- Biotechnology

- In-vitro Toxicology Assays Market

In-vitro Toxicology Assays Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

In-vitro Toxicology Assays Market by Product (Consumables, Assays, Instruments, Software, and Services), by Technology (Cell Culture Technology, High Throughput Technology, Molecular Imaging Technology, and OMICS Technology), Application (Systemic Toxicology, Dermal Toxicity, Endocrine Disruption, Ocular Toxicity, and Others) End-user (Pharmaceutical and Biotechnology Companies, Diagnostics Laboratories and Academic Institutes & Research Laboratories), and Regional Analysis from 2026 to 2033

In-vitro Toxicology Assays Market Share and Trends Analysis

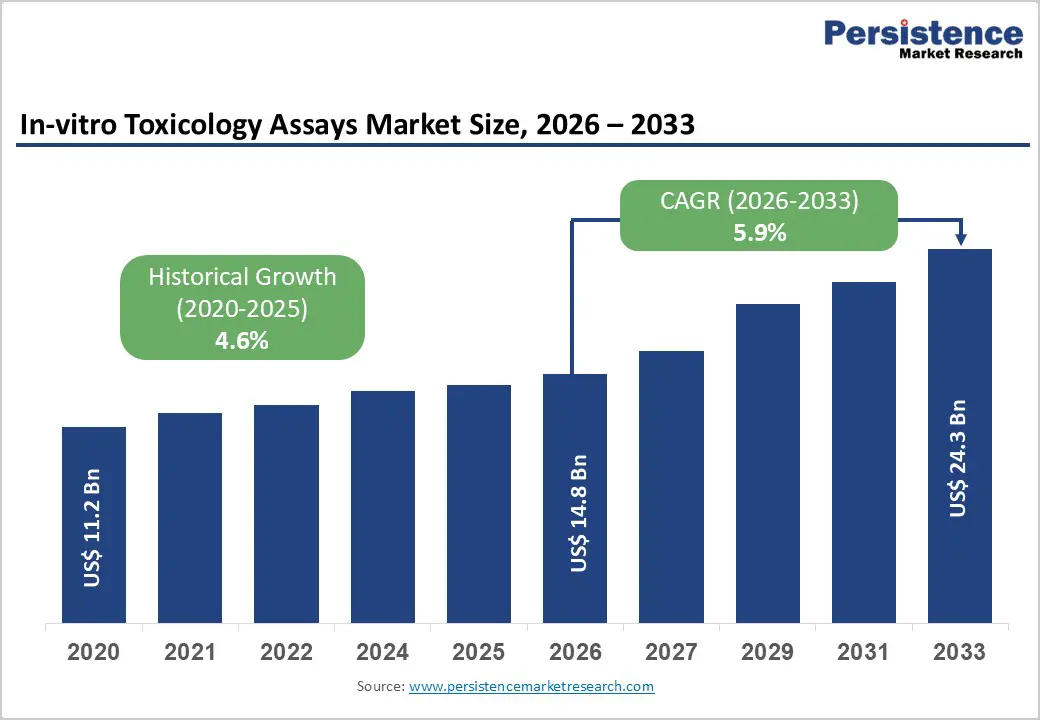

The global in-vitro toxicology assays market size is estimated to grow from US$ 14.8 billion in 2026 to US$ 24.3 billion by 2033. The market is projected to record a CAGR of 5.9% during the forecast period from 2026 to 2033. Global demand for in-vitro toxicology assays is rising steadily, driven by increasing regulatory pressure to reduce animal testing, expanding pharmaceutical and biotechnology pipelines, and growing safety assessment requirements across chemicals, cosmetics, and medical products. Rising volumes of drug candidates, complex biologics, and novel chemical entities are expanding the need for early-stage toxicity screening to identify safety risks before clinical development. Increased focus on cost containment and failure reduction in drug development is accelerating the adoption of predictive, high-throughput in vitro testing platforms.

