- Electrical Equipment & Services

- Synchrophasor Market

Synchrophasor Market Size, Share, and Growth Forecast 2026 - 2033

Synchrophasor Market by Component type (Phasor Measurement Unit (PMU), Phasor Data Concentrator and Others), by Application (Monitoring and Analysis, Control and Offline Applications), and Regional Analysis for 2026 - 2033

Market Overview

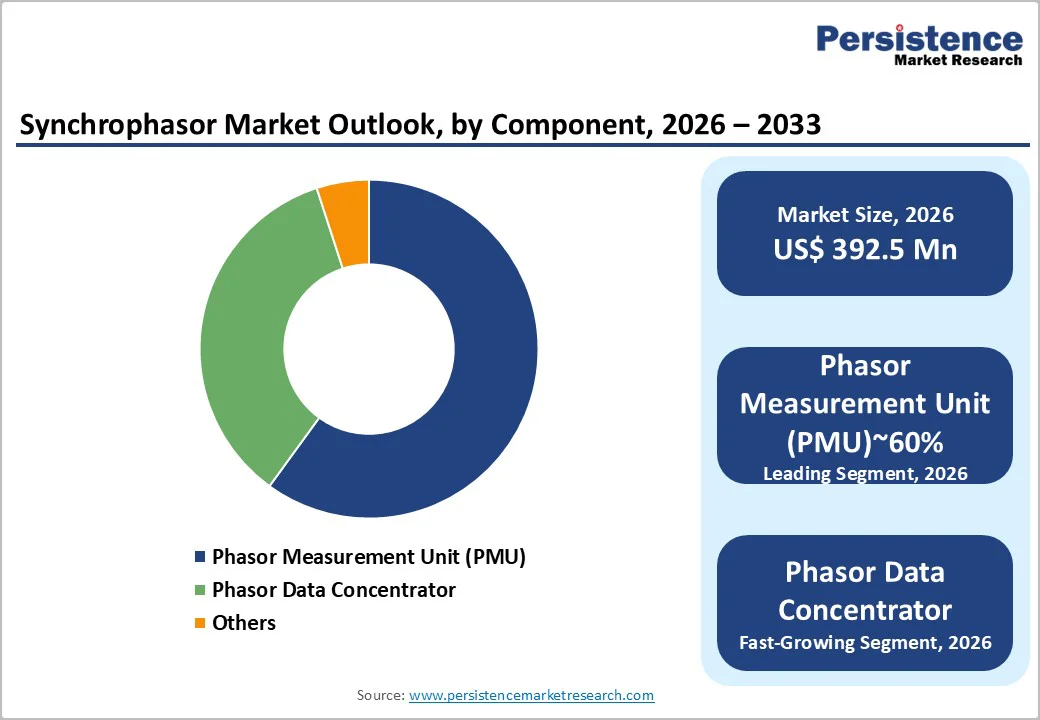

The global Synchrophasor market size was valued at US$ 392.5 Mn in 2026 and is projected to reach US$ 846.3 Mn by 2033, growing at a CAGR of 11.6% between 2026 and 2033. The synchrophasor market is experiencing accelerated expansion driven by comprehensive smart grid modernization initiatives across developed and emerging economies, regulatory mandates requiring real-time grid monitoring for enhanced stability, and escalating deployment of renewable energy sources demanding advanced synchronization technologies.

