectives.

Europe Track and Trace Packaging Market Trends - Harmonized Pharmaceutical Compliance and Smart Label Modernization

Europe represents a mature and structurally robust track and trace packaging market, underpinned by early adoption of pharmaceutical serialization and a harmonized regulatory framework. The implementation of centralized medicine verification repositories has created sustained demand for system upgrades, data integrity enhancements, and lifecycle management services rather than first-time installations alone.

As a result, the European market increasingly focuses on modernization, interoperability, and long-term platform resilience. Germany, the U.K., and France remain at the forefront due to strong industrial automation ecosystems and advanced packaging capabilities. Pharmaceutical manufacturers and packaging converters in these countries are investing in next-generation serialization lines, vision inspection upgrades, and secure data exchange platforms to support both compliance and operational efficiency. In parallel, food and consumer goods brands across Western Europe are leveraging QR codes and smart labeling initiatives to support transparency, sustainability disclosures, and digital consumer engagement, expanding the commercial value of track and trace infrastructure beyond regulatory use cases.

Southern European markets such as Spain and Italy continue to benefit from the EU-wide regulatory harmonization, which reduces barriers to cross-border traceability investments. Packaging equipment suppliers and software vendors operating across Europe increasingly offer standardized, multi-country solutions that simplify compliance across different national systems. Ongoing collaboration between regulators, industry associations, and technology providers further supports consistent adoption and minimizes fragmentation. Overall, Europe’s market growth is driven less by mandate expansion and more by system optimization, digital engagement, and integration with broader Industry 4.0 initiatives.

Asia Pacific Track and Trace Packaging Market Trends- Export-Oriented Serialization and Rapid Regulatory Alignment

Asia Pacific is the fastest-growing regional market for track and trace packaging, supported by large-scale manufacturing capacity, expanding domestic consumption, and progressive regulatory alignment. China and India represent the largest volume opportunities, particularly in pharmaceuticals, food, and consumer goods, where rising concerns over counterfeit products and supply chain transparency are accelerating adoption. Manufacturers in both countries are increasingly investing in serialization and traceability infrastructure ahead of formal enforcement deadlines to remain competitive in export-oriented supply chains.

China’s pharmaceutical and consumer goods sectors are seeing growing deployment of QR codes and centralized data platforms to support product authentication, recall efficiency, and regulatory reporting. Major domestic manufacturers and exporters are aligning packaging systems with international standards to facilitate trade with North America and Europe. In India, the expansion of pharmaceutical exports and government-backed traceability initiatives has driven increased adoption of serialization at both primary and secondary packaging levels, with contract manufacturers playing a key role in scaling implementation.

Japan contributes a different growth dynamic, emphasizing advanced automation, sensor integration, and high-precision packaging technologies. Japanese manufacturers are integrating smart sensors and data-rich identifiers into packaging for quality assurance and lifecycle monitoring, particularly in high-value pharmaceuticals and electronics. Across Southeast Asia, governments are piloting anti-counterfeiting and food traceability programs, encouraging early-stage investment by regional manufacturers. These developments position Asia Pacific as a rapidly evolving market where regulatory preparation, export competitiveness, and manufacturing scale drive sustained demand growth.

Competitive Landscape

The global track and trace packaging market is moderately concentrated at the platform and systems integration level, while hardware and consumables remain fragmented. Leading vendors offer integrated software, hardware, and services, creating high switching costs and recurring revenue streams. Competition spans niche technology specialists and vertically integrated solution providers, with global compliance capabilities serving as a key differentiator.

Developments have been characterized by acquisitions to expand geographic reach, enhance edge-level data capture, and strengthen end-to-end platform offerings. Vendors are increasingly combining serialization, inspection, and analytics capabilities to address both compliance and commercial use cases. Partnerships with integrators and logistics providers further accelerate market penetration.

Key strategies include platform expansion through SaaS models, vertical integration of inspection and serialization technologies, managed service offerings to reduce customer CapEx, and targeted acquisitions to strengthen compliance and data orchestration capabilities.

Key Industry Developments

- In February 2025, Antares Vision launched its DIAMIND Connect platform, integrating advanced AI tools for intelligent data processing and analysis to enhance traceability, customer engagement, and supply chain digitalization across multiple industries. This platform expansion strengthens Antares Vision’s position in delivering end-to-end track and trace solutions globally and supports broader adoption of digital traceability systems.

- In March 2025, TraceLink announced the rollout of its “Trace Histories” feature to provide comprehensive visibility into product journeys, improving recall management and counterfeit detection across complex supply chains. The enhancement is aimed at life sciences and regulated sectors where real-time product provenance is critical.

Companies Covered in Track and Trace Packaging Market

- Antares Vision Group

- TraceLink

- OPTEL Group

- Systech

- Zebra Technologies

- Avery Dennison

- Honeywell International

- Siemens

- Syntegon Technology

- Markem-Imaje

- SEA Vision

- SICK AG

- Mettler-Toledo

- Videojet Technologies

- Domino Printing Sciences

- Cognex

- Toshiba Tec

- Kezzler

Frequently Asked Questions

The global track and trace packaging market is valued at US$5.8 billion in 2026.

By 2033, the track and trace packaging market is expected to reach US$11.8 billion.

Key trends include widespread pharmaceutical serialization, increasing adoption of RFID for automated, non-line-of-sight tracking, integration of QR codes for consumer engagement and transparency, convergence of track and trace systems with IoT and warehouse automation platforms, and growing use of data analytics to support recall management and regulatory reporting.

Barcode-based technologies, including 2D DataMatrix and QR codes, are the leading segment, accounting for the largest share of adoption due to their low cost, global compatibility, and strong regulatory acceptance across pharmaceuticals, food, and logistics.

The track and trace packaging market is projected to grow at a CAGR of 10.7% between 2026 and 2033.

Major players with strong technology portfolios and global reach include Zebra Technologies, Avery Dennison, Antares Vision Group, SICK AG, and TraceLink.