Regulatory frameworks supporting alternative testing methods, coupled with ethical concerns related to animal use, are further strengthening market demand. Technological advancements in cell-based assays, automation, 3D culture systems, and data analytics are improving predictive accuracy, reproducibility, and testing efficiency. Growing outsourcing of preclinical testing to CROs, expanding research activity in academic institutions, and rising awareness of mechanistic toxicology are supporting adoption. Increasing healthcare and R&D investments across developed and emerging markets continue to drive long-term global market expansion

Key Industry Highlights

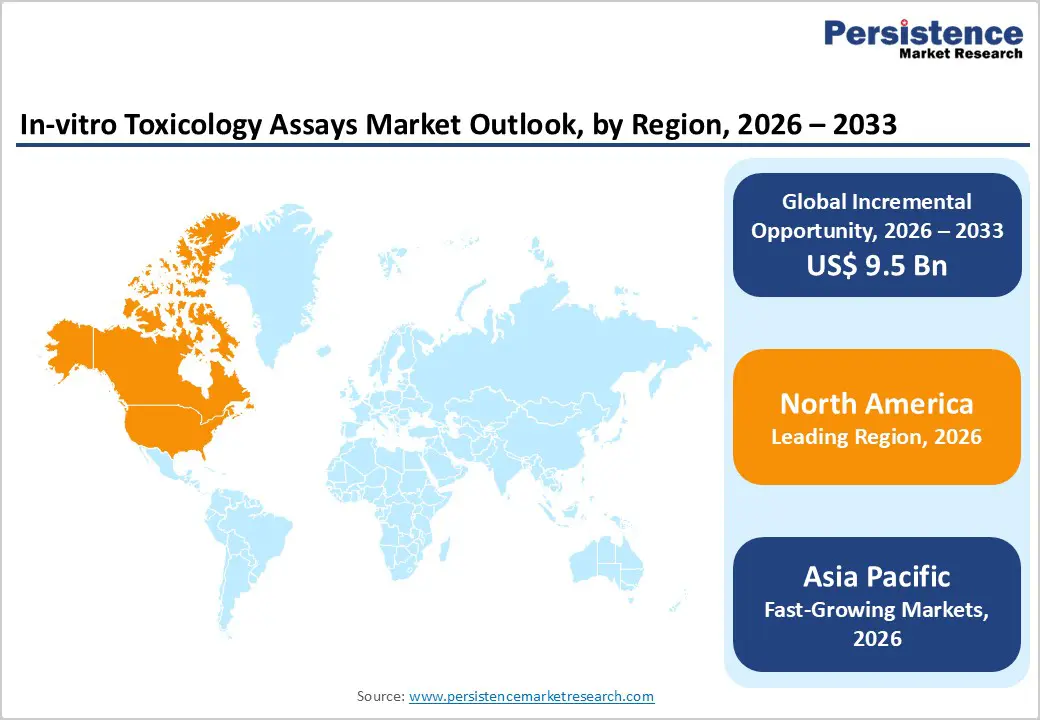

- Leading Region: North America holds the largest market share at 48.5%, supported by strong regulatory enforcement, advanced laboratory infrastructure, high pharmaceutical R&D spending, and early adoption of validated in-vitro testing platforms.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace due to rapid growth in pharmaceutical manufacturing, increasing regulatory alignment with global standards, expanding CRO presence, and rising research investments.

