- HVAC

- Thermostatic Mixing Valves Market

Thermostatic Mixing Valves Market Size, Share, and Growth Forecast, 2025 - 2032

Thermostatic Mixing Valves Market by Nominal Diameter (DN 15 Valves, DN 20 Valves, DN 25 Valves), Capacity (Up to 5 GPM, 5-10 GPM, 10-15 GPM), Valve Type (Emergency, High/Low, Point-of-Use, Standard), and Regional Analysis for 2025 - 2032

Thermostatic Mixing Valves Market Size and Share Analysis

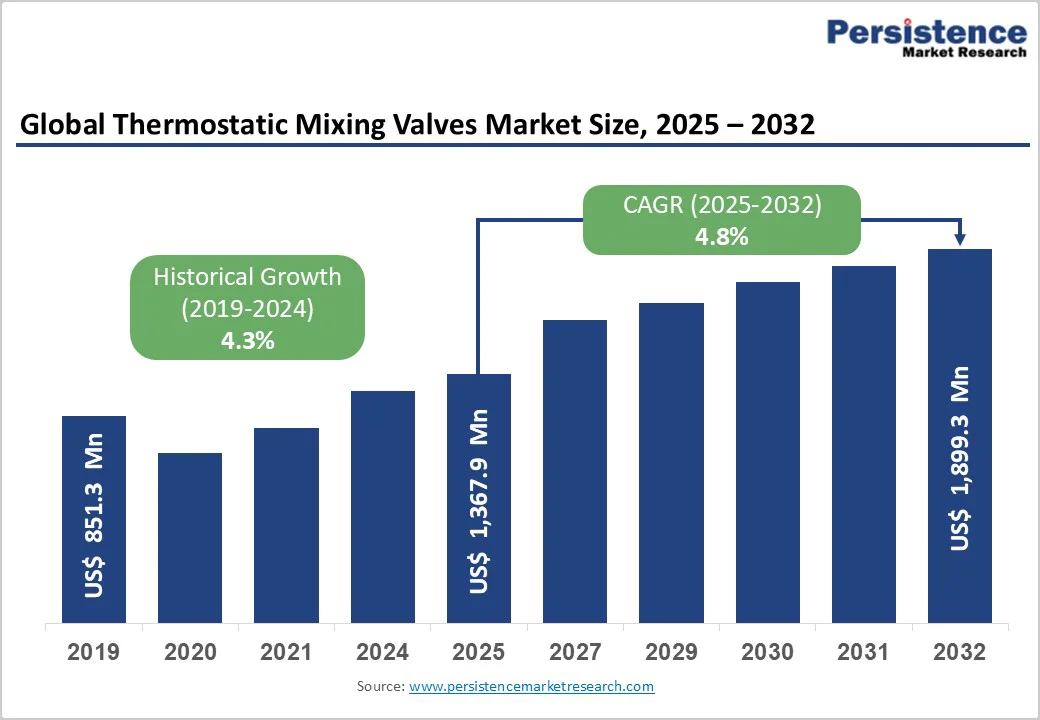

The global thermostatic mixing valves market size is likely to be valued at US$ 1,367.9 million in 2025, and is projected to reach US$ 1,899.3 million by 2032, growing at a CAGR of 4.8% during the forecast period 2025 - 2032.

This robust expansion is underpinned by increasingly stringent building codes and safety standards that mandate the installation of temperature control devices in both residential and commercial plumbing systems, significantly driving demand. The surge in construction activities across emerging economies also fuels market growth as new infrastructure projects prioritize the integration of modern water safety solutions.

Growing public health awareness, especially concerning the risk of Legionella bacteria in water systems, further encourages the adoption of thermostatic mixing valves to maintain safe water temperatures, reduce scalding risks, and enhance overall water system hygiene across various end-use sectors.

