- Healthcare Services

- Toxicology Laboratories Market

Toxicology Laboratories Market Size, Share, and Growth Forecast, 2026 - 2033

Toxicology Laboratories Market by Laboratory Type (Clinical, Forensic, Pharma & Biotech Labs), Service Type (Screening, Quantitative Analysis, Toxicity Profiling), Technology Platform (Chromatography, Mass Spectrometry, Immunoassays), and Regional Analysis for 2026 - 2033

Toxicology Laboratories Market Share and Trends Analysis

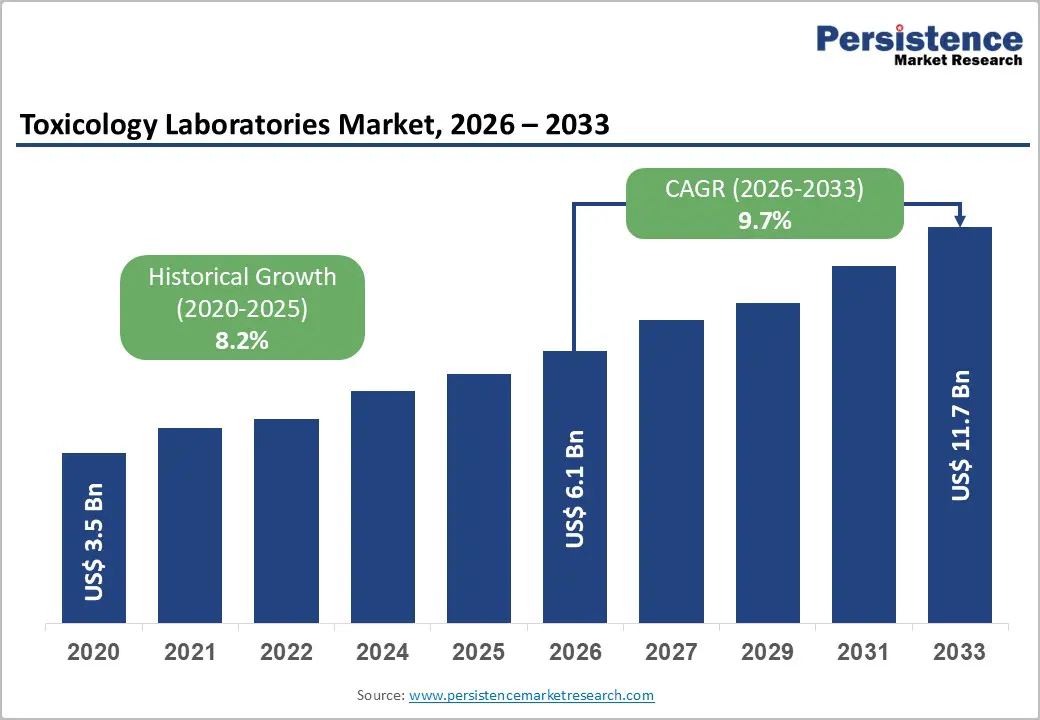

The global toxicology laboratories market size is likely to be valued at US$ 6.1 billion in 2026, and is projected to reach US$ 11.7 billion by 2033, growing at a CAGR of 9.7% during the forecast period 2026-2033. The market is primarily driven by stringent regulatory requirements for drug safety and product compliance, which compel pharmaceutical, clinical, and industrial organizations to conduct comprehensive toxicity assessments before product approval.

Simultaneously, the growing demand for forensic and workplace drug screening, fueled by rising substance abuse, workplace safety initiatives, and legal compliance, adds recurring testing volume. The rapid adoption of advanced analytical technologies such as chromatography, mass spectrometry, and immunoassays enhances detection sensitivity, accuracy, and throughput. Furthermore, expanding global healthcare infrastructure investments, coupled with laboratory digitalization and automation, are accelerating operational efficiency and increasing market penetration across emerging regions.