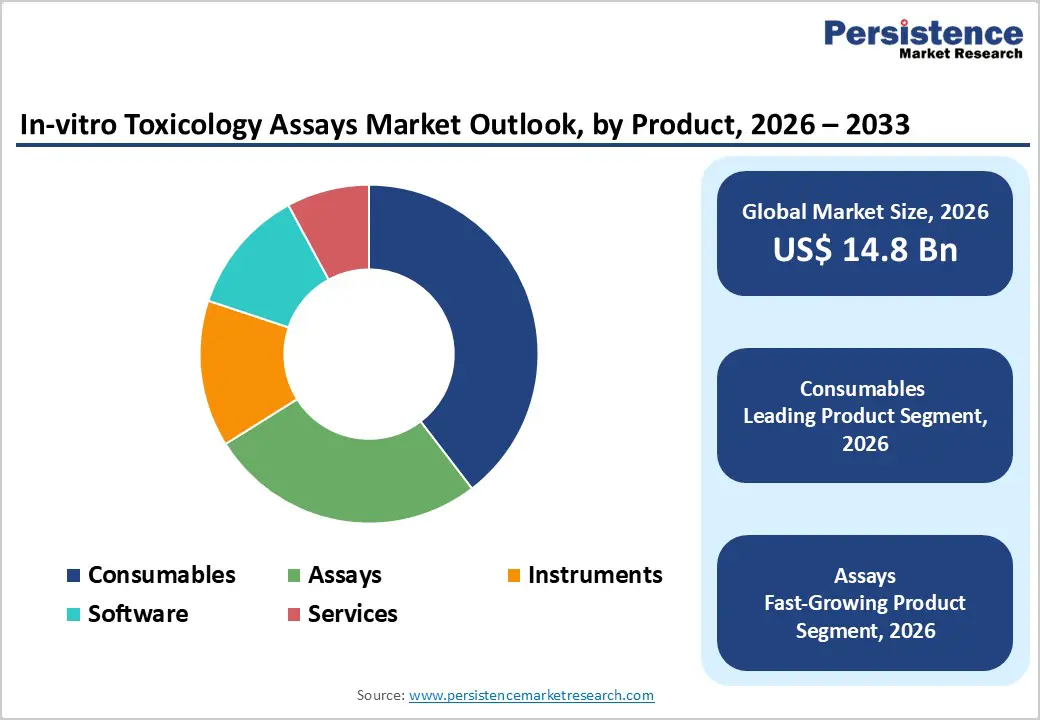

- Leading Product Segment: Consumables dominate the market due to their recurring use, cost efficiency, and essential role in routine cytotoxicity, genotoxicity, and organ-specific toxicity testing.

- Fastest-Growing Product Segment: Assays are witnessing rapid growth as their application expands across high-throughput screening, mechanistic toxicology, and regulatory safety evaluation.

- Leading Application Segment: Cell culture technology remains the largest application segment due to widespread adoption in preclinical safety testing and regulatory acceptance.

- Fastest-Growing Application Segment: Molecular imaging technology is expanding rapidly as demand increases for mechanistic insights and enhanced toxicity prediction accuracy.

| Key Insights | Details |

|---|---|

| In-vitro Toxicology Assays Market Size (2026E) | US$ 14.8 Bn |

| Market Value Forecast (2033F) | US$ 24.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Dynamics

Driver – Increasing Regulatory Pressure to Reduce Animal Testing and Rising Preclinical Safety Requirements Driving Market Growth

The growing global emphasis on reducing, refining, and replacing animal testing is a major driver of growth in the in-vitro toxicology assays market. Regulatory authorities across North America, Europe, and parts of Asia are increasingly mandating or encouraging the use of validated in-vitro methods for safety evaluation of pharmaceuticals, chemicals, cosmetics, and industrial substances. Frameworks such as EU REACH, the EU Cosmetics Regulation, and evolving FDA guidance are accelerating the transition toward alternative testing approaches.

Additionally, the expansion of pharmaceutical and biotechnology pipelines is increasing demand for early-stage toxicity screening to identify safety liabilities before costly animal studies or clinical trials. In-vitro assays enable rapid, cost-effective, and ethically compliant toxicity assessment, supporting better decision-making during lead optimization and candidate selection. Technological advancements including high-throughput screening, 3D cell culture systems, and mechanistic toxicity models are further enhancing predictive accuracy and translational relevance. Growing chemical production, environmental safety monitoring, and medical device testing requirements also contribute to rising assay adoption. Together, regulatory alignment, ethical considerations, and the need for efficient preclinical safety evaluation are driving sustained global demand for in-vitro toxicology assays.

Restraints – High Validation Costs, Limited Standardization, and Variable Regulatory Acceptance Constraining Adoption

The in-vitro toxicology assays market faces several restraints related to cost, complexity, and regulatory variability. Advanced in-vitro platforms such as organ-on-chip systems, OMICS-based assays, and 3D tissue models often require significant upfront investment in equipment, skilled personnel, and assay development, limiting adoption among smaller laboratories and institutions in cost-sensitive regions. Additionally, validation and standardization of novel assays can be time-consuming and resource-intensive, particularly when aligning results with regulatory expectations across multiple jurisdictions. Inconsistent regulatory acceptance of newer in-vitro models, especially for systemic and long-term toxicity endpoints, can discourage widespread implementation.

Data interpretation challenges, lack of universally accepted reference standards, and variability in assay reproducibility further complicate adoption. In emerging markets, limited technical expertise, underdeveloped laboratory infrastructure, and lower awareness of alternative testing methods continue to restrict penetration. While in-vitro assays offer long-term efficiency benefits, these economic, technical, and regulatory barriers may slow near-term market expansion, particularly outside well established pharmaceutical and research hubs.

Opportunity – Advancements in Predictive Toxicology, High-Throughput Platforms, and Emerging Market Expansion Creating New Growth Avenues

Significant growth opportunities exist in the integration of advanced predictive toxicology tools and expansion into emerging markets. Rapid progress in 3D cell culture, organ-on-chip technologies, and OMICS-based assays is improving the physiological relevance and predictive power of in-vitro toxicology models. These innovations enable more accurate assessment of complex toxicity mechanisms, supporting broader regulatory acceptance and increased use in later-stage safety evaluation. High-throughput and automated screening platforms present additional opportunities by enabling faster compound evaluation, reducing development timelines, and supporting large-scale chemical and drug screening programs.