Key Industry Highlights

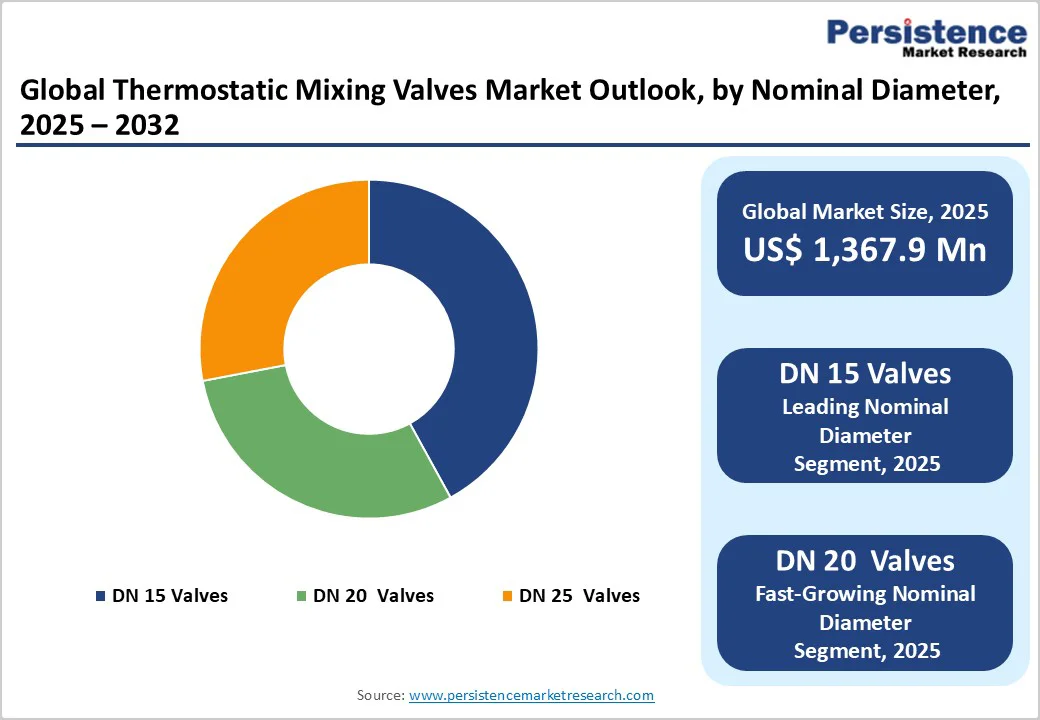

- Leading Size Segment: DN 15 valves dominate with a 42.4% share in 2025, driven by extensive utilization in residential applications.

- Flow Capacity Leadership: The up to 5 GPM capacity segment leads the market with a 39.2% share, primarily serving residential applications where efficiency and precise temperature control are critical.

- Product Type Dynamics: Point-of-use valves command approximately 35.1% of market share due to their reliability and ease of installation, while thermostatic valves are expanding rapidly at a 4.8% CAGR, driven by their rising adoption in centralized systems.