Key Industry Highlights

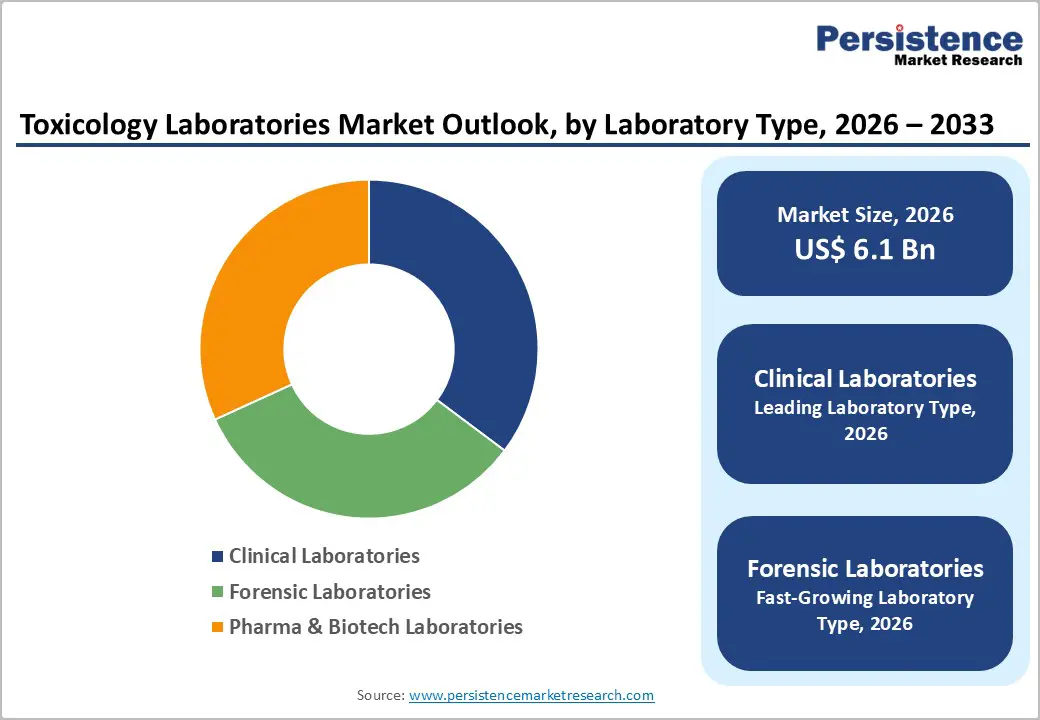

- Dominant Laboratories: Clinical laboratories are expected to command around 31% revenue share in 2026, while forensics are likely to grow the fastest at 10.1% CAGR through 2033, driven by rising demand for drug safety testing.

- Leading Service Types: Screening services are projected to hold roughly 30% revenue share in 2026, while quantitative analysis is likely the fastest-growing during 2026–2033, reflecting growing pharmaceutical and research needs.

- Dominant Technology Platforms: Chromatography is anticipated to lead with about 33% revenue share in 2026, while AI-enabled analytics and mass spectrometry represent the fastest-growing through 2033.