Key Market Highlights

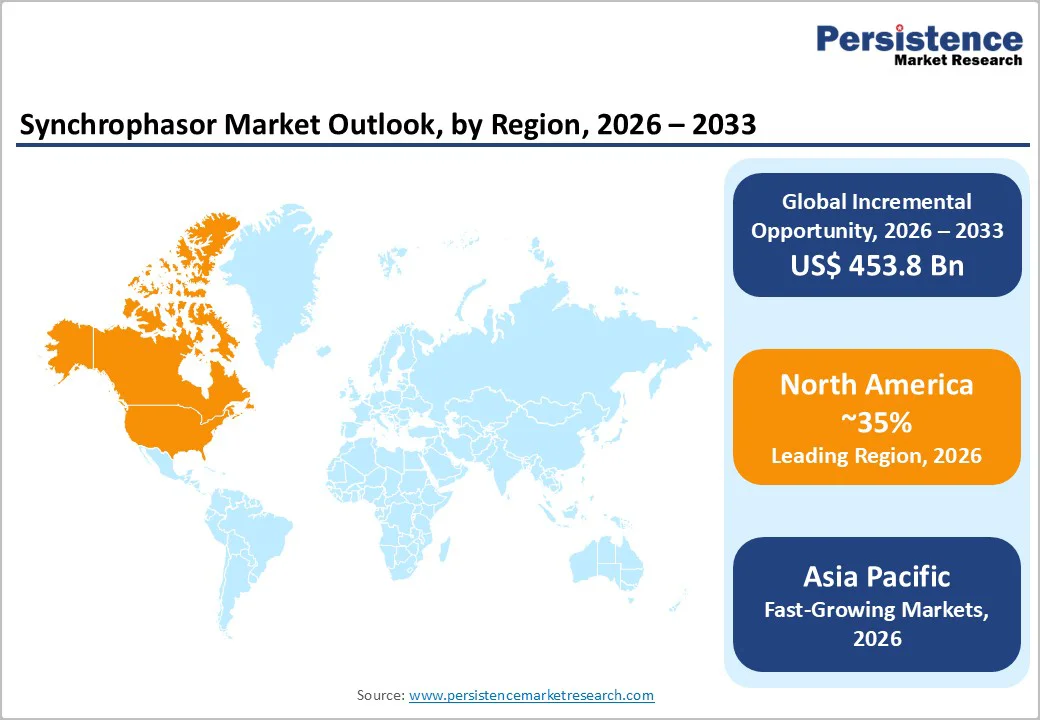

- North America Market Dominance: North America commands 47.7% global synchrophasor market share, supported by established regulatory framework (FERC/NERC mandates), advanced utility infrastructure, and substantial government investment through Department of Energy Smart Grid programs supporting sustained market expansion.

- Asia-Pacific Fastest Growth Region: Asia-Pacific expands at 8.5% CAGR, led by China's ultra-high-voltage transmission network expansion (6.8% CAGR) and India's URTDSM project planning 1,700-2,000 PMU deployments, establishing region as primary growth driver through 2033.

- Monitoring and Analysis Applications Dominance: Monitoring and Analysis applications command 45% market share, providing foundational grid visibility supporting operational decision-making, with stability monitoring representing single largest application reflecting universal utility requirement for real-time frequency and voltage assessment.

- Control Applications Fastest Growing Segment: Control applications expand at 150% higher growth rates versus monitoring, driven by increasing synchrophasor-based automated control system deployment achieving 15% grid stability improvement compared to traditional remedial action schemes.

- Software and Analytics Key Growth Opportunity: Software platforms and advanced analytics represent highest-growth market segment with 15% CAGR projection, driven by cloud-based platform adoption, machine learning integration, and artificial intelligence-powered grid optimization expanding from 20% to 35% of total synchrophasor market value by 2033.

| Global Market Attributes | Key Insights |

|---|---|

| Synchrophasor Market Size (2026E) | US$ 392.5 Mn |

| Market Value Forecast (2033F) | US$ 846.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 11.6% |

| Historical Market Growth (CAGR 2020 to 2024) | 8.5% |

Market Dynamics

Market Growth Drivers

Accelerating Smart Grid Modernization and Infrastructure Digitization Requirements

Global utilities are undertaking unprecedented smart grid modernization initiatives, with governments worldwide establishing binding timelines and regulatory frameworks mandating synchronous phasor technology deployment across transmission and distribution networks. The United States Department of Energy's Smart Grid Investment Grants (SGIG) program distributed over $3.5 billion in federal funding supporting synchrophasor system implementation across utility operators, establishing foundational deployments across major interconnections.

Smart grid infrastructure modernization addresses critical requirements including real-time situational awareness, advanced protection and control capabilities, improved system reliability, and enhanced operational efficiency in response to increasingly complex grid dynamics. PMUs provide synchronized voltage and current measurements at up to 200 samples per second, compared to SCADA systems delivering 2 second measurement intervals, enabling operators to detect and respond to grid disturbances with millisecond precision.

Growing Integration of Variable Renewable Energy Sources and Enhanced Grid Stability Requirements

Renewable energy integration, including wind and solar installations exceeding 4,000 GW globally by 2026, creates unprecedented grid stability challenges requiring advanced monitoring and control technologies. Variable generation patterns from wind turbines and photovoltaic systems, characterized by rapid output fluctuations due to cloud cover and wind speed variations, generate frequency and voltage instability necessitating real-time monitoring and corrective action. Synchrophasors enable Wide-Area Monitoring Systems (WAMS) providing synchronized measurements across geographically distributed locations, supporting dynamic stability assessment, oscillation monitoring, and voltage regulation essential for managing grids with high renewable energy penetration.

Restraints

High Capital Investment Requirements and Complex System Integration Challenges

Synchrophasor system deployment requires substantial capital investment, encompassing PMU hardware ($5,000-$50,000 per unit), Phasor Data Concentrators (PDCs), communication infrastructure (fiber optic networks), and advanced software platforms supporting real-time analytics. Total implementation costs for comprehensive WAMS across transmission systems exceed $50-200 million for large utilities, creating budget constraints particularly for smaller utilities and developing economy operators. System integration complexity, including communication network establishment, cybersecurity protocol implementation, and inter-vendor compatibility challenges, requires specialized engineering expertise and extends project timelines.