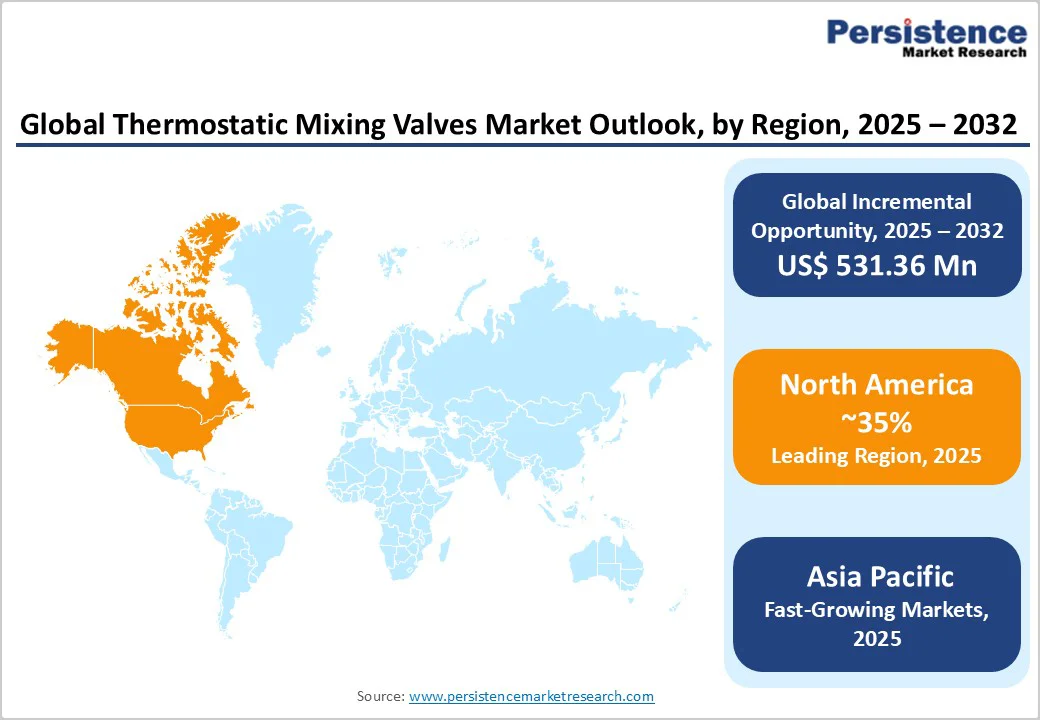

- Regional Leadership: North America leads the global market, with the United States contributing over 75% of regional revenue, supported by strong plumbing standards and early smart home technology adoption.

- Technological Advancement: Digital thermostatic mixing valves with IoT capabilities are emerging as a premium segment, offering remote monitoring, predictive maintenance, and building automation system (BAS) integration.

| Key Insights | Details |

|---|---|

| Thermostatic Mixing Valves Market Size (2025E) | US$ 1,367.9 Mn |

| Projected Market Value (2032F) | US$ 1,899.3 Mn |

| Global Market Growth Rate (CAGR 2025 to 2032) | 4.8% |

| Historical Market Growth Rate (CAGR 2019 to 2023) | 4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Stringent Safety Regulations and Anti-Scalding Mandates

Government regulations mandating the installation of thermostatic mixing valves (TMVs) in public, healthcare, and commercial facilities are a major catalyst for market growth. These regulations are designed to protect vulnerable populations, such as children, the elderly, and people with limited mobility, by implementing strict water safety standards and temperature limits to prevent scalding injuries.

Countries such as the UK and the US have established standards such as TMV3, ASSE 1016, and ASSE 1070, and compliance failures have led to significant penalties for care facilities, reinforcing the importance of adherence. As a result, the demand for TMVs is steadily expanding across hospitals, educational institutions, nursing homes, hotels, and public buildings, ensuring a stable market irrespective of economic cycles.

In addition to the above, rapid urbanization and infrastructure investment are fueling market expansion globally. Rising construction activity in both developed and emerging markets, especially in Asia Pacific, is accelerating the integration of modern plumbing solutions such as TMVs into new residential and commercial developments.

Renovation and retrofit projects in older buildings across North America and Europe also present substantial opportunities as these markets update existing infrastructure to meet current safety codes. The residential sector is a key demand source in North America, reinforced by the spread of smart home technology and heightened consumer awareness of water safety.

High Initial Installation and Maintenance Costs

The relatively high capital expenditure for TMV procurement and professional installation poses a significant barrier, particularly in cost-sensitive developing markets. Installation demands skilled technicians, specialized equipment, and compliance testing, which increase project costs. Advanced commercial-grade TMVs with features such as digital controls and antimicrobial coatings also carry premium prices that may limit adoption.

Ongoing maintenance, including regular calibration, part replacement, and servicing every 12 months in healthcare settings, further adds to lifecycle expenses. Retrofit projects often encounter compatibility issues with existing plumbing, requiring modifications and additional equipment, escalating overall costs beyond initial projections.