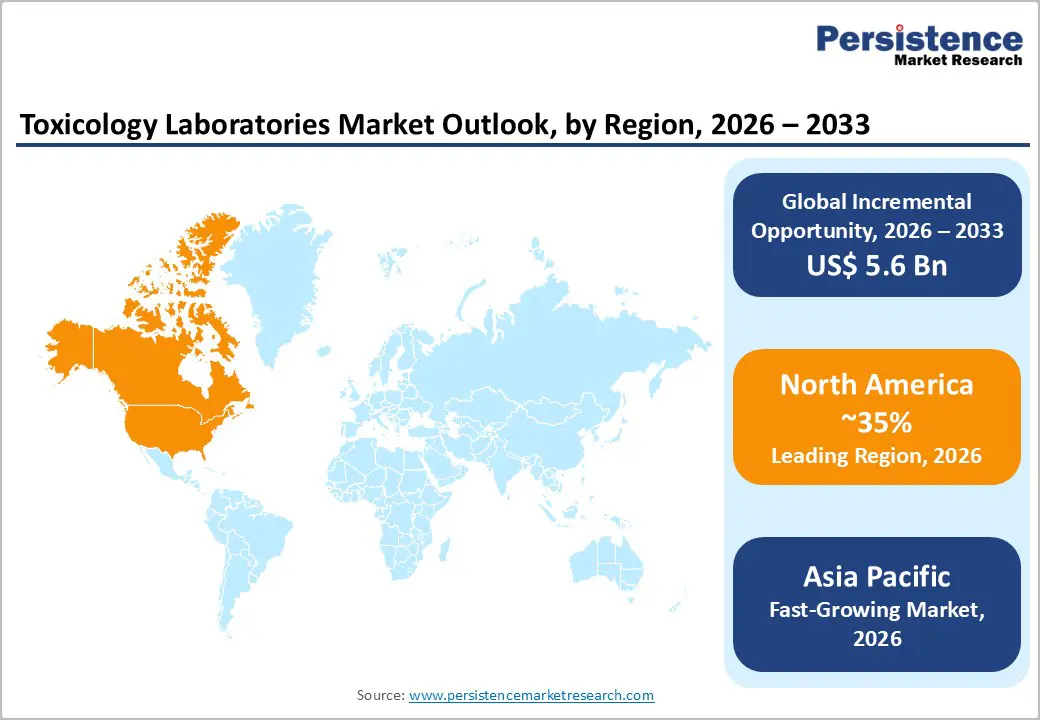

- Regional Leadership: North America is poised to lead with an estimated 35% market share in 2026, while Asia Pacific is expected to be the fastest-growing market at approximately 11.2% CAGR through 2033, driven by healthcare infrastructure expansion and outsourcing.

- Competitive Environment: Market development is being steered investments, merger & acquisition (M&A) activities, and regional expansions, focusing on technology partnerships, lab digitalization, and Asia Pacific.

| Key Insights | Details |

|---|---|

|

Toxicology Laboratories Market Size (2026E) |

US$ 6.1 Bn |

|

Market Value Forecast (2033F) |

US$ 11.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.2% |

DRO Analysis

Regulatory Compliance & Public Safety Requirements

Governments and international regulators such as the U.S. Food and Drug Administration (FDA) and European authorities continue to tighten toxicology requirements for drug approvals, public health products, and safety testing. In April 2025, the U.S. FDA released a roadmap aimed at reducing reliance on animal testing in pre-clinical safety studies, signaling an increased focus on risk-based, evidence-driven toxicity evaluation frameworks that laboratories must now support with accurate analytical data and higher throughput workflows. This regulatory shift is driving demand for advanced testing capabilities and data traceability.

Beyond pharmaceuticals, regulatory compliance extends to workplace and public safety contexts. In 2025–2026, the U.S. FDA and partner agencies increased enforcement actions on unsafe imported consumer products, requiring labs to screen for a broader range of toxicants and contaminants. This reflects a broader enforcement trend toward systematic screening and scientific evaluation of chemical risks across food, cosmetics, and industrial goods sectors. As a result, toxicology laboratories are experiencing expanded service demand across clinical, forensic, and consumer safety sectors, strengthening recurring test volumes and revenue reliability.

Technological Advancements & Cross-Sector Demand

Adoption of cutting-edge analytical techniques such as liquid mobile phase (LC-MS), gas mobile phase (GC-MS), immunoassays, and AI-enhanced data interpretation is transforming laboratories into high-precision testing hubs with faster turnaround and deeper detection sensitivity. Regulatory science itself is evolving, with frameworks increasingly recognizing computational and human-based methods alongside traditional assays. For example, in early 2026, an expansion of human cell-based toxicology services across Asia-Pacific enhanced accessibility to human-relevant screening data, supporting both drug development and safety testing workflows across multiple industries. These technology integrations also reduce data ambiguity and improve compliance outcomes.

This technological shift aligns with growing demand from clinical, forensic, and pharmaceutical segments. Rising incidence of drug misuse, therapeutic monitoring needs, and complex pre-clinical toxicity profiling for new molecular entities require laboratories to offer high-confidence analytics and rapid reframing of test panels. Additionally, automated sample handling and digital workflows are reducing turnaround times while improving reproducibility. Combined, these trends significantly enhance operational efficiency, broaden service portfolios, and strengthen laboratories’ strategic role as multi-industry safety and evidence partners, driving long-term market expansion.