Cybersecurity Vulnerabilities and Regulatory Compliance Burden

Synchrophasor systems operate as critical infrastructure, creating exposure to cyber-attack risks potentially disrupting grid operations. NERC CIP (Critical Infrastructure Protection) compliance requirements establish mandatory security standards including access control, encryption, and incident response procedures, increasing operational burden and implementation complexity. Regulatory compliance uncertainty regarding data privacy, system authentication, and communication protocol standards creates implementation delays and cost escalation for utility operators.

Opportunities

Micro-PMU Deployment for Distribution Network Monitoring and Advanced Grid Analytics Integration

Micro-PMU technology, engineered for lower cost ($1,000-$5,000 per unit) and simplified deployment across distribution networks, represents the fastest-growing market segment with projected 13.2% CAGR through 2033. Distribution network operators seek real-time visibility for fault detection, islanding detection, and distributed energy resource (DER) integration, creating substantial addressable market expansion opportunity. Advanced analytics platforms integrating machine learning algorithms, artificial intelligence predictive capabilities, and cloud-based processing enable anomaly detection, equipment failure prediction, and optimization of power flows, supporting estimated 20% operational cost reduction for utility operators. Integration with Internet of Things sensors and digital twin technologies creates convergence opportunities enabling proactive asset management and predictive maintenance replacing reactive repair approaches.

Software-Defined Grid Architecture and Cloud-Based Synchrophasor Analytics Solutions

Software solutions addressing PMU data processing, real-time analytics, and grid visualization represent the highest-growth application segment with estimated 15% CAGR through 2033. Cloud-based platforms enabling scalable data storage, distributed processing capabilities, and global accessibility address infrastructure constraints limiting traditional centralized architectures. Scalable cloud-native architectures incorporating containerized microservices, elastic resource orchestration, and edge computing enable sub-second response times supporting critical grid protection functions. Market sizing analysis projects software and analytics segment expanding from current 20% to 35% of total synchrophasor market value by 2033.

Category-wise Insights

Component Type Analysis

Phasor Measurement Units (PMU) command dominant positioning within product segmentation, representing approximately 60% of synchrophasor market value and comprising the foundational technology element enabling all downstream applications. PMU hardware encompasses diverse form factors including relay-integrated units embedding synchrophasor functionality within protection relays, standalone PMU devices, power quality meters with synchrophasor capability, and advanced digital protective relays incorporating multi-parameter measurement functions.

PMU deployment concentration reflects widespread installation across transmission substations (400kV and above), generator stations, critical interconnection points, and increasingly across distribution networks (11-33kV levels) supporting emerging micro-PMU applications. Dominant positioning derives from universal requirement across all synchrophasor system deployments, with every WAMS implementation requiring multiple PMUs providing synchronized measurements at geographically distributed locations. Fastest-growing product segment comprises Software and Analytics platforms, with growth rates of double PMU hardware growth, reflecting transition from data collection emphasis toward intelligence extraction from massive synchrophasor datasets

Application Insights

Monitoring and Analysis applications command dominant positioning representing approximately 45% of synchrophasor deployment value, driven by foundational requirement for real-time grid visibility supporting operational decision-making. Monitoring applications encompass situational awareness provision, system state determination, disturbance detection, and stability assessment, with grid operators utilizing synchrophasor data streams supporting dynamic security assessment, transient stability evaluation, and small-signal stability analysis.

Stability monitoring represents the single largest application category, reflecting universal requirement across all grid operators for real-time frequency and voltage monitoring preventing cascading failures and widespread blackouts. However, Control applications represent the fastest-growing segment with growth rates 150% higher than monitoring applications, driven by increasing deployment of synchrophasor-based automated control systems including wide-area damping controllers (WADC), emergency voltage support systems, and frequency stabilization algorithms.

Regional Insights

North America

North America maintains dominant market positioning commanding approximately 34.7% of global synchrophasor market share, driven by established regulatory framework, advanced utility infrastructure, and substantial government investment supporting technology deployment. The United States, as primary market driver, implements FERC-approved reliability standards and NERC mandatory requirements establishing baseline synchrophasor deployment mandates across all registered entities operating critical bulk power system infrastructure.

U.S. market leadership reflects innovation ecosystem concentration supporting emerging technology development, with Schweitzer Engineering Laboratories (SEL), ABB, General Electric (GE Digital), and Siemens Energy maintaining substantial North American manufacturing and engineering operations. Government investment through Department of Energy Smart Grid demonstration projects and utility-led capital expenditures maintains steady 4.3% annual growth rate for North American synchrophasor market expansion.