Limited awareness of TMV safety benefits and regulatory requirements in emerging economies hinders market penetration. Many residential consumers and small commercial property owners in Asia Pacific, Latin America, and Africa are unfamiliar with anti-scalding technologies and do not perceive TMVs as essential.

Educational gaps around Legionella prevention and water temperature management reduce urgency for adoption. Restricted distribution channels in rural or semi-urban areas also limit product availability and access to qualified installers. Weak or fragmented regulatory enforcement and absence of mandatory building codes also allow conventional mixing methods to persist, slowing TMV adoption despite associated health risks.

Smart Building Integration and IoT-Enabled Thermostatic Mixing Valves

Digital transformation is producing substantial growth opportunities in the thermostatic mixing valve market, with advanced smart valves featuring IoT connectivity, remote temperature monitoring, and predictive maintenance gaining widespread adoption in commercial and institutional facilities.

Smart TMVs such as Watts’ e-ULTRAMIX® system enable electronic temperature adjustment, automatic thermal disinfection cycles, and real-time data logging accessible via building automation systems through MODBUS protocol. These digital valves offer superior temperature stability, resulting in enhanced performance and energy efficiency.

Facility managers benefit from remote temperature control via smartphone apps, multi-channel safety alerts, and programmable temperature setback schedules, enhancing operational safety and reducing energy consumption. The integration of AI and machine learning to enable predictive analytics represents a premium and rapidly evolving segment in TMV technology.

The healthcare and institutional sectors are major growth drivers for smart TMVs, with modernization efforts aimed at improving patient safety and infection control. Hospitals, nursing homes, and eldercare facilities require TMVs that meet stringent safety standards to protect vulnerable populations while effectively managing water temperatures to prevent Legionella growth.

The aging global population has increased demand for TMVs compliant with NHS specification D08 and similar regulatory frameworks. Educational institutions, government buildings, and public facilities also face mounting regulatory pressure to adopt anti-scald devices across washrooms and common areas.

Category-wise Analysis

Nominal Diameter Insights

DN 15 TMVs dominate the market with a roughly 45% share, largely due to their extensive use in residential settings and small commercial installations. Their compact size, cost-effectiveness, and versatility make them ideal for sinks, showers, and bathroom fixtures with flow rates up to 5 GPM. These valves offer various connection options such as compression, threaded, or push-fit, and are widely trusted across homes, healthcare facilities, and hospitality point-of-use applications.

At the same time, DN 20 valves are likely to be the fastest-growing segment, driven by rising commercial construction and group installations requiring higher flow rates of 5-15 GPM. Commonly found in hotels, gyms, and healthcare facilities, DN 20 valves provide stable temperature control for multiple users simultaneously.

Their growth is further accelerated by retrofit projects and technological improvements such as faster thermostatic response and improved resistance to scale buildup, positioning this segment strongly for continued expansion in commercial and institutional markets.

Capacity Insights

Thermostatic mixing valves with capacities up to 5 GPM hold around 39.2% market share, primarily aided by their widespread utilization in bathrooms and kitchens across the residential sector. These valves are ideal for single-user fixtures such as showers, faucets, and sinks, and their compact design and affordability make them popular for under-sink installations and small renovation projects.

They also fulfill point-of-use needs in commercial spaces requiring localized temperature control, aligning with water conservation standards in many regions.

In contrast, the 10-15 GPM capacity segment is the fastest growing, fueled by a huge demand from commercial and institutional applications such as gyms, hospitals, industrial sites, and commercial kitchens.

These valves are valued for their ability to maintain stable water temperatures for multiple users and emergency fixtures, with advanced models achieving precise temperature control within ±2°F. This capacity range is increasingly preferred in environments requiring higher safety and efficiency performance standards, supporting robust expansion in commercial and healthcare markets.