High Cost of Advanced Instrumentation

Sophisticated analytical platforms such as mass spectrometers, high-performance liquid chromatographs, and automated systems require substantial capital expenditure for acquisition, calibration, validation, and ongoing maintenance. In 2025, ongoing tariff increases and global supply chain disruptions raised the cost of laboratory reagents, consumables, and imported diagnostic equipment, forcing laboratories to adjust procurement strategies and hold larger inventory buffers to avoid service interruptions. These higher baseline costs constrain budgets and delay critical upgrades for many facilities, limiting their ability to adopt newer high-throughput testing technologies.

Even when funding is available, the resources required for operator training, method validation, and regulatory compliance deter smaller or cost-constrained laboratories from adopting cutting-edge instrumentation. Purchasing delays and increased cost per test impact operational flexibility and financial planning, particularly where validated methods must be re-verified after minor component or software changes. These economic barriers reduce the pace of technological adoption, limit smaller labs’ ability to compete, and may slow overall market growth in high-demand regions.

Skilled Workforce Shortages & Regulatory Complexity

Toxicology workflows depend on highly trained professionals with expertise in analytical chemistry, instrumentation, data interpretation, and regulatory compliance. In late 2025, workforce shortages reached national policy discussions in the U.S. with the introduction of the Medical Laboratory Personnel Shortage Relief Act, aiming to expand training resources and federal support for medical laboratory personnel, underscoring how acute staffing gaps have become within healthcare systems. Limited personnel availability is affecting both clinical and forensic laboratories, creating bottlenecks in high-demand testing areas.

Despite legislative attention, chronic shortages persist globally, driven by retirements, limited training pipelines, and burnout among existing professionals. Nearly half of laboratory leaders report ongoing difficulties hiring qualified staff, which impacts turnaround times and operational efficiency. These bottlenecks are compounded by regulatory complexity in multi-jurisdictional environments, where varying compliance standards add administrative burdens, slow cross-border service expansion, and increase reliance on a limited number of expert personnel capable of navigating diverse quality frameworks.

Expansion in Emerging Economies & Outsourcing Potential

Regions such as Asia Pacific, including China, India, and ASEAN markets, are experiencing rapid growth in pharmaceutical R&D, biotechnology activity, and healthcare investment. Governments across these regions are actively strengthening clinical research ecosystems and regulatory frameworks to support drug development and safety testing. This expansion is increasing demand for toxicology services, particularly as more clinical trials and biologics development programs are being conducted locally, requiring reliable and scalable toxicity assessment capabilities.

These trends offer significant opportunities for outsourcing toxicology testing services to cost-effective regional laboratories. Multinational pharmaceutical companies are increasingly leveraging these markets to optimize operational costs while maintaining quality and regulatory compliance. With the global market projected to reach US $11.7 billion by 2033, Asia Pacific is positioned to capture a substantial share due to its skilled workforce, improving infrastructure, and supportive policy environment. Additionally, global regulatory alignment efforts are making cross-border collaboration more feasible, further strengthening outsourcing potential.

Advanced Testing Methods, AI Integration & Laboratory Digitalization

The adoption of in vitro assays, omics-based profiling, and computational toxicology (in silico modeling) is accelerating, supported by major regulatory and industry shifts. In March 2026, the U.S. FDA issued new guidance promoting “New Approach Methodologies (NAMs)”, encouraging the use of human-relevant and non-animal testing approaches in drug development. Additionally, global pharmaceutical companies are increasingly adopting AI-driven toxicology models, with industry reports highlighting reduced drug development timelines and improved predictive accuracy through these technologies.

The digitalization and workflow automation, including laboratory information management system (LIMS), cloud-based reporting, and advanced analytics, are transforming laboratory operations. AI-enabled tools are improving data interpretation, reducing turnaround times, and enabling high-throughput testing at scale. These innovations enhance both operational efficiency and regulatory compliance, positioning laboratories as critical partners in drug safety and environmental testing. These advanced methodologies and digital transformation create strong opportunities for service differentiation, improved client outcomes, and expansion across clinical, forensic, and industrial toxicology domains.