The increasing use of artificial intelligence and data analytics to interpret complex toxicological datasets is further enhancing assay value. Emerging markets in Asia Pacific and Latin America offer strong long-term growth potential due to expanding pharmaceutical manufacturing, rising regulatory alignment with global standards, and increasing investment in research infrastructure. Growth of contract research organizations, public–private collaborations, and outsourcing of preclinical testing is improving access to in-vitro toxicology services. Collectively, technological innovation, digital integration, and geographic expansion are expected to unlock substantial new opportunities across the global market.

Category-wise Analysis

By Product, Consumables Dominate Due to High Usage Frequency and Recurring Demand

The consumables segment is projected to dominate the global in-vitro toxicology assays market in 2026, accounting for a revenue share of 39.6%. Segment leadership is driven by the recurrent and high-volume use of reagents, culture media, antibodies, plates, probes, and assay kits across routine toxicological testing workflows. Consumables are essential for cytotoxicity, genotoxicity, organ toxicity, and dose-response studies conducted during early-stage drug discovery, chemical screening, and regulatory safety assessment. Unlike instruments, consumables require frequent replenishment, generating consistent revenue streams for suppliers. Their widespread adoption across pharmaceutical, biotechnology, academic, and contract research laboratories further reinforces dominance. Increasing regulatory pressure to reduce animal testing and the growing shift toward cell-based and high-throughput in-vitro assays continue to elevate consumable demand. Continuous innovation in assay reagents, ready-to-use kits, and standardized testing formats is improving reproducibility and efficiency, supporting sustained market leadership of this segment.

By Application, Systemic Toxicology Leads Due to Broad Safety Assessment Requirements

The systemic toxicology segment is projected to dominate the global in-vitro toxicology assays market in 2026, accounting for a revenue share of 41.2%. This dominance is attributed to the critical role of systemic toxicity testing in evaluating whole-body exposure risks associated with pharmaceuticals, chemicals, cosmetics, and environmental compounds. Regulatory agencies require comprehensive systemic safety data to assess potential toxic effects across multiple organs and biological systems before clinical or commercial approval. Growing emphasis on early-stage risk identification, dose optimization, and toxicity screening during preclinical development is accelerating adoption. The increasing complexity of drug formulations, biologics, and novel chemical entities further drives demand for predictive systemic assays. Advances in cell culture models, 3D systems, and organ-relevant in-vitro platforms are enhancing translational relevance, enabling more accurate systemic toxicity evaluation. These factors collectively support sustained dominance of the systemic toxicology application segment.

By End-user, Pharmaceutical and Biotechnology Companies Lead Driven by R&D Intensity

The pharmaceutical and biotechnology companies segment is projected to dominate the global in-vitro toxicology assays market in 2026, accounting for a revenue share of 48.4%. Leadership is driven by high R&D intensity, extensive preclinical testing requirements, and growing drug development pipelines across small molecules, biologics, and advanced therapies. These companies rely heavily on in-vitro toxicology assays to screen lead compounds, assess safety profiles, reduce late-stage failures, and comply with global regulatory expectations. Increasing adoption of non-animal testing approaches and integrated safety assessment strategies further strengthens demand. Pharmaceutical and biotechnology firms also invest significantly in advanced assay platforms, high-throughput screening systems, and mechanistic toxicity studies to improve predictive accuracy and development efficiency. While academic institutes and diagnostic laboratories contribute to market growth, pharma and biotech companies remain the primary revenue drivers due to their scale, testing frequency, and long-term reliance on in-vitro toxicology solutions.

Region-wise Insights

North America In-vitro Toxicology Assays Market Trends

The North America in-vitro toxicology assays market is expected to dominate globally with a value share of 48.5% in 2026, led primarily by the U.S. The region benefits from a strong pharmaceutical and biotechnology ecosystem, advanced laboratory infrastructure, and high adoption of alternative testing methodologies. Stringent regulatory requirements from agencies such as the FDA and EPA are accelerating the shift toward validated in-vitro assays for safety evaluation. High R&D spending, robust preclinical pipelines, and early adoption of advanced technologies such as high-throughput screening, 3D cell culture, and organ-on-chip platforms further support market leadership.