Europe

Europe represents the second-largest global market with approximately 25% market share, characterized by ambitious decarbonization objectives, extensive renewable energy integration (reaching 50%+ in some countries), and stringent regulatory requirements for grid modernization. European Union regulatory framework including ENTSO-E (European Network of Transmission System Operators for Electricity) Compliance Network standards and member state-specific requirements drive synchrophasor deployment across transmission system operators (TSOs) including TenneT (Netherlands/Germany), RTE (France), and National Grid (UK).

Germany, as largest European market, implements aggressive renewable energy transition with wind and solar installations exceeding 50% of electricity generation requiring real-time grid monitoring and control through synchrophasor systems. European regulatory harmonization initiatives establish standardized technical specifications facilitating cross-border power trading and integrated grid operations requiring synchronized measurements across national boundaries. Growth rate of 5.3-5.8% CAGR reflects mature market penetration with established deployments requiring incremental expansion rather than foundational buildout.

Asia Pacific

Asia-Pacific emerges as fastest-growing regional market with 8.5% CAGR projection through 2033, driven by rapid electricity demand growth, massive transmission expansion, and renewable energy integration across developing economies. China, as dominant Asia-Pacific market, implements ultra-high-voltage (UHV) transmission network expansion (exceeding 200,000 circuit-kilometers) requiring advanced PMU deployment for synchronized measurement and control across State Grid Corporation's vast infrastructure. China's synchrophasor market growth at 6.8% CAGR reflects UHV network expansion momentum with thousands of PMU deployments supporting grid stability in increasingly complex interconnected systems.

India's grid modernization initiative, the Unified Real Time Dynamic State Measurement (URTDSM) scheme, represents largest single synchrophasor deployment project globally, with approximately 1,700-2,000 PMUs planned across transmission networks, coupled with 32 Phasor Data Concentrators (PDCs) supporting wide area monitoring capabilities. Indian deployment momentum, advancing through phased implementation, addresses critical grid stability challenges following 2012 blackout affecting 670 million people, establishing precedent for comprehensive synchrophasor system deployment across emerging market utility operators.

Competitive Landscape

Market Structure Analysis

The synchrophasor market demonstrates moderate consolidation with leading manufacturers including Schweitzer Engineering Laboratories (SEL), ABB, General Electric (GE Digital), and Siemens Energy commanding approximately 50-60% of global market share through comprehensive product portfolios, established distribution networks, and strong utility relationships. Specialty competitors including Omicron, Hitachi Energy, Schneider Electric, and regional manufacturers compete through technical differentiation, customized solutions, and localized support networks.

Market consolidation trend reflects increasing software value-capture with acquisition activity targeting analytics platforms and digital service providers. Customer integration deepens through extended service agreements, managed services, and subscription-based analytics platforms creating recurring revenue streams and customer switching barriers.

Key Market Developments

- In August 2026, GE Digital Expands Cloud-Native PMU Analytics Platform General Electric deployed enhanced cloud-based synchrophasor analytics platform supporting distributed edge processing, machine learning anomaly detection, and predictive maintenance enabling utility operators to optimize grid performance and asset management.

- In October 2024, Schweitzer Engineering Laboratories (SEL) Launches SEL-9 Series Relay Platform SEL introduced next-generation relay platform featuring enhanced synchrophasor processing, AI-based fault detection, and improved cybersecurity capabilities, representing technological advancement in embedded PMU functionality supporting utility modernization objectives.

Companies Covered in Synchrophasor Market

- Schweitzer Engineering Laboratories, Inc.

- Powerside

- Electro Industries GaugeTech

- GE Vernonva

- VIZIMAX

- Siemens

- WAMSTER

- Arbiter Systems

- NR Electric Co., Ltd.

- Hitachi Energy

- Others Key Players

Frequently Asked Questions

The global synchrophasor market is valued at approximately US$ 392.5 million in 2026 and is projected to reach US$ 846.3 million by 2033, representing 11.6% CAGR during the forecast period, driven by smart grid modernization.

Primary market drivers include smart grid modernization initiatives supported by global government investment, mandatory regulatory requirements from FERC and NERC establishing synchrophasor deployment mandates, renewable energy integration requirements generating grid stability challenges, and aging infrastructure replacement driving technology modernization cycles across utility operators.

Phasor Measurement Units (PMU) command dominant positioning representing 60% of synchrophasor market value, serving as foundational technology enabling all downstream applications.

North America maintains dominant market leadership commanding 34.7% of global synchrophasor market share, supported by established regulatory framework, advanced utility infrastructure, and substantial government investment, while Asia-Pacific emerges as fastest-growing region with 8.5% CAGR driven by China's UHV network expansion and India's URTDSM project deployment.

Market leaders include Schweitzer Engineering Laboratories (SEL), ABB Ltd., General Electric (GE Digital), and Siemens Energy.