Category-wise Analysis

Laboratory Type Insights

Clinical laboratories are expected to dominate in 2026, accounting for approximately 31% of the segmental revenue share in 2026, driven by their central role in routine drug screening, therapeutic monitoring, and patient care diagnostics across hospitals, diagnostic chains, and outpatient facilities. These labs handle high-volume daily workflows, supported by rising healthcare utilization, increasing chronic disease burden, and the growing need to monitor drug interactions and toxicity levels. A key supporting development is the 2025–2026 focus by regulatory bodies on biomarker-based toxicology and advanced analytical workflows, with the U.S. FDA actively promoting research in pharmacogenomics and translational safety evaluation, reinforcing the critical role of clinical laboratory infrastructure in modern healthcare systems.

Forensic laboratories are projected to represent the fastest-growing segment, projected to expand at a CAGR of about 10.1% through 2033, driven by increasing forensic investigations, criminal case analysis, and public safety initiatives. Growth is supported by expanding roadside drug testing programs and stricter legal mandates for substance detection. The rising complexity of synthetic and designer drugs is further increasing demand for advanced toxicology capabilities. A key 2025 development includes the launch of a government-backed forensic laboratory in Shillong, India, equipped with GC-MS systems to strengthen toxicology investigations, demonstrating how public sector investments are enhancing forensic testing infrastructure and accelerating segment growth.

Service Type Insights

Screening services are poised to lead with an estimated 30% of the toxicology laboratories market revenue share in 2026, driven by their high-frequency use in pre-employment testing, workplace compliance programs, and clinical diagnostics. These services enable rapid, large-scale substance detection, making them essential for organizations requiring quick and reliable results. Demand is reinforced by regulatory requirements for drug-free workplaces and public safety monitoring. In 2025–2026, government-led toxicology screening programs in defense and transportation sectors expanded significantly, with large-scale sample processing for operational safety, highlighting the critical role of screening services in maintaining workforce and public safety standards.

Quantitative analysis services are anticipated as the fastest-growing segment, expected to register a CAGR of 9.8% during 2026–2033, as pharmaceutical and biotech industries require precise measurement of low-level toxicants for drug development and clinical trials. These services are essential for generating accurate dose-response and exposure data, which are critical for regulatory approvals. A major supporting development is the U.S. FDA’s 2026 guidance promoting New Approach Methodologies (NAMs), emphasizing the need for high-quality, human-relevant quantitative toxicology data, thereby increasing reliance on advanced analytical techniques and accelerating demand for quantitative testing services.

Regional Insights

North America Toxicology Laboratories Market Trends

North America is expected to dominate by accounting for approximately 35% of the toxicology laboratories market share in 2026, supported by high healthcare expenditure, stringent regulatory frameworks, and a well-established pharmaceutical R&D ecosystem. The United States plays a central role, driven by strong oversight from regulatory bodies such as the U.S. FDA and extensive workplace drug testing requirements. The region benefits from a mature healthcare infrastructure and widespread adoption of toxicology testing across clinical, forensic, and industrial applications, ensuring consistent demand across multiple end-use sectors.

Key growth drivers include consistent funding for clinical and forensic toxicology and widespread adoption of advanced technologies such as LC-MS and GC-MS across laboratories. A notable 2026 development includes the U.S. Department of Health and Human Services (HHS) expanding funding for overdose surveillance and toxicology programs, strengthening lab capacity for drug monitoring. Regulatory mandates ensure steady demand, while investments in digital lab infrastructure, automation, and data integration platforms continue to enhance operational efficiency and reinforce regional leadership.

Europe Toxicology Laboratories Market Trends

Europe holds a significant position in the global market, with strong performance across countries such as Germany, the U.K., France, and Spain. The region benefits from well-integrated healthcare and forensic systems, along with regulatory harmonization across European Union (EU) member states, enabling standardized toxicology testing practices. This alignment supports cross-border collaboration and enhances efficiency in delivering toxicology services, while also ensuring consistent quality and compliance across multiple jurisdictions.

Growth is driven by stringent chemical safety regulations and rising demand for environmental and product safety testing across industries. A key 2025 development includes the European Chemicals Agency (ECHA) advancing PFAS-related restrictions, increasing toxicology testing requirements across manufacturing and environmental sectors. Furthermore, investments in high-throughput analytical technologies and digital reporting systems are modernizing laboratories, while collaboration between regional labs and global contract research organizations (CROs) continues to strengthen overall service capabilities and scalability.