Valve Type Insights

Point-of-use thermostatic mixing valves dominate the market with a share of around 35% in 2025, favored for their versatility and ease of installation across residential, commercial, and institutional settings.

Installed at individual fixtures such as sinks, showers, and bathtubs, they provide instant temperature control and effective anti-scald protection. These valves are especially popular in residential bathrooms and healthcare facilities due to their suitability for retrofits, compact design, and safety-enhancing features such as integrated check valves and strainers.

On the other hand, standard thermostatic mixing valves represent the fastest-growing segment, expanding at a 2025 - 2032 CAGR of about 4.8%, boosted by their increasing deployment in commercial buildings and centralized hot water systems.

They integrate seamlessly with building management systems (BMS) and digital controls, enabling programmable temperature management and enhanced energy efficiency. This smart integration makes them a key component in modern, smart building infrastructure, supporting their demand in large-scale commercial and institutional projects.

Regional Insights

North America Thermostatic Mixing Valves Market Trends

North America holds a significant portion of the thermostatic mixing valves market share. The United States dominates this regional market, accounting for about 75% of regional revenue, driven by stringent safety standards such as ASSE 1016, 1017, and 1070, which mandate the use of anti-scald valves across residential, commercial, and institutional buildings.

The U.S. residential construction sector, responsible for nearly 50% of TMV consumption, along with expanding smart home adoption, underpins resilient demand. Major urban centers such as New York, Los Angeles, Chicago, and Houston contribute significantly to commercial sector growth, fueled by infrastructure development in hotels, offices, and mixed-use projects.

Canada represents the fastest-growing market in North America, supported by considerable growth in its HVAC sector and residential development initiatives. The market here benefits from an innovation ecosystem that advances IoT-enabled thermostatic valves, integration with building automation systems, and predictive maintenance capabilities.

Ongoing infrastructure rehabilitation and strategic acquisitions by leading players such as Watts Water Technologies and Zurn Industries enhance market consolidation and competition. The adoption of advanced digital and smart TMVs is increasing, reflecting the country’s commitment to energy efficiency, safety, and modernization across residential and commercial segments.

Europe Thermostatic Mixing Valves Market Trends

Europe is a key region for the TMV market, owing to the strong regulatory frameworks related to construction and water quality of the European Union (EU), infrastructure upgrades, and emphasis on water safety in healthcare and social care environments.

The United Kingdom leads with over 30% of the regional market revenue, propelled by TMV2 and TMV3 certification mandates under National Health Services (NHS) guidelines for hospitals, care homes, and public buildings. Germany is an instrumental market, supported by dynamic construction, strict plumbing standards, and energy-efficient building practices.

Renovation projects in France, Spain, Italy, and stringent anti-scald regulations in Scandinavian countries further boost demand.

EU-wide regulatory harmonization facilitates standardized product specifications and cross-border trade, benefiting manufacturers with strong local distribution such as Watts, Caleffi, Danfoss, and Pegler Yorkshire. The market favors premium thermostatic mixing valves featuring digital controls, antimicrobial coatings, and advanced materials.

Green building initiatives, retrofit demand in historic buildings, and energy efficiency directives continue to fuel adoption. Emphasis on quality certifications, warranties, and technical support underscores Europe’s commitment to high safety and performance standards in TMV applications.

Asia Pacific Thermostatic Mixing Valves Market Trends

The Asia Pacific thermostatic mixing valves market is the fastest-growing globally, driven by rapid urbanization, infrastructure development, and rising incomes across China, India, and ASEAN countries. China leads the market, growing at an impressive 16.7% CAGR, bolstered by extensive urban housing projects, industrial growth, and government modernization initiatives.

Market expansion in India is fueled by government programs such as the Smart Cities Mission and Pradhan Mantri Awas Yojana, alongside strong commercial real estate growth. In Japan, market growth is attributable to the steady replacement demand due to aging infrastructure and tourism-related hotel upgrades.