North America also demonstrates strong collaboration between industry, academia, and contract research organizations, enabling rapid technology translation and assay standardization. The presence of leading assay developers and service providers, combined with strong funding support and regulatory clarity, continues to reinforce sustained regional dominance across pharmaceutical, chemical, and environmental toxicology applications.

Europe In-vitro Toxicology Assays Market Trends

The Europe in-vitro toxicology assays market is expected to grow steadily, supported by strict regulatory frameworks and a strong emphasis on reducing animal testing. Regulations such as REACH and the EU Cosmetics Regulation have significantly increased reliance on in-vitro methods for chemical and cosmetic safety assessment. Countries including Germany, the U.K., France, Italy, and the Nordic region are key contributors due to well-established research infrastructure and active pharmaceutical development.

European healthcare and regulatory systems strongly favor cost-effective, ethically compliant, and scientifically validated testing approaches, accelerating adoption of cell-based and mechanistic assays. Growing investments in academic research, public-private collaborations, and contract research services further expand market penetration. Additionally, regional focus on assay standardization, data reliability, and regulatory acceptance supports long-term growth. Continued innovation in OMICS-based toxicology and advanced cell models is expected to sustain market expansion across Europe.

Asia Pacific In-vitro Toxicology Assays Market Trends

The Asia Pacific in-vitro toxicology assays market is expected to register a relatively higher CAGR of around 7.9% between 2026 and 2033, driven by expanding pharmaceutical manufacturing, increasing regulatory awareness, and rapid healthcare infrastructure development. Countries such as China, India, Japan, South Korea, and Southeast Asian nations are witnessing rising demand for preclinical safety testing due to growing drug development activity and chemical production. Increasing government investments in research infrastructure, regulatory modernization, and alternative testing frameworks are accelerating adoption. The region is also benefiting from cost-effective laboratory operations, expanding CRO presence, and rising participation in global clinical and preclinical studies.

Growing awareness of animal welfare, alignment with international regulatory standards, and increasing collaborations with multinational pharmaceutical companies are strengthening market momentum. These factors collectively position Asia Pacific as the fastest-growing regional market for in-vitro toxicology assays.

Market Competitive Landscape

The global in-vitro toxicology assays market is highly competitive, with key participation from companies such as Charles River Laboratories International, Inc., SGS S.A., Merck KGaA, Eurofins Scientific, and Abbott Laboratories. These players leverage broad assay and testing portfolios, strong relationships with pharmaceutical and chemical companies, advanced laboratory capabilities, and global operational networks.

Competitive strategies focus on expanding assay offerings, improving predictive accuracy, integrating high-throughput and advanced cell-based technologies, and supporting regulatory-compliant, animal free testing. Ongoing investments in assay validation, platform innovation, automation, and expansion into emerging markets continue to intensify competition and drive market evolution.

Key Industry Developments:

- In January 2026, M&G Investments (M&G) led a US$50 million Series C funding round for bit.bio, a Cambridge-based biotechnology company specializing in next-generation human cell programming technology. The funding supports the continued growth of the University of Cambridge spin-out and reflects strong investor confidence in its innovative platform and long-term potential to advance drug discovery and development in the UK.

Companies Covered in In-vitro Toxicology Assays Market

- Charles River Laboratories International, Inc.

- SGS S.A.

- Merck KGaA

- Eurofins Scientific

- Abbott Laboratories

- Laboratory Corporation of America Holdings

- Evotec S.E.

- Thermo Fisher Scientific, Inc.

- Quest Diagnostics Incorporated

- Agilent Technologies, Inc.

- Catalent, Inc.

- Danaher Corporation

- Bio-Rad Laboratories, Inc.

- BioIVT

- Gentronix

- Others

Frequently Asked Questions

The global in-vitro toxicology assays market is projected to be valued at US$ 14.8 Bn in 2026.

Stringent regulatory mandates to reduce or replace animal testing combined with rising pharmaceutical and chemical safety assessment needs and technological advancements in in-vitro platforms drive market growth.

The global in-vitro toxicology assays market is poised to witness a CAGR of 5.9% between 2026 and 2033

Significant opportunities exist in emerging markets, expansion into new application sectors (e.g., food and medical devices), and commercialization of advanced technologies such as AI-integrated assays and organ-on-chip platforms.

Charles River Laboratories International, Inc., SGS S.A., Merck KGaA, Eurofins Scientific, and Abbott Laboratories are some of the key players in the in-vitro toxicology assays market.