Asia Pacific Toxicology Laboratories Market Trends

Asia Pacific is projected to be the fastest-growing regional market for toxicology laboratories, projected to expand at a CAGR of around 11.2% through 2033. Growth is driven by rapid healthcare infrastructure development, increasing pharmaceutical and biotech activity, and rising investments in laboratory capabilities. Countries such as China, Japan, and India are leading this expansion, supported by growing clinical trials, environmental monitoring mandates, and increasing awareness of toxicology testing in public health systems.

A significant 2025–2026 development includes the Government of India expanding forensic science laboratory infrastructure, enhancing toxicology testing capacity nationwide. Similarly, China’s strengthened food and drug safety enforcement initiatives in 2025 have increased demand for toxicology screening across industrial and consumer safety domains. Competitive opportunities are further supported by public-private partnerships, technology transfer initiatives, and localization of global lab networks, alongside government funding for modernization, skill development, and workforce training programs.

Competitive Landscape

The global toxicology laboratories market exhibits a moderately consolidated structure, with leading players such as Labcorp, Quest Diagnostics, Eurofins Scientific, and SGS collectively accounting for a significant share of total revenue. These companies leverage extensive laboratory networks, strong regulatory expertise, and broad service portfolios spanning clinical, forensic, pharmaceutical, and environmental toxicology. Their competitive advantage is further strengthened by continuous investments in advanced analytical technologies such as LC-MS/MS, GC-MS, and high-throughput screening platforms, along with growing adoption of digital tools for data management and workflow optimization.

The mid-sized and specialized laboratories are actively competing by focusing on niche services such as bioanalytical testing, forensic toxicology, and environmental safety assessments. Barriers to entry remain relatively high due to capital-intensive instrumentation, stringent accreditation requirements, and the need for highly skilled professionals. However, increasing digitalization is enabling technology-driven entrants to participate through LIMS platforms, AI-based analytics, and remote data interpretation services. Market dynamics are expected to evolve with ongoing mergers, acquisitions, and strategic partnerships, as leading players expand geographically and enhance capabilities, while collaborations between laboratories and biotech/pharma firms continue to drive innovation and service diversification

Key Industry Developments

- In March 2026, VivoSim Labs released new data validating its NAMkind™ liver and intestine models for predicting toxicity in antibody-drug conjugates (ADCs), demonstrating strong correlation with clinical outcomes. The models help distinguish between antibody, payload, and linker-related toxicity, enabling safer ADC design and improving early-stage drug development efficiency.

- In December 2025, Labcorp acquired outreach laboratory assets from Community Health Systems (CHS) for approximately US$ 194 million, strengthening its presence across 13 U.S. states. This move enhances Labcorp’s diagnostic and toxicology service reach, particularly in decentralized and regional healthcare markets.

- In June 2025, Frontage Laboratories launched a massive GMP-compliant contract research, development, and manufacturing organization (CRDMO) facility in Exton, Pennsylvania, enhancing its capabilities for pharmaceutical and biotech clients. The site features nine GMP suites and integrated labs, enabling end-to-end services from formulation to clinical supply, strengthening its position as a one-stop contract development and manufacturing organization (CDMO) provider.

Companies Covered in Toxicology Laboratories Market

- LabCorp

- Thermo Fisher Scientific

- Eurofins Scientific

- Charles River Laboratories

- Covance Inc.

- SGS SA

- Quest Diagnostics

- Agilent Technologies

- PerkinElmer Inc.

- Bio Rad Laboratories

- Intertek Group plc

- Bureau Veritas

- ALS Limited

- Neogen Corporation

- Randox Laboratories

Frequently Asked Questions

The global toxicology laboratories market is projected to reach US$ 6.1 billion in 2026.

Stringent regulatory requirements, rising drug safety testing, and increasing adoption of advanced analytical technologies are driving the market.

The market is poised to witness a CAGR of 9.7% from 2026 to 2033.

Expansion in emerging economies, adoption of high-throughput methods, and digitalization of laboratory workflows present key opportunities.

Labcorp, Quest Diagnostics, Eurofins Scientific, and SGS SA are some of the key players in the market.