The region’s role as a global manufacturing hub with cost advantages and integrated supply chains has further enhanced its competitiveness. Growing consumer awareness of water safety, evolving regulatory standards, and the demand for premium products also support sustained market momentum.

This dynamic growth in Asia Pacific reflects increasing adoption of advanced thermostatic and digital mixing valves that offer precise temperature control and energy efficiency, aligning with global sustainability trends. Manufacturers in the region are investing in quality improvements, international certifications, and technological innovations to meet rising expectations and compete with established Western brands.

The convergence of rapid urban development, regulatory support, rising affluence, and manufacturing excellence positions Asia Pacific as a crucial market driving the future expansion of the thermostatic mixing valve industry worldwide.

Competitive Landscape

The global thermostatic mixing valves market landscape is shaped by the increasing regulatory emphasis on water safety and anti-scald protection across residential, commercial, and healthcare sectors.

Governments worldwide are enforcing stricter building codes and hygiene standards, compelling widespread TMV adoption and favoring top manufacturers, such Watts Water and Danfoss, capable of delivering compliant, innovative solutions. The integration of TMVs with smart building management systems is further transforming product offerings, enabling enhanced temperature precision, energy efficiency, and remote monitoring capabilities.

Competitive consolidation is underway with leading global players focusing on strategic partnerships, acquisitions, and geographic expansion to capture scale economies and broaden market reach. Regional specialists and niche players continue to innovate for specific applications, intensifying competition and driving product diversification.

As the market evolves, success increasingly depends on technological leadership, regulatory alignment, comprehensive service offerings, and flexible solutions tailored to diverse end-user requirements.

Key Industry Developments

- In November 2025, A. O. Smith announced the acquisition of Leonard Valve Company for US$ 470 million, representing a strategic expansion into the fast-growing digital and thermostatic mixing valve market for commercial and institutional applications. The acquisition combines Leonard Valve's advanced water management technologies, including digital mixing valves and the Heat-Timer boiler control platform, with A. O. Smith's core water heating and boiler offerings to create an integrated smart water building management solution.

- In November 2025, Watts Water Technologies Inc. completed the acquisition of Superior Boiler, a leading manufacturer of customized steam and hot water boilers for commercial, institutional, and industrial applications, with annual sales around US$ 60 million. The addition of Superior’s mission-critical heating solutions complements Watts’ portfolio, supporting its commitment to innovation, customer service, and long-term success in heating and water quality markets.

- In October 2025, Toolstation rolled out its new own-brand heating and plumbing range called Flume, featuring stylish, high-performance towel radiators and complementary valve accessories. The Flume collection includes various flat and ladder radiators, reliable thermostatic radiator valves (TRVs), lockshield valves, system inhibitors, and brass shank fill valves, all designed to deliver quality, ease of installation, and coordinated aesthetics.

Companies Covered in Thermostatic Mixing Valves Market

- Reliance Worldwide Corporation

- MISUMI Group Inc

- Honeywell International Inc

- Watts Water Technologies Company

- Danfoss A/S

- Bradley Corporation

- Armstrong International Inc.

- Caleffi S.p.A

- Afriso-Euro-Index GmbH

- Pegler Yorkshire

- ESBE Group

- Hans Sasserath GmbH & Co. KG

- Bianchi F.lli S.P.A

Frequently Asked Questions

The global thermostatic mixing valves market is projected to reach US$ 1,367.9 million in 2025.

The growing emphasis on water safety, energy efficiency, and temperature control in residential, commercial, and healthcare facilities is primarily driving the market.

The market is poised to witness a CAGR of 4.8% from 2025 to 2032.

Increasingly stringent building codes and safety standards that mandate the installation of temperature control devices in plumbing systems, the surge in construction activities across emerging economies, and growing public health awareness, especially concerning the risk of Legionella bacteria in water systems, are key market opportunities.

Reliance Worldwide Corporation, MISUMI Group, Honeywell International, and Danfoss A/S are some of the key players